A bank covenants pricing model

Flavio BazzanaDepartment of Computer and Management Sciences University of Trento - Italy

Trento, January 2008

Abstract

Covenants are particular clauses in firms’ debt contracts that restrict business policy, giving creditors the possibility to put specific action into force when the covenants are violated. Three main reasons are accounted for in the litera-ture: (1) covenants resolve the conflicts of interest between shareholders and bondholders, (2) they are used as instruments of business policy and (3) they are used as credit monitoring by the banks. Using this instrument the banks can also reduce the expected loss rate of the loan, offering a lower rate to the firm. In order to calculate the spread the bank must estimate the probability of covenant violation and the contribution of the covenant to the LGD when the firm respects this constraint. As a consequence, the bank can modify the

elr of the loan without asking the firm for more collateral, and by choosing a combination of the financed part and of the limit of the financial ratio.

1. Introduction

Covenants are particular clauses in debt contracts of firms – bank loans and bonds in particular – that restrict business policy, giving creditors the possibility to put into force precise action when the covenants are violated. There are three main reasons for the existence of covenants: (1) covenants resolve the conflicts of interest between shareholders and bondholders, (2) they are used as instruments of business policy and (3) they are used for credit monitoring by the banks1. Shareholders and bondholders, having different rights on the cash flows generated by the firm, can 1 Citron, Robbie and Wright (1997), Berlin and Loeys (1988), Park (2000), Black et al.

often find themselves in conflict of interests situations. The shareholders can make business policies that reduce the market value of debt, determining a transfer of wealth from the bondholders. We can think, as an example, of an extraordinary distribution of dividends, to increase financial leverage, or to buy back capital fi-nanced with the issue of new debt or with the sale of the firm’s real assets . In ad-dition, the choice of risky investments gives rise to conflict between the two sub-jects, because the additional risk will be distributed in an asymmetric way, not fa-vouring bondholders. Covenants, therefore, limiting such behaviour, can reduce the conflict of interests between shareholders and bondholders. The empirical evidence2 of a positive difference between the spread of standard bonds and bonds with cove-nants, can also be used by a firm to reduce the average cost of debt, following an optimal composition of financing instruments3. Unfortunately, covenants also pro-duce undesirable effects, reducing flexibility in business policy. The type of cove-nant and its limits, must be chosen, therefore, in order not to compromise business policy, and to be credible for bondholders and banks. Covenants can be also be used as a protection of hostile acquisitions4. As an example, the issue of a bond with a covenant that limits the firm’s increase in financial leverage can be used to protect from leveraged buy-out (LBO), or from acquisitions with debt increase.

The first classification of bank covenants is found in Zimmerman (1975), where the author proposed an operating handbook to explain the use of such instruments in bank loans. Afterwards the covenants were studied in more depth in more de-tailed academic works, with the publication of four fundamental articles. In Jensen and Meckling (1976) the covenant was inserted in organic way in the agency costs theory to solve the conflict between shareholders and bondholders. In the same year Black and Cox (1976) publish the first article on the pricing of covenants, us-ing the bond model proposed by Merton (1974) based on the options theory. The two authors consider the covenant as an option that the underwriter of the bond can use when the covenant is violated. A year later, Myers (1977) included the covenants in the more general theory that explains business motivations for indebt-edness. Smith and Warner (1979) is the first article specifically dedicated to cove-nants, with a detailed classification, and with the first empirical analysis of the dif-ferences between uses of spread standard loan. These four articles can be considered as the scientific base of the literature. In the years following these publications, we see a consolidation of the theme developed in the initial articles, with some analysis

2 Dichev and Skinner (2002), Bradley and Roberts (2004). 3 Leland (1994), Leite (2001).

of banking arguments, like monitoring (Berlin and Loeys, 1988), and several em-pirical works (Kalay, 1982 and Malitz, 1986). In the last few years three important study areas have been looked at in detail: (1) the problems relating to the cove-nants’ violation, (2) the differences between covenants on public debt and on pri-vate debt, and (3) the role of covenants in the optimal choice of the financial struc-ture.

Regarding the first area, most of the literature is on aspects of accounting ex-cept for some articles related to the renegotiation of the debt contract as a result of covenants violation (see, for example, Berlin and Mester, 1992). Upon the publica-tion of Positive Accounting Theory by Watts and Zimmermann (1986), the adop-tion of determinate accounting principles became, in fact, an instrument of business policy, that can be used to avoid the violation of covenants in debt contracts. Most of the literature is focused on the empirical verification of such a hypothesis (Beneish and Press, 1993; Chen and Wei, 1993; Smith, 1993; Sweeney, 1994; De-fond and Jambalvo, 1994; Wilkins and Zimmer, 1996; Beatty, Ramesh and Weber, 2002; Beatty and Weber, 2003). The main focus of the articles related to bank covenants, the second study area, was about the differences within bond covenants in typical banking topics such as: banking relationships (Citron, Robbie and Wright, 1997; Carletti, 2004), the role of collaterals (Rajan and Winton, 1995) and monitoring (Black, et al., 2004; Carletti, 2004). Thanks to the availability of large database on banking loans, some empirical articles have been written about this sector. (Dichev and Skinner, 2002; Niskanen and Niskanen, 2004). There are fewer publications analysing the use of covenants in the optimal composition of the fi-nancial structure of a firm. Leland (1994) was the first theoretical article on this argument, following from other most recent papers that analyze more specific as-pects, like contract theory and agency costs (Leite, 2001; Harvey, Lins and Roper, 2004), and the link with managerial incentives (Douglas, 2002).

