Self managed superannuation funds and the bear market of 2007-2008

Full text

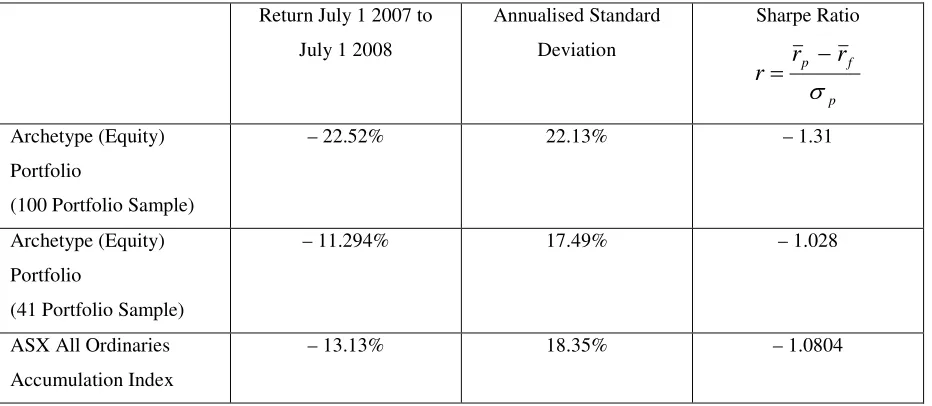

Figure

Related documents

• Follow up with your employer each reporting period to ensure your hours are reported on a regular basis?. • Discuss your progress with

* Corresponding author. E-mail address: paola.zappa1@unimib.it.. Controversial too are the empirical findings on the effectiveness of social learning, once contextual variables and

4.1 The Select Committee is asked to consider the proposed development of the Customer Service Function, the recommended service delivery option and the investment required8. It

innovation in payment systems, in particular the infrastructure used to operate payment systems, in the interests of service-users 3.. to ensure that payment systems

Marie Laure Suites (Self Catering) Self Catering 14 Mr. Richard Naya Mahe Belombre 2516591 info@marielauresuites.com 61 Metcalfe Villas Self Catering 6 Ms Loulou Metcalfe

National Conference on Technical Vocational Education, Training and Skills Development: A Roadmap for Empowerment (Dec. 2008): Ministry of Human Resource Development, Department

Standardization of herbal raw drugs include passport data of raw plant drugs, botanical authentification, microscopic & molecular examination, identification of