Revolving

Loan

Funds

in

North

Carolina

A

Profile

of

the Industry

Matt

Hull

and Carl

RistCarlRist istheSenior

Program

Manager

fortheCorporation for

Enterprise

Development (CFED).

MattHullisa

programassociateat

CFED.

He

hasaMaster'sinRegionalPlanning

fromthe Universityof

North Carolinaat

ChapelHill.

Just

beyond

the gleaming corporate headquarters that herald NorthCarolina as one ofthe nation's banking centers exists a

$90

million lendingindustrythatquietly serves local markets. Withoutthe fanfare that

accompa-nies the corporate banking world, these revolving loan funds (RLFs)

make

loanstobuildbusinesses andrevitalizecommunities inareas underserved

by

private financial institutions.

As

inmost

states, little isknown

about thisin-dustry collectively, but as a result ofthe research described in this article, a

clearerpicture ofNorth Carolina's

RLF

industry hasbegun

to emerge. For example:•

RLFs

represent atleast $90million incapitaldedicatedto small businesslendinginNorthCarolina.

•

With

amedian

loan fund size of $1.3 milhon, North Carolina's fiondsare,

on

average, significantlylargerthantheRLFs

inany

other statesur-veyed.

• North Carolina's

RLF

industry has a unique structure—

larger fimds, but fewer ofthem

—

that is, in largepart, a product ofstategovernment

policyandfunding.

•

While

a handful ofhigh-performing funds dominate the state'sRLF

in-dustry, the rest

of

thestate'sRLFs

do nothave a very diversified capitalbaseand,

on

average,areonly revolvingtheircapital, if atall.What

isaRevolvingLoan Fund?

Revolving loan funds (RLFs) are community-based financial institutions

that provide access to capital for individuals and communities underserved

by

private financial institutions.RLFs

exist in every stateand

are supportedby

funders at all levels of government, as well asby

private andphilan-thropic institutions.

They

provide loanstolocalbusinessesthatcannotattractprivate financing, and recycle the repayments

by

relending the capital tootherbusinesses.

RLFs

are aflexible andeffective tool forpromotingbusi-ness development, job creation, and economic self-sufficiency.

RLFs

have proven to be financially sustainable institutions that collectivelymanage

up

toseveral billion dollars inassets.The

Counting on Local

Capital ProjectThe

profile ofNorth Carolina'sRLFs

in this articlewas

developedby

the Corporation forEn-terprise

Development

(CFED)

as partofa nationalresearch and policy project, Counting on Local

Capital. Counting on LocalCapital, fiinded

by

theFord Foundation, seeks to build

knowledge

aboutthe size, level of activity, and impact of

RLFs.

North Carolina is one of seven states profiled as part ofthe project, joining Arkansas, California,

Illinois,Minnesota,Ohio,and Washington.

Methodology

North Carolina

was

selected as one of sixstate partners in the national Counting on Local

Capital project in July 1997.

The

state'sapplica-tion

was

sponsoredjointlyby

the North CarolinaDepartment of

Commerce

andthe North CarolinaRural

Economic Development

Center.Since a single, comprehensive inventory of

RLFs

inNorth Carolina did not exist, one oftheprimary tasks

was

to develop such a list.With

help

from

various state andnon-profit sources, 88organizations thought to be operating loan flmds

were

identified and sent a detailed survey.From

this list, 53 organizations

(60%)

responded.Over

halfoftheresponding organizationsindicated that

they did not operate a loan fimd,while

24

organi-zations responded that they operated at least one

RLF.

Three of the organizations operatedtwo

separate loan funds, bringing the total

number

ofRLFs

in thestudyto27.Among

the 27RLFs

in our sample, specialnote should be

made

about four of these funds.While

the purpose ofour surveywas

to identifyand profile

economic

developmentRLFs,

we

re-ceived surveys

from

four of the larger cities inNorth Carolina that reported

on

relatively largeRLFs

frinded primarily withCommunity

Devel-opment

Block Grant(CDBG)

grants toEntitie-ment

Cities.Each

ofthese ftmdsmakes

acombi-nation of

economic

development and housingloans, butthe fund

managers were

unable topro-vide data on just the

economic

developmentpor-tion of the portfolio. Despite the fact that these differences

make

these four fundssomewhat

un-like the other funds in our profile, this report

in-cludes

them

in itsanalysisbecause:• theDepartment of

Housing

andUrban

Devel-opment

(HUD), which

funds both SmallCit-ies

CDBG

grants andCDBG

grants toEnti-tlement Cities, has been,

by

far, the largestsourceoffederal dollars for

RLFs,

and• data

on

RLFs

funded withCDBG

grants toEntitlement Cities, in particular, has

been

themost

difficultto obtainduringtheresearchon

RLFs

forthe Countingon

Local Capitalproj-ect.