If we analyse the empirical works in more depth, a large part5 of them have tried to test the debt covenant hypothesis proposed by Smith and Warner (1979). The methodology used was to compare the average of some balance ratios from groups of firms that have underwritten debt contracts with covenants, with control groups of firms with standard debt contracts, using statistical experiments. In this way it is possible to identify the statistically significant differences between the two groups of firms, and to validate the debt covenant hypothesis. Some secondary re-sults of such studies (Dichev and Skinner, 2002; Mather and Peirson, 2006) with more specific articles (Bradley and Roberts, 2004; Chava, Kumar and Varga, 2005), 5 Booth and Chua (1995), Dichev and Skinner (2002), Beatty, Ramesh and Weber (2002),

make it possible for us to have some preliminary empirical evidence on the price of covenants. We can find out if significant differences in the interest rates between standard debt contracts and those with covenants exist, either for bond issues, or for banking loans. First of all, as found in the first two cited articles, the bank covenants are more numerous and more restricting than bond covenants. Thus, the violation cases are more frequent in bank covenants, and such violations do not seem to be an index of default for the firm. Dichev and Skinner (2002) suppose, therefore, that the banks use the covenants as screening instruments after the loan assignment, in order to modify their conditions, instead of asking for an anticipated refund. Mather and Peirson (2006), however, underline that the role of the cove-nants in the spread reduction is of extreme interest to the financial managers of the firm. From the data of their survey it emerges that the most debated part of the debt contract is the covenants structure. In fact, it often occurs during the negotia-tion procedure, that the choice of the covenants is taken into more consideranegotia-tion than the other decisions, such as, for example, the choice of collaterals or the finan-cial conditions of the loan. Bradley and Roberts (2004) attempt to distinguish be-tween spreads bebe-tween bank loans with covenants and standard loans. The two authors, using a simultaneous estimation model, have found statistically significant values for such differences, as suggested by the debt covenant hypothesis by Smith and Warner (1979). Such statistical techniques have become necessary because the banks tend to use the covenants in risky operations which are already assigned to an increased spread. In order to estimate the impact of the covenant on the loan spread, it is therefore necessary to calculate an integrated estimation of the two aspects, in order to isolate the single contributions.

2. The model

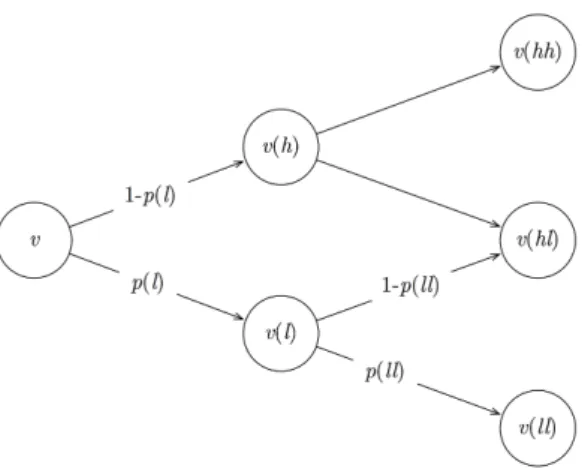

We suppose that a bank must finance a quote !v of a two-year investment project of initial cost v, with market values and probabilities at different states of nature depicted in FIGURE 1. The other part

(

1!!)

v of the project is cover by the firm using equity. The relations between the market values of the project are vll <vl <v<vhl<vh <vhh. The bank loan is at fixed rate rs, with interest and capital payments only at maturity. The firm gives the bank the market value of the project as collateral. To simplify the analytical treatment we let v=1 so the debt cash flow for the firm will be !,0,!!(

1+rs)

2.FIGURE 1. The values of the investment project

In order to obtain non-trivial solutions, the only default position at maturity will be at vll state of nature, i.e.

vll <!

(

1+rs)

2 <vhl (1) With this assumption the expected loss rate at maturity iselrs =plpll PDs !!1" vll !

(

1+rs)

2 # $ %% %% %%% & ' ((( ((( (( LGDs "$$$$$$#$$$$$$% (2)If we suppose neutrality of risk, the bank chooses the interest rate in order to equal the amount of the loan at free-risk rate r, with the expected refund from the loan, i.e.

plpll!vll expected recovery value

at default

! "### ###$ +

(

1"plpll)

!(

1+rs)

2expected loan value at maturity

!########"########$=!

