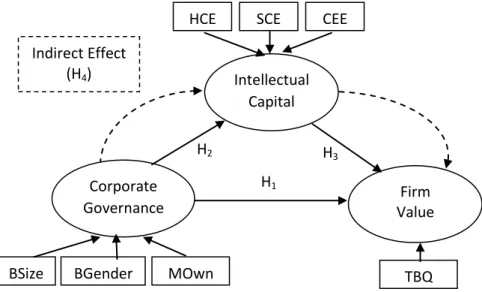

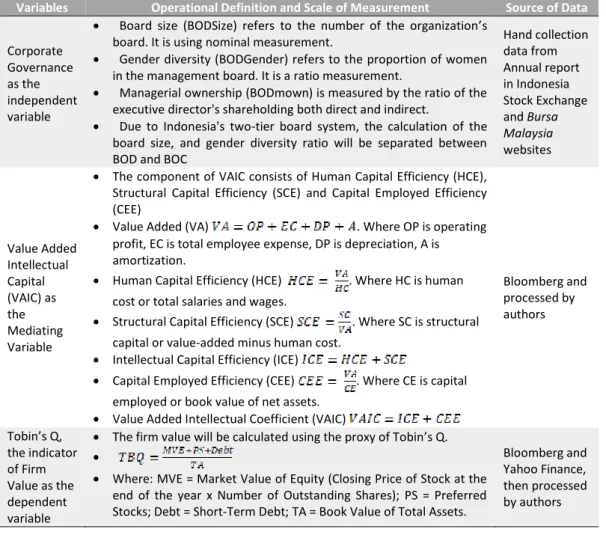

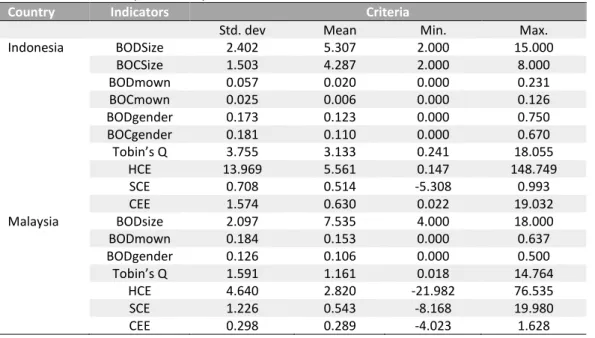

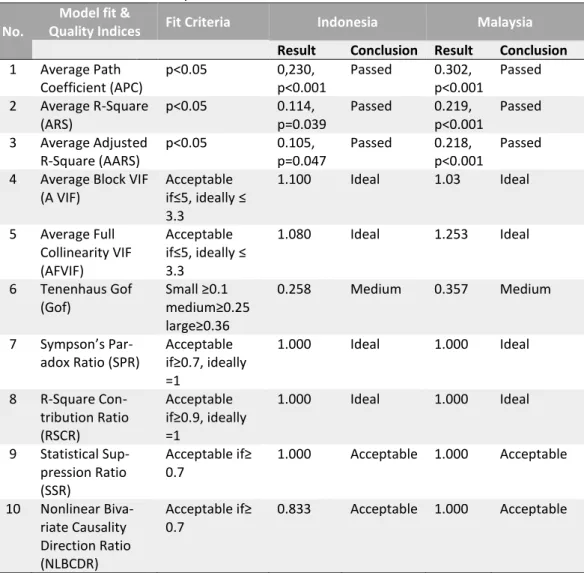

The Intervening Role of Value Added Intellectual Capital on The Relationship between Corporate Governance and Firm Value

Full text

Figure

Related documents

As in the previous Oversight Report , the Bank assesses the UK PPS fully to observe eight of the nine relevant Core Principles for sterling and euro payments and seven of the

It consists of generic measures (social marketing campaign, vessel monitoring and compliance) and control of source populations in Bluff Harbour to reduce the immediate risk of

Any realistic assessment of the current configuration of Congress must recognise: (a) that there are not 10 Republican votes in the Senate willing to support virtu- ally any

They were also moved longer distances than during the days before the experiments, and they were removed from the field to a higher extent than were fawns bedded in hay fields

With approval of the supervisory committee, a student may take two elective courses (6 credit hours) at the graduate level or higher from other departments, excluding

3.11 The development charges described in Schedule “B” to this By-law shall be imposed on non-residential uses of land, buildings or structures, and, in the case of a mixed

• starting package : as from October 6 th 2014 holiday packages including accommodation (minimum stay of 4 nights) and guaranteed registration to the Maratona