Recognizing these differences, though, this articlewillattimes exclude these four fiinds

from

the analysis. Thus,

when

reference ismade

to"Economic

Development

ONLY

RLFs,"

thismeans

the 23RLFs

(excluding these four distinctfunds) that

make

economic

development loansonly. Otherwise,

when

this report refers to "AllRLFs," this will indicate the entire sample of 27

RLFs

from North

Carolina in the database,in-cluding thesefourdistinctfunds.

Findings

from

theNorth

CarolinaRLF

ProfUe

The

BasicsThe

organizations thatoperateRLFs

inNorthCarolina are predominantly nonprofits (46

per-cent)andpublic sectororganizations (42percent).

Moreover, the

27

RLFs

thatrespondedtooursur-veyare relatively active lenders. Eighty-three

per-cent

had

made

aloan withinthelast sixmonths.In addition,

compared

to the other statesstudied forthisproject.NorthCarolina's

RLFs

are relativelymore

mature.The

largestshare ofRLFs

inNorthCarolinahave

been

operating for6to 10Chart1. Yearsin operation:N.C.

revolvingloan

funds

45%- 40%- 35%- 30%- 25%- 20%- 15%- 10%-

5%-1

0%-y

y

j^^^^^^SJJ

i

Sbll

^-1to5 6to10 IVbrethanIO

years. One-third ofall funds began operating in

the last five years; the oldest fund started lending

in 1981.

Finally,the vastmajority oforganizationsthat

operate

RLFs

in North Carolina operate a singlefimd (88 percent), while only 12 percent operate

multiple funds.

Compared

to the other statesstudied for this project. North Carolina ranks

among

the states with the smallest percentage ofRLFs

with multiple fimds.Where

theMoney Comes

From:

Sourcesof

RLF

CapitalThe

27RLFs

thatrespondedto oursurveyre-port$90.5million in total capitalfrompublic,

pri-vate, and philanthropic sources.

The

total capitalin the "economic development only"

RLFs

isal-most

$70 million.Based

on total capital reportedin its RLFs, North Carolina ranks fifth

among

theseven states surveyed as part ofthe Counting

on

LocalCapital project.

As

shown

in the following chart, the federalgovernment

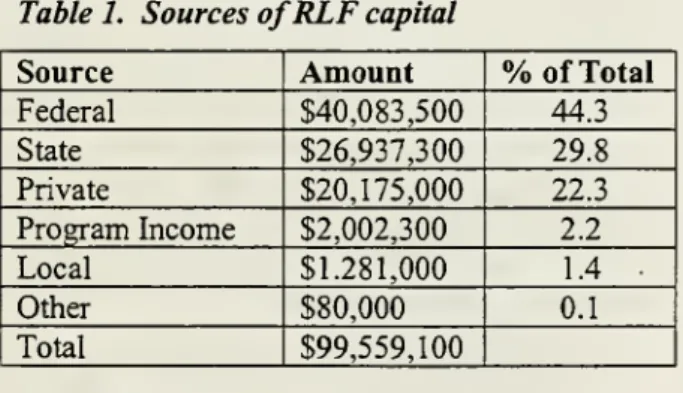

has beenthe largest source ofcapitalfor these RLFs.

As

indicated in the chart below,the federal

government

has mvestedmore

than$40 million inNorthCarolina

RLFs,

oralmost45percent oftotal capital.

The

second largest sourcehas been state government, with an investment of $26,937 milHon or almost 30 percent of total capital.

The

third largest source hasbeen

thepri-vatesector,

which

accountsforalmostone quarteroftotal capital.

Table1. Sources

of

RLF

capitalSource

Amount

%

ofTotalFederal $40,083,500 44.3

State $26,937,300 29.8

Private $20,175,000 22.3

Program Income

$2,002,300 2.2Local $1,281,000 1.4

Other $80,000 0.1

Total $99,559,100

Federal

funding

Among

federal fimders, the Department ofHousing

andUrban

Development

(HUD)

hasmade

the largest investment inRLFs

in NorthCarolina. Largely through

Community

Develop-ment

Block Grants(CDBG)

made

to EntitlementCities,

HUD

has contributed roughly $22.5mil-lion or

56

percent of all federal dollars in NorthCarolina

RLFs.

Other contributing federalagen-cies in decreasing order include the U.S.

Depart-ment

ofAgriculture, theEconomic Development

Administration, the Small Business

Administra-tion, andtheAppalachian RegionalCommission.

Itshouldbe noted thatthe Small Cities

CDBG

program

is also funded with federal dollars fi^omHUD,

but is administered at the state level. Forthis reason. Small Cities

CDBG

grants arein-cluded as part ofstate capital sources in the

sec-tionthat follows.

However,

ifSmall CitiesCDBG

dollars are included with federal sources,HUD's

shareoftotal capital increasesto$33.9million, or

almost 38 percent oftotal capital in North

Caro-lina

RLFs.

State

funding

The

role of stategovernment

in supportingRLFs

is one of the unique features of theRLF

industry inNorth Carolina.

As

noted intheafore-mentioned chart, state

government

sourcesmake

up

the second largest share of capital in NorthCarolina

RLFs. With

roughly equalsharescoming

fi^om General

Assembly

appropriations andCDBG

grantsmade

through the Small Citiespro-gram, the state

government

has invested $26.9million in North Carolina

RLFs

or almost 30per-cent of total capital.

Among

the seven statesstudied in Counting

on

Local Capital, NorthCarolina ranks

among

the leading three statesbased on the share of total capital contributed

firomstatesources.

Of

particular note is the role of the GeneralAssembly

in appropriating funds to capitalizeRLFs

in North Carolina. Since the late 1980s,when

the GeneralAssembly

appropriated funds tothe North Carolina Rural

Economic Development

Center to establish a microenterprise

demonstra-tion, the state has directly appropriated funds to

several of the state's leading

RLFs

as part of acomprehensive development finance strategy

aimed

at fillingcapitalgaps inNorthCarolina.Private sector

funding

Overall, private sources of capital

make

up

the third largest source ofcapital in North

Caro-lina

RLFs,

accounting for approximately 22per-cent oftotal capital.

The

largest source ofprivate capital isfoundations ($15.9 million or 79percentofprivate sources), followed

by

banks ($2.6lion or 13 percentofprivate sources).

Among

theother statesstudied forthisproject, onlyArkansas

has such a major foundation investment in its RLFs.

However,

the distribution ofprivate capital ishighly uneven across

RLFs

in North Carolina.The

state's largestRLF,

the Self-Help Ventures Fund,which

is one ofthe nation's leadingcom-munity development financial institutions, has a

total of almost

$16

million in private capital ormore

than three quarters of all capital in NorthCarolina contributed

by

private sources.Capital sourcesfortheaverage

RLF

inNorth

CarolinaThe

majority of the capital in the typicalNorth Carolina

RLF

comes

from state sources,augmented by

a significant portion of federaldollars, and a smaller portion ofprivate dollars.

This is portrayed in the graph below,

which

ex-cludes from analysis boththe Self-Help Ventures

Fund

and the four large publicRLFs

that fundbotheconomic development andhousing.

CapitalizationStructure

and

Trends

Size

of

RLFs

The

sizeofthemedian

RLF

inNorthCarolinais significantly larger than in any of the other

states studied forthisproject. Overall, the

median

size of

RLFs

in North Carolina is $1.3 million,witlia range in size

from

$27.9 million (theSelf-Help Ventures Fund) to $90,000 (Metropolitan

Low-Income Housing and CDC).

In fact, inno

other state

was

themedian

RLF

size larger than$1 million. Moreover, this finding is notdistorted

by

the presenceofahandfuloflargerRLFs. Even

excluding the Self-Help Ventures

Fund

and thefour

RLFs

that fund both housingand

economic development loans, themedian

RLF

size inNorthCarolina is still $1.2 million.

At

thesame

time,basedonthe seven statesurveysconductedaspart

ofthe Counting on Local Capital project. North

Carolina has a smallertotal

number

offunds thanallbutone otherstate.

There are several

key

implicationsthatfollowfrom the larger average size of

North

Carolina'sRLFs.

First, the state'sRLFs

may

be closer toachieving sustainability than the funds in other

states. Practitioners interviewed for this project

estimate that it takes a capital base of $3 to $3.5

million and an active loan portfolio ofatleast $2

millionto generateboththe revenuesnecessaryto

supportthe staffneeded to operate a

RLF

profes-sionally, and the

volume

of loans necessary toachieve areasonablydiversifiedportfolio.

Second, larger average fund size

may

alsolead to

more

efficientRLF

administration. For example, 83 percent ofNorth CarolinaRLFs

re-ported

making

at least one loan in the past sixmonths, a figure thatis the second highest

among

all otherstatessurveyedforthisproject.

Debt

vs. equityOverall, debtcapital totals$27.7million or31

percent of the total capital in North Carolina

RLFs.

The

largest source ofdebt capital isfoun-dation investments, followed

by

federal sourcesand banks.Tj^jically, foundation investments and

federal loans carry highly subsidized rates and

terms,

making

much

ofthisdebt "nearequity."As

with private capital, debt financing ofRLFs

in North Carolina is highly uneven.Ex-cludingthe Self-HelpVentures Fund, debt capital

makes up

only 18 percentoftotal capitalinNorthCarolina

RLFs,

themajorityofwhich comes from

the

USDA's

Intermediary RelendingProgram

(IRP).

Based

on

thisfindingtherewould

appeartobe significant opportunities for

RLFs

in NorthCarolina to use their equity capital to leverage

additionaldebtcapital.

Capitalneedsvs. capital availability

Despite capital resources

of

roughly $90mil-lion in North Carolina's

RLF

industry,respon-dents to our surveyindicated a greatneed for

ad-ditional capital. In fact, a total of 15

RLFs

inNorthCarolina reported a

combined

need of$19.3million in additional capital, or almost 25 percent

ofthetotal capitalbase of

RLFs

inthestate.Another 19

RLFs

in the state reported $11.7million inavailable capital for lending. While this

might appear a likely source for funds that need

additional capital, this level of available funds

may

also represent a prudent reserve of 10-15percent.

Where

tlieMoney

Goes:Loan

productsAt

the median, the averageloan sizereportedby

North Carolina'sRLFs

was

$51,500, with theloans ranging in size

from

$17,500 to $100,000.This average loan size'

was

the largestamong

allStates studied as part of Counting

on

LocalCapi-tal. Moreover, the

median

minimum

loan size($17,500)

was

higher than that reported in anyother state. If outliers such as the Self-Help

Ven-tures

Fund

and the four housing/economicdevel-opment RLFs,

are excluded, the average loan sizeand the

median

minimum

loan size both increaseto $63,250 and $20,000, respectively.^

Interest-ingly,

when

examining averageloansizebased onthe age of the fund, it appears that older

RLFs

tend to have lower average loan sizes thannewer

funds.

In terms of fmancing position, the largest

share of

RLFs

in the state (45 percent) offersub-ordinated financing.

Almost

one-third ofRLFs

(30 percent) offer primary fmancing. Another 25

percent of funds reported "other" positions,

in-cluding "gap financing" and "equal collateral."

However,

ofthe funds that offer primaryfinanc-ing, one-halfare

newer

fimdsthathavemade

theirfirstloan since 1990.

RLF

loan termsThe

averageRLF

in North Carolina offersloans at an interest rate of4.5 percent and aterm

of8 years. In addition, the vast majority of

RLFs

(75 percent) charged fixed rates

—

only a smallminority (7 percent) reported offering variable

rates.

The method

of establishing the interest ratevaried across

RLFs

in North Carolina andpro-vided

some

rather contradictory fmdings.Of

the23

RLFs

that responded to a question aboutwhat

kind of interest rate they charge, almost

40

per-centindicated charging a subsidizedrate.

Twenty-five percent of respondents indicated charging a

market rate.

Another

37 percent of respondentsreported charging a rate based

on

some

"other"formula, typically one based

on

the prime rateplus a certain percentage point or

some

otherun-subsidizedrate.

Ifone

combines

these "other" responses withthose charging marketrates, it

would

appear thatthe majority of

RLFs

in North Carolina do notsubsidize the interest rate charged for their loans.

However,

basedon

the responsesfrom

the eightRLFs

that reported the interest rate that theycharge, a

median

figure of4.5 percent, itwould

appear that

RLFs

inNorth

Carolinado

charge asubsidizedinterest rate. Thus,the data

on

whetherRLFs

in North Carolina typically charge marketor subsidizedinterestratesisinconclusive.

Businessestargeted

Existing businesses are the primary target of

North Carolina

RLFs.

Of

the 23 respondents (outChart2. Types

of

businesses targetedbyRLFs

inNorth

Carolinaofa total of

27 RLFs)

who

reported that theytar-get particular groups ofpotential borrowers, the largestpercentage (87 percent) indicated that they

target existing businesses.

At

thesame

time, alarge percentage ofrespondents (78 percent) also indicated that they target start-up businesses. In

addition,almost half (48 percent)ofthe

RLFs

that target particular groups of borrowers report thatthey target microenterprises. Further, while both

older and

newer

funds targeted start-ups andex-isting businesses fairly equally,

newer

fimdstended to target microenterprises

more

frequentlythan olderfunds.

Additionalproduct

demand

Sixty-eight percent of the respondents

indi-cated that the

most

commonly

requested productnot offered

by

NorthCarolina'sRLFs

was

ventureor equity capital. Despite this

demand,

though,there is ver>' little activity around venture or

eq-uity capital

among

the state's RLFs.Only

onefund that

was

identified, butwhich

did notreturnCFED's

survey, offers equity financing tobor-rowers. This fund, the Innovation Research

Fund

(IRF) ofthe NorthCarolinaTechnological

Devel-opment

Authority, is yet anotherexample

of acentrally-operating, state-initiated

RLF.