(

1+r)

2(3)

Resolving the equation (3) in respect to the interest rate, we obtain rs=

(

1+r)

2 !plpllvll ! 1!plpll " # $ $ $ % & ' ' ' 1 2 !1 (4)If we put this value in expression (1), supposing that the right inequality is always true, we obtain this more simple non-trivial condition:

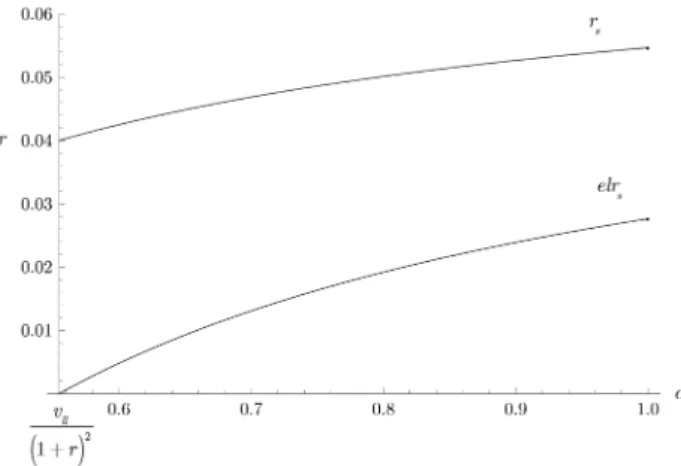

The only variable subject to the control of the bank is the quote financed, so we can calculate the expected loss rate and the interest rate functions in respect to !. It is easy to show that both the functions are growing and concave, i.e.

!elrs !! , !rs !! " # $$ % $$ & ' $$ ( $$>0; !2elr s !!2 , !2r s !!2 " # $$$ % $$$ & ' $$$ ( $$$<0 (6)

as showed in the FIGURE 2. In this model the only way for the bank to reduce the expected loss rate, and, consequently, the interest rate for the firm, is to reduce the quote of the loan6. If we suppose that the firm cannot accept a reduction in the loan below a certain amount, the bank must introduce a covenant in the contract.

FIGURE 2. Expected loss rate and interest rate on standard loan

We can suppose, as a first approximation, that if the firm respects the covenant, in the vll state of nature the bank will be refunded without loss. Therefore, the only default point remains at vll state of nature, if the firm doesn’t respect the covenant. The covenant has no contracting cost, but, if violated, there are some costs of rene-gotiation c for the bank. In this case the bank can ask the anticipated refund of the loan, or can decide to waive the violation. The first decision will be made only if the amount at time two of vl less the renegotiation costs, is greater than the ex-pected value of the loan obtained when waiving the violation, i.e.

vl!c!

(

)

(

1+r)

>pllvll +(

1!pll)

!(

1+rcw)

2 (7) 6 We suppose that the bank can’t ask the firm for more collaterals.in which rcw is the corresponding interest rate. In order to obtain non-trivial solu-tions, we must add a more restrictive conditions on the parameters of the model than those in expression (1). We must suppose that the value obtaining in the case of refund is less than the discounted value of the loan at maturity, i.e.

vl!c!<!

(

1+rcw)

2(

1+r)

(8) In order to calculate the expected loss rate of the loan in cases of anticipated re-fund, and in cases of waiving, we need to define the probability of covenant viola-tion by the firm. We can suppose that the covenant is made in the form of balance sheet ratio, i.e. as financial covenant. So, defining !=ib!ˆic, the probability of covenant violation by the firm in the state vl is equal to pv( )

! , in which!pv

( )

! !!"0, i.e. the violation becomes less likely if the constraint is far from the current value of the balance sheet ratio. We can also suppose, without loss of generality, that !2pv

( )

! !!2 "0 and the standard properties of a probability function. The value of ! has an upper limit k in order to respect the assumption that the bank doesn’t suffer any loss in state vll if the firm respects the covenant. Now we can define the expected loss rate in the case of anticipated refunds as

elrcr =plpv

( )

! PDcr ! "## ##$!1" vl"c"(

)

(

1+r)

"(

1+rcr)

2 # $ %% %% %% & ' ((( ((( ( LGDcr !#########"#########$ (9)and in the case of waiving the covenant violation as elrcw =plpllpv

( )

! PDcw !###"###$!1" vll"c"(

1+r)

"(

1+rcw)

2 # $ %% %% %%% & ' ((( ((( (( LGDcw !########"########$ (10)in which rcr and rcw are the interest rates on the loan in the two cases, respectively. As in expression (3) we can calculate the value of the two interest rates using the equivalence principle in the case of neutrality of risk. The first interest rate is cal-culated resolving the following equation

!

(

1+r)

2=(

1!pl)

!(

1+rcr)

2 expected loan value at maturity!#######"#######$ + +pl"#pv

( )

"(

vl!c!)

