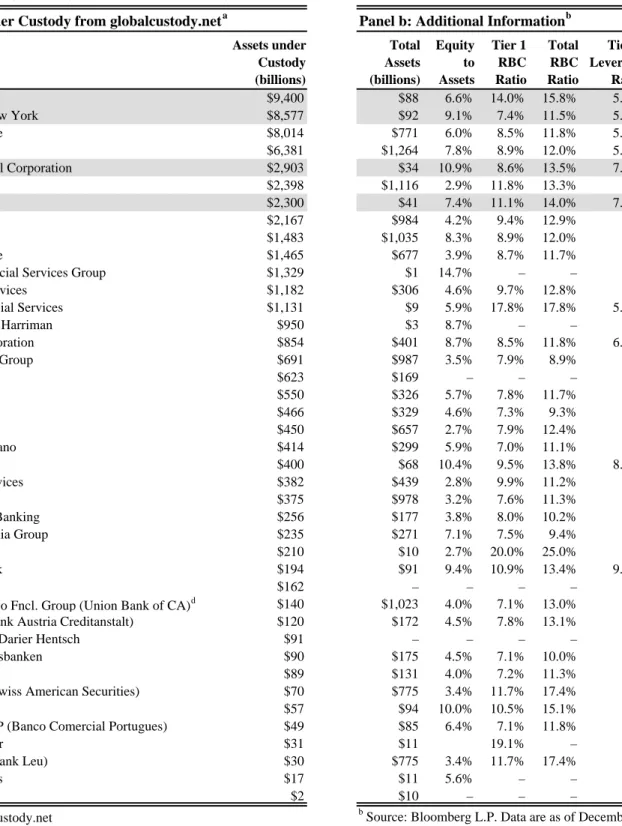

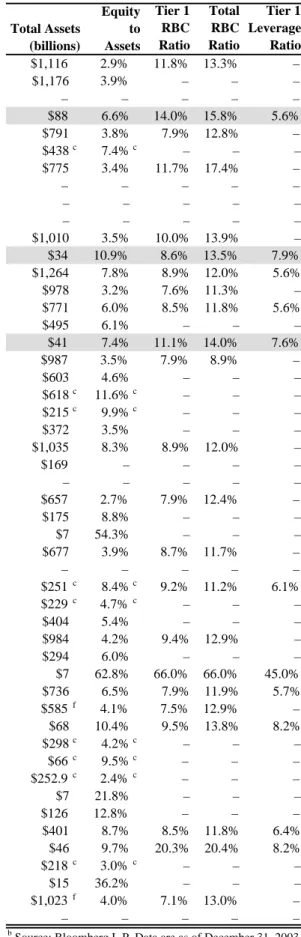

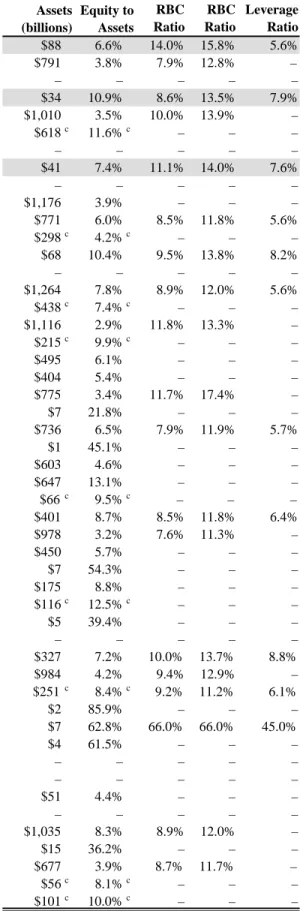

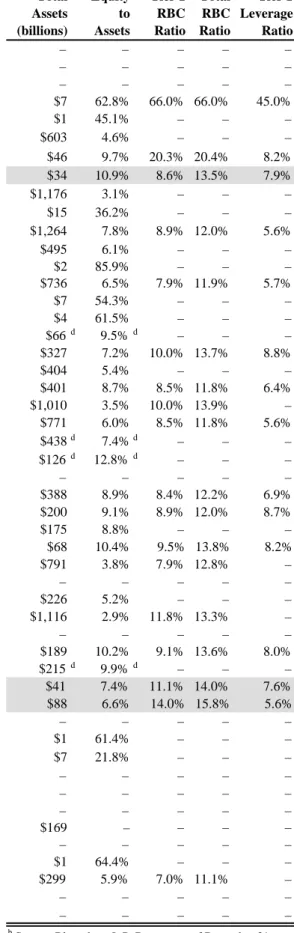

The potential impact of explicit Basel II operational risk capital charges on the competitive environment of processing banks in the United States

Full text

Figure

Related documents

According to the Law on the Central Bank of Russia, the bank’s monetary-policy objective is to maintain the stability of the ruble. In practice, the CBR has since 2009 been

The specific object of this book is to provide electric power engineers with information on the state of development of the renewable energy sources, as well as their.

Although cervical RF neurotomy is not univer- sally successful, it is the only intervention for neck pain that has been shown to be capable of provid- ing patients with complete

Note that we have also conducted tests for the implicit speech acts influence on sales (i.e., assertives, commissives, directives, positive and negative trends, and incoherence) yet

Solvency II will require the insurers to hold capital against market risk, credit risk and operational risk and will play a role similar to the one Basel III has in the banking

There is also a strong consensus that financial condition is causally related to lack of auto insurance – the lower a household’s income, the more likely the household will not

and proceed with post office motorboat, or leave Ivalo Mondays, Wednesdays and Fridays 8.00 a.

Instead of purchasing an entire new set of dishes, you may wish to simply update your present dishes by purchasing a few pieces of a different pattern in popular new