The

sec-ond most

frequentlyrequested servicenot offeredby

North Carolina'sRLFs

was

management

training, followedby worker

training.LendiBg

Activityand

Fund

Performance

Lending

activityRLFs

in North Carolinamanage

a currentportfolioofalmost$46 millioninloans andreport

cumulative lending activity of over

2000

loansworth

more

than $102million.On

amedian

capi-tal base of$1.3 million, the average

RLF

hasal-most

20 loans outstanding worth $763,729.On

acumulative basis,the

same

averageRLF

hasmade

33 loans for slightly

more

than $1 million.From

theperspective oftheaveragefund, itappearsthat

RLFs

inNorth Carolina are only barely revolvingtheir capital, if atall.

However,

excludingthe fourhousing/economic development

RLFs

(forwhich

there isalmost

no

lending data), North Carolina's"economic developmentonly"

RLFs

havemade

atotal of $101,874,615 loans, cumulatively,

on

slightly less than $70 million in capital. Thisseems to indicate that

some

of the state's funds.particularly largerfunds, are revolvingtheir

capi-taltoa

much

largerextentthanothers.Compared

to the other states in the Counting on Local Capital project,RLFs

inNorth Carolinaappear to be relatively effective lenders. For

ex-ample,

among

the sixstatesthatreportedcumula-tivelendingfigures,

RLFs

inNorthCarolinamade

the thirdhighest cumulative

number

ofloans andthe third highest cumulative dollar

volume

ofloans. This

was

accomplisheddespite the fact thatNorth Carolina contains a smallertotal

number

offimds than all but one other state and thatNorth

Carolina ranks fifth

among

the seven statesstud-ied in terms of total capital. In addition, North

Carolina

RLFs

reported the highestmedian

per-centage (73 percent) ofcurrent loan

volume

as ashareoftotalcapital.

Additional data

on

lendingactivity:•

Only

22 percent (6 out of 27)RLFs

haveloan loss reserves.

The

total accumulated inthese loan loss reserves across all

RLFs

inNorth Carolina

was

only $1,619,841—

orslightlylessthan 2percentoftotalcapital

re-ported.

• Credit tests

on

borrowers are verycommon.

Eightypercent of respondents indicated

per-forming

some

type ofcrediteligibility teston

prospectiveborrowers.

Delinquencies

and

defaultsBecause

there isno

standard definition ofde-linquencies in the

RLF

industry, surveyrespon-dents

were

firstaskedhow

they definedelinquen-cies.

Almost

two-thirdsofthe surveyrespondents(63 percent) reported a definition for delinquent

loans.

The most

common

definitions ofdelin-quency

were

equally splitbetween

"paymentsover 30 days late" (35 percent) and "payments over60 days late"(35percent).

In total, the

20

RLFs

that reported ondelin-quencies reported a total of 135 delinquent loans

valued at $2,523,030. Delinquency rates

among

individual funds rangedfrom

percent to 16.9 percent.The

aggregatedelinquencyrate for the 15RLFs

that reported at least one delinquent loanwas

4.8 percent; the aggregate delinquency rate for the20

RLFs

who

reported zero ormore

delin-quencies

was

4.3 percent.These

rates contrastfavorably

when

compared

with delinquency ratesamong

small banks. For example, basedon

pre-liminary data for 1998, thepercentage ofpastdue

and "non-accrual"commercialloans

among

bankswith

$300

million in assets or lesswas

5.22per-cent.^

Compared

with delinquencies, informationabout defaults

was

not reported as consistentlyamong

theRLFs

that responded to our survey. Infact, only

40

percent of the survey respondents(11 out of27) could provide a definition of

de-faults.

The most

common

responses ranged from60 days pastdue (25 percent) to 90 days pastdue

(16 percent) to 120 dayspastdue(25 percent).

Intotal, the 14

RLFs

thatreported on defaultsreported a total of 173 loans in default valued at

$1,614,062. Defaultrates

among

individual fundsranged from percentto 11.2 percent.

The

aggre-gate default rate for the 9

RLFs

that reported at least one loan in defaultwas

4.1 percent; theag-gregatedefault rate forthe 14

RLFs

thatreportedeither or

more

loansindefaultwas

3.5 percent.Performance measure:

Portfolio atriskThe

RLFs

reporting defaulted and delinquentloans providethe

raw

dataneededtocalculateoneofthe

most

importantperformance measures:per-centage ofportfolio at risk. In assessing the

vi-ability andsustainability ofthe

RLF

industry, itisessential that practitioners and fimders determine

the total

amount

ofthe capital that is currently at risk, eitherbecause of delinquencyordefault.The

chart above reveals that eight to nine percent ofthe capital base is currently at risk.

While

thisdoes not

mean

thatall thiscapital willbe lost, itisan important indicator for evaluating the risk of

RLF

portfolios and the level ofloan lossreservesthat are necessary to ensure that the industry's

capital baseisnot eroded. Currently, the loan loss

reserves totaling slightly less than 2 percent of

totalcapital areinadequatetoreplace the capitalat risk.

Technicalassistance

The commitment

to providing quality techni-cal assistance services to borrowers appearsrela-tively strong

among RLFs

inNorth Carolina.The

large majority of the state's

RLFs

(80 percent)provide

some

type oftraining or technicalassis-tance to borrowers.

The

servicemost

commonly

provided is one-on-one technical assistance (80

percent).

The

secondmost

frequently offered typeofservice

was

classroomtraining(40percent).Of

the 16respondentswho

reportedprovidingone-on-onetechnical assistance, almosttwo-thirds

also reported providing

some

other type ofserv-ice. This

would

suggest thatmost

funds providetechnical assistance, not simply as a cursory

service, but rather as an essential part of their

products and services.

However,

this ismore

characteristic ofthe

newer

flmds, as 75 percent ofthose funds offering

no

technical assistanceserv-ices

made

their firstloanin 1985 orearlier.RLF

management and

administrationRLFs

in North Carolina typically rely onrather limited staff and resources to accomplish

their mission.

Based on

information reported by11 of27 survey respondents, the

median

RLF

inNorth Carolina has one staffperson and an

oper-ating budget of $60,000 peryear. This falls inthe

middle ofthe

few

states in the project that couldprovidesignificantdata

on

this question.Despite these rather limited resources,

RLFs

in North Carolina typically provide the range of managerial and administrative tasks

common

toRLFs,

andby

and large,do

soin-house.The most

common

tasks provided in-houseby

NorthCaro-lina

RLFs

were

loan packaging (92 percent),fol-lowed by

receipt of loanpayments

and portfoliomanagement

(83 percent each). North CarolinaRLFs

use outside contractors to a lesser extent,although a significant portion contracts out for

loan closings (29 percent)

and

liquidations (25percent).

The

taskmost

commonly

not providedby

North CarolinaRLFs

was

underwriting (25 percent).Thismay

be areflection ofthe fact that,since a large share of

North

CarolinaRLFs

(45percent)typically take a subordinated position on

deals, lenders with the primary position are likely

performthe underwriting.

The

Impact

ofRLF

Lending

The most

common

measure

for assessing theimpact of

RLF

lendingon

individuals andcom-munities underserved

by

private fmancialinstitu-tionsisto

measure

jobcreationandretention. Thismeasure

is notoriouslydifficultto quantify, giventhe inherent complexity ofthejob creation

proc-ess and the difficulty ofisolating the importance

ofa single factor, even one as important as

capi-tal, in such a

complex

process. Nonetheless, jobcreationremains thebest

proxy

availabletoRLFs

for

documenting

the impact oftheirlending ontheeconomic

condition ofdistressed communities or individuals.Thus,this articlepresentsthisdataforNorth Carolina

RLFs

below, along withinforma-tion about the extent to

which

RLFs

in the statetarget different types of communities and

indi-vidualsthat

may

lack accesstocapital.Job

creationand

retentionThe most

common

impact measures usedby

North Carolina

RLFs

arejob creation (70 percentofsurvey respondents) and job retention (63

per-cent). Together, the

RLFs

who

responded to thesurveyand couldprovide data

on

job creationandretention helped to create 5,257 jobs and retain

another 5,793.

By

far, the leaderamong

thestate's

RLFs

was

the Self-Help Ventures Fund,which

reportedhelpingtocreate 1,580jobs andto retain3,605,almosttwo-thirds ofalljobs retainedby

RLF

lendinginNorthCarolina. In comparison,the typical

RLF

was

focusedmore

on

jobcreation than retention, reporting amedian

of 170 jobscreated and

46

jobs retained.Only

a handful ofNorth Carolina

RLFs

reported data onself-employment.

This

median

figure of 170 jobs created perRLF

inNorthCarolinawas by

far thehighestme-dian job creation figure

among

the six states inour study that provided significant data

on

jobcreation and retention.

However,

onemust

becautious in interpreting these figures. In addition

to the difficulties with reportingjob creation and

retentionmentioned above, it

must

also be notedthat only 56 percentof NorthCarolina survey

re-spondents actually reported data

on

job creationand only

44

percenton

job retention. In general,there is a great

need

toimprove

the definitionsand reporting

methods

for impact measureswithinthe

RLF

industry.Targetingstrategiesfor

RLF

borrowersThe

practice of targeting capital to specificgroups of borrowers is essential to a strategy for

reaching underserved entrepreneurs.

Not

surpris-Table2.

Borrowers

targeted:

(%

of

RLFs)

Low/Moderate

income:

83%

Women:

58%

Disabled:

17%

Minorities:58%

Youth:

4%

Other:

29%

ingly, in North Carolina almost all

RLFs

target their lending to potential borrowers in particularunderservedgroups. In fact, only

two

respondents(7 percent) indicated that they did not practice

some

kind oftargeting.The

groupmost

likely tobe targeted

was low

to moderateincome

borrow-ers (83 percent).