(

1+r)

+(

1!pv( )

")

!(

1+rcr)

2 $ % % & ' ( ( amount of expected recovery value at default!#######################"#######################$

giving the value of rcr =

(

1+r)

2 !plpv( )

!(

vl!c")

(

1+r)

" 1!plpv( )

! " # $ $ $ $ $ % & ' ' ' ' ' 1 2 !1 (12)If the bank decides to waive the covenant violation, the interest rate must solve the following equation

!

(

1+r)

2=(

1!plpll)

!(

1+rcw)

2expected loan value at maturity

!#########"#########$+ +plpll"#pv

( )

"(

vll!c!(

1+r)

)

+(

1!pv( )

")

!(

1+rcw)

2 $ % % & ' ( ( expected recovery value at default!#########################"#########################$

(13)

obtaining the value of

rcw =

(

1+r)

2 !plpllpv( )

! vll!c"(

1+r)

" 1!plpllpv( )

! " # $ $ $ $ $ % & ' ' ' ' ' 1 2 !1 (14)We can generalize the model defining the set O!

{

(

pl,pll)

,(

vl,vll)

,a,c,r}

of out-side variables, and the setI !

{ }

!," of inside variables, directly controlled by the bank. Using expression (14) and the inequality (8) we can define the feasible set of the parameters for this first model as!k "

( )

O,I :!> vll 1+r(

)

2,vl#c!< !(

1+rcw)

2 1+r(

)

,"<k $ % && && ' && && ( ) && && * && && (15) We can, also, summarize and simplify in a compact way the values of the interest rates as 1+rj(

)

2 =(

1+r)

2 !PDj"RRj 1!PDj , j#{

s,cr,cw}

(16) and of the expected loss rates can be simplify aselrj =PDj 1! RRj

(

1!PDj)

1+rj(

)

2 !PDj"RRj # $ % % % % & ' ( ( ( (, j){

s,cr,cw}

(17)in which the recovery rate is calculated only on the capital part of the loan. The value of the PDs and RRs are showed in TABLE 1.

Type of loan PD RR

Standard plpll vll !

Covenant with anticipated refund plpv

( )

!(

vl!c!)

(

1+r)

!Covenant with waive plpllpv

( )

! "#$vll!c!(

1+r)

%&' ! Table 1. Values of the parameters for the different type of loansFor a standard loan, the bank can reduce the expected loss rate by reducing the quote financed, while in the case of financial covenant the bank can also modify the constraint on the balance ratio used. In this case we must consider two different cases, the waive and the anticipated refund decisions by the bank.

We can define the set of parameters for which the bank decides to waive the covenant violation as

Wk !

{

( )

O,I " #k :pllvll+(

1$pll)

!(

1+rcw)

2$(

vl$c!)

(

1+r)

%0}

(18) and the corresponding set of anticipating refund straightforward as Rk ! "k#Wk. Now the model is fully defined over all the variables and we can show the values of expected loss rates over the !k set for the inside I variables. In FIGURE 3 you find the three elr defined on the part financed by the bank.Figure 3. Expected loss rates for standard and covenant loans, pv

( )

! =30%,c=0.5% The bold line represents the effective elr when the bank decides to insert acove-nant in the loan contracts. In this case, the debt covecove-nant hypothesis is validated: the expected loss rate of the covenant loan is lower than the elr on standard loan. The discontinuity in the elr depends on the presence of renegotiation costs.

Figure 4. Expected loss rates for standard and covenant loans, pv

( )

! =60%,c=0.5%Figure 5. Expected loss rates for standard and covenant loans, pv

( )

! =30%,c=1.8% If the probability of violation becomes greater, the differences in the expected lossrates become smaller as showed in FIGURE 4. Only if we suppose a very high prob-ability of violation, will the debt covenant hypothesis not be validated. This strictly depends on the presence of the renegotiation costs that are charged to the loan spread of the firm. You can see in FIGURE 5 that if we change the value of renegotiation costs, maintaining the initial probability of covenant violation, the debt covenant hypothesis is no longer valid. The expected loss rate for the cove-nant loan, at the beginning of the Wk set, is greater than the expected loss rate on standard loan.

Now we can change the hypothesis on the covenant violation with a more realis-tic one. We suppose that if the firm respects the covenant, in the vll state of nature the bank will be only partial refunded. As before the bank will decide to ask for anticipated refund of the loan in the first time period if expression (7) is true. The expected loss rate in this case remains the same as before, because if the firm vio-lates the covenant the values of the LGD in the second time period do not change. Instead, the elr when the bank decide to waive the violation, will change to

elrcw =plpll PDcw !!pv

( )

! 1" vll"c"(

1+r)

"(

1+rcw)

2 # $ %% %% %% & ' ((( ((( (+(

1"pv( )

!)

