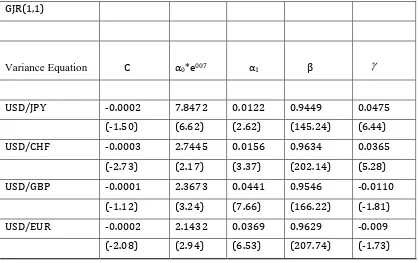

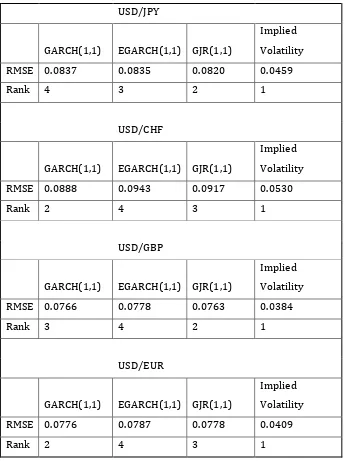

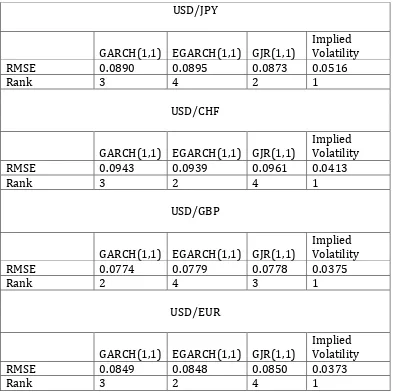

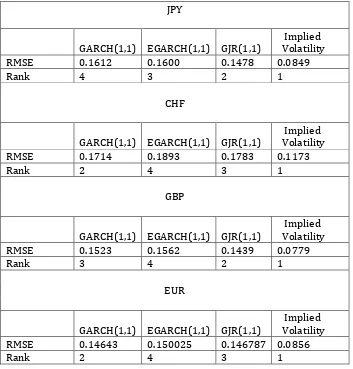

Forecasting exchange rate volatility: GARCH models versus implied volatility forecasts

Full text

Figure

Related documents

The University of Minnesota’s College of Design, which includes interior design, architecture, landscape architecture, graphic design and other programs, places a strong emphasis

Selama penelitian telah terjadi kematian yang cukup tinggi yang mengakibatkan terjadinya penurunan tingkat kelangsungan hidup benih ikan lele dumbo pada masing- masing

Methods and materials: A total of 1340 non-enhanced and enhanced planning computed tomography (CT) slices of eight OARs (the bladder, rectum, kidney, clavicle, humeral head,

It is recommended that a South African hate-crime law should criminalise conduct, particularly violent conduct that is motivated by the race, the ethnicity, the sexual

The aim of this paper is to explore student participation in institutional level decision making in the context of the creation of Ireland’s inaugural Technological University..

The challenges associated with designing a new novel solution to personalised learning will involve: overcoming the limitations of current systems; the development of a

prophylactic carpal tunnel release (CTR) in distal radius fractures without median nerve symptoms versus patients undergoing volar plating and found no difference in

In this paper, we position ULL as part of a broader shift in the nature of urban governance in which forms of innovation and experimentation are being