Women

and

minorities (58per-cent each)

were

alsocommon

targets ofRLF

lendinginNorthCarolina.

Conclusions

ThisprofileofNorthCarolina's

RLF

industryleadsto a

number

ofbroadconclusions:In

North

Carolina,RLFs

area $90

millionindustry. Together,

on

a capital base of $90.5million,

RLFs

in North Carolina havemade

over2000

loans worth over$102

million.As

a resultofthis lending, these

RLFs

have helped to retainalmost 5,800jobsandcreateanother5,200.

Unlike

most

other states,North

Carolina'sRLF

industry hasa

unique

structure that is, inlarge part, aproduct

of

stategovernment

policyand

funding.While

most

states have a largenumber

ofrelatively smallRLFs,

North Carolina hasa fairly smallnumber

offundsthat are larger in size.With

amedian

loan fundsize of$1.3mil-lion.

North

Carolina's funds are,on

average,sig-nificantlylargerthan the

RLFs

in any oftheotherstatesstudiedforthisproject.

Moreover,

much

of the resources in theseRLFs

areconcentratedinafew

fundsthatoperatestatewide

and

havereceived significantresourcesfrom

the stategovernment.This includestheSelf-Help

Ventures Fund, the state's largestRLF,

whose

rapidgrowth hasbeen

aidedby

state gov-ernmentresources, including a multi-milliondol-larappropriation in 1995. This alsoincludes both

the Microenterprise

Loan

Program

of the NorthCarolina Rural

Economic Development

Centerand the Capital Support

Loan Fund

ofthe NorthCarolina Minority Support Center, each of

which

was

initially created with a GeneralAssembly

appropriation and operates statewide through a

network

of local organizations. Finally, this listcontains the large

Community

Development

Block

Grant(CDBG)

RLF

at the Department ofCommerce

Finance Center,which

hasgrown

rapidly as the result ofa

key

policy decision intheearly 1990s. Since 1992,allunitsoflocal

eminent have been required to return all

repay-ments from loans

made

to private companiesus-ing

CDBG

funds to theCommerce

FinanceCen-ter. Previously, these repayments had

been

usedby

some

local governments to create theirown

RLFs.

There is

some

evidence that the uniquestructure

of North

Carolina'sRLF

industryhasledtogreaterlendingefficiency. First ofall, on a

very basic level, almost all of

RLFs

in NorthCarolina are active. Eighty-three percent reported

making

at least one loan in the past six months, a figure that is the second highestamong

all otherstates surveyed as a part of this project. Second,

these funds are

making good

use oftheir capital.RLFs

inthestate reported the highestmedian

per-centage (73 percent) ofcurrent loan

volume

as ashare oftotal capital. Third,

among

the six statesthat reported cumulative lending figures,

RLFs

inNorth Carolina

made

the thirdhighest cumulativenumber

ofloans and the third highest cumulativedollar

volume

of loans. Thiswas

accomplisheddespite the fact that

North

Carolina contains asmaller total

number

of funds than all but oneother stateand that thestate ranksfifth

among

thesevenstatesstudiedintermsoftotalcapital.

Finally, with a larger

median

loan fund size ($1.3 million) than in all the other states studiedfor this project. North Carolina's

RLFs

may

beclosertoachievingsustainability thanthe fundsin

those other states. Practitioners estimate that it

takes a capital base of $3 to $3.5 million and an

active loanportfolio ofatleast$2 million to

gen-erate both the revenues necessary to support the staffneeded to operate a

RLF

professionally andthe

volume

of loans necessary to achieve area-sonablydiversified portfolio.

But, hasgreater efficiency ledtoless equity?

The

flip side ofNorth Carolina'sRLF

industry,which

is characterizedby

relatively larger,poten-tially

more

efficient funds, is the fact that there are fewer ofthem.While

this survey could notdetermine whether access to

RLF

capitalwas

relatively

more

uneven

across North Carolinacompared

with statesthathave

hundredsoffimds,such a fmding is not inconceivable. Moreover, North Carolina's typically larger funds carry the

highest average loan size ($51,500) of all the

states studied.

While

this loan size is still notwithin the range typically offered

by

commerciallenders, does this

mean

thatsome

smallerborrow-ers in the target markets ofthese funds are not

being served?

These

are questions that call for further inquiry.In order to continue growing, the state's

RLF

industrymust overcome

some

fundamental

barriers related to its unique structure.

The

handful of larger funds that dominate the state's

industry

and

havebeen

theprimarybeneficiaryofdirect state funding and policy support tendto be

high-performing,

have

a diversified capital base,and revolve their capital.