1"vll +f( )

! "(

1+rcw)

2 # $ %% %% %% & ' ((( ((( ( ) * + + + + , -. . . . expected LGDcw "$$$$$$$$$$$$$$$$$$$$$$$$$$#$$$$$$$$$$$$$$$$$$$$$$$$$$% (19)in which f

( )

! is the increase on the refund that depends on the limit of the cove-nant fixed by the bank. We can suppose that this value decreases when this limit is far from the current value of the financial ratio in the balance sheet, i.e. !f( )

! !!"0. We can also suppose, withou any loss of generality, that !2f( )

! !!2 "0. The interest rate will be calculated resolving the following equa-tion!

(

1+r)

2=(

1!plpll)

!(

1+rcw)

2expected loan value at maturity !#########"#########$+

+plpll"pv

( )

"(

vll!c!(

1+r)

)

+(

1!pv( )

")

(

vll +f( )

")

#$ %&'

expected recovery value at default

!########################"########################$

(20)

giving the value of

rcw=

(

1+r)

2 !plpll pv( )

! vll!c"(

1+r)

" +(

1!pv( )

!)

vll+f( )

! " " # $ $ $ % & ' ' ' 1!plpll " # $ $ $ $ $ $ % & ' ' ' ' ' ' 1 2 !1 (21)the expected loss rate in the case of waiving with the set of inside and outside vari-ables. In this case the feasible set of the parameters are changing in the following way ! "

( )

O,I :!> vll 1+r(

)

2,vl#c!< !(

1+rcw)

2 1+r(

)

$ % && && ' && && ( ) && && * && && (22) and the set in which the bank decides to waive the violation asW !

{

( )

O,I " #:pllvll +(

1$pll)

!(

1+rcw)

2$(

vl$c!)

(

1+r)

%0}

(23) If we calculate the partial derivatives of the expected loss rate with respect to !, supposing that the bank cannot change the quote financed, we find that:!elrcw !pv

( )

! "0 ! "## ##$ !pv( )

! !! #0 ! "## ##$ #0, !elrcw !f( )

! #0 ! "## $## !f( )

! !! #0 ! "## $## "0 (24)The signs in expression (24) are determined using the assumptions made on the probability of violation and of the increase of the refund. The results in expression (24) are necessary, but not sufficient conditions to find a minimum in the expected loss rate, i.e.

min

!!Welrcw

(

pv( )

! ,f( )

!)

(25)In fact, if we expand the first order condition !elrcw !pv

( )

! !pv( )

! !! + !elrcw !f( )

! !f( )

! !! =0 (26)we find the following compact expression f

( )

! +c"(

1+r)

! "# $%& 'pv( )

! '! (0 ! "## ##$ )!"#1)pv( )

! $%&'f( )

! '! (0 ! "## $## =0 (27)in which there are some probability of finding a value of ! that respects the first order condition. In the next paragraph we build an empirical model in which we define analytically both the functions pv

( )

! and f( )

! , finding a effective minimum for the elrcw.Now we can relax the hypothesis of the fixed quote financed with a more realis-tic one in which the bank can decide to change this value. Thus, the minimization problem (25) becomes

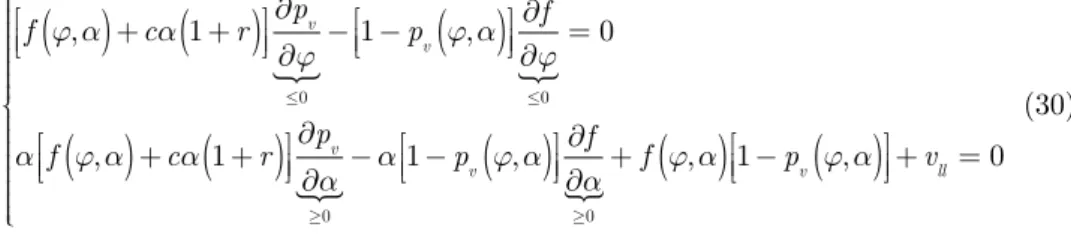

min !,"

with the first order conditions as follow !elrcw !pv

( )

!," !pv( )

!," !! + !elrcw !f( )

!," !f( )

!," !! =0 !elrcw !pv( )

!," !pv( )

!," !" + !elrcw !f( )

!," !f( )

!," !" + !elrcw !" =0 " # $$ $$ $$$ % $$ $$ $$ $ (29)Expanding the system of equations (29) we obtain the following compact expres-sions f

( )

!," +c"(

1+r)

! "# $%& 'pv '! (0 ! )!"#1)pv( )

!,"$%&'f '! (0 ! =0 "!"#f( )

!," +c"(

1+r)

$%&'pv '" *0 !)"1)pv( )

!," ! "# $%&''"f *0 !+f( )

!," 1)pv( )

!," ! "# $%&+vll =0 + , --. (30)As above there are some probability of finding a value of the pair

( )

!," that solves the system of equations.3. An empirical model

We suppose, in order to simplify the analysis, that the bank must finance a part of the investment project of a new firm. The balance sheet of the firm becomes as in

TABLE 2.

