Market Analysis and Statistics G00233424

Market Share Analysis: Enterprise Content

Management Software, Worldwide, 2011

Published: 19 June 2012Analyst(s): Tom Eid, Bianca Francesca Granetto

Gartner tracks more than 80 vendors in the enterprise content management

software market. Vendor performance results show growth in imaging/

document capture, records management and Web content management

technologies, as well as process-based and job-aligned offerings.

Key Findings

■ Enterprise content management (ECM) software vendor revenue has showed signs of overall

growth and recovery, with total software revenue increasing 11.1% annually to a worldwide market size of $4.3 billion in 2011, up from growth of 7.7% annually and a worldwide market size of $3.9 billion in 2010.

■ Aggregate vendor revenue growth in 2011 was again in the single digits in North America and

Western Europe (picking up positively from 2010). Double-digit growth has come from Asia/ Pacific, Eastern Europe, Eurasia, Greater China, Latin America, and the Middle East and Africa.

■ There has been a modest shift in overall total market share of the top three multinational

vendors. The combined market share of EMC, IBM and OpenText declined from approximately 50% in 2009 to approximately 46% in 2011. All three vendors lost relative market share during this period, with incremental share gains going predominantly to both large and small regionally focused vendors.

■ Gartner has tracked more than 70 acquisitions in the ECM market since 2004. The level of

merger and acquisition (M&A) activity picked up again in 2011 and is continuing in 2012, driven by global vendors wishing to enter markets or expand their share of this and adjacent markets and midsize vendors looking to consolidate their regional positions.

Table of Contents

Market Share Data...2 Analysis...5

Tier 1 — Worldwide ECM Vendors...5

Notable Multiregional Vendors...7

Tier 2 — North America-Based Vendors...7

Tier 3 — Europe-Based Vendors...10

Mergers and Acquisitions...11

Recommended Reading...14

List of Tables

Table 1. ECM Software, by Vendor, Total Software Revenue, Worldwide, 2009-2011 (Millions of Dollars) ...3Table 2. M&As in the ECM Market, 2009-2012...12

Table 3. ECM "Other Vendors" Category by Region...14

Market Share Data

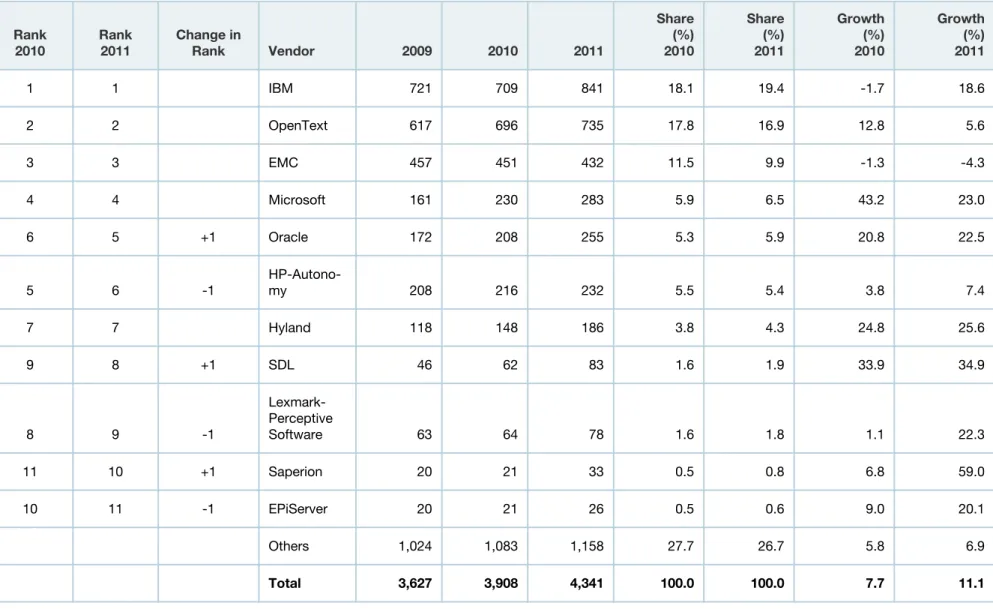

Table 1. ECM Software, by Vendor, Total Software Revenue, Worldwide, 2009-2011 (Millions of Dollars) Rank