On

the other hand, therestofthe fundsinNorthCarolina's

RLF

industrydo

nothave avery diversified capitalbase and,on

average, are only barely revolving their capital, if

atall.

Building North Carolina's

RLF

industry willrequire a two-pronged strategy that will require

both increasing the total

amount

ofcapital in theindustry and, at the

same

time, building theman-agement

capacityand

sophistication oftheaver-age fund.

RLF

practitioners and statepolicymak-ers should consider a formal intermediary or

in-dustry associationto carry outthisstrategy.

Increasing the

Amount

of

Capital in NorthCaro-lina RLFs.

The

North CarolinaRLF

profilere-vealed asignificant

demand

foradditional capital.While

the state'sRLFs

appear to be, on average,more

efficient thatRLFs

inotherstates, thestate'sindustry is relatively small, even after adjusting

for population differences.

Among

the sevenstates studied for the Counting

on

Local Capital project, North Carolina ranked fifth inRLF

dol-larspercapita.

One

possible strategy for increasing theamount

ofcapitalinNorthCarolina'sRLFs

would

be to explore the creation of

mechanism

to poolexisting fiands so thatthey canbe used

more

effi-ciently and effectively. In order to explore this

possibility, the survey asked

RLFs

if theywould

supportthe creation ofa regional or statewide

in-termediary or support organization to deliverthis

typeofservice.

While

the responses in North Carolinawere

notquiteas enthusiastic asinother states,there

stillappearstobesignificant interest insucha

concept.

Given

this interest, the state'sRLF

prac-titioners should

now

considertheestablishmentofTable3.

Ranking of

needsinsurvey

(%

of

respondents ranking)"mostimportant" "second

most

important"

Data

Collection35%

10%

Portfolio

Management

16%

11%

Asset

Management

6%

0%

Policyand

Advocacy

10%

5%

CapacityBuilding

19%

33%

Evaluation

5%

25%

Secondary

Market

16%

21%

a

more

formal institution—

whether aninterme-diary or a tradeassociation

—

to assisttheindus-try.

With

the need for additional capital farout-weighing available capital

among

the state'sRLFs,

though, such aninstitution shouldfocus onmuch

more

thanjustre-allocating existingcapital.Rather, this

new

institution should have a broadmission that

would

include both increasing totalcapital in the state's

RLFs

and

building theman-agement

capacityofthestate'sfunds.Increasing the

Management

Capacity in NorthCarolina

RLF.

In considering strategies forin-creasing the capital in

North

Carolina'sRLFs,

whether

by

accessingnew

sourcesofcapital, suchas private

bank

capital or secondary markets, orby

utilizingnew

types of capital, such as debtcapital, one important consideration

must

not beoverlooked. All ofthese strategies will require a

new

level ofstandardization in loan underwritingand documentation procedures across

RLFs

inNorthCarolina.

For the

most

part, the North CarolinaRLF

profilerevealedthattheperformance ofthestate's

average fund lags behind the small cluster of

in-dustry leaders. Nevertheless, in a state with

rela-tively

few

funds, these funds are critical inen-suring equitable access to

RLF

capital across thestate.

Of

course, the state's average funds areby no

means

unsophisticated.For

example,compared

with the

RLFs

in the other states studied for thisproject. North Carolina's

RLF

reportedsome

ofthe highest levels

of

computer technology usagein datacollection. Yet,

when

asked abouttheim-portance of various support services needed to

improve

RLF

performanceand impact,oursurveyrespondents indicateda

number

ofneeds.The

needmost

frequentlymentioned as either"most

important" or "secondmost

important"by

respondents (52 percent)

was

capacity building.Assistance with data collection (45 percent) and

secondary markets (37 percent)

were

alsomen-tioned frequently

by

respondents as themost

im-portant orsecond

most

important need.These findings reinforcethe

need

fora formalmechanism

—

whetherinstituted in a tradeasso-ciation or intermediary

—

to build themanage-ment

capacity of the state's fundsby

capturingand

sharing the expertise of industry leaders inNorthCarolinaandnationwide,

^jj^

Endnotes

' Throughoutthisrqjort,

when

referenceis

made

tothe"average loansize"of NorthCarolinaRLFs,this refers to

—

moreprecisely—

themedianoftheaverage loansizeofall27

RLFs

includedinthis study.We

usethisabbreviatedterminologytomake

the textmorereadable.^Partofthereasonforthislarger

minimum

sizeof loansisthatmostofthestate'smicroenterpriseprogramscountasone

RLF

undertheRuralCen-ter'sMicroenterpriseLoanProgram.

^

FRBSF

EconomicLetter,"New

View

ofBank

Con-sohdation,"FederalReserve

Bank

ofSanFran-cisco,