Assets Liabilities

Fixed assets 1 Capital 1! !

Bank debt !

Total assets 1 Total liabilities 1

Table 2. Balance sheet of the firm at t = 0

The bank decides to insert a financial covenant on the loan contract with a con-straint on the financial leverage !

(

1! !)

of the firm. That is, if the leverage be-comes greater than lˆ, the bank can ask for an anticipated refund of the loan. At time one, if the value of the project becomes vl, the firm will incur in a loss equals to the difference between the initial value of the project, one, and the currentmar-ket value (TABLE 3).

Assets Liabilities

Fixed assets vl Capital 1! !

Loss !

(

1!vl)

Bank debt !

Total assets vl Total liabilities vl

Table 3. Balance sheet of the firm at t = 1, before the capital increase

In order to cover the loss the shareholders must increase the capital by the same amount. They can decide to pay in all the increase with cash as in TABLE 4.

Assets Liabilities

Fixed assets vl Capital 1! !+1!vl

Cash 1!vl Loss !

(

1!vl)

Bank debt !

Total assets 1 Total liabilities 1

Table 4.Balance sheet of the firm at t = 1, after the capital increase with cash

The shareholders can also decides to postpone the capital paid-in in the second time period, so the balance sheet resembles TABLE 5.

Assets Liabilities

Fixed assets vl Capital 1!!

Credit to

shareholders 1!vl Uncalled capital 1!vl

Loss !

(

1!vl)

Bank debt !

Total assets 1 Total liabilities 1

Table 5.Balance sheet of the firm at t = 1, after the capital increase with postpone paid-in

In TABLE 4 the financial leverage remains constant, but in TABLE 5 the bank

be-comes greater, i.e.

lp = !

1!!!

(

1!vl)

(31)What happens in the two cases if the final market value of the project becomes vll ? In TABLE 4, if we suppose that vll +

(

1!vl)

>!(

1+rs)

2, the bank will give a total refund, in TABLE 5 the bank will receive only vll . If the shareholders decide to cover only a part of the capital paid-in with cash, the balance sheet becomes as inTABLE 6

Assets Liabilities

Fixed assets vl Capital 1!!+"

Credit to

shareholders 1!vl!! Uncalled capital 1!vl!!

Cash ! Loss !

(

1!vl)

Bank debt !

Total assets 1 Total liabilities 1

Table 6.Balance sheet of the firm at t = 1, after the mixed capital increase

with the following financial leverage

lm = !

1!!+"!

(

1!vl)

,0"""1!vl (32) Now we can define the LGD for the bank, in the case of standard loan, using the value of the cash paid-in from the shareholders asLGDs= 0 if !

(

1+rs)

2 vll !"!1"vl 1" vll+" !(

1+rs)

2 if 0!"< !(

1+rs)

2 vll # $ %% %% %% %% & %% %% %% %% (33)rs = r if !

(

1+rs)

2 vll !"!1"vl 1+r(

)

2 "plpllvll+" ! 1"plpll # $ % % % % & ' ( ( ( ( 1 2 "1 if 0!"<!(

1+rs)

2 vll ) * ++ ++ ++ +++ , ++ ++ ++ ++ + (34)Using these results, the expected loss rate for the bank will change in the following

elrs = 0 if !

(

1+r)

2 !plpllvll 1!plpll(

)

vll+plpll """1!vl plpll#1!(

1!plpll)

(

vll+")

!(

1+r)

2!plpll(

vll+")

$ % && && &&& ' ( ))) ))) )) if 0""< !(

1+r)

2!plpllvll 1!plpll(

)

vll +plpll * + ,, ,, ,, ,, -,, ,, ,, ,, (35)As noted in the last paragraph, if the value of the parameters belongs to the W set defined in expression (23), the bank will waive the covenant violation. Now we suppose that the bank cannot change the value of the part financed, and the pa-rameters belong to the W set. With this assumption we must define both the func-tions pv

( )

! and f( )

! in order to search for a minimum point of the expected loss rate. Firstly, we can suppose that the probability of violation, given the initial lev-erage of the firm !(

1! !)

and the limit lˆ fixed by the bank becomes, follows an exponential probability function, aspv

( )

! =1 "e!!

" (36)

Secondly, we must find an analytical expression for f

( )

! . In our example the func-tion is equal to the value of cash !, thus, using expression (32) and the following!=ˆl!"

(

1!")

we findf

( )

! ="(

1+!!"!)

"+!!"! !vl (37)

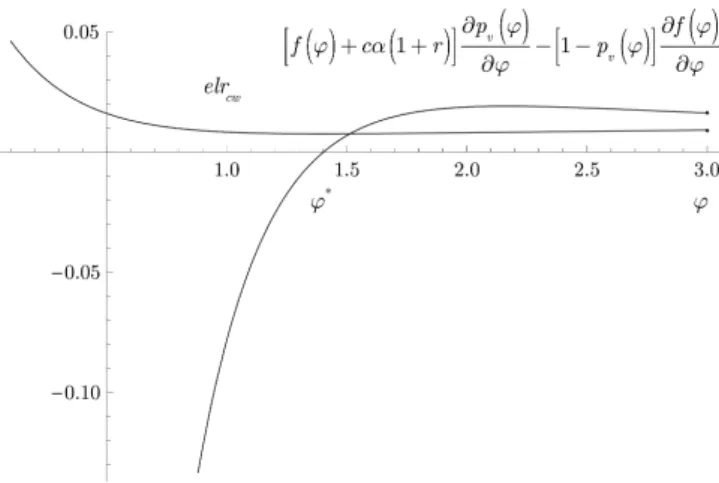

With this hypothesis the equation (27) doesn’t have an analytical solution, there-fore analysing their graph we can find an optimal value of !*. In FIGURE 6 you can see that an optimal point exists, and this point is a minimum for the expected loss rate.

Figure 6. Solution of the minimization problem c=1%,!=80%,"=0.3

This result can be used by a bank with more simple hypothesis on the distribution of the financial ratio, for example using the triangular distribution, or using di-rectly the values of the empirical probability of violation (Unicredit Banca Medio-credito, Centrale dei Bilanci, 2005).

Now we can relax the hypothesis of constant part financed, with the more real-istic one in which the bank can define even the value of !. In order to simplify the treatment of the analitycal expressions, we change the ! variable using the limit of financial leverage l directly. The functions pv

( )

l,! and f l( )

,! becomepv

( )

l,! =1 "e !l!!( )1!! " (38) f l( )

,! =!+! l !vl (39)We can, putting this two espression in system (30), verify empirically if an optimal point of the pair

( )

l,! exists (FIGURE 7). We use an higher value of c to find an inner solution of the minimization problem, i.e. the solution belogn to the W set as show in FIGURE 7. This point is a saddle point as showed in FIGURE 8 in which we draw the level curves of elrcw over the plan( )

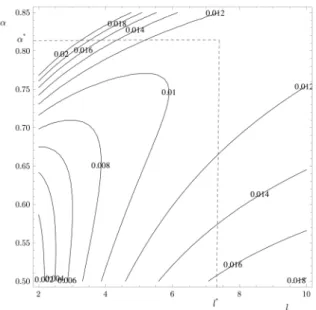

l,! . As a final result the bank can reduce the elrcw value defining first the value of the quote financed, then chosing the optimal value of the limit of the financial leverage in the covenant. Otherwise the bank can offer the firm some optimal combination of the pair( )

l,! , so the firmitself can choose the best combination.

Figure 7. Solution of the minimization problem c=1%,!=2

4. Conclusions

In this work we propose a model to be able to price bank loans with covenants. Using this instrument a bank can reduce the expected loss rate of the loan, offering a lower rate to the firm. In order to define the value of the spread on this loan cor-rectly, the bank must estimate the probability of covenant violation and the con-tribution of the covenant to the LGD when the firm respects this constraint. When the variables of the problem belong to the set for which the bank decides to waive the covenant, the choice of the limit of the financial ratio for the covenant can be decided with a minimization problem. Otherwise, the bank can modify the elr of the loan without asking for more collateral, but by choosing a combination of the quote financed and of the limit of financial ratio. The proposed model can be inte-grated in the internal models of the banks to calculate the credit risk of the loan, even more simply by using the empirical value of the probability of covenant viola-tion.

The proposed pricing model can be expanded upon by using a different hy-pothesis for the definition of the probability of covenant violation, and relaxing the neutrality of risk of the bank in order to calculate even the unexpected loss rate.

5. References

ASQUITH P., WEBER J., BEATTY A. (2005), Performance Pricing in Bank Debt

Contracts, Journal of Accounting and Economics, 40 (1-3), pp. 101-28.

BEATTY A., RAMESH K., WEBER J. (2002), The Importance of Accounting Changes

in Debt Contracts: The Cost of Flexibility in Covenant Calculations, Journal of Accounting and Economics, 33 (2), pp. 205-27.

BEATTY A., WEBER J. (2003), The Effects of Debt Contracting on Voluntary

Ac-counting Method Changes, The AcAc-counting Review, 78 (1), pp. 119-42.

BENEISH M.D., PRESS E. (1993), Costs of technical violation of accounting-based

debt covenants, The Accounting Review, 68 (2), pp. 233-57.

BERLIN M., LOEYS J. (1988), Bond Covenants and Delegated Monitoring, Journal

of Finance, 43 (2), pp. 397-412.

BERLIN M., MESTER L. (1992), Debt Covenants and Renegotiation, Journal of

Fi-nancial Intermediation, 43 (2), pp. 95-133.

BLACK E.L., CARNES T.A., MOSEBACH M., MOYER S.E. (2004), Regulatory

Moni-toring as a Substitute for Debt Covenants, Journal of Accounting and Econom-ics, 37 (3), pp. 367-391.