2010 Rank2011 Change inRank Vendor 2009 2010 2011

Share (%) 2010 Share (%) 2011 Growth (%) 2010 Growth (%) 2011 1 1 IBM 721 709 841 18.1 19.4 -1.7 18.6 2 2 OpenText 617 696 735 17.8 16.9 12.8 5.6 3 3 EMC 457 451 432 11.5 9.9 -1.3 -4.3 4 4 Microsoft 161 230 283 5.9 6.5 43.2 23.0 6 5 +1 Oracle 172 208 255 5.3 5.9 20.8 22.5 5 6 -1 HP-Autono-my 208 216 232 5.5 5.4 3.8 7.4 7 7 Hyland 118 148 186 3.8 4.3 24.8 25.6 9 8 +1 SDL 46 62 83 1.6 1.9 33.9 34.9 8 9 -1 Lexmark-Perceptive Software 63 64 78 1.6 1.8 1.1 22.3 11 10 +1 Saperion 20 21 33 0.5 0.8 6.8 59.0 10 11 -1 EPiServer 20 21 26 0.5 0.6 9.0 20.1 Others 1,024 1,083 1,158 27.7 26.7 5.8 6.9 Total 3,627 3,908 4,341 100.0 100.0 7.7 11.1

Notes: Gartner defines total software revenue as revenue generated from new licenses, updates, upgrades, subscriptions and hosting, technical support, and maintenance. Professional services, training and certification, and hardware revenue are not included in total software revenue.

Autonomy was acquired by HP in October 2011. Perceptive was acquired by Lexmark in May 2010. Source: Gartner (June 2012)

Analysis

Overall ECM Market Segment Performance Analysis

In the ECM market, improvements in analytics, digital asset management and personalization features have enabled vendors to experience revenue growth for Web content management (WCM). Imaging and records management drove revenue growth as vendors improved their information management and e-discovery capabilities. Compliance-related and content-in-context requirements expanded opportunities for ECM technologies as vendors enhanced workflow, policy management and process automation offerings.

ECM suites consist of document management, imaging processing, records management and WCM applications that interoperate but can also be sold and used separately. Some vendors have added technology components such as digital asset management for handling rich media,

electronic forms and document composition for high-volume generation of customized documents. Vendor performance in the ECM market declined to single-digit growth in 2010 but returned to double-digit growth in 2011. A complement to "Market Share: All Software Markets, Worldwide, 2011," this report analyzes 2009 through 2011 vendor revenue growth rates as well as vendor market share in the worldwide ECM software market.

The ECM market has three distinct tiers of vendors as measured by total software revenue market share (see Table 1 for a summary of worldwide vendor market share):

■ Tier 1 — EMC, IBM and OpenText are worldwide vendors that accounted for 46.2% of market

share in 2011, down from 49.5% in 2009.

■ Tier 2 — HP-Autonomy, Hyland, Microsoft, Oracle and Lexmark-Perceptive Software are North

America-based vendors with a multiregional presence (primarily in North America and EMEA) that accounted for 23.9% of 2011 market share, up from 19.9% in 2009.

■ Tier 3 — These are EMEA-based regional and best-of-breed vendors that accounted for 29.9%

of 2011 market share, slightly down from 30.6% in 2009.

Results indicate that vendors that are more focused on select regions and countries are outperforming the worldwide vendors.

Tier 1 — Worldwide ECM Vendors

EMC

EMC's core content management strengths are focused on the infrastructure and transactional content management use cases of the ECM market. In addition, EMC is driving a major transition from on-premises-based products to ones that more fully leverage the evolving cloud-based opportunities. 2012 results could show both a positive revenue gain and growth in ECM share, as 2011 efforts to further penetrate the large accounts and emerging markets are reaping benefits. Revenue results have been supported by:

■ Large customer wins for EMC Documentum xCP and EMC Captiva in Greece, Israel and

Turkey, as well as large wins in key vertical markets, including banking, energy and national government.

■ A comprehensive set of products for enterprises that want to move from a traditional archiving

approach to a larger, comprehensive and more holistic information governance strategy, for both static and active content, addressing archive, compliance and e-discovery requirements.

■ EMC OnDemand announcements in 4Q11 position products for case management, content

management, customer communications management and document capture to be delivered through cloud-based management services.

EMC formed the Information Intelligence Group in 2011 to emphasize cloud content management and industry solutions, including solutions for financial services, government, healthcare, life

sciences and manufacturing. EMC has recently launched EMC Documentum D2 to improve the user experience and EMC Documentum Mobile to enhance user accessibility from smart devices.

