Technology-driven

Targeted Marketing

Mark Smith, Executive VP at Portrait Software, is a 15-year veteran in customer analytics. Prior to Portrait, Smith was a co-founder of Quadstone, a company that came to be known for its innovative customer analytics solutions.

By Mark Smith

Executive Vice President, Portrait Software

ExEcutivE SummaryIn today’s increasingly tight financial environment, imagine having to report to your chief executive officer or board that the six-figure sum spent to reduce customer churn actually increased it or that half the direct marketing budget was totally wasted.

Not a scenario that anyone would welcome but one that goes on continually in financial services organisations and most of the time, the organisation has no idea of the ‘levers’ behind such undesirable results.

However, a revolutionary analytical approach called uplift modelling can provide true insight into direct marketing targeting to reduce budget spend, communicate with fewer customers but deliver a greater revenue result.

Combine this with ‘individualisation’ strategies that intelligently provide more relevant messages at each and every customer interaction point and cross-sell and upsell rates skyrocket.

inSight into targEting

We need to target customers whose behaviour we can change, rather than taking credit for outcomes that would have occurred even without our intervention. This paper discusses the use of a new kind of modelling – uplift modelling – to improve the profitability and effectiveness of direct marketing spend. We start from five observations about targeted marketing aimed at demand generation (cross-selling, up-selling and deep-selling). These are:

1. Direct marketing works better for some customers than others.

2. Direct marketing has negative effects on some customers, reducing their level of spend.

3. The customers who spend most when targeted are not necessarily the best targets for marketing: some of those whose spend is high when targeted would spend as much, or more, without treatment.

Volume 3 Number 1 2009 a Financial Standard publication 4. Not all purchases by targeted customers are caused by our

direct marketing. Some would have bought anyway. 5. The standard approach to targeting involves modelling only

the treated group from a previous campaign. This allows us to estimate each customer’s conditional probability of purchase if targeted, but not the change in that probability resulting from our targeted action.

Mathematically, such “response” models predict Prob (purchase treatment) (1)

(the probability of purchase given treatment) while our returns are based on uplift, defined as

Prob (purchase treatment) – Prob (purchase no treatment). (2) In light of the points above, it is clear that traditional methods of targeting are suboptimal, based as they are on so-called “response” models that actually predict conditional purchase probability1 (equation 1).

Ideally, we should model the difference in behaviour between the treated and control groups. This would allow us to predict the change in each customer’s purchase probability when treated (equation 2). We call such models uplift models.

In this paper, we show real-world examples of how uplift models generate higher returns on marketing spend, often from lower targeting volumes. This constitutes a multiple win, because sales increase while targeting costs are reduced. Additionally, where incentives are used, the cost of these is usually significantly reduced because they are not “wasted” on customers who would purchase anyway. Customer satisfaction also tends to improve as customers who dislike being contacted are less likely to be targeted.

The same shift in approach can also bring even larger benefits in the area of customer retention, where similar considerations apply, and where it is distressingly common for retention activity to drive up attrition rates. Adoption of uplift modelling involves a move from targeting on the basis of estimated attrition probability to an approach based on savability. We illustrate that such a change can have a very significant impact on the bottom line, which is natural given the counterproductive effect of spending money to drive customers away.

Who can BEnEfit from uplift modElling? Uplift modelling requires control groups and is of greatest benefit in competitive markets where customers are subject to many influences, so it is perfect in financial services. It can be used to reduce costs, to increase revenues and to enhance customer satisfaction and retention.

Uplift modelling allows businesses to optimise their targeting of customers in such a way as to maximise the return on investment of marketing spend or to optimise some alternative goal. The benefits from this in the areas of demand generation and customer retention can include:

l Reducing the number of customers required to achieve a given level of business stimulation and thus reducing costs. l Increasing the level of business generation achieved for any

given level of spend.

l Lowering customer dissatisfaction by decreasing the level of negatively received material.

l Enhancing understanding within the business of the effectiveness of various kinds of marketing spend.

l Eliminating many or all of the negative effects associated with mistargeted campaigns.

l Increasing customer retention.

Additionally, there is the potential to use these methods in other areas, such as optimising the management of actions based on behavioural credit scores, optimising collections targeting and optimising response to customer complaints.

There are four qualification criteria important for evaluating the potential impact of uplift modelling:

l Control groups: Uplift modelling absolutely requires the systematic use of randomised control groups, so is only of benefit to businesses that already use, or are prepared to adopt this approach.

l Size of customer base: Businesses with large customer bases will tend to benefit disproportionately more than those with fewer customers, because reasonable volumes are needed to model this second-order effect. Though dependent on response rates, uplifts and the ratio of treated to control group sizes, we would not normally expect the technique to work well on campaigns targeting fewer than about 100,000 people.

l Influences: Uplift modelling is of particular benefit in situations in which many factors influence a customer’s behaviour. Companies with a largely channel, single-communication route to customers, in less competitive markets, will benefit less from uplift modelling than those with many channels and communication paths and greater competition.

l Overall level of uplift: Portrait believes that the approach of uplift modelling is correct even when the overall level of uplift is high and there are no obvious negative effects involved in a campaign. In these circumstances there are alternatives, albeit suboptimal ones. In circumstances where campaigns show little overall uplift, or negative overall uplift, other than a complete change of approach, there is no known alternative to uplift modelling.