BLACK F., COX J.C. (1976), Valuing corporate securities: Some effects of bond

in-denture provisions, Journal of Finance, 31 (2), pp. 351-67.

BOOTH J.R., CHUA K. (1995), Structure and Pricing of Large Bank Loans, FRBSF

Economic Review, 3 (1), pp. 52-62.

BRADLEY M., ROBERTS M.R. (2004), The Structure and Pricing of Corporate Debt

Covenants, mimeo.

CARLETTI E. (2004), The Structure of Bank Relationships, Endogenous Monitoring,

and Loan Rates, Journal of Financial Intermediation, 13 (1), pp. 58-86.

CHAVA S., KUMAR P., WARGA A. (2005), Agency Costs and the Pricing of Bond

Covenants, mimeo.

CHEN K.C.W., WEI K.C.J. (1993), Creditors’ Decisions to Waive Violations of Ac-counting-Based Debt Covenants, The Accounting Review, 68 (2), pp. 218-32.

CITRON D., ROBBIE K., WRIGHT M. (1997), Loan Covenants and Relationship

Banking in MBOs, Accounting and Business Research, 27 (4), pp. 277-96.

DEFOND M.L., JIAMBALVO J. (1994), Debt covenant violation and manipulation of

accruals, Journal of Accounting and Economics, 17 (1-2), pp. 145-76.

DICHEV I.D., SKINNER D.J. (2002), Large-Sample Evidence on the Debt Covenant

Hypothesis, Journal of Accounting Research, 40 (4), pp. 1091-123.

DOUGLAS A.V.S. (2002), Capital Structure and the Control of Managerial

HARVEY C.R., LINS K.V., ROPER A.H. (2004), The Effect of Capital Structure when Expected Agency Costs are Extreme, Journal of Financial Economics, 74 (1), pp. 3-30.

JENSEN M.C., MECKLING W.H. (1976), Theory of the firm: Managerial behavior,

agency costs and ownership structure, Journal of Financial Economics, 3 (4), pp. 305-60.

KALAY A., (1982), Stockholder-bondholder conflict and dividend constraints,

Jour-nal of Financial Economics, 10 (2), pp. 211-33.

LEITE T. (2001), Optimal Financial Structure: An Incomplete Contracting Model,

Scandinavian Journal of Economics, 103 (4), pp. 707-22.

LELAND H. (1994), Corporate Debt Value, Bond Covenants, and Optimal Capital

Structure, Journal of Finance, 49 (4), pp. 1213-52.

MALITZ I. (1986), On Financial Contracting: The Determinants of Bond Covenants,

Financial Management, 15 (2), pp. 18-25.

MATHER P., PEIRSON G. (2006), Financial covenants in the markets for public and

private debt, Accounting and Finance, 46 (2), pp. 285-307.

MERTON R. (1974), On the pricing of corporate debt: The risk structure of interest

rates, Journal of Finance, 29 (2), pp. 449-70.

MYERS S.C. (1977), Determinants of corporate borrowing, Journal of Financial

Economics, 5 (2), pp. 147-75.

NISKANEN J., NISKANEN M. (2004), Covenants and Small Business Lending: The

Finnish Case, Small Business Economics, 23 (2), pp. 137-49.

PARK C. (2000), Monitoring and Structure of Debt Contracts, Journal of Finance, 55 (5), pp. 2157-95.

RAJAN R., WINTON A. (1995), Covenants and Collateral as Incentives to Monitor,

Journal of Finance, 50 (4), pp. 1113-46.

SMITH C., WARNER J. (1979), On Financial Contracting: An Analysis of Bond

Covenants, Journal of Financial Economics, 7 (June), pp. 117-61.

SMITH C.W. (1993), A perspective on accounting-based debt covenant violations,

The Accounting Review, 68 (2), pp. 289-303.

SWEENEY A.P. (1994), Debt-covenant violations and managers’ accounting

re-sponses, Journal of Accounting and Economics, 17 (May), pp. 281-308.

TORABZADEH K.M., ROUFAGALAS J., WOODRUFF C.G. (2000), Self-Selection and

the Effects of Poison put/call Covenants on the Reoffering Yields of Corporate Bonds, International Review of Economics and Finance, 9 (2), pp. 139-56.

UNICREDIT BANCA MEDIOCREDITO, CENTRALE DEI BILANCI (2005), I covenant di

bilancio nei finanziamenti a medio e lungo termine, Bancaria Editrice, Roma.

WATTS R.L., ZIMMERMANN J.L. (1986), Positive Accounting Theory, Prentice-Hall,

WILKINS T., ZIMMER I. (1996), Economic Consequences of Debt Covenant Viola-tion: The Case of Inno-Pacific Holdings Limited, British Accounting Review, 28 (2), pp. 121-37.

ZIMMERMAN C.S. (1975), An Approach to Writing Loan Agreement Covenants,