IBM

IBM retained its leading share position in the 2011 ECM worldwide analysis. IBM's transition from a more technology-centric focus to one emphasizing line-of-business and industry solutions, such as case management, content analytics, imaging and capture, and information life cycle governance, is starting to pay off. Key branded products include Case Manager, Content Analytics, the Content Manager family, the FileNet family and Production Imaging. IBM has fared well during the recent downturn and period of regional economic uncertainty. It has protected its customer base,

enhanced its partner program and direct sales initiatives, and continued to add new customers for its ECM technologies. Significant investments continue to support expansion through partners in emerging markets and into the midmarket segments. Revenue success is driven by:

■ Presence in mature markets (Northern Europe, Germany, Benelux and Scandinavia, Eurasia,

and South Africa) and industries (banking, national government, healthcare providers, insurance and utilities).

■ Rationalization and simplification of its product offerings and a new "ECM" labeled organization,

drawing products from separate brands (IBM, FileNet, Lotus, Datacap) under one common strategy. This also includes a reorganization of its products into functional categories and business requirements, such as Compliance and Risk, Finance and Administration, and Human Resources and Operations.

■ Market messaging for content analytics and case management technologies — Case

management has been a target for multiple campaigns and events and the introduction of new solutions (for example, IBM Content and Predictive Analytics for Healthcare).

IBM is positioning into adjacent technology markets and cross-fertilizing through its events and campaigns for content and data: themes for big data, social, SmartCloud, content analytics and mobile. In 2012, IBM is expected to continue to deliver on this strategy, consolidating and improving its message and reach into both mature markets and the Middle East and Africa and Eurasia regions.

OpenText

OpenText has maintained its market share position during the past several years, growing primarily through acquisitions for ECM-focused technologies, as well as into adjacent and converging markets. For example, in 2011, OpenText acquired business process management (BPM) vendors Metastorm and Global 360. The recent acquisitions of Operitel and weComm provide enhanced e-learning and mobile application technologies. The latter is particularly strategic since it provides a concrete component to OpenText's mobility strategy launched in 2010 with OpenText Everywhere and other packaged applications for its ECM suite. OpenText's growth strategy has enabled entry into new and rapidly changing markets of the enterprise application landscape and has supported new trends such as mobility. Revenue growth has been a function of:

■ Mining the current customer base and that of the "acquiree" with new market segments to

target (first and foremost) the needs of marketing departments and chief marketing officers

■ Leveraging BPM and ECM technologies and acquisitions for both new products and new sales

channels, providing a positive impact on partner retention as well as new partner acquisition

■ Expanding partnerships with SAP, Microsoft and Oracle to drive deployments for transactional

content management, archiving and composite content applications (for example, accounts payable, employee file management and travel receipt management)

OpenText is expected to increasingly utilize the latest technology developments, such as cloud-based services, collaboration and social, mobility, and user security. With customer experience management solutions, OpenText is targeting the space of digital marketing and marketing content management to add to its WCM offerings.

Notable Multiregional Vendors

Tier 2 — North America-Based Vendors

HP-Autonomy

For many years, HP has had a small ECM market presence, with stand-alone imaging and records management offerings. However, with the acquisition of Autonomy in October 2011, this market position was changed dramatically. Since 2009, Autonomy has expanded its ECM market presence by acquisition and leveraging the Idol brand and technologies into a single platform. Core ECM technologies develop revenue streams for archiving, document management, e-discovery,

information access with search, records management and WCM offerings. Revenue growth is being driven by the following:

■ Expansion in Asia/Pacific and Western Europe

■ Implementation of solutions aligned to analytics and search, archiving and compliance, online

channels (e-commerce, personalization and segmentation) and social media management and collaboration

■ Emphasis on meaning-based computing as a broad technology enabler that leverages ECM

capabilities rather than focusing on specific content management products

Hyland Software

Hyland has focused its ECM platform, OnBase, for transactional content management capabilities to small and midsize businesses (up to 1,000 employees) and midtier enterprises (up to 2,500 employees) and increasingly to larger enterprises. Hyland primarily sells OnBase directly in select vertical markets, such as healthcare and higher education. The company leverages its broad channel of value-added resellers and OEM partners to extend OnBase for document management, imaging, records management and process management solutions into international markets and for industries such as commercial, community banking, government (local, state and national) and insurance. Market activities center on:

■ Strong growth in North America but limited market presence in regions other than Latin

America; investments have been made in EMEA and Asia/Pacific as well as for OnBase OnLine, a software as a service (SaaS)-based offering.