croSS-SElling in financial SErvicES

The value of a new banking product is often high enough to justify cross-sell mailings, even when these generate additional sales in only one in a thousand cases. However, comparatively small segments are often responsible for most or all of the extra sales generated. We have used uplift models to identify such segments, resulting in increases in campaign profitability by up to five times. A typical scenario involves cross-selling activity aimed at increasing product holding. The value of many banking products is high, so that even an increase in product take-up as low as a tenth of a per centage point can provide a positive return on investment for mailings. However, we have shown that with appropriate targeting, we can usually achieve between 80 per cent and 110 per cent of the same incremental sales while reducing mailing volumes by factors ranging from 30 per cent to 80 per cent. Because the banks in question have themselves attempted to model uplift, they typically have historical data allowing full longitudinal validation2 of results. One of the complicating factors in these scenarios is that the uplift from the campaign is usually significantly smaller than

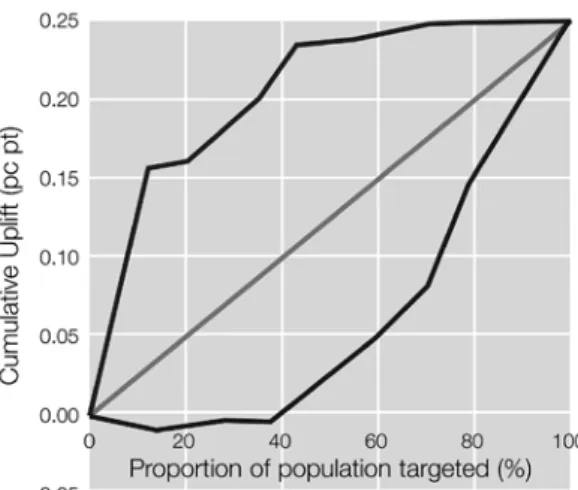

the natural purchase rate of the product being promoted – typically by a factor of five to twenty. It is therefore not unusual to see a purchase rate in the control group of around 1 per cent, and in the treated group of 1.1 per cent. However, drivers of the base purchase rate are often quite different from those of the incremental purchases resulting from the campaign. Graph 1 shows an example of one such campaign. Here, the net effect of the campaign was to increase the uptake of the product by a quarter of a per centage point. However, the uplift model shows that over 60 per cent of the increase in sales comes from just 10 per cent of the targeted population, 90 per cent comes from 40 per cent of the population and 99 per cent comes from 70 per cent of the population. Notice also that the “champion” model produced substantially worse results than random targeting – in fact, in this case, reversing the ranking would have been very much more effective than using its actual output.

compariSon of targEting StratEgiES

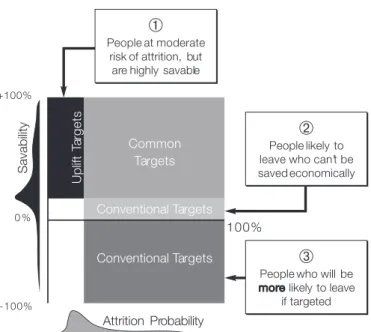

Conventional models wastefully target some customers whose outcomes would be almost as good or better if not treated. Uplift models identify an extra group of customers whose outcomes can be profitably improved but who are overlooked by conventional models because the absolute level of their outcome falls below some arbitrary threshold.

Graph 2 shows the probability of attrition3 on the horizontal axis, and savability – decrease in churn likelihood when treated vertically. We can identify three swap sets.

1. Uplift models target a set of people whose probability of attrition is not huge, but who can be made much less likely to leave4 (segment 1, top left, burgundy). Retention activity can be very effective here. In the context of demand-generation, the corresponding people are those whose probability of purchase when targeted is not high, but who are unlikely to purchase at all without inducement. We call this segment ‘the persuadables’.

Volume 3 Number 1 2009 a Financial Standard publication 2. The second swap set consists of people who are at considerable

risk of attrition, but are unlikely to be saved by our action (segment 2, thin pink strip above the horizontal axis). Trying to retain them costs more than the likely return. In a demand-generation setting, the corresponding people are good customers, who spend money, but whose behaviour is largely unaffected by our actions. Uplift models discourage targeting these groups while conventional models recommend them. 3. The third swap-set is segment 3 (blue, below the axis), which

is targeted using the conventional approach, but not an uplift approach. This consists of people whose outcomes are worse if treated, so we actually spend money to drive customers and revenue away in this segment. There seems no argument at all for such expensive and counterproductive activity for this segment that we call ‘the do-not-disturbs’.

rESponSE codES, incEntivES, cauSation and thE critical importancE of control groupS Response codes do not prove that a customer purchase is caused by the associated marketing action. This is especially true when incentives are offered, as customers have a strong motive for using discount codes even when they would have purchased anyway. Only control groups allow reliable proof of causality. The potential for being misled about the effectiveness of marketing is largest when a campaign involves a discount or other incentive. Most people will, if they are aware of a discount, use it even if they would have purchased the same product anyway.

The conclusion, therefore, is that rigorous use of control groups is the only safe way to assess the true impact of a marketing campaign.5

nEgativE EffEctS

Negative effects are real and costly. They are most clearly seen in some retention activity, but can also be hidden in marketing campaigns that are successful overall. They both reduce revenue and increase costs, so merit special attention.

It’s not hard to understand why negative effects often occur in retention activity. The conventional approach first identifies customers at high risk of attrition. By and large, these are people who are already dissatisfied in some way. An intervention, particularly by phone, runs a high risk of the customer’s responding by asking for immediate cancellation – bringing forward some attrition and crystallising other cancellations that may otherwