KILLER APP OR KILLED BY GREED?

VC AND MANAGER TIME ORIENTATION IN IPO FIRMS

David Halliday

A dissertation submitted to the faculty at the University of North Carolina at Chapel Hill in partial fulfillment of the requirements for the degree of Doctor of Philosophy in the Strategy and

Entrepreneurship program in the Kenan-Flagler Business School.

Chapel Hill 2017

ABSTRACT

David Halliday: Killer App or Killed by Greed? VC and Manager Time Orientation in IPO Firms Under the direction of Richard Bettis

ACKNOWLEDGEMENTS

Thank you to all of my dissertation committee members, Rich Bettis, Olga Hawn, Scott Rockart, Jeff Edwards, and Hugh O’Neill for their ongoing efforts to assist me on this

TABLE OF CONTENTS

Chapter One: Introduction ... 1

Importance to Strategy ... 2

Dissertation Goals ... 3

A History of Time Orientation ... 4

Chapter Two: Literature Review Part I - Time Orientation Characteristics ... 9

Time as a Strategic Construct ... 9

Costs of Managerial Myopia ... 11

Benefits of Temporal Myopia ... 16

The Effect of Myopic Ownership ... 18

Chapter Three: Literature Review Part II - Venture Capital Horizon and IPOs ... 23

Venture Capital Introduction ... 23

VC Contributions to Portfolio Firms ... 25

VC Myopia & Long-Termism ... 27

Time Orientation and Firm IPOs ... 30

Chapter Four: Theory and Hypothesis Development ... 32

Project Selection ... 33

Owner and Manager Interactions ... 35

Venture Capitalists ... 36

Hypotheses ... 37

Chapter Five: Data, Methods, and Results ... 43

Methods ... 52

Results ... 52

Discussion of Control Variables ... 54

Response Surface Discussion ... 58

Robustness Checks ... 59

Chapter Six: Discussion and Conclusion ... 62

Discussion of Empirics Part I: Manager Orientation ... 63

Discussion of Empirics Part II: VC Orientation ... 66

Contributions ... 68

Limitations ... 69

Conclusion ... 71

APPENDIX 1: TABLES ... 73

APPENDIX 2: FIGURES ... 79

LIST OF TABLES

Table 1: Construct Definitions ... 73

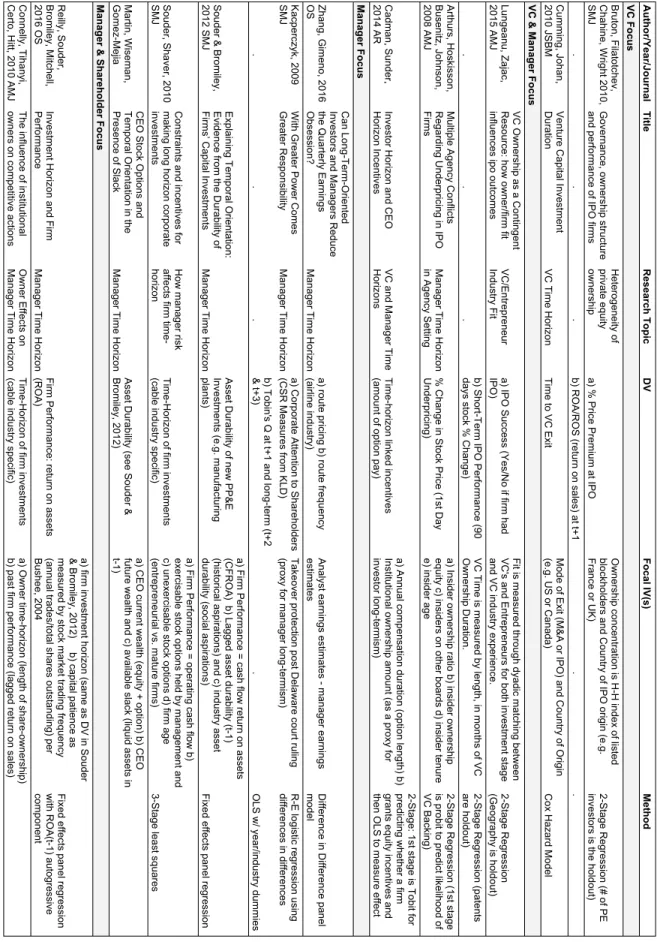

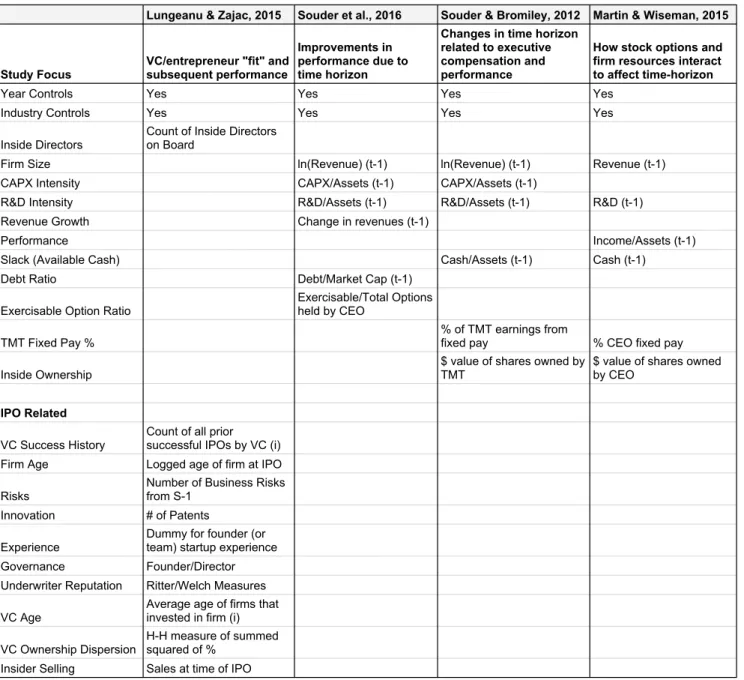

Table 2: Relevant Time Horizon Studies Analyzing Topic, DV, and Method ... 74

Table 3: Choice of Study Controls for Closely Related Time Horizon Studies ... 75

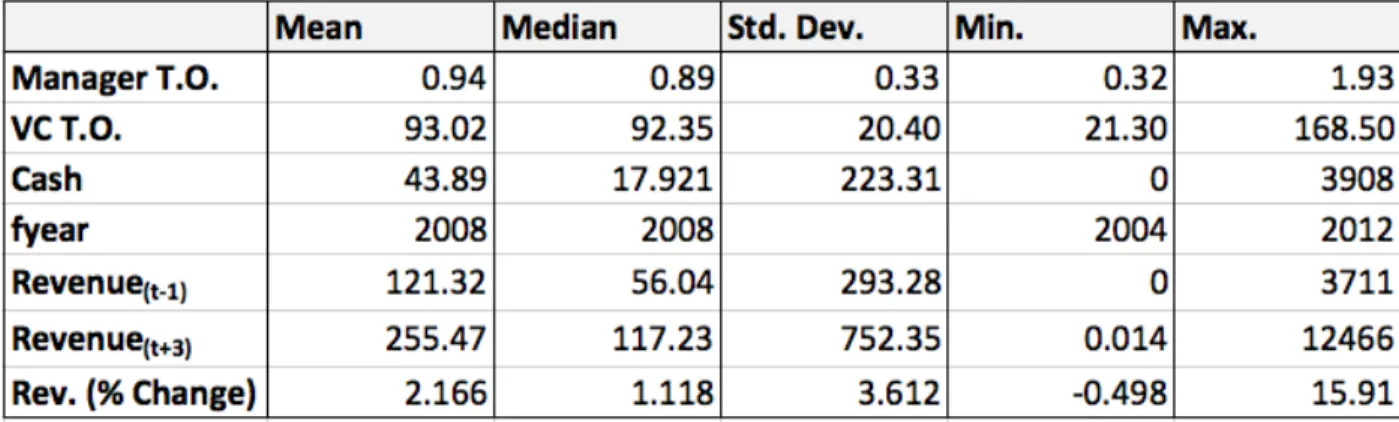

Table 4: Data Summary ... 76

Table 5: Correlation Matrix ... 76

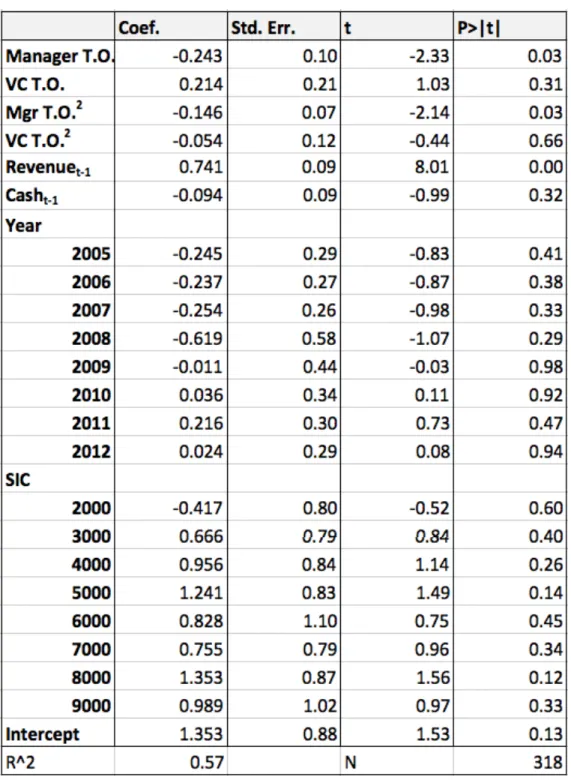

Table 6: Focal Study Results ... 77

LIST OF FIGURES

Figure 1: Hypothesized Manager Horizon Effect on Change in Firm Performance ... 79

Figure 2: Hypothesized VC Horizon Effect on Change in Firm Performance ... 79

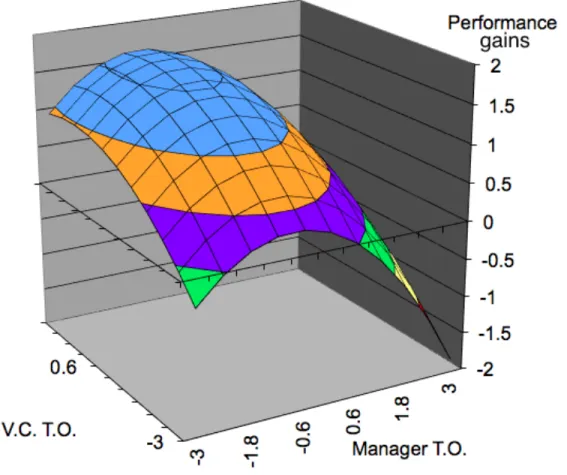

Figure 3: Hypothesized Response Surface of Dual Effects of VC and Manager Horizon on Firm Performance ... 80

Figure 4: Focal Model Manager Effect ... 81

Figure 5: Focal Model VC Effect ... 81

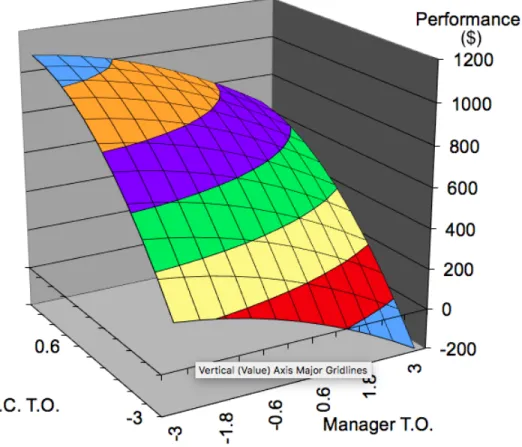

Figure 6: Focal Model Response Surface ... 82

Figure 7: Robustness Test Response Surface ... 83

Figure 8: Robustness Test Manager Effect ... 84

LIST OF ABBREVIATIONS

BTOF The Behavioral Theory of the Firm CAPEX Capital Expenditures

CAPM Capital Asset Pricing Model CEO Chief Executive Officer ETF Exchange Traded Fund

GAAP Generally Accepted Accounting Principles IO Institutional Owner

IPO Initial Public Offering IRR Internal Rate of Return

LIWC Linguistic Inquiry Word Count M&A Merger and Acquisition

NASDAQ National Association of Securities Dealers Automated Quotations NPV Net Present Value

NYSE New York Stock Exchange R&D Research and Development

Chapter One: Introduction

“The qualities most useful to ourselves are… self-command, by which we are enabled to… endure present pain in order to obtain a greater pleasure in some future time.”

-Adam Smith, 1759

Humans often make poor choices when facing decisions with inter-temporal trade-offs. These decision inconsistencies are exacerbated when choices that contain instant gratification are pitted against those with distant payoffs (R. Thaler, 1981). Quite literally, we appear to be of two minds on these issues. Adam Smith, highlighted how lack of “self-command” between our present selves and our future selves led to poor planning and suboptimal investments in future utility (Smith, 1790). This tension between present and future, or current self and eventual self has become known as the “dual-mind” perspective on individual decision making. Researchers in a number of fields such as economics (Schelling, 1984), behavioral economics (Thaler, 1981), and strategy (Souder and Bromiley, 2012; Souder et al., 2016) have struggled to reconcile

persistent observations of sub-optimal short-term decision making—among individuals and executives alike—with normative theories about utility and profit maximization.

short-term payoffs offer salient examples of myopia, whether in the accounting cover-ups at Enron or Lehman Brothers, the slow demise of Zynga due to a refusal to invest in R&D1, or the recent illegal packaging of loans by Lending Club2. These processes can have been seen in each of the past few decades, with each decade providing characteristic glimpses of the negative effects of short-termist behavior. In the 80’s a wave of short-termism swept American business due to the rise of hostile takeovers (Porter, 1992). In the 90’s the dot-com bubble showed how short-sighted, lofty aspirations can lead to firm underperformance (Kim and Bettis, working). Finally, in the 00’s, short-termism like that found during the Countrywide mortgage scandal— where strong short-term sales incentives led to the firm’s collapse—preceded the largest financial crisis in nearly a century.

Importance to Strategy

Indeed, business strategy is an inherently time-oriented task (T. K. Das, 1987). When entrepreneurs define a new market opportunity, exploring and exploiting this opportunity

requires investments that have both heterogeneous paybacks and heterogeneous payback periods (Souder & Bromiley, 2012). Superior performance comes from selecting the investment

opportunities that optimize profits and the timing of the realization of those profits. Making non-optimal short-term investments may provide abundant capital at the expense of higher returns. But on the other hand, a potentially profitable business may not be able to realize those profits if they run out of liquidity first. Since managers will have different time orientations, I will refer to these differences as time orientation heterogeneity.

Venture capital (VC) provides an excellent setting to study the effects of owner time

orientation on firm performance. VC funds have contractually defined durations (Sahlman, 1990) that typically must be exited after 10 years. In addition, VC firms tend to invest substantial parts of their fund with each portfolio company. This results in concentrated ownership where

entrepreneurial firms have relatively few—and easily identifiable—substantive owners. Therefore, VC investments offer what is effectively a laboratory to study owner and firm time orientation. Likewise, examining IPO firms offers an excellent research setting because IPO firms relatively have few owners and typically only one product line. In about 40% of my sample, the IPO firm is still led by a founder, indicating a high degree of institutional and cultural continuity.

Dissertation Goals

supported and which related theories appear to explain why some evidence suggests alternative conclusions.

A History of Time Orientation

Time-based behavior may have evolved out of optimal animal foraging behavior (Carter, Pedersen, & McCullough, 2015) where tradeoffs between exploiting what remains of a current patch of resources or exploring for a new patch of resources are critical for survival. Thus, time orientation is critical factor in understanding resource gathering, accumulation, and consumption.

As a distinct construct, time orientation began to emerge in the strategy and management literatures in the early to mid-1980's (T. K. Das, 1987; Tushar Kanti Das, 1984; Laverty, 1996). These new academic inquiries reflected changed trends within the business world. The 1980's are often called the "deal decade" (Blair, 1993) because of the dramatic increase in brash raids, hostile takeovers, and high-leverage re-financings. Whether due to corporate raiders or simply impatient investors, managers began to feel stronger pressures for short-term performance. The average length of time that investors held stocks fell from 7 years on average in 1960 to 2 years by 1985 (Porter, 1992). Further, the amount of institutional ownership had grown rapidly in the previous decade. Institutional investors created pressures on US managers to make decisions that sacrificed long-term value to meet short-term goals (Laverty, 1996; Porter, 1992). These

pressures led management to act in ways inconsistent with the best long-term interests of their firm (Stein, 1988).

As a result, American companies were thought to be under-performing due to their widespread inability to invest in long-term projects (Porter, 1992). This perception led to

firms that did invest heavily in long-horizon investments risked getting acquired before the stock price rose to better reflect fundamental value (Drucker, 1986b). Indeed, by the end of the decade, Lorsch and Maclver, in their book on the current state of corporate boards, reported that 99% of directors had encountered a decision between maximizing stock value and acting in what would be the long-term interest of the company (Lorsch & MacIver, 1989). A survey of CEOs of major corporations found that 82 out of 100 blamed the stock market's focus on quarterly earnings for contributing to a decline in firm time horizon (Drucker, 1986b).

This led to a good deal of navel-gazing in both the popular and academic presses. In 1984, Business Week said that short-term institutional owners act as a "Damoclean sword" hanging over companies heads, forcing executives to "keep earnings on a consistently upward track" (Business Week, 1984). Leading scholars and practitioners such as Michael Porter and Peter Drucker weighed in on the issue. Porter wrote a seminal paper called "Capital Choices: Changing the Way America Invests in Industry" in 1992 to identify the causes and consequences of short-termism in American business. He called corporate investment "the most critical

determinant of competitive advantage" and was particularly pessimistic about American business' reluctance to invest in critical soft skills such as employee training while at the same time engaging in large value-destroying mergers. This led him to question not only US firms’ sense of time orientation, but also the very systems used to allocate capital (Porter, 1992).

long-term, relationship-based capital in Japan and Germany. Pundits have suggested that, since relationship-based bank capital is long-term in nature, it therefore fosters long-term strategic thinking (Black & Gilson, 1998). Japanese and German banks play a more central role in the businesses they finance than do their American counterparts, helping guide firm strategies consistent with both their long-term financing and the firm's strategic goals (Aoki, 1995). These banks often even have board seats emphasizing their governance responsibilities and intertwined financial interests. However, US banks are explicitly prevented by the Glass-Steagall Act from exercising control over companies they own or lend to (Jensen, 1989). Critics have charged that the reduced reliance on long-term private bank financing in favor of public equity financing increases managerial susceptibility to stock market pressures (Porter, 1992). In short, through the 80's, there was a strong perception that American firms were being performed and out-invested by Japan and Germany and that this commitment to investment and performance was due to their long-term orientations.

component and a short-term speculative component (Scheinkman & Xiong, 2003). Kim and Bettis (working) demonstrated a similar conceptual argument using M&A decisions to understand how managerial behavior changes during bubbles.

The focus on accounting fraud also stands out during this time period, in both the

academic and popular consciousness; for example, Enron epitomizes the short-termism inherent to the late 90's. Most accounting fraud is thought to be a symptom of managerial short-termism, often arising out of missed quarterly earnings, and the resulting pressures to meet expectations (Halliday et al., working). In Enron's case, the eventual bankruptcy came from a fundamental misalignment between their goals of generating new asset markets and their short time horizon for executing these goals.

Sarbanes-Oxley was a regulatory reaction to the dot-com excesses which led to more scrutiny of firms' accounting policies, leading in turn to more long-term oriented strategic decisions (Cohen, Dey, & Lys, 2008). In addition, clawback provisions allowed for retroactive judgments to be made against former CEOs if their financial statements were subsequently determined to be fraudulent. Thus, the intent was to make their strategic decisions long-term in nature. Predictably, the lead-up to the financial crisis followed the same pattern but in a different industry. Both consumer and investment banks offered a number of short-term incentives to make long-term decisions. Countrywide offered immediate bonuses for the sales of subprime mortgages, decisions which over the long-run, actually just four years, led to Countrywide's bankruptcy. Since the financial crisis, academic interest in time horizon research has exploded in the management literature (Souder et al., 2016). In examining the history of time horizon

In short, much of the academic history of time orientation assumes a distinction between "instant gratification" and a more long-term oriented "optimal resource allocation" perspective. This can be reductively called the inherent tension between greed and patience. In his Theory of Moral Sentiments, Adam Smith wrote of "two-selves" pitting present desires against greater future pleasures (Smith, 1790). In their early work on hyperbolic discounting, Thaler and Shefrin reinterpreted Smith's sentiments as two distinct drives: a "myopic doer" and a "farsighted

Chapter Two: Literature Review Part I - Time Orientation Characteristics Time as a Strategic Construct

Recent management literature has examined the antecedents, consequences, and effects of time orientation on firm performance. At first, this literature was primarily theoretical (T. K. Das, 1987; Tushar Kanti Das, 1984; Porter, 1992; Stein, 1988), but scholars have begun to empirically study the phenomenon in accounting (Bushee, 1998, 2001), finance, and strategy (Gaspar, Massa, & Matos, 2005; Souder & Bromiley, 2012). However, there are still lingering questions about how time should be treated within the literature. Is time merely a component in investment calculations such as net present value (NPV) or internal rate of return (IRR)? Is it a component of investment risk as hypothesized in behavioral finance (Kahneman & Tversky, 1979; R. H. Thaler & Shefrin, 1981)? Or does time represent a dynamic component of aspiration levels, as in the behavioral theory of the firm (BTOF) (Cyert & March, 1963)?

To best examine the time-horizon construct, I will define three constructs (table 1) and then examine how manager time-horizon has been studied in prior literature (table 2). The three relevant constructs are time horizon, temporal orientation, and short-termism. Time horizon refers to the time-period related to firm decisions. It is defined as the collective ex ante managerial expectation about the duration of time over which potential firm investments will generate productive returns (Souder & Shaver, 2010; Reilley et al., 2016). It is critical to note that time horizon is a firm level construct aggregated from the preferences of individual

investments (Marginson & McAulay, 2008; Sanders & Hambrick, 2007; Souder & Bromiley, 2012). Time horizon is tightly tied to a firm's investment horizons (Reilly et al., 2016).

Effectively, time horizon is the "when" of firm aspiration levels and guides the strategies taken to achieve those aspirations. This framework helps put time orientation in context with prior behavioral theories such as BTOF and prospect theory (Cyert & March, 1963; Kahneman & Tversky, 1979). For example, in traditional aspiration level theory, firms adjust their strategy in response to relative changes in historical and competitor performance. In a classic BTOF framework, this helps explain the relationship between firm performance and subsequent firm risk-taking. Likewise, managers use temporal and strategic reference points to guide their

decisions. Using the temporal framework helps explain empirical observations about risk-taking, specifically the asymmetry between strategic actions undertaken in the loss vs. gain frameworks (Andersen, Denrell, & Bettis, 2007; Bowman, 1980). In both frameworks, time horizon can act as an additional explanatory variable that accords with existing behavioral theory. Therefore, instead of simply explaining the amount of risk undertaken, as in existing theories on reference points, time orientation can be integrated with pre-existing theories to explain not just what type of risk managers undertake, but also when these risky investments are expected to pay off.

On the other hand, temporal orientation (also time orientation) is a construct more deeply rooted in individual psychology. It relates more to psychological outlooks of individual

managers at the firm level (Souder and Bromiley, 2012). Time orientation is not a static or homogeneous characteristic of a firm. Rather, it is sensitive to dynamic conditions both internal and external to the firm (Souder & Bromiley, 2012). Within the firm, managers themselves may hold heterogeneous time perspectives, such as a desire for short-term projects that have strong early cash-flows versus long-term projects that require upfront research costs. Indeed, a CEO’s personal time preferences may not even match the time orientation of her firm's strategy. Further, time orientations can conflict not only among agents, but also between principals and agents. For example, firm owners may desire longer-horizons in exchange for higher potential profits, while managers may seek short horizons in order to lessen employment risk. Thus, a firm's time orientation at any given point in time can be thought of as the result of a culturally-mediated and negotiated consensus among managers, owners, and other prominent stakeholders (Cyert & March, 1963; Hofstede, 1993).

Finally, short-termism (also myopia or hyperbolic discounting) is defined as “a preference for actions in the near term that have detrimental consequences for the long term (Marginson and McAulay 2008, p. 274). Laverty (1996) describes this process as the extent to which investment actions aim at desirable near-term outcomes at the expense of longer-term outcomes (Laverty, 1996). In a short-termism framework, decision makers give up favorable long-term projects to engage in "demonstrably suboptimal" short-term projects (Jackson & Petraki, 2011: 11).

Costs of Managerial Myopia

chosen orientation and its competitive environment. This mismatch can occur in one of two ways. First, firms can have ex ante time orientations that are thought to be optimal, but do not ultimately match the business environment. Second, firms can have ex ante time orientations that are known to be sub-optimal, yet still are acted upon. In the context of this research, this

conception could include VCs who encourage a portfolio firm to IPO before they are ready so that the VC can yield positive returns for their investors.

Since longer time orientations tend to result in improved performance, shorter (myopic) orientations tend to reduce performance (Laverty, 1996). Executives may forego more profitable but longer-to-profitability investments such as R&D in exchange for less profitable but also less delayed investments such as marketing (Stein, 1989). While managers may have optimum time orientation preferences, compensation incentives and other stakeholder pressures can encourage managers to behave in a myopic fashion.

Myopic behavior may lead to a self-fulfilling cycle of short-termism and poor performance. In other words, myopic strategic behavior may not only lead to poor future earnings, but may also strengthen the need to engage in ever-more myopic behaviors in the future. As Daniel Vasella, former CEO of Novartis, said, "Once you get under the domination of making the quarter--even unwittingly--you start to compromise in the gray areas of your

business, that wide swath of terrain between the top and bottom lines. Perhaps you'll begin to sacrifice things such as... improvements to your products, customer service, [and] employee training... that are important and that may be vital for your company over the long term" (Leaf & Vasella, 2002).

CEO Myopia Effects: Hyperbolic Discounting

intertemporal choice in particular (Maccrimmon & Wehrung, 1986; March & Shapira, 1987). A key component of time orientation is its complex association with perceived and actual risk as well as executive attitudes to risk-taking. The simplest and most well-studied empirical

phenomenon is that executives and non-executives alike change their discounting rates over time relative to a stable exponential function (R. Thaler, 1981). A salient managerial example would be the decision to cut (or not) R&D programs in order to meet current profit targets. This decision would have a high short-term payoff because R&D must be expensed in the year in which it occurs, per GAAP regulations. However, the high long-term costs come in the form of lost NPV-positive projects for which the R&D was intended.

Thus, payoff horizon itself becomes a form of risk independent of other sources such as cash flow volatility, likelihood of project success or failure, performance relative to competitors, or asymmetry between gains and losses (Dasgupta & Maskin, 2005). Payoff horizon risk stems from two potential sources. First, employment risk occurs because managers may be fired before the long-horizon projects they have approved begin to pay off. Second, managers must accept additional risk since payback uncertainty increases as time horizons increase.

takeover. Corporate governance scholars refer to this as "governance by trading" (Edmans & Manso, 2011).

CEO Myopia Effects: Cognition & Compensation

However, a monolithic characterization of decision makers as merely myopic is

insufficient to explain managerial behavior. Decades of cognitive research into management has shown that managers have dynamic attitudes toward risk. For example, managers act in a risk averse manner, but believe they can control risk over time by gathering market intelligence and "changing the odds" in their favor (March & Shapira, 1987, p. 1414). Further, managers may have incentives to engage in long-horizon projects in order to push the results of those projects into the future. This means—in the context of intertemporal choice—that managers may in fact hold inconsistent views on time orientation. On the one hand, longer time orientations create employment and payback risks, but on the other hand, longer-time orientations allow managers to manage risks over time and thus promote long-term projects as opportunities that are

perceived to have fewer risks (Pepper & Gore, 2015).

managers reduce their employment risk by investing in fewer revenue generating projects (Asker, Farre-Mensa, & Ljungqvist, 2014). Likewise, managers with short-term earnings pressures will cut R&D spending (Bushee, 1998), engage in corruption (Salter, 2012) and commit accounting fraud {Halliday et al., working}. The evidence for this need not come solely from archival sources. In a 2005 survey, 78% of CEOs admitted they would give up long-run value in order to meet short-run earnings targets (Graham, Harvey, & Rajgopal, 2005).

One of the antecedents to these managerial behaviors is the structure of CEO and top manager incentives. Agency theory (Jensen and Meckling, 1976} suggests that option and equity compensation packages align manager and owner goals. Long-term option compensation plans have become the most common way to align compensation with long-term firm performance (Hoskisson, Hitt, & Hill, 1993). Other forms of compensation schemes are thought to lead to shirking (cash pay) or short-termism (annual bonuses) (Souder & Bromiley, 2012). However, option pay has a dynamic time component to it as options approach exercisability and/or new options are issued.

reduced market share when more strategic competitors moved to fill the missing capacity. Finally, executives invest less in "soft" assets such as social responsibility and stakeholder engagement when compensation policies offer short-term incentives (Flammer & Bansal, 2015). Further, options have the unintended consequence of increasing the riskiness of CEO behavior. An increase in stock uncertainty increases the value of the volatility component of the stock option. Thus, option pay contracts—even when in line with traditional agency theory views— encourage strategic or tactical actions that add to the "speculative component of stock prices" (Bolton et al., 2006).

Benefits of Temporal Myopia

The debate around the effects of short-termism has been characterized by a number of paradoxes where time appears to have both enhancing and detracting effects on firm

performance. While the large majority of evidence points to a causative link between myopia and underperformance, some scholars have proposed counter-claims, which make one of four

arguments: 1) the argument itself is misspecified; 2) managers are not myopic and hence actually make optimal decisions given environmental conditions; 3) myopia can confer competitive advantages; 4) Long-term decisions might be suboptimal.

[invest fully] may be a condition for the level of long-run performance" (Schumpeter, 1994, p. 83). In other words, the necessity to retain firm capital and resources may require the firm to make myopic investments in order to retain optionality (real options) in future investments (McGrath, 1999). Thus, what may appear to be suboptimal in isolation is actually optimal in aggregate.

Second, it could be that firms are not actually myopic in their orientation. Gilson argues that stock market pressures--especially the market for corporate control--ensure that firms make optimal long run investments (Gilson, 1996). Following in the efficient market tradition, both Jensen and Stein contend that managers may be myopic but markets are not (Jensen, 1986; Stein, 1989). In other words, they grant that individual managers may be irrationally myopic, but that these managers are disciplined by market forces. As a result, they make value maximizing decisions. The competitive nature of the markets, therefore, ensures that managers make optimal intertemporal choices. Further evidence that neither managers nor owners are myopic comes from studies showing that stock markets react positively to the announcement of long-horizon projects (Woolridge, 1988).

Third, strategic short-termism may confer competitive advantages. Whether and when a firm decides to explore new knowledge instead of exploiting existing opportunities is critical to understanding the impact of time orientation on a firm. Rapidly transitioning from exploration to exploitation of a new product can give firms first-mover advantages or a sequence of temporary advantages (Forbes, 2005). This is particularly critical in dynamic environments where transitory opportunities can disappear quickly after being exploited by competitors (Gumpert & Stevenson, 1985). Small entrepreneurial firms are in the best position to pivot in favor of prospective

respond to environmental pressures and reassign the optimal level of resources to determining future opportunities. In addition, evolutionary processes may be pushing businesses--especially young, high-growth firms--into shorter reaction times for their competitive moves. If that is true, the value of future knowledge, and hence the value of long-term investments, declines (Bettis & Hitt, 1995).

Fourth, some prior research questions whether long-termism is necessarily positive. Corporate governance researchers have suggested that using “poison pills” to protect managers from the threat of takeovers allows managers to focus on long-horizon strategies. However, researchers have found that managers with poison pill protection actually invest less and make investments of shorter duration than non-poison pill firms (Mahoney, Sundaramurthy, & Mahoney, 1997).

The Effect of Myopic Ownership

The effects of market-based ownership tend to lead to managerial short-termism. Even in the absence of pressure from owners, markets may cause managers to behave myopically. For example, Desjardins (2015) finds that when firms lose coverage from stock market analysts managers make longer-horizon investments and buy more durable assets. Thus, even in cases where stakeholders (analysts) are not in a direct position to punish managers, managers appear to respond by engaging in non-optimal long-term behaviors.

Sampson and Shi (Sampson & Shi, 2016) empirically tested it through a longitudinal study examining the interdependent effects. They used a "market discount factor" derived from CAPM discounted estimated future earnings to arrive at a common measure of short-termism. Their results confirm that markets respond to managerial behavior such as cutting R&D or CAPEX expenditures, but also that managers respond to changes in discount rates. These effects are moderated, as expected in BTOF, by slack resources. Firms with higher slack have lower sensitivity to ownership pressures. A related issue with stock market ownership is the frequency of turnover. The average equity holding period of owners declined from seven years in 1940 to less than a year in 2000 (Haldane, 2010). This leads to higher stock volatility and increased uncertainty for managers.

Owner Myopia: Institutions

Institutions, such as banks, pension funds, mutual funds, ETF's and hedge funds, own an ever-increasing percentage of public firms. In 1940, IOs held 8% of shares. By 2009, they held 73% of shares (Barton & Wiseman, 2014; Gilson & Gordon, 2013). This change in corporate governance power from diversified individual owners to more concentrated IOs has had a profound effect on the relationship between owners and managers, especially with respect to time horizon. Research has found mixed effects of IOs on firm time orientation. On the one hand, there is a perception of IOs as "barbarians at the gate" (Grundfest, 1993), where owners "sell first and ask questions later." Pound and Shiller report in the Wall Street Journal that 55% of IOs would sell their holdings based only on a negative report of short-term performance (Drucker, 1986a; Pound & Shiller, 1987). Traditionally, IOs perform the "Wall Street Walk" (Admati & Pfleiderer, 2009; Gillan & Starks, 2007) which means selling their shares instead of getting involved in costly monitoring. Thus, negative earnings surprise announcements

(Kothari, 2001). It is therefore not surprising that more aggressive ownership involvement in firms means that CEO tenure has fallen from ten years in 1995 to six years in 2009 (Favaro, Karlsson, & Neilson, 2011). This creates incentives for CEOs to engage in earnings manipulation or other short-termist behavior in order to limit employment risk.

Myopic ownership (also called “transient ownership”) helps explain the pejorative effects of institutional ownership on firm time orientation. By examining current market capitalizations relative to discounted expected future earnings Bushee (Bushee, 2001) found that transient owners exhibit a strong preference for short-term earnings, leading to market misvaluations. Based on these preferences, firms with more transient owners incentivize short-term behaviors that have negative long-term repercussions. For example, they grant more compensation in the form of stock options, and have higher pay-for-performance sensitivity (Shin, 2006). As noted in the section on option pay, this increases volatility and incentivizes managerial myopia. This has led to a fear of "quarterly capitalism" where investor attention has shifted from annual earnings reports to a more rapidly updated emphasis on unaudited quarterly earnings reports (Kim and Bettis, working).

Dedicated Owners

The effect of IOs is not homogenously negative, however. Indeed, institutions are often considered to be "sophisticated investors" that appropriately monitor management and reduce pressures on management to engage in myopic behavior (Bushee, 1998). Further, most research finds a positive association between institutional ownership and time horizon. These are puzzling findings in light of the common view that IOs increase myopic behavior. For example, why did 60% of CEOs surveyed by Business Week consider IOs to be a top source of short-term

Dedicated owners own large blocks of shares for time periods greater than one year. The large relative position and long-time horizon give these IOs incentives to monitor and engage in effective corporate governance. Transient owners, on the other hand, have small stakes which limit incentives to either monitor or gather private information (Bushee, 2001). Hence, they can only make short-horizon price predictions from public information. When these predictions fail, transient owners sell rapidly (Kim and Bettis, working; Porter, 1992).

The positive effects of dedicated owners can more than offset the negative effects of transient owners (Bushee, 1998). While not completely synonymous, dedicated owners and blockholders are often discussed together. Blockholders, by definition, own 5% or more of a company, and they often wield a high degree of power. Since blockholders are limited by market liquidity, they cannot easily sell their shares. Given the relatively high ownership concentration within the blockholder's portfolio, they have incentives to bear costs such as monitoring and participating in corporation governance that diversified transients do not share. Seen in a broader light, large blockholders becomes partners with management, and the coordination of effort and shared goals between the two lead to a number of positive long-term firm-level outcomes. Blockholders have a number of way in which they can interact with management to push a long-term agenda. The most common method is proxy voting (Connelly et al., 2010), but they also employ board representation, setting executive compensation, directly negotiating with

management, or even using the media to "jawbone" against executive actions (Kang & Sorensen, 1999).

On the positive side, blockholders and dedicated owners can help owners re-orient to long-term horizons. Chen, Harford, and Li have found that the presence of blockholders results in corporate governance improvements and positive cultural changes in the company (X. Chen, Harford, & Li, 2007). These changes subsequently lead to superior performance. Connelly et al. used dyadic firm rivalries (Coke vs. Pepsi, e.g.) to examine the influence of heterogeneous ownership on firm actions (Connelly et al., 2010). They found that firms with more blockholders engaged in more strategic competitive actions, such as R&D expenditures, CAPEX investments and strategic alliance formation. Since these investments can lower short-term profits (Laverty, 1996), managers benefit from the support of long-term shareholders until the share price recovers.

On the other hand, firms with more transient owners engage in tactical behaviors that emphasize short-term execution periods and short-term results. These include pricing and

Chapter Three: Literature Review Part II - Venture Capital Horizon and IPOs Venture Capital Introduction

At first glance, venture capital (VC) appears to be at odds with public-market based investing. Michael Porter (1992) asked how, in a system dominated by stock market short-termism, an alternative investment system can thrive in which VCs invest in illiquid private companies for periods exceeding ten years. As an asset class, venture capital is inherently time-oriented because VCs negotiate with investors and portfolio companies to manage time horizons for initial investments, follow-on investments, and exit. VC funds raise money from limited partners for pre-set durations, which are almost always ten years (Sahlman, 1990). VC firms earn fees for both money management and capital appreciation. Depending on fund size, firms may optimize their investment goals based on either maximizing fee collection or maximizing capital appreciation. Some evidence suggests smaller funds seek to maximize capital appreciation while larger funds seek to maximize fee income (Mulcahy, 2016).

This duality can result in strong conflicts of interest between their role as fee collecting agents and their governance participation as principals (Arthurs, Hoskisson, Busenitz, & Johnson, 2008).

At the same time, VCs incur costs to source deals, perform due diligence, monitor managers, assist with strategy development and provide other value-added services to the portfolio companies. Since VCs have finite resources to monitor, they manage agency problems and information asymmetry issues (Jensen & Meckling, 1976) with three key tools: board

membership, coaching, and staged investments. First, staged investments allow VCs to distribute limited quantities of cash in order to limit agency issues between rounds (Paul A. Gompers, 1995). Second, VCs limit their risk on any one portfolio firm by syndicating their investment with other VCs (Paul A. Gompers, 1995). Third, VCs aggregate their investments across many portfolio firms, which increases their risk tolerance for any one investment (Loewenstein & Thaler, 1989).

VC Contributions to Portfolio Firms

As providers of private equity to speculative and highly risky young companies, VCs serve a number of strategic roles for their portfolio firms. As a whole, VCs serve as

intermediaries between an organization and its external environment. They provide critical resources such as legitimacy through association with high-status VCs (Pfeffer & Salancik, 1978). Like blockholders in public firms, VCs are rarely passive investors. They not only invest, but they also "build winners" (Croce, Martí, & Murtinu, 2013) through a range of strategic value-add capabilities. VC firms contribute by helping to develop strategy, leading follow-on

investment rounds, making valuable stakeholder introductions, engaging in active monitoring, participating on boards, and providing informal on-site visits (Croce et al., 2013; Lerner, 1995). The vast majority of past empirical work has subsequently found a positive effect of VC

contributions to firm growth (e.g., Lungeanu and Zajac 2015).

VCs add value by monitoring the actions of senior management including strategic decisions and financial health. IOs, including VCs, are "sophisticated investors" with the experience and expertise to add value through monitoring (Morsfield & Tan, 2006). Since owners incur costs to monitor, they only engage in monitoring if they have a long-term

orientation to their portfolio firm (Arthurs et al., 2008). Monitoring improves long-term post-IPO profitability and it is also correlated with pre-IPO firms receiving more fundraising rounds and hence a higher likelihood of an IPO (Paul A. Gompers, 1995).

(Edwards, 1996) explains how the fit between employee skills and firm needs enhances productivity--or vice versa--VCs may fail to contribute to portfolio firms if there is a misfit between expertise and need. Further, VC expertise is not prima facie valuable. It only serves as a productive asset if it meets the needs of focal firms in "normatively appropriate" conditions (Lungeanu & Zajac, 2015). Thus, VCs may try to force a square peg into a round hole by using their specific set of skills and experiences to (mis)apply expertise in the wrong context,

potentially damaging a portfolio firm's performance.

This is especially evident when the investment time horizons of owners and managers diverge (Stein, 1989) which can result in damaging performance consequences (Arthurs et al., 2008). In these cases, VCs more often provide managerial compensation incentives that correspond with their own time orientations and exit preferences (Cadman & Sunder, 2014). These contracts include a higher proportion of pay in stock options, and stock option expiration dates oriented to potential exit periods. Confirming much prior corporate governance research, Cadman and Sunder find that these short-term incentives do speed up the time to IPO and reduce long-run performance (Cadman & Sunder, 2014). The opposite is true as well. Long-horizon incentives enhance long-run abnormal returns. As in other research, the mechanism is theorized to be poor managerial project selection that emphasizes selecting short payback projects over long-run, capital-intensive projects (Stein, 1989).

Long-term owners see strategic potential in their portfolio firms and invest and monitor accordingly. These VCs accept short-term losses and potential long-term negative cash flows in addition to providing strategic consulting services for their entrepreneurs (Bygrave & Timmons, 1992). On the other hand, short-term oriented VCs will free-ride off of long-term VCs,

exit early (Admati & Pfleiderer, 2009). Bygrave and Timmons suggest that short-term VCs emphasize more liquid investments with a payoff horizon of 2-4 years and that long-term VCs focus on projects with 5-10 year payouts (Bygrave & Timmons, 1992). And while myopic VCs may have strong incentives to "grandstand" (Paul A. Gompers, 1995) and push their portfolio firms into early IPOs, these motives are attenuated by pressures to maintain their reputation through engaging in optimal rather than myopic exits (Arthurs et al., 2008).

In an interview with an angel investor in San Francisco (Kazanjy, 2016), he used language remarkably consistent with Levinthal and March's "myopic learning" principals to discuss how VCs push their firms toward either a local or global maximum (Levinthal & March, 1993). He thought that myopic--and possibly unskilled--VCs push firms toward a local

maximum and then invest too quickly in those firms. On the other hand, long-term oriented--or more highly skilled--VCs patiently wait and guide entrepreneurs to a global maximum by investing heavily in product growth. This does not mean that long-term oriented VCs put time-pressure on their portfolio firms. Rather, they exert time-time-pressures on entrepreneurs but only after seeing product-market fit and appropriate entrepreneurial strategic capabilities. At this point, even the most long-term VC will attempt to "foreshorten the exit horizon to generate liquidity in order to return cash to investors" (Kazanjy, 2016).

VC Myopia & Long-Termism

owners appropriately match the time orientation of their investment with the strategic orientation of the portfolio firm. Since myopia reduces optimal investment outcomes, VCs will make longer term investments, especially considering their capital is fully committed for periods of ten years or more. However, VCs have a number of incentives to take portfolio firms public before it is optimal. Angel investor Pete Kazanjy called these "mal-incentives" (Kazanjy, 2016). VCs must weigh the economic cost of "defecting" from an optimal investment time horizon against the gains they could make by forcing an early IPO and using the resulting publicity to raise future fund rounds. Since 75% of VC firms never raise a second fund, the time pressures on VCs to show successful exits are quite strong (Mulcahy, 2016). This may allow VCs to exit profitably from a firm, but, if that exit is premature because the VCs seek to exploit an IPO for reputation gain, firms lose access to necessary resources due to the loss of potential IPO proceeds and will hence be less viable in subsequent periods (Nam et al., 2014).

to go public prematurely (Arikan & Capron, 2010). VC Long-Termism

Despite the extensive research that has been done on VC myopia, VCs are generally not myopic investors (X. Chen et al., 2007). The strategic rationale for long-termism among VC investors is strong. Only dedicated investors can gain the inside knowledge needed to monitor effectively. Further, based on the VC "nurturing" arguments discussed in previous chapters, principals need time to share expertise and help build appropriate strategic plans (X. Chen et al., 2007).

VC investment horizon is dependent on entrepreneur network, investment stage, and industry. Conceptually, it makes sense that high-tech and high IP industries require longer time horizons. R&D efforts require large upfront costs, and have uncertain and varying times to product development and subsequent monetization. For example, biotechnology requires large upfront development costs and a continuing stream of costs as the drug reaches a marketable stage. For a software company with a high intangible resource base, the product must be

developed and proven before the entrepreneur can IPO (Arikan & Capron, 2010). Further, these types of firms need more prestigious VCs and underwriters in order to signal product quality at the time of IPO. This limits uncertainty and increases the likelihood of IPO success, particularly in reducing underpricing (Sanders & Boivie, 2004).

Likewise, market conditions play an important role in VC time horizon.

funds, time horizons correspondingly increase. Further work needs to be done to determine the effects of these exogenous influences on owner time horizon and subsequent firm performance. Time Orientation and Firm IPOs

While an IPO may appear to be primarily a firm financing and liquidity event, management scholars view it more holistically as a "social process" where IPO firms form relationships with prestigious partners and culturally evolve to adapt to the demands of being a public firm (Arikan & Capron, 2010). And yet the pressure on firms to IPO arises from

contractual and liquidity processes during the VC cycle, which creates pressure on firms to exit (Paul Alan Gompers & Lerner, 2004). One key cultural change is that, at the IPO, firms receive an infusion of cash and managers lose the option of choosing their owners (Nelson, 2003).

In addition, firms go public to raise cash. This is used to pay off pre-existing debts, invest in projects, engage in M&A transitions, or retain for its strategic value (Kim and Bettis,

Chapter Four: Theory and Hypothesis Development Time Orientation Construct

Researchers have long assumed that firms that did “a better job of managing for the future” (Hill, Hitt, & Hoskisson, 1992) could gain a competitive advantage over their rivals since business strategy decisions are inherently time-oriented (T. K. Das, 1987). Conceptual

frameworks such as exploration and exploitation (Schumpeter, 1934; March, 1991) demonstrate how firms incur upfront costs for projects that have heterogeneous lifetimes and payout

schedules (Souder & Bromiley, 2012). Understanding the processes that drive firm time horizons is crucial to the field of strategy since superior performance results from executives choosing projects that optimize the size and timing of profits.

When managers act on or set short-term aspiration levels, they may ignore long-horizon projects. Cyert and March observed that managers routinely emphasize “short-run reactions to short-run feedback rather than anticipation of long-run uncertain events. [Managers] solve pressing problems rather than develop long-run strategies” (Cyert & March, 1963, p. 167).

Project Selection

One of the theorized causal mechanisms for why managerial short-termism negatively impacts performance is that myopic managers tend to choose projects with more favorable short-term payouts in order to avoid uncertainty and meet short-short-term goals (e.g., Souder and Bromiley, 2012). Compared to long-term projects, these short-term projects may result in higher

management and financing costs, resulting in lower long-term profitability.

There are a number of related decision-making heuristics and biases that could impact project selection, time horizon, and profitability. For example, managers may set IRR hurdles well above their cost of capital. Survey evidence shows that IRRs are, on average, set at roughly double a firm’s marginal cost of capital {Jagannathan et al., 2016}. When firms use these IRRs as an input to net present value (NPV) calculations, high hurdles reduce the apparent value of a long-horizon project. Further, high IRR hurdles will result in a firm investing in fewer profitable projects than a competitor with a lower hurdle rate, resulting in lower long-term total

profitability. Likewise, firms may obtain similarly biased results when using other project

valuation techniques. Using payback period—which over 50% of firms use according to Graham and Harvey’s (2001) survey—as a selection mechanism ignores the long-run cash flows after the payback period is met, which likely biases project selection to projects that result in the shortest-term cash flows.

selection, return expectations, and time orientation interact. Zynga is a well-known social e-gaming company that had a peak market value of over $10B in February of 2012. Founder and CEO, Mark Pincus has been admittedly short-termist in his approach to the company (Farivar, 2013). He routinely turned down long-horizon projects to focus on short-term incremental changes to product development3 and monetization. He said that he “did every horrible thing in the book” to increase revenues. These “things” were typically short-term projects that

emphasized nearly instantaneous payoffs such as adding additional in-game monetization elements such as requiring customers to pay for more lives, coins, etc. These strategic moves increase revenues, but typically at the expense of losing customers. A game developer suggested that future game engagement was related to how much fun it was to play, but he “had a [project manager] tell me—many times—that they 'couldn't get data on fun” and consequently were not interested in longer time projects (Farivar, 2013). During one of Zynga’s secondary offerings, they claimed that their existing products and their future product pipeline were all long-term oriented. Specifically, they claimed that their game pipeline was “strong… robust… [and] very healthy.” However, in a later4 shareholder lawsuit, the judge called these claims “mere business puffery.”

Facebook makes a relatively strong counterpoint to Zynga as a company that emphasizes long-term projects. Even though both Zynga and Facebook raised similarly large amounts of venture capital (approximately $865M and $1.2B, respectively), the two firms employed different approaches to their decisions about time-to-revenue generation. Illustrative of

Facebook’s longer-term approach, Mark Zuckerberg bought Instagram in 2012. At the time of

purchase, Instagram had zero revenues and any future revenues were likely to be realized in a matter of years, not months. According to the Wall Street Journal, Instagram had yet “to develop a model for generating revenue, and substantial obstacles remain,” such as whether smartphone screens were even a feasible medium for advertising {Raice and Ante, 2012-04-10}. Instagram was a purely mobile app and Facebook itself lacked the ability to sell advertising on mobile devices. Turning Instagram into a viable business had a multi-year path to revenues and profitability. This was a long-term decision, at least within the context of the social media

industry in 2012. Zuckerberg even said “I’m here to build something for the long-term. Anything else is a distraction.”

Owner and Manager Interactions

periods lead to long-horizon decisions.

In much the same way, Connelly et al. (2010) tested strategic and tactical actions in a hand-coded sample of articles on major US firms and found that large, dedicated owners led to an increase in strategic actions. Since large owners (>5%) have illiquid positions, they have strong incentives to monitor executives and set appropriate long-term incentives that emphasize quality project selection and long-horizons. Large owners also provide voting blocks that offer executives implicit (or even explicit) assurance that they will vote in management’s favor, supporting strategic actions and agreeing to not discipline managers or sell their shares because of those decisions (Connelly et al., 2010). Thus, owners influence managerial time orientations, even in the absence of direct firm control.

Venture Capitalists

legitimacy. Since VCs, especially lead VCs, tend to have large ownership stakes and the potential to invest in future rounds, VCs have the incentives to cooperate with management in developing and executing long-term firm strategies.

However, there is another perspective to the ten-year investment cycle of VC funds. As VCs reach the end of their fund cycle, funding concerns can severely limit the portfolio firm’s strategic flexibility. This can lead to short-termism on the part of the portfolio firm executives. In other words, the cyclical form of VC financing could lead to entrepreneurs being forced to forego high quality projects or even go public before it is optimal in order to meet their financing needs (Arikan & Capron, 2010). Further, prior research on VC motives indicates that some VCs are naturally short-term oriented. Gompers created his “grandstanding” hypothesis based on evidence that both younger VCs and those with lower legitimacy take firms public early,

resulting in higher underpricing, worse performance, and a higher chance of firm failure (Paul A. Gompers, 1995). IPOs are the “ultimate signal” of VC success, and grandstanding firms exploit this trading off the potential gains of holding winners in exchange for the prestige that comes with taking a portfolio firm public. This allows them to raise follow-on funds which generate both fee and equity income.

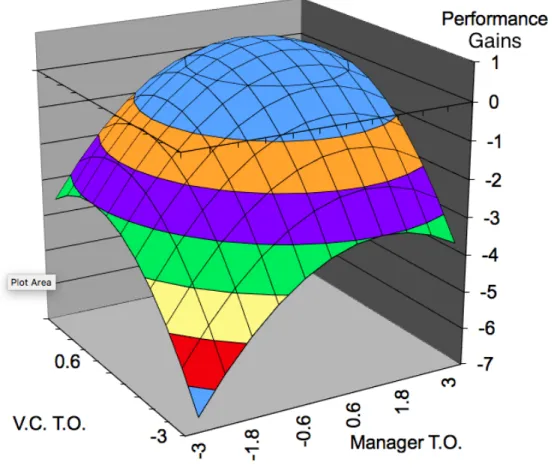

Hypotheses

shape of the three-dimensional surface with respect to improvements in firm performance. H1 Development: Manager Time Orientation

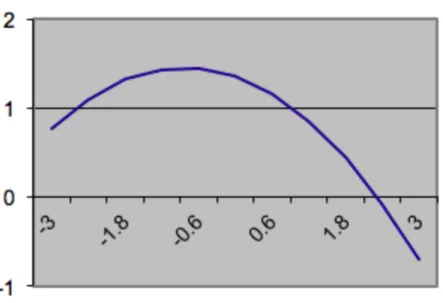

As noted in the previously-cited literature on manager myopia and based on the previous theory developed in chapter five, three key elements suggest that short managerial horizons lead to reductions in future firm performance. First, entrepreneurs need sufficient time for both the exploration and exploitation phases of building their company. In particular, overly short exploration horizons are linked to poor product development choices because managers are pushed to accept products developed on local maxima instead of continuing optimal search for a global maximum (Levinthal and March, 1993). The longer exploration time due to longer time horizons can lead to a match between a product and its potential market, leading to

improvements in firm performance. Second, short-termism leads to leads to poor project selection and a reduction in future performance levels. Jaganathan et al. (2016) use survey evidence to show how high IRR thresh holds—due to the desire for short-term profits—come at the cost of ignoring profitable long horizon projects. In aggregate this leads firms to pass up positive NPV projects reducing profitability and competitive position (Souder and Bromiley, 2012). Third, short-term managers solve “pressing problems” instead of planning for the future (Cyert and March, 1963). This leads to a preference for projects that have immediate payouts instead of more-profitable projects that take time to develop. Taken together, these three key pieces of theoretical support suggest that short time horizons will lead to reductions in future performance.

product development, leading to wasted capital and other exploration related resources (Souder et al., 2016). This could cause the firm to expend too much capital on exploration leaving fewer resources with which to scale their project. Additionally, these managers may miss other

opportunities that appear as market conditions change. Second, the fact that overly long

managerial time horizons might also lead to lower long-run changes in firm performance is also due in part to a set of psychological biases related to managerial cognition of risk and

uncertainty. March and Shapira (1987) found that managers do not perceive risk as a range of probable outcomes but instead as only two outcomes which include the most likely outcome and the “worst case scenario.” Further, managers believe that over time they can “change the odds” of the risks that they bear (March & Shapira, 1987). For example, managers may mistakenly believe that, given a long enough horizon, they can change sunk cost investments, such as a manufacturing plant, more than they actually can. Thus, overly long-horizon managers may be more willing to back questionable long-term projects under the mistaken belief that all risks can be controlled as the project reaches its payback period. Since long-term projects rarely show short-term results, overconfident managers may mistakenly believe that unobserved results are better than they actually are (March and Shapira, 1987).

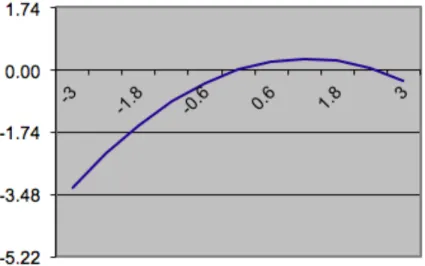

Taken together, the claims that short-horizon managers lead to reductions in future firm performance and that overly long horizon managers lead to lower firm performance suggests the following relationship between time horizon and performance growth. The hypothesized shape is illustrated in figure 1:

H2 Development: VC Time Orientation

Next, I argue for a similar relationship between VC time horizon and firm performance gains and losses over time. VCs and entrepreneurs work together closely throughout the development stage of the firm. VCs provide critical advice and capital which affects the development of firm capabilities over time. Much research supports the general relationship between longer venture capital time horizons and the development of superior portfolio firm capabilities and hence better long run performance. VCs with a long-term orientation benefit because a long horizon allows them to invest both tangible resources (capital) with valuable intangible resources, such as experience, contacts and prestige, in order to “build winners” in their portfolio (Croce et al., 2013). VCs invest time and resources in their partnership with young companies in order to help them acquire the necessary resources to succeed (Pfeffer and

Salancik, 1979). Generally, a longer time horizon helps VCs match these investments with the appropriate firm strategy.

There is also support for the claim that short VC time horizons harm the future

1995). Taken together, the two arguments that short VC horizons lead to lower changes in performance and moderate to longer than average time horizons lead to stronger changes in performance. This suggests that firm performance improves as time horizon improves, at least until well above average horizons.

On the other hand, VCs with overly long-term orientations may encourage firms to make long-horizon, and often illiquid, investments where shorter-term, more flexible strategies are more appropriate. Firms in dynamic environments that make faster strategic decisions improve their ability to exploit opportunities before they disappear or are taken by competitors (Gumpert & Stevenson, 1985). This could lead to first-move advantages (Makadok, 1998) or a series of transient advantages (Bettis & Hitt, 1995; Forbes, 2005). This applies especially to

entrepreneurial and IPO firms because their small size leads to flexibility and speed in exploiting dynamic opportunities (Chen & Hambrick, 1995). These points indicate that overly long time horizons could lead to strategic mismatches between portfolio firm and dynamic environments, resulting in lower performance.

Taken together, the claims that short horizon VCs lead to lower future performance, that longer horizon VCs generally lead to improved changes in performance, and that extremely long horizon VCs lead to a slow reduction in suggests the following relationship time horizon and performance improvements, as illustrated in figure 2:

H2: Performance growth improves as VC time horizon increases toward its mean and continues to improve as VC time horizon exceeds its mean, ultimately

decreasing when VC time horizon is high relative to its mean.

Chapter Five: Data, Methods, and Results

To test the above hypotheses, I searched for a range of data sources with high reliability, accuracy, and consistency of information for recent IPO firms. This search led me primarily to publicly available data sources monitored by the SEC. This guaranteed access to the rich data sets available for public companies while still ensuring that I could analyze young,

entrepreneurial firms. I use four primary sources: SEC S-1 filing documents, Compustat, VentureXpert, and Bloomberg. IPO firms are of particular interest because they represent a critical transition period where small entrepreneurial firms access public capital markets. In the process, they access to resources for growth as well as transition from opaque, private firms to more transparent public firms. Further, studying IPO firms offer a discrete event that offers a unique window into an entrepreneurial firm’s strategy as well as invaluable insight on the effect of ownership on future performance. IPO firms tend to have a (relatively) small number of owners and fewer business units.

To define my sample of IPO firms, I first find all de novo5 IPO firms from 2004 to 2012. This represents a robust time-period used by recent scholarship (e.g. Brau et al., 2016) that includes at least one full business cycle. This time period also avoids the extreme IPO outliers from the 1999-2000 internet bubble. The results from these two years have been shown to dramatically bias regression results due to high-sigma data, even when included in large samples spanning many decades. For example, Ritter and Welch (2002) found that their findings on over

5 “From the beginning.” These are firms that were founded independently as opposed to being spun-off from a

40 years of IPO data were reversed after excluding those two years. Similar findings have been echoed in the management literature by Arthurs et al. (2008) and Nam et al. (2014) who chose similar sample periods (i.e. 2004-2012) for their IPO studies. To exclusively study

entrepreneurial firms, I followed the definition of de novo firms in Gao and Jain (2012) and Brau, Cicon and McQueen (2016). I excluded equity carve-outs and spinoffs, private equity reverse IPOs, foreign issuers, real estate investment trusts, financial firms, and firms older than 25 years. This allows for the study of relatively young, entrepreneurial firms. Consistent with nearly all IPO studies, I also excluding firms raising less than $5 million and those with share prices under $5. This process leaves 419 IPO firms in the sample. Since I seek to examine the effect of VC horizon on changes in firm performance, I exclude 85 firms that do not have venture capital backing, and 13 additional firms that were missing critical time-horizon related data.

Variable Constructions

DV1: Change in Firm Performance

To construct my dependent variable, I obtain revenue data from Compustat. To measure changes in firm performance over time, I use revenues at three years after the IPO (t+3)

returns (CAR or cumulative abnormal returns), is another potential measure for performance (Lungeanu and Zajac, 2015). However, firms can only generate positive CARs when the stock market has not fully imputed firm potential into the current price. In this case, there is no reason to believe that time-orientation is not imputed or considered by analysts or investors as all measures are available in public documents at the time of IPO. To best measure revenues, and in line with recent research on time horizon (e.g. Souder and Bromiley, 2012; Flammer and

Kacperczyk, 2016; Nadkarni and Chen, 2017; Lungeanu and Zajac, 2015), I use the natural logarithm of firm revenues to keep the effect of a change in revenue, rather than a dollar change in revenue, constant (Wooldridge, 2015).

IV1: Manager Time Orientation

Since it is difficult to directly measure a manager’s time-horizon preference with respect to their firm, I seek to isolate, as far as possible, a measure of time-horizon that is unbiased by related concepts such as risk or uncertainty. Prior literature offers little help in finding a viable measure for private pre-IPO firms.6 Therefore, I focus on a measure that is quite specific to time-horizon: the use of “forward-looking” words (described further below) that an IPO firm uses to describe its business strategy. Specifically, I analyze the “futurity” of the language in the strategy section of a firm’s IPO filing-document, Securities and Exchange Commission (SEC) form S-1. To my knowledge, no study has used linguistic analysis specifically on the business strategy portion of a firm’s S-1.

Under the Securities Act of 1933, when firms decide to go public on a major stock exchange (NASDAQ or NYSE), they file a comprehensive document with the SEC called an

6 Lungeanu and Zajac’s (2015) measured counts of the word “money” in SEC filing documents to denote a

short-term orientation. Other research has used R&D spending as a proxy for long-short-termism (e.g. Bushee, 1998), even

though R&D has also been used as a proxy for a diverse set of constructs such risk-taking (e.g. Palmer and

1. This document, ranging from 100 to 300 pages, includes extensive firm information such as market risks, financial statements, a description of firm strategy, and comprehensive information about underwriters, share sales, share structure and pricing. S-1’s are transparent and reliable because they are scrutinized by a range of monitoring agents such as SEC officials, stock market analysts, potential institutional investors, lawyers, and underwriters, among others (Arthurs et al., 2008).

To calculate my focal independent variable, I use established linguistic analysis tools to examine a little noticed part of the S-1 document: The “Business Strategy” section. Each S-1 has a short, about 20 pages, section detailing the firm’s current products, relationships with

customers and suppliers, the nature of competition within the industry, as well as future firm strategy. To establish a time-orientation measure, I use the word list “Future Orientation” contained in the software package Linguistic Inquiry Word Count (LIWC). This list of words and phrases comes primarily from the Harvard IV psychology word index dictionary. The LIWC future orientation lists includes approximately 70 entries related to thinking about or planning for the future, such will, going, planning, and invest. Prior research (e.g. Nadkarni & Chen, 2014; Prabhu & Chandy, 2007) has used this dictionary for time-orientation research in the strategy field. Using just the business strategy section, instead of the entire S-1 document, helps isolate the time orientation of managers. Indeed, given the myriad inputs to an S-1 document, this strategy section is likely to have the most input from management, rather than from lawyers or accountants, for example, as one would find in the “legal risks” section. Thus, using the entire 300-page S-1 document would dilute the impact that management has. Instead, I isolate the one section which most likely reflects senior executive’s real attitudes toward time-horizon.

over total words in the strategy section of the S-1 and then multiply by 100:

Manager𝑻.𝑶. Score = 100 ∗𝐶𝑜𝑢𝑛𝑡(Future Words)

𝐶𝑜𝑢𝑛𝑡(Total Words)

IV2: VC Time Orientation

Measuring a venture capital firm’s time horizon is difficult because of the private nature of VC transactions. There are a number of self-reported databases, however this data has

potential biases because firms are likely to claim their successes and obfuscate or hide their failures. Another critical issue with studying VC time orientation is that there are few data points on which to base valid measurements. Potential measures like the overall average investment holding period may be biased because VCs either do not report failures or hold them on the books (Mulcahy, 2016) to collect management fees from limited partners.

Next, I compute an aggregate measure for the VC Time Orientation (VCT.O.) of each focal IPO firm. This is the dollar weighted average time-horizon of each of the IPO firm VCs. I calculate this by multiplying each VC investor i’s time by the dollar amount i invested in each VC firm. I then sum these and divide by the total investment level to realize the weighted average VC time horizon:

Through this process, I generate an aggregate VC time horizon score as it applies to each IPO firm. This score is measured in months. I use Thomson Reuter’s SDC VentureXpert

database. This database covers VC firm/portfolio company/investment stage deal pairings from a broad variety of venture capital deals in particular, and private equity deals more broadly.