Journal of Politics and Law; Vol. 6, No. 4; 2013 ISSN 1913-9047 E-ISSN 1913-9055 Published by Canadian Center of Science and Education

108

Does Negotiating with Terrorists Make Them More Risk Seeking?

Peter J Phillips1 & Gabriela Pohl21 School of Accounting, Economics and Finance, University of Southern Queensland, Toowoomba, Queensland, Australia

2 Gabriela Pohl, School of Humanities and Communication, University of Southern Queensland, Toowoomba, Queensland

Correspondence: Peter J Phillips, School of Accounting, Economics and Finance, University of Southern Queensland, Toowoomba, Queensland 4350, Australia. Tel: 617-4631-5490. Email: [email protected]

Received: August 6, 2013 Accepted: August 30, 2013 Online Published: November 29, 2013 doi:10.5539/jpl.v6n4p108 URL: http://dx.doi.org/10.5539/jpl.v6n4p108

Abstract

We treat government concessions as additions to an expected payoffs schedule rather than as being synonymous with it. Government concessions that add to terrorists’ expected payoffs past some point on a positively sloped risk-reward trade-off schedule will not make all terrorists more risk seeking. Such concessions do not represent certain ‘windfall gains’ to terrorists of the kind that interact with relative and absolute risk aversion. Although the expected payoffs to higher risk actions may be augmented by the government’s concessions, terrorists must still bear risk in order to attain them. Terrorist groups that were unwilling to bear that risk before will not be enticed to bear it after expected payoffs are enhanced. Conversely, negative concessions or penalties will make terrorists more averse to risk because penalties alter the risk-reward trade-off in ways that make lower-risk actions more desirable to risk-averse terrorists. Our paper also explores the risk-reward characteristics of new and innovative terrorist actions relative to the structure of an existing expected payoffs schedule.

Keywords: terrorism, government policy, concessions, penalties, risk, innovation, Red Army Faction, 2nd of June Movement

1. Introduction

In a grainy black and white photograph taken in early 1975, a weary man stares obediently into the camera. The sign he is holding says in block capital lettering, “PETER LORENZ—GEFANGENER DER BEWEGUNG 2. JUNI.” (Note 1) Peter Lorenz was a German politician and mayoral candidate for West Berlin. He was kidnapped by the 2nd of June Movement a few days before the mayoral elections in February 1975. After five days, the German government agreed to grant several concessions to the terrorists on the condition that Lorenz be released unharmed. These concessions included the release of 5 prisoners, transport to Yemen, about 100,000 Deutschmark in cash and media coverage of the departing 707 from Frankfurt airport (Winkler, 2008, p.246). Upon receipt of these concessions, Lorenz was released. The conventional wisdom that terrorists should never be negotiated with was disregarded. It would, however, be reinstated in just a matter of weeks as the German government confronted another set of terrorist demands, this time from the Red Army Faction (RAF) who were holding twelve hostages in the German embassy in Stockholm.

109

conventional wisdom that concessions make terrorists more likely to engage in terrorist activity and, perhaps, to engage in riskier acts of terrorism.

The optimality of the ‘never negotiate’ policy was subjected to theoretical scrutiny by Lapan and Sandler (1988) but the analysis did not treat risk preferences explicitly. It is not uncommon for analytical work to leave risk preferences implicit and where risk preferences have been incorporated into the analysis, it has been usual to specify a particular type or level of risk preference, hold that specification constant, and explore the impact of government concessions in a comparative statics framework. Sandler, Tschirhart and Cauley’s (1983) analysis is an example (Note 2). These economic studies focus on hostage-taking or kidnapping scenarios where terrorists attempt to bargain with the government in order to extract concessions. The examples with which we opened the paper are typical. Risk preferences have been treated in a similar manner in the international relations literature where the focus has been on inter-group or international conflict. Risk preferences are specified and the solution, if any, to the bargaining problem is determined within the boundaries of that specification. An example is Powell’s (2002) analysis which represents an assessment of Rubinstein’s (1982) ‘standard model’ under conditions of risk neutrality. Powell’s analysis applies to scenarios where a ‘bargaining surplus’ may be divided in different proportions between the ‘players’.

Analytical solutions to a number of the problems that are explored in this and related literature are often more easily attainable when risk preferences are left to one side or where risk neutrality is assumed. This leaves open the possibility for obtaining additional results by exploring what happens when risk preferences are specified in different ways. Skaperdas (2006) operates first under the assumption of risk neutrality before exploring the implications of risk aversion. Related concepts that emerged with the publication and dissemination of Kahneman and Tversky’s (1979; 1992) presentation of prospect theory, especially their concept of loss aversion, have been inserted into bargaining theory. Butler (2007) is representative of modern studies that explore the implications of different psychological and strategic aspects of bargaining, including different treatments of risk preferences, in scenarios previously explored with less nuanced specifications of attitudes towards the risk and potential losses and potential gains. Butler (2007), for example, finds important qualifications to the types of conclusions that might be reached by approaching bargaining problems from an expected value maximisation perspective—Fearon’s (1995) model, for instance—rather than a prospect theoretical perspective (Note 3). We are focused on the following problem. Can government concessions or penalties shape terrorists’ preferences for risk? (Note 4) The setting for this problem is broader than the bargaining scenarios analysed in the papers listed above. The setting is a terrorism context where there are expected payoffs to terrorist actions, which include assassination, hijacking, bombing, hostage-taking and armed assaults. What these expected payoffs may be is still a matter for debate but they may include some or all of the following: the infliction of fatalities, the garnering of media coverage, the fostering of grassroots support, the formation of strategic links with other like-minded terrorist groups and so on (Abrahms 2006; 2008; 2011). We do not treat the concessions—ransoms, release of prisoners, changes of government policy and so forth—that might come from the government in response to an act of terrorism as the payoffs to terrorism. Rather, the government’s concessions or penalties schedule adds to or alters but does not replace an underlying expected payoffs schedule that is characterised by a particular trade-off between risk and reward.

www.ccsenet.org/jpl Journal of Politics and Law Vol. 6, No. 4; 2013

110

2. The Shape of Payoffs, Concessions and Penalties

Terrorists confront an expected payoffs schedule characterised by some, presumably positive, trade-off between risk and reward. Powell (2002) utilises a purely theoretical risk-reward trade-off. Phillips (2009) treats inflicted human tragedy measured by injuries and fatalities as the payoff to terrorism and sees a positive trade-off between risk and reward emerging empirically from the RAND-MIPT data as a concave set in expected-payoff-risk space. In dealing with bargaining scenarios it is easy to confuse a total payoffs schedule with the government’s concessions schedule. The two will only be synonymous if concessions are the only relevant payoffs to a terrorist action. Usually, though, there will be some payoffs that lie outside of the government’s control or its policy-making regimes. As mentioned in the introduction, these could be one or a combination of many different factors and some of them might be intangible or psychic in nature. A government’s concessions schedule may alter or add to the existing expected payoffs schedule but it is not synonymous with it and does not replace it. A payoffs schedule that incorporates all of the payoffs to terrorism, assuming they can all be measured (Note 5), would be multi-dimensional. We can imagine, however, that the payoffs schedule will be positively inclined in risk-reward space in order to encompass the positive trade-off between risk and reward that confronts terrorists. As Phillips (2009) has shown, different types of terrorist actions can be combined. When risk is measured by standard deviation or variance and the payoffs to each type of action are imperfectly correlated, a positively inclined and concave payoffs schedule emerges in risk-reward space. It is positively inclined because terrorist actions with a higher average payoff are attended by a higher risk or variance of their outcomes. It is concave because imperfect correlation between the payoffs to the different types of terrorism—payoffs to different actions do not move perfectly together over time—introduces concavity as an important aspect of the statistical structure. Only perfectly correlated payoffs across terrorist actions will produce a linear risk-reward trade-off. This concave trade-off between risk and reward that emerges when average payoffs and variance are considered in a context where terrorist actions can be combined is the clearest picture available of the type of statistical properties that may characterise the terrorists’ total or overall payoffs schedule.

We could examine a basic but unrealistic situation where a government’s ‘schedule of concessions’ replaces or becomes synonymous with the total payoffs schedule. However, unless we are willing to assume that concessions from the government are the only payoffs to terrorism this approach would lead us into the difficulties identified by Ross (2004, p.216). Even if we could make such an assumption the resulting analysis would, at best, apply only to a very small number of terrorist actions. The problem of government concessions in a terrorism context must be approached by treating the government’s concessions schedule as something that alters or adds to the payoffs schedule but does not replace it. If the payoffs schedule is characterised by a particular trade-off between risk and reward an alteration of or addition to the payoffs schedule may change this risk-reward trade-off. It is possible that the alteration or addition could increase the payoffs to risky terrorist actions. However, this is different from making those riskier actions more desirable from a terrorist’s point of view. Only if the concessions schedule alters the terrorists’ risk preferences in a manner that makes them more risk seeking will riskier actions—even those attended by higher payoffs than before—be desired by terrorists. If a payoffs schedule to terrorism might be conceived of as depicting a trade-off between risk and reward that is positively inclined and probably concave, the concessions and penalties that might be expected to characterise the government’s strategy or policy towards terrorists must also be shaped in some way. The ‘shape’ of the government’s concessions schedule is important. Recent work in other parts of economics, especially the analyses prepared by Carpenter (2000) and Ross (2004), has focused on the convexity and concavity of ‘incentives schedules’. The problem addressed in the literature that encompasses agency theory and theoretical finance theory or financial economics is analogous to ours. Their problem is to alter or add to a total remuneration schedule with an incentives schedule in order to entice the individual being remunerated to take more or less risk. The language used in this contemporary literature speaks of convexifying or concavifying a utility function. A schedule that convexifies a utility function makes the individual more risk seeking. A schedule that concavifies a utility function makes the individual more averse to risk. The ‘folklore’, as Ross (2004) calls it, in financial economics and agency theory had been that a convex schedule convexifies a utility function while a concave schedule concavifies it. The shape, convex or concave, of the government’s concessions schedule is central to our problem.

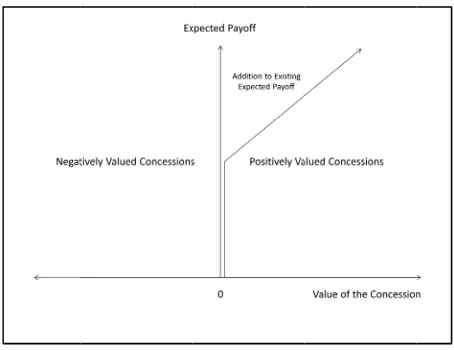

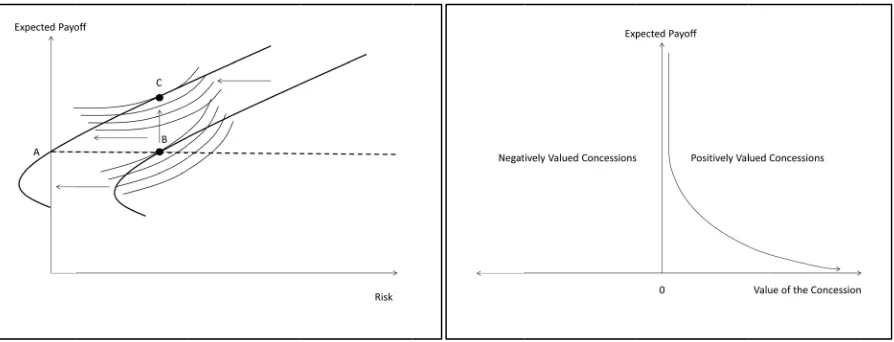

looks at it governmen making the discussion magnifies grant posit relatively more risky has been addition th actions hav it is usual The simpl schedule i past some example. A some poin theoretical steeper or important

Figure 1 d expected p positively terrorist’s has zero v axis but sh of risk tha terrorism, payoff ma terroristic hostages o forced—or hostage-ta the terrori governmen certain tha therefore,

t, payoffs are nt’s concessio ese risky terro n in the next s

payoffs past s tive and increa high expected y course of act

altered beyon hat we explore

ve a higher pay in the financia lest and most

s by adding to e point is a ‘p A convex sche nt is depicted in

l or technical r flatter than properties of t

depicts a gover payoff. At this

valued as ex payoffs past th alue. This first hould be interp at the terrorist the terrorist ta ay be those th violence is in or more hostag r be perceived aking scenario

st takes the m nt. The expec at a terrorist a it is not certain

e higher than ons have incre orist actions mo

section. For n some point. Im asing concessi d payoff and ri tion associated nd this expecte e first is a stee yoff. Such a co al economics li

obvious way o it. A convex positive additio

edule of conce n Figure 1. Th meaning. The shown and th the schedule ar

F

rnment conces point, the con xpected payoff his point. Up u t segment of th preted as coinc

takes. If there akes more risk hat are also m nflicted. Highe ges of a certain d to be able to or to avoid a t more payoff he ted payoffs ar action will ach n that any conc

they were be eased the payo

ore desirable. R now, let us ex

magine that te ions when the isk vis-à-vis o d with a relativ

[image:4.595.184.411.333.508.2]ed payoff by epening of the oncession mus iterature to dep y in which a x schedule of c on’. We shall essions that wh here is nothing e slope of the he linear segm re its positive e

Figure 1. Conve

ssions schedul ncessions sche fs increase. T until the conce he concessions ciding with it.

e is a positive k to obtain hig most undesirab er risk-higher n type (for exa o be forced—t threatened repe e can expect a

re risky and t hieve an actua cessions will b

111 efore. The pro

offs to risky t Ross (2004) m xplore the shap errorists becom terrorists succ ther feasible t vely high expe

the governme e risk-reward t st be convex. T pict such sched government’s concessions th consider ‘neg hen added to th g about the ‘lin

schedule past ments could b expected value

ex concessions

le that has a p edule ‘kinks’ an The positive v

ssions schedul s schedule has A concessions e risk-reward t gher expected ble from the

payoff attack ample, children —to provide con eat of the viole and the more the outcomes al payoff that be able to be fo

oblem with th terrorist action makes this poin pe of a conce me aware or pe

cessfully execu terrorist action

ected payoff, t ent’s concessi trade-off past The concession dules geometri

concessions hat magnifies t

gative addition he payoffs sch near’ schedule t the point wh be replaced w

edness and its

s schedule

ositive value p nd becomes po value of the c

le ‘kinks’ it co s been drawn s s schedule like trade-off chara d payoffs. Acti perspective o ks may have m

n) and so forth ncessions to e ence. Under th concessions h are attended b

is the same a orced.

his intuition is ns this is not nt. This point w ession from th

erceive that th ute a terrorist ns. Now if terr they face a pay ions schedule.

some point su n itself has an ically in payof may alter the the expected p ns’ or penaltie hedule magnifi

presented here here it is kink with curved se convexity.

past some poin ositively value concession is oincides with th

slightly to the r e this one is rel acterising the ions that have of the citizenr more expected h. As such, a g either alleviate hese circumsta he can expect by variability. as that which

s that although the same thin will be the foc he government he government action which h rorists embark

yoffs schedule . The alteratio uch that higher expected value ff-value space. e terrorist’s pa payoffs to terro es in a subseq ies the payoffs e that holds sp ked could be e egments. The

nt of the terro ed and increas an addition to he vertical axi right of the ve lated to the am

existing payof e a higher expe ry upon whom d fatalities or government ma e a crisis such ances, the more

www.ccsen

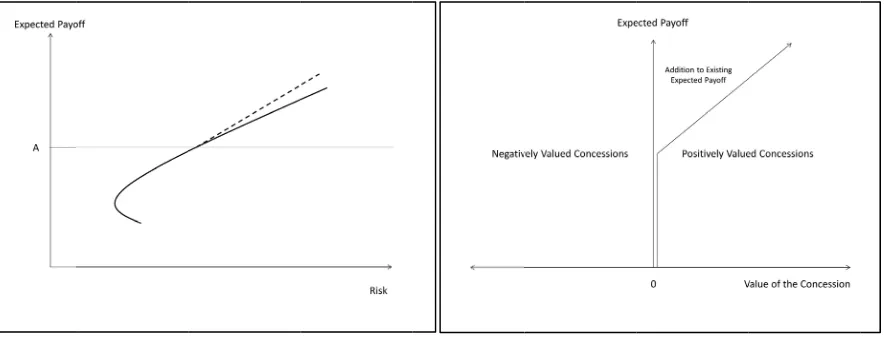

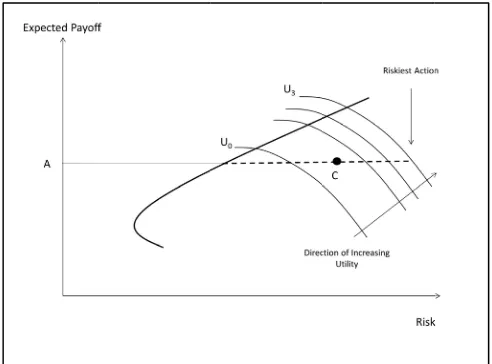

The impac schedule d associated possibility undertakin first panel depicts a p schedule b schedule fr

Point A in and becom concession greater tha tell us that payoffs. If However, more desir higher lev diverge sig presence o Now let u payoffs pa schedule d point. Fig sanctions t penalties, the additio that attend seeking an opportunit terrorist ac averse to r risk action schedule to

net.org/jpl

[image:5.595.74.516.201.370.2]ct of the conce does not imme d with risky ter y. Because the ng a higher risk l, a concave e positive trade-before the add from Figure 1 i

Figure 2

n the first pane mes positively ns schedule. T an A, expected t this will mak f the terrorists increasing the rable. All of t vels of risk and

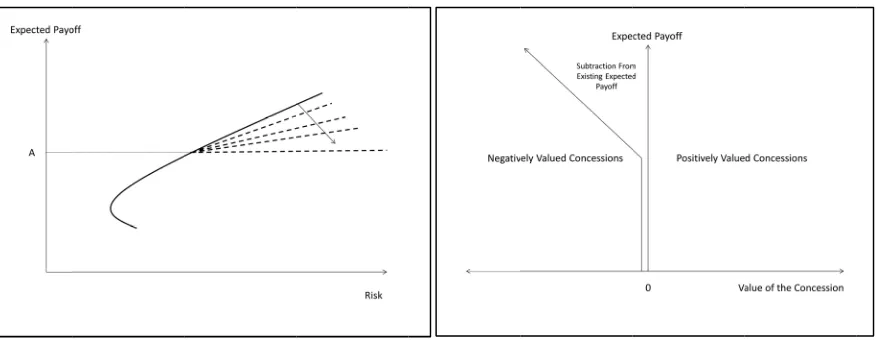

gnificantly fro of this type of c us consider a ‘n

ast some point depicted in Fig ure 3, deliber to terrorist act such as prison on of a negativ d riskier terror nd less likely ty set. Once m ctions will be risk or if the st n will terrorists o the existing p

ssions schedul ediately add t rrorist actions a

e expected pa k action does n expected payo

off between ri dition of a real is depicted.

2. Adding a co

el corresponds y valued. Pas This alteration d payoffs are h ke the terrorists s take more ri e expected pa the payoffs are

d a greater ch om the outcom concessions sc negative conc . Figure 3 con gure 1. It attach

rately stylised tions that have n sentences, are ve concessions

rist actions. In to choose to more, however associated wi tructure of the s avoid higher

payoffs schedu

Journal o

le on the existi o or subtract and those actio ayoffs to all not guarantee offs schedule isk and reward l or perceived

onvex concessi

to the point at st this point, is depicted by higher per unit s more risk see isks, higher ex ayoffs to riskie e risky. Nothi hance that the me that was exp

chedule will th ession’ or pen ntains a negativ hes increasing d though it ma

e an expected e already refle schedule to th ntuitively, it m

engage in the r, it is not ne ith an increase e expected pay r risk terrorist a

ule.

of Politics and L

112 ing payoffs sch

from the terro ons must be pe terrorist actio a particular ac

is sketched. A d will suffice.

concessions s

ions schedule t

t which the co the existing y the dashed li t of risk than t eking. The risk xpected payof er terrorist act ing is certain. actual outcom pected. Only i hey be enticed t nalty that incre ve concessions penalties to ac ay be, might payoff past so ected in the ex he existing pay might be expe e more risky ecessarily the e in terrorist ri yoffs changes s actions as a co

Law

hedule is depic orists’ ‘wealth erpetrated in o ons are uncer

ctual payoff or Any positively The solid line schedule. In th

to an existing p

oncessions sche expected payo ine. For terrori they were befo kier terrorist a ffs and govern tions does not Higher expec me—both the p

if terrorists are to engage in h eases monoton s schedule that ctions that hav be interpreted ome point (No

isting expected yoffs schedule ected that this

terrorist actio case that redu isk aversion. O such that it bec onsequence of

cted in Figure h’ (Note 6). Th order for conce

rtain and subj r its associated y inclined pay e represents th he second pan

payoffs schedu

edule in the se offs schedule ist actions with ore. Conventio actions now ha nment concess t necessarily m cted payoffs ar

payoff and the e made more r igher risk-high nely in the neg t is a mirror im ve expected pa

d as attaching ote 7). It is ass d payoffs sche is to reduce th would make ons that might

ucing the pay Only if terrori comes optimal f adding the ne

Vol. 6, No. 4;

2. The conces he concession essions to beco ject to variab d concession. I yoffs schedule he expected pa el, the conces

ule

econd panel ‘k is altered by h expected pa onal wisdom w ave higher expe sions are avail make those ac re characterise e concession— risk seeking b her reward acti gative for exp mage of the co ayoffs beyond g new penaltie sumed that exi edule. The effe he expected pa

3. Risky C Concessio payoffs sc manner th payoffs an does achie offset each are determ adjustmen all terroris expected p and then, i Ross (200 question fo ‘additions’ to the wea immediate context, co clear how needed in Our result Adding th will not co concession depicted in action, a p choose a indifferenc The first p the indiffe relatively schedule t positive co concession eastwards higher exp The more he continu Figure 3

Choices and C

ns schedules t chedule. In th hat allows us t nd, in doing so eve payoffs pa h other to som mined by what nts to the existi

sts more risk se payoffs to mor in the second c 04) presents a or popular spe ’ that Ross con alth of the indi e value to the t

oncessions sch Ross’s secon order to expla s are consisten e positively sl onvexify all te ns schedule wi n Figure 3. Al positively slop less risky ac ce curve mapp panel of Figure erence curve m flat to indicat to indicate the

oncessions ad ns do not shift

along the exis pected utility f

risky actions d ues to take no m

3. Adding a con

Concessions Sc

that are not sy e previous sec to explore situ o, believes that ast some point me degree. The t the terrorist p ing payoffs sc eeking or more re risky terrori case, diminishe

mathematical ecifications of t nsiders from an

ividual who re terrorist. They hedules have n nd theorem an

ain the impact nt with Ross’s loped convex c errorists’ utility ill not make ter

lthough it can ped negative c

tion. These c pings to the pay

e 4 depicts an mapping associ

te a low level willingness o dd to the exist ft the terrorist sting payoffs s for the relative do not become

more risk than

ncave concessi

chedules

ynonymous wi ction, expecte uations where t the governm t. The positive e net effects of perceives to b chedule by the e averse to risk ist actions wer ed by the addit l theorem and the individual n agency theor eceives them.

are unlike, fo no immediate d its fourth co t of concession s but the argum concessions sc y functions or rrorists more r never convex concessions sc conclusions ar yoffs schedule existing expec iated with the of risk aversi of a less risk av

ting payoffs sc onto a set of schedule. Alth ely more risky e more desirabl n he did in the

113 ions schedule

ith an existing ed payoffs, ris the terrorist m ent may be fo e or negative f simultaneous be the case. Th e imposition of k. In the cases re enhanced by tion of negativ d proof (Note

’s absolute risk retical perspec

The concessio or example, win effect on the orollary will h ns on terrorist ments through chedule depict r encourage ter

risk seeking. N xify a utility fu chedule will m re best explai e depicted in Fi

cted payoffs sc relevant utilit ion and are lo verse terrorist chedule. Ross flatter more ri hough the terro y actions he do le to him as a r absence of the

to an existing

g payoffs sched sk and conces must bear high

rced to yield c concessions th sly imposed p he question th f either positiv

that we consid y the addition ve concessions 8) that provi k aversion (No ctive have mar ons schedules ndfall gains of ‘wealth’ of th hold and alter

s’ risk prefere which they ar ed in Figure 2 rrorists to cho Now consider th

unction or ma make it rationa

ned and illus igures 2 and 3 chedule. The te

ty function. Th ocated towards t to engage in s’s theoretical isk seeking ind orist now obta oes not necess result of their n e alteration to

payoffs sched

dule alter or a ssions were lin

her risk to inc concessions if hat the govern ositive and ne at we seek to ve or negative

dered in the pr of positively v .

ides a technic ote 9). In most rket value and that we are co f resources. If, he terrorist gr rnative theoret ences or choice

re arrived at ar 2 to the existin

ose a riskier a he concave co ake the terroris al for the risk strated by add

.

errorist’s utilit he indifference s the eastern p more risky ter work suggest difference cur ains higher exp sarily become

now-higher ex the payoffs sc

dule

add to that exi nked together crease his expe f the terrorist a

nment applies egative conces

answer is wh e concessions m

revious section valued conces

al response to t cases, the typ

represent addi onsidering hav , within a terro roup, then it is tical argument es of risky act re more access ng payoffs sche action. This typ oncessions sche sts choose a ri k-averse terrori ding the terro

www.ccsen the imposi maximisin payoffs sc ‘steeper’ m Ross’s tec scenario w terrorism c this alterat concession there was resources. way to ex terrorist’s Nothing is make thos manner tha A concess the terroris or wealth preferred receives a has not ma payoffs ar averse to r choose a l preferred t schedule i risk. That happens, t action asso Positive co Let us no concave sc simply the acts to com is a very s for risk ap

net.org/jpl

ition of the po ng point from B chedule in a m more risk-avers

Figure

chnical-mathem where the addit

context, this m tion of the exp ns schedules w

none before In fact, the co xplain the imp

risk preferenc s certain. Incre se riskier terro at can make th sions schedule sts’ ‘wealth’ o or resources to bear a par higher expect ade higher risk e higher, the t risk will not w less risky actio

the amount of s imposed the is, rather than the terrorist ch ociated with th oncessions tha w explore the chedule that re e mirror image mpletely offset straightforward pply to any con

ositive conces B to C. It is p anner that incr se indifference

e 4. Convex co

matical approa tions to an exi may not be the c

pected payoffs will alter the e

may not incre oncessions sch pact (or non-im

ces is as follow ements to the e

rist actions mo he terrorist mor

that increases or accumulated that are the r rticular amoun ted payoff than k actions more

errorist must s wish to do so. on after the co f risk associate

terrorist may n moving upwa hooses a lower he initial choic at increase expe

e case of nega educes the exp e of the convex t the additiona d concessions ncave monoton

Journal o

ssions schedule possible in fact

reases the terro e curve mappin

ncessions and

ach provides isting schedule

case and we m schedule doe expected payo ease terrorists hedule may hav

mpact) of the ws. The conce expected payo

ore desirable b re risk seeking s the expected d payoffs or res

eference point nt of risk befo n before but h e attractive to t still bear more A careful ins oncessions are ed with point

switch to a les ards to point C r risk action an e at point B. T ected payoffs d ative concessi pected payoffs x schedule in F al expected pay

schedule but nely increasing

of Politics and L

114 e. This is indi t that a positiv orist’s risk ave ng.

terrorist prefe

a rigorous exp e add to the ‘w must find an alt

s not entice te offs schedule, ’ ‘wealth’ or ve no immedia

positive conc essions schedu ffs associated because they d g.

d payoffs of m sources endow t for both rela ore the conce he is not entice terrorists who risk to obtain spection of Fig

added to the e B and the ass ss risky action C, the terrorist nd one that, pr This would be a do not entice t ions. A sched to terrorism. T Figure 2. Past

yoffs obtained our conclusio g concessions

Law

icated by the ve concessions ersion and shif

erences for mor

planation for wealth’ of the

ternative logic errorists to cho the addition o add to the ter ate value to th cessions sched ule only intera with increasin do not interact

more risky terro wment and it is ative and abso ssions schedu ed to bear mor are more aver n higher expect

gure 4 reveals expected payo ociated expect and obtain the may be shifte resumably, has a desirable out the terrorist to dule of negativ

The schedule t some point, th d from increasi ons regarding i schedule. In F

vertical move s schedule will fts the terroris

re risky action

why this may individual rece al-economic e oose riskier act of a concessio rrorists’ accum he terrorists. In dule depicted i acts with risky ngly risky terro

t with terrorist

orist actions is s, of course, ac olute risk aver ule was applie re risk. The co se to risk. Alth ted payoffs an s that the terro offs schedule. W

ted payoff, aft e same expect ed horizontally s less expected tcome for the g engage in risk ve concession that we have d his negative co ingly risky ter its effect on te Figure 5 the ef

Vol. 6, No. 4;

ement of the u l alter the expe st westwards o

ns

y be the case eiving them. I explanation for tions. Althoug ons schedule w

mulated payof n this case, the in Figure 2 on y expected pay orist actions d t risk aversion

s not an additio ccumulated pa

rsion. If a terr ed, he now si

ncessions sche hough the expe nd a terrorist w

orist might act Where the terr fter the conces

ted payoff with y westwards. I

d ‘impact’ tha government. kier terrorist ac

s or penalties drawn in Figure oncessions sche rrorist actions. errorist prefere ffect of the con

2013 utility ected nto a in a n the r why h the where ffs or e best n the yoffs. o not n in a

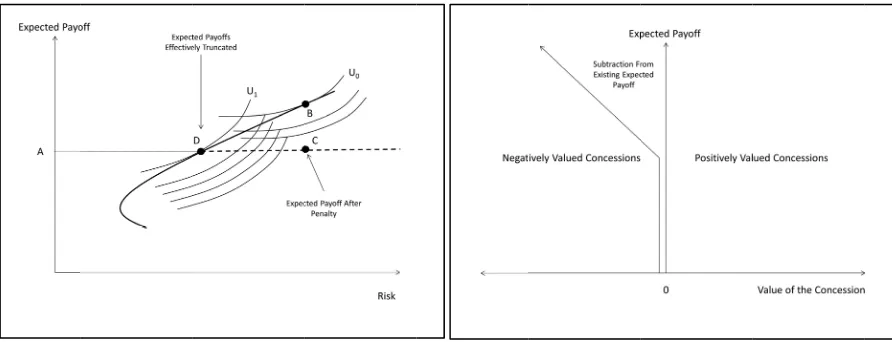

negative c explanatio negative c is no imm explained choice of subtraction terrorist is The impos offsets the terrorist fi expected p preference would obt will lead h action at p coincides schedule li 4. Making If, contrar magnifies concession declining c manner op does so in the upside the terroris intact, the finds the e given the t more risk whilst leav action at p The protec It is difficu inadverten concession

concessions s on for the res oncessions sub mediate subtrac

as follows. F risky actions n from the terr s initially at po sition of the ne e gains in exp nds himself ex payoffs sched es and move to tain at point C him to choose point C. The i

with an intuit ike the one in

g Terrorists M

ry to conventi expected pay ns schedule wi concessions sc pposite to our such a way a e potential inta

st. The reason terrorist cann expected payof

trade-off now averse terroris ving the upside point C. By do

ction on the do ult to imagine ntly. The only

ns schedule fo

schedule is d sulting concav btract from the ction from the

irst, one may when the po rorists’ accumu oint B. This is egative conces pected payoffs xpecting a pay dule has been o a lower risk C but it is obta

[image:8.595.72.518.307.478.2]the less risky impact of the tive assessmen the second pan

Figure 5. Con

More Risk See

ional intuition yoffs past som

ill make all te chedule (Ross, negative conc s to protect th act (Ross, 200 for this lies in ot receive a pa ffs schedule is

characterising st was initially e potential inta oing so he rece ownside effecti e that a govern possibility is or expected pay

depicted. Aga vification of t e terrorist’s ‘w terrorist’s ‘we wonder why ositive conces

ulated payoffs s the same poi ssions schedule s obtained fro yoff of C from

effectively tr action at poin inable with fa y, lower payof negative conc nt of the likely nel of Figure 5

ncave concessi

eking

n, a convex, p me point does errorists more , 2004, p.218) cessions sched he terrorist from 04). This posit

n its effect on ayoff less than s effectively re g risk and rewa located at poi act ‘pulls’ eve eives a higher ively reduces t nment or a terr a situation w yoffs below so

115 ain, Ross’s te

the terrorist’s wealth’. In less

ealth’ or resou the negative c sions do not s or resources int from which

e that is depic om risky terror m the relatively runcated. It is nt D. At point ar less risk. Th ff action at po cessions sched

y impact of p 5.

ons and terrori

positive, mon s not make al

risk seeking? . Such a conce dule. It too ‘tr m expected pa tive monotone the expected p n A regardless elocated westw ard. This is dep int B, the conc erything westw expected payo the risk associa rorist group co where a terrori ome point. If t

echnical-mathe utility functi s technical term urces or accum

concessions m even when n endowments. I h the story con ted in the seco rist actions be y higher risk t s now rationa D, the terrori he utility maxi int D rather th dule is much m penalties such

ist preferences

notonely increa ll terrorists m The answer is essions schedu runcates’ the e ayoffs that are ly declining c payoffs schedu s of how much wards and mor picted in the f cessions schedu wards. The terr

off but does no ated with more ould impose su ist attaches an

the negative c

ematical appr ion under con ms and for situ mulated payoff might interact either represe In the first pan ntained in Fig ond panel of F eyond some p terrorist action al for the terr st expects the mising behavi han the more r more straightf as those depi

s for risk

asing concess more risk seek s a convex, po ule works, bro expected payo below some l concessions sc ule. Although h risk he takes re risky action first panel of F

ule that protec rorist now choo

ot bear any ‘re e risky terroris uch a concessi n inverse valua concessions sch

roach provide nditions where uations where fs, the result ca

with the terro ents an additio

nel of Figure 5 gure 4 commen Figure 5 compl

point. As such n instead of B. rorist to adjus same payoff a iour of the terr risky, equal pa forward and it icted by a con

ions schedule king, what typ ositive, monoto adly speaking offs schedule b

evel whilst lea hedule convex the upside rem s. The terrorist

s become desi Figure 6. Wher cts on the down

oses a ‘more r eal’ additional st actions.

ons schedule, ation to a neg hedule involve s an e the there an be rists’ on or 5, the nced. letely h, the . The st his as he rorist ayoff t also ncave that pe of onely

www.ccsen the limit, monotonel such circu payoffs de capture an is effectiv ‘infinite’. 5. Expecte When neg there to be penalties f still observ more varia choose an the newly terrorists n three pote maximises Expected u seeking ra risk. This not all acts resources Figure 5, f Innovation we know theory that of the aver a new kind the existin innovation existing ex that which action. It i example. I about the t knowledge

net.org/jpl

[image:9.595.74.521.175.346.2]the death of ly declining co umstances, not ecline past som nd imprisonme vely truncated

Figure 6

ed Payoffs an

gative concessi e a reordering for skyjacking

ve some terror able outcomes action at poin added penalti not choose les ential answers

s expected uti utility theory ather than risk

type of terrori s of terrorism to the most ris for example. n is also an im

about the expe t attempts to e rages of the pa d of terrorist a ng equilibrium ns and the pay

xpected payoff h would be co is only after th It is only after types of payof e within the ex

f the terrorist oncessions sch t surviving th me point if dea ent. If death is even though,

6. Convex posi

d Innovations

ions or penalti of terrorists’ in the United rists to engage s than others a nt C, say, in Fi ies for the hig s risky actions to these que lity. Even if h does not rule

averse. A risk ist is depicted

in the face of sky action. Th

mportant part o ected payoffs explain terroris ayoffs obtained action until th m and structur

yoffs associate ffs schedule, pr ommensurable he action is trie the action is tr ffs that might b xisting expecte

Journal o

(Note 10) fo hedule may be e failed action ath is perceived accorded a ‘p , from a poin

tive declining

s in Terrorist

ies are added preferences. T States in the 1 e in them just actions that the igure 5 when t gher expected s with lower e stions. First, t he tries to ma out erroneous k seeking terro

by the indiffer increasingly h his would expl

of the explanat schedule, the sts’ choices. Th

d from terroris hat action is pe res, which mu ed with them.

roviding the te or obtainable ed for the first

ried for the firs be obtainable b ed payoffs sch

of Politics and L

116 ollowing a fai

perceived by n might be po d by the terror

ayoff equivale nt of view oth

concessions an

Actions

to an existing This is clearly 970s (Landes as we see som ey could have the expected p payoff action expected payof

the terrorist m aximise expec s or poor decis orist will give rence curve m harsh penalties lain why we m

tion for the typ risk-reward tr he expected pa st actions in th erpetrated at le

ust then be r A terrorist ac errorist who in

at the same l time that gove st time that ter by means of th edule that prov

Law

iled terrorist the terrorist u ositively and rist as being be ent’ of A, for e her than the te

and terrorist pre

g expected pay the case follo 1978). Despite me terrorists e e chosen. Why payoff is the sa n are taken int

ffs and lower may not choos

ted utility, the sion-making. S up expected p mapping in Figu . A risk seekin might observe

pes of actions rade-off that c ayoffs schedul he past, does no

east once. Sch reassembled in ction of a new

nnovates with level of risk b ernments will rrorists themse he innovative a vides an indic

action then a under some cir increasingly v etter than other example, the te errorist’s, the

eferences for r

yoffs schedule owing the intro e the introduct ngage in actio y would any te ame as a less r

o consideratio negative conc se his actions e terrorist may Second, the te payoffs in ord ure 7. This wil ng terrorist wil actions to the

that we obser characterises it le, if it is const ot reflect the p humpeterian in n a manner th w kind may be

an expected p by means of a react with sec elves will be m action. Until th

ation of the ris

Vol. 6, No. 4;

a positive, con rcumstances. U valued as expe r outcomes su errorist’s down

downside app

risk

e, we would ex oduction of ha tion of penaltie ons that have m

errorist continu risky action D on? Why woul cessions? Ther s in a manner y make a mis rrorist may be der to take on

ll explain som ll allocate all o

right of point

rve relative to t and the econ tructed on the payoffs availab nnovations ‘sha

hat includes t e located abov

payoff that exc well-tried terr curity measure more knowledge

that should and reward expected p innovation

6. Discuss

A negativ lower risk not shift t expected p terrorist ac remains ju schedule g preference relationshi existing pa the more te Although w types of co and increa expected u riskier act increasing concession risky and risky actio The only t one that le which actu payoffs are of risk as concession open the p payoffs pa payoffs thr

d be associated ds of the action payoffs sched n in terrorist ac

sion, Conclusi

e, concave co lower reward the utility ma payoffs schedu ctions past som ust as risk aver

geometry dep es for risk in a ip between exp ayoffs schedul echnical-math we have, for t oncessions sch asing past som utility from the tions simply b past some po ns schedule tru more risky ac on each with th type of conces eaves the highe

ual payoffs can e reshaped suc lower risk act ns schedules w possibility of ast some thresh rough more ris

d with the actio n at all in any dule comes to

[image:10.595.175.421.140.322.2]ction.

Figure 7. Th

ions and Futu

oncessions or p section of the aximising risk

ule. Although me point it doe

rse as he was b picts the impa a manner that h

pected payoffs le but does not hematical appro the most part, hedules with th me point will n

e risky actions because the ex oint will make uncates the ter ctions. The terr he same expect ssions schedule er expected pa nnot fall. When ch that higher r

tions. These re with different s positively val hold point will sky terrorist ac

on. Indeed, the way. It is only reflect a new

he risk seeking

ure Research

penalties sche e expected pay averse terror a positive co es not make the

before. Our ex act of governm

has not been p s, risk and con

t replace it or oach taken by drawn ‘stylise he same prope not make all te that he was w xpected payof e terrorists be rrorists’ expec rorist is now f ted payoff. A r e that will cert ayoffs to more n expected pay risk higher exp esults can be e shapes. From a lued concessio l not be attend ctions. When l

117 e existing expe y through the ‘ w trade-off be

g terrorist pref

edule shifts th yoffs schedule. rist to a highe oncessions sch ese risky actio xpected payoff ment concessi presented befo ncessions in a c

become synon Ross (2004) b ed’ concession erties. That is, errorists more willing to under ffs are higher

have as thoug cted payoffs ef faced with a c risk-averse uti tainly make th risky terrorist yoffs below so pected payoff t extended and a government’ ons attached t ded by an incre less risk-averse

ected payoffs s ‘entrepreneuria etween risk an

fers more risk t

he utility maxi A positive, co er risk higher hedule increase ons more desira fs schedule, ind ions on the t ore in the litera

context where nymous with i but they are mo ns schedules, th convex conces risk seeking. T rtake but he w r. Concave co gh they are m ffectively equa choice between lity maximiser he terrorist mor t actions intact ome point are r

terrorist action the same anal ’s point of view

to terrorist ac ease in the num

e terrorists do

schedule does n al’ actions of t nd reward tha

to less

imising risk av onvex concess

expected pay es the expecte able to all terr difference curv terrorist’s exp

ature. It allow a concessions it. The results ore accessible. he results will ssions schedul The terrorist w ill not be entic ncessions that more averse to ates the expec n a less risky r will choose t re risk seeking t whilst provid

ruled out, the t ns effectively h lytical apparat

w, the results ctions that are mber of terrori engage in such

not reflect the the terrorist tha at incorporate

verse terrorist sions schedule yoff section o ed payoffs to orists. The terr ve and conces pected payoffs ws us to explor s schedule alte are consistent

hold for any les that are pos will obtain a h ced to embark t are negative risk. The con cted payoffs of action and a the less risky a g is the implau ding a ‘floor’ b terrorist’s expe have the same tus can be use imply that kee expected to sts pursuing h h actions and w

www.ccsenet.org/jpl Journal of Politics and Law Vol. 6, No. 4; 2013

118

they are successful at it, the government may use positively valued concessions to alleviate the crisis without making terrorists more risk seeking.

The analytical treatment of concessions within the terrorism studies literature is quite advanced but relevant results can be found in a research program that is ongoing in other parts of economics. Both Ross (2004) and Carpenter (2000) make some progress in identifying the conditions under which a convex schedule will convexify an agent’s utility function. The type of problem that Ross and Carpenter address is a part of the research program directed towards the investigation of the principal-agent problem. In turn, parts of this research program fall under the broader research program that investigates the role of incentives in economic decision-making and risk taking (Note 11). This literature has received an additional boost following the financial crisis of 2008 where excessive risk taking and misaligned incentives figured prominently in the analytical post-mortems carried out over the ensuing several years (Note 12). The number of theoretical advances since Ross (2004) has not been substantial and his paper remains among the few to rigorously address the problem of whether convex schedules convexify an agent’s utility function (Note 13).

Granting concessions may not be a sub-optimal negotiation strategy but will granting concessions make terrorists more risk seeking? Will granting concessions that increase the expected payoffs to more risky terrorist actions entice terrorists to engage in those actions? We have addressed this question in this paper. Convex positively valued concessions that increase the expected payoffs to risky terrorist actions will not make ‘terrorists’ as a general category more risk seeking. This result emerges clearly when the concessions schedule is treated as being distinct from the expected payoffs schedule. Existing theoretical work has often focussed on exploring decision-making within scenarios where the concessions that may be received from the government are the terrorists’ payoffs. Our treatment, by contrast, sets down an expected payoffs schedule that is altered by the imposition of positive or negative government concessions. Expected payoffs are risky and the actual outcomes of a terrorist action may diverge from those that were expected. Linked as they are in our analysis to the payoffs to risk actions, positive concessions are also risky and uncertain. Although they may increase the expected payoffs to more risky terrorist actions, positive concessions do not represent additions to the terrorists’ accumulated payoffs, resources or ‘wealth’. The expected payoffs schedule is altered but not in a manner that entices the utility maximising risk averse terrorist to engage in riskier actions.

A research program that explores the relationship between incentives, broadly speaking, and terrorist behaviour may be either mathematical or more logical-theoretical in nature. A mathematical approach would build upon the types of results found in Carpenter (2000), Ross (2004) and Braido and Ferreira (2006). In particular, it would be interesting to prove that the results contained in Ross (2004) apply in situations where a terrorist group dynamically accumulates actual payoffs and concessions over time in a series of terrorist actions. Such an analysis would highlight the relevance of decreasing and increasing absolute risk aversion in the examination of terrorist choices in a dynamic setting. Higher mathematics is not the only pathway that may be followed. Incentives shape terrorists’ behaviours in ways that can be explored through logical argument. This paper has pointed out that terrorists’ expected payoffs may be altered by the imposition of concessions and this, in turn, may shape terrorists’ choices of risky actions. Two important problems that may be approached in a similar manner concern the examination of the interaction between incentives provided within a terrorist group and the choices of terrorists associated with that group and the examination of the effects of attempts by terrorist groups to resource, encourage or incentivise lone individual terrorists (Note 14) who are operating more or less independently in dispersed locations. The use of different methods, some drawn from research in other parts of economics, to explore terrorist behaviour will likely yield some worthwhile results.

References

Abrahms, M. (2006). Why terrorism does not work. International Security, 31, 42-78. http://dx.doi.org/10.1162/isec.2006.31.2.42

Abrahms, M. (2008). What terrorists really want: terrorist motives and counterterrorism strategy. International Security, 32, 78-105. http://dx.doi.org/10.1162/isec.2008.32.4.78

Abrahms, M. (2011). Does terrorism really work? Evolution in the conventional wisdom since 9/11. Defence and Peace Economics, 22, 583-594. http://dx.doi.org/10.1080/10242694.2011.635954

Braido, L. H. B., & Ferreira, D. (2006). Options can induce risk taking for arbitrary preferences. Economic Theory, 27, 513-522. http://dx.doi.org/10.1007/s00199-004-0581-6

119

Carpenter, J. N. (2000). Does option compensation increase managerial risk appetite? Journal of Finance, 55, 2311-2331. http://dx.doi.org/10.1111/0022-1082.00288

Coles, J. L., Daniel, N. D., & Naveen, L. (2006). Managerial incentives and risk taking. Journal of Financial Economics, 79, 431-468. http://dx.doi.org/10.1016/j.jfineco.2004.09.004

Dong, Z., Wang, C., & Xie, F. (2010). Do executive stock options induce excessive risk taking? Journal of Banking and Finance, 34, 2518-2529. http://dx.doi.org/10.1016/j.jbankfin.2010.04.010

Enders, W., & Sandler, T. (1993). The effectiveness of anti-terrorism policies: a vector-autoregression-intervention analysis. American Political Science Review, 87, 829-844. http://www.jstor.org/stable/2938817

Enders, W., & Sandler, T. (2002). Patterns of transnational terrorism, 1970-1999: alternative time-series estimates. International Studies Quarterly, 46, 145-165. http://dx.doi.org/10.1111/1468-2478.00227

Fahlenbruch, R., & Stulz, R. M. (2011). Bank CEO incentives and the credit crisis. Journal of Financial Economics, 99, 11-26. http://dx.doi.org/10.1016/j.jfineco.2010.08.010

Fearon, J. D. (1995). Rationalist explanations for war. International Organisation, 49, 379-414. http://dx.doi.org/10.1017/S0020818300033324

Frey, B. S., & Luechinger, S. (2003). How to fight terrorism: alternatives to deterrence. Defence and Peace Economics, 14, 237-249. http://dx.doi.org/10.1080/1024269032000052923

Graham, J. R., Harvey, C. R., & Puri, M. (2013). Managerial attitudes and corporate actions. Journal of Financial Economics, 109, 103-121. http://dx.doi.org/10.1016/j.jfineco.2013.01.010

Kahneman, D., & Tversky, A. (1979). Prospect theory: an analysis of decision under risk. Econometrica, 47, 263-292. http://www.jstor.org/stable/1914185

Landes, W. M. (1978). An economic study of U.S. aircraft hijacking: 1961 to 1976. Journal of Law and Economics, 21, 1-31.

Lapan, H. E., & Sandler, T. (1988). To bargain or not bargain: that is the question. American Economic Review Papers and Proceedings of the One-Hundredth Annual Meeting of the American Economic Association, 78, 16-21. http://www.jstor.org/stable/1818090

O’Neill, B. (2001). Risk aversion in international relations theory. International Studies Quarterly, 45, 617-640. http://dx.doi.org/10.1111/0020-8833.00217

Panageas, S., & Westerfield, M. M. (2009). High-water marks: high risk appetites? Convex compensation, long horizons and portfolio choice. Journal of Finance, 64, 1-36. http://dx.doi.org/10.1111/j.1540-6261.2008.01427.x Phillips, P. J. (2009). Applying portfolio theory to the analysis of terrorism: computing the set of attack method combinations from which the rational terrorist group will choose in order to maximise injuries and fatalities.

Defence and Peace Economics, 20, 193-213. http://dx.doi.org/10.1080/10242690801923124

Powell, R. (2002). Bargaining theory and international conflict. Annual Review of Political Science, 5, 1-30. http://dx.doi.org/10.1146/annurev.polisci.5.092601.141138

Pratt, J. W. (1964). Risk aversion in the small and in the large. Econometrica, 32, 122-136. http://www.jstor.org/stable/1913738

Ross, S. A. (2004). Compensation, incentives and the duality of risk aversion and riskiness. Journal of Finance, 59, 207-225. http://dx.doi.org/10.1111/j.1540-6261.2004.00631.x.

Rubinstein, A. (1982). Perfect equilibrium in a bargaining model. Econometrica, 50, 97-110. http://www.jstor.org/stable/1912531

Sandler, T., Tschirhart, J. T., & Cauley, J. (1983). A theoretical analysis of transnational terrorism. American Political Science Review, 77, 36-54. http://www.jstor.org/stable/1956010

Siqueira, K., & Sandler, T. (2006). Terrorists versus the government: strategic interaction, support, sponsorship.

Journal of Conflict Resolution, 50, 878-898. http://dx.doi.org/10.1177/0022002706293469

www.ccsenet.org/jpl Journal of Politics and Law Vol. 6, No. 4; 2013

120

Tchistyi, A., Yermack, D., & Yun, H. (2011). Negative hedging: performance-sensitive debt and CEO’s equity

incentives. Journal of Financial and Quantitative Analysis, 46, 657-686.

http://dx.doi.org/10.1017/S0022109011000068

Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: cumulative representation of uncertainty.

Journal of Risk and Uncertainty, 5, 297-323. http://dx.doi.org/10.1007/BF00122574

Windram, R. (2005). Risk-taking incentives: a review of the literature. Journal of Economic Surveys, 19, 65-90. http://dx.doi.org/10.1111/j.0950-0804.2005.00239.x

Winkler, W. (2008). Die Geschichte der RAF. Rororo.

Notes

Note 1. Peter Lorenz—prisoner of the Movement 2 June.

Note 2. Also see Landes (1978), Enders and Sandler (1993), Enders and Sandler (2002), Frey and Luechinger (2003) and Siqueira and Sandler (2006).

Note 3. O’Neill’s (2001) discussion of the treatment of risk aversion within international relations theory contributes the background to this discussion.

Note 4. The ‘conventional wisdom’ might be interpreted as follows: governments should not negotiate with terrorists because doing so will encourage terrorism. Lapan and Sandler (1988) looked into the optimality of a ‘never negotiate’ strategy but did not address what seems to be another aspect of the conventional wisdom. That is, granting the terrorists some concessions emboldens them. This could be taken to mean that it encourages more risk seeking.

Note 5. An economist’s approach might be to use monetary equivalents (Enders and Sandler 2002).

Note 6. ‘Wealth’ is the accumulated payoffs of the terrorist or terrorist group or the terrorist or terrorist group’s resources. It might have a monetary equivalent or it might not. The terrorists’ ‘wealth’ is assumed to interact with the terrorists’ relative and absolute risk aversion in the same sense that monetary wealth interacts with an economic agent’s risk aversion in more orthodox settings.

Note 7. For example, in the 1960s and 1970s, much stricter prison sentences were imposed for aircraft ‘skyjacking’ after a spate of incidences (see Landes 1978). This can be analysed as negative additions to the existing expected payoffs schedule.

Note 8. See Ross’s second theorem and its fourth corollary (p.216-217).

Note 9. An individual’s utility is described by both relative and absolute risk aversion (see Pratt 1964). Different specifications of the utility function (power, exponential, logarithmic and quadratic) are characterised by different types of relative and absolute risk aversion. A popular specification is ‘decreasing absolute risk aversion’ (DARA). Individuals with decreasing absolute risk aversion allocate more resources to risky actions as payoffs accumulate.

Note 10. This is a government’s negative concessions or penalties schedule. In this case, relevant causes of death do not include the terrorist’s suicide.

Note 11. See the review by Windram (2005).

Note 12. For example, see Fahlenbrach and Stulz (2011).

Note 13. See Braido and Ferreira (2006), Coles, Daniel and Naveen (2006), Panageas and Westerfield (2009), Dong, Wang and Xie (2010), Tchistyi, Yermack and Yun (2011) and Graham, Harvey and Puri (2013).

Note 14. These could be thought of as ‘quasi’ lone wolves. A true lone wolf terrorist operates alone.

Copyrights

Copyright for this article is retained by the author(s), with first publication rights granted to the journal.