■ Frequent and focused M&A actions to obtain market-specific technologies, vertical market

presence and professional services expertise.

■ Emphasis on customer satisfaction, moderate deployment costs and integration with

vertical-market-specific vendors.

Microsoft

Since 2008, Microsoft has consistently registered the highest ECM market annual growth rates. It is positioned to challenge the three leading share vendors in the coming years, with the expanding market acceptance of SharePoint 2010. The large SharePoint installed base is expected to upgrade this new version, enabling Microsoft to reposition under the SharePoint brand newer and older products. Combined with Foundation 2010, Designer 2010, Forefront Protection 2010, Duet

Enterprise (a joint solution with SAP) and Windows Server 2008 R2 Hyper-V, SharePoint addresses both conceptually and productwise the requirements of a new generation of workers.

Gartner anticipates that SharePoint Online and Office 365 will continue to grow share faster for Microsoft with small and midsize businesses primarily in mature markets rather than in the emerging ones. Moving on-premises-based products to those delivered as an online service should continue to generate some conversion revenue for Microsoft, especially from illegal and pirated versions. The latter part of 2011 and into the first quarter of 2012 clearly shows Microsoft's determination to expand its functionality for SharePoint Online to capture the attention of more sizable subscription. Revenue results are a function of:

■ Increased emphasis on marketing and communications strategies for the ECM market and

extending SharePoint from its social and collaborative content management capabilities into a viable strategic platform offering.

■ Growing transactional content management demands from larger enterprises, as well as

addressing online channel optimization opportunities with its SharePoint Server for Internet Sites and FAST Search Server for Internet Sites.

■ Expanding the share of adoption by enterprises of the latest Windows Phone 7 and of the

Windows Embedded Handheld 6.5 platform. However, the focus will increasingly shift from hardware sales and management to application compatibility, access and consumption.

Oracle

Oracle has continued to expand its market presence by integrating its core infrastructure

technologies, such as the portal and business process management components, with its business applications and content management technologies. For the ECM market, the Oracle WebCenter strategy and platform includes Oracle WebCenter Content. Oracle made an important WCM

acquisition with FatWire (July 2011, with products now called Oracle WebCenter Sites), which could improve traction with line-of-business and marketing buyers. Oracle's ability to integrate acquired features and functionality provides a full ECM offering that is attractive to both business

professionals and IT managers. Oracle WebCenter enables customers to leverage the Oracle product stack, which can reduce the overall cost of deployment. Revenue is being enhanced by the following:

■ Alignment with WebCenter strategic initiatives to grow revenue in Asia/Pacific, Eastern Europe,

Latin America and EMEA.

■ Product extensions for archiving, imaging, packaged application integration, process

management, records management and rights management.

■ International reach based on the size and capabilities of Oracle's sales force and its broad

product development and support organizations.

Lexmark-Perceptive Software

Perceptive, acquired by Lexmark in June 2010, operates as a stand-alone business unit. Through organic growth and acquisitions, Perceptive provides a comprehensive ECM suite that includes archiving, customer communications management, document management, imaging and intelligent capture, process management, records management, search, and other features. Departmental solutions target ERP and business systems and focus on content in the context of work tasks such as accounts payable, claims processing, contract management, human resources and patient admissions. Performance results benefit from:

■ Emphasis shifting from almost exclusively North America to diversification into Asia/Pacific,

EMEA and Latin America

■ Integrated, transactional content management solutions driving adoption in the

communications, education, financial services, healthcare and government industries

Tier 3 — Europe-Based Vendors

EPiServer

In the 2011 market share analysis, EPiServer has moved down one position. After gains in previous years, EPiServer has shown an ability to steadily grow revenue, with a focus on WCM technologies and online channel optimization offerings. The go-to-market strategy for EPiServer is centered on continuous expansion through its indirect channel, with more than 550 partners and more than 4,000 customers. EPiServer has upheld a mature marketing, positioning and product strategy that anticipates market requirements moving beyond the core content management functionality. Positive financial performance is driven by:

■ Consistent delivery of its international strategy, working through its partners in 30 countries and

opening offices in 12 countries

■ Challenging midtier market leaders with a growth strategy that includes expansion of its product

portfolio through acquisition

SDL

2011 was a breakthrough year for SDL, which gained market position from its 2009 and 2010 ranking. This company steadily executes on its growth and product strategy based on its vision of "Global Information Management," with a deep focus on acquisitions. SDL in 2011 purchased video content management vendor Calamares, adding further product capabilities and customers to the 2010 acquisitions of Fredhopper, Language Weaver and Xopus. SDL revenue performance is a reflection of its focus on market growth, target market segmentation and acquisitions. Moreover, SDL recently announced the acquisition of WCM vendor Alterian. Revenue performance has been a function of:

■ Product differentiation and yet complementary synergies between its language technologies

and services and its content management offerings, which allowed cross-selling activities into a widely established customer base

■ Consolidation of its internationalization strategy and developing U.S. market penetration

becoming a more prominent component of total revenue

Saperion

Under the guidance of Saperion's new CEO, the company's 2011 reorganization as Saperion

Enterprise Systems is paying off, as it moved into 10th position in the ECM market share analysis. A primary focus was placed on targeting large-enterprise customers, and it proved successful by winning several new ones in 2011. However, Saperion also continues to target the midmarket sector, and particularly worth noticing is its strategic OEM agreement with Datev. Since 2009, Saperion has been evaluating SaaS offerings, and in 2011 this strategy became visible with Saperion ECM as a Service. Growth is being driven by:

■ Continued investment its cloud-based archiving solutions and process-based document

management ones, as well as diversifying these to target different market segments and needs and to offer applications to support mobility

■ Integration with popular enterprise applications, such as SAP and Microsoft SharePoint ■ International market expansion with solution partners in emerging markets, such as Gulfnet

Communications (Kuwait), Smartcap IT Solutions (China) and Atos, with new customer wins in both public and private sectors in Argentina, Kuwait, Lithuania, Russia and Turkey

Mergers and Acquisitions

The content management vendor landscape continues to change, with more than 70 M&As of vendors of ECM and related technologies having occurred since 2004. M&As are expected to continue aggressively throughout 2012 as vendors and service providers look to expand their customer bases, add adjacent and converging technology capabilities, and improve overall market presence. Table 2 identifies M&As that have occurred by the vendors identified in the Market Share reports in the ECM market since 2009.

Table 2. M&As in the ECM Market, 2009-2012

Buyer Acquiree Date of Acquisition

Autonomy Interwoven March 2009

Iron Mountain Digital (selected assets for digital data protection and recovery, archiving, and e-discovery)

May 2011

EPiServer Mediachase March 2012

Hyland Valco Data Systems July 2009

eWebHealth March 2010

Hershey Systems September 2010

CSC Group September 2010

HP Autonomy October 2011

IBM Datacap August 2010

PSS Systems October 2010

Vivisimo April 2012

Lexmark Perceptive Software June 2010

Pallas Athena October 2011

Isys March 2012

Nolij March 2012

Brainware March 2012

Limelight Networks Clickability May 2011

OpenText Vizible April 2009

Vignette July 2009

Nstein February 2010

StreamServe October 2010

Buyer Acquiree Date of Acquisition

Global 360 July 2011

Operitel September 2011

weComm March 2012

Oracle FatWire June 2011

SDL International XyEnterprise July 2009

Fredhopper January 2010

Xopus June 2010

Language Weaver July 2010

Calamares May 2011

Alterian February 2012

Source: Gartner (June 2012)

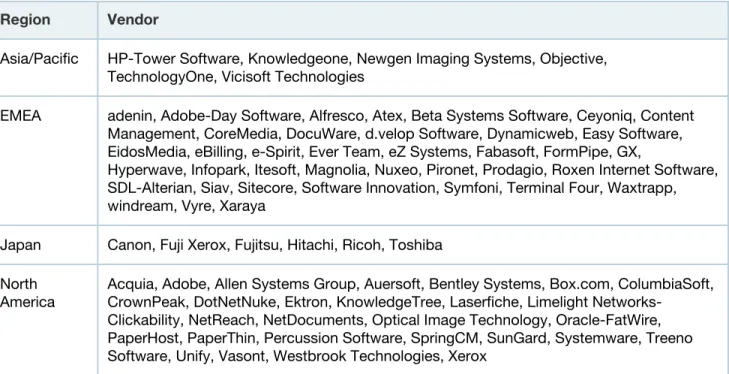

Gartner tracks more than 80 vendors in the content management market. The "other vendors" category includes the companies shown in Table 3, listed in alphabetical and geographic order (based on the regional location of their headquarters).

Table 3. ECM "Other Vendors" Category by Region

Region Vendor

Asia/Pacific HP-Tower Software, Knowledgeone, Newgen Imaging Systems, Objective, TechnologyOne, Vicisoft Technologies

EMEA adenin, Adobe-Day Software, Alfresco, Atex, Beta Systems Software, Ceyoniq, Content Management, CoreMedia, DocuWare, d.velop Software, Dynamicweb, Easy Software, EidosMedia, eBilling, e-Spirit, Ever Team, eZ Systems, Fabasoft, FormPipe, GX,

Hyperwave, Infopark, Itesoft, Magnolia, Nuxeo, Pironet, Prodagio, Roxen Internet Software, SDL-Alterian, Siav, Sitecore, Software Innovation, Symfoni, Terminal Four, Waxtrapp, windream, Vyre, Xaraya

Japan Canon, Fuji Xerox, Fujitsu, Hitachi, Ricoh, Toshiba

North America

Acquia, Adobe, Allen Systems Group, Auersoft, Bentley Systems, Box.com, ColumbiaSoft, CrownPeak, DotNetNuke, Ektron, KnowledgeTree, Laserfiche, Limelight

Networks-Clickability, NetReach, NetDocuments, Optical Image Technology, Oracle-FatWire, PaperHost, PaperThin, Percussion Software, SpringCM, SunGard, Systemware, Treeno Software, Unify, Vasont, Westbrook Technologies, Xerox

Source: Gartner (June 2012)

Recommended Reading

Some documents may not be available as part of your current Gartner subscription.

"Emerging Technology Analysis: ECM Technologies in a Cloud Services Maturity Framework" "Forecast: Enterprise Software Markets, Worldwide, 2009-2016, 1Q12 Update"

"Market Share: All Software Markets, Worldwide, 2011" "Market Methodology: Software"

"Market Trends: Online Channel Initiatives Drive Web Content Management Growth" Evidence

This report required data collection and preparation of market statistics information. Prevailing market conditions and political and economic events that affect vendor performance, such as regulations, M&As, a slowed worldwide economic recovery and new-version migration, have been taken into account.

Gartner uses public sources of information and works with software vendors to establish estimates for the market. Information from Gartner's secondary research and internal community meetings has also been used to arrive at certain conclusions. The data in this research report is published as Gartner estimates/opinion, not as facts that the vendor reported.

This document is published in the following Market Insights:

Regional Headquarters

Corporate Headquarters 56 Top Gallant Road Stamford, CT 06902-7700 USA

+1 203 964 0096

Japan Headquarters Gartner Japan Ltd.

Atago Green Hills MORI Tower 5F 2-5-1 Atago, Minato-ku Tokyo 105-6205 JAPAN + 81 3 6430 1800 European Headquarters Tamesis The Glanty Egham Surrey, TW20 9AW UNITED KINGDOM +44 1784 431611

Latin America Headquarters Gartner do Brazil

Av. das Nações Unidas, 12551 9° andar—World Trade Center 04578-903—São Paulo SP BRAZIL

+55 11 3443 1509 Asia/Pacific Headquarters

Gartner Australasia Pty. Ltd. Level 9, 141 Walker Street North Sydney

New South Wales 2060 AUSTRALIA

+61 2 9459 4600

© 2012 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. This publication may not be reproduced or distributed in any form without Gartner’s prior written permission. The information contained in this publication has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or adequacy of such information and shall have no liability for errors, omissions or inadequacies in such information. This publication consists of the opinions of Gartner’s research organization and should not be construed as statements of fact. The opinions expressed herein are subject to change without notice. Although Gartner research may include a discussion of related legal issues, Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner is a public company, and its

shareholders may include firms and funds that have financial interests in entities covered in Gartner research. Gartner’s Board of Directors may include senior managers of these firms or funds. Gartner research is produced independently by its research organization without input or influence from these firms, funds or their managers. For further information on the independence and integrity of Gartner research, see “Guiding Principles on Independence and Objectivity” on its website, http://www.gartner.com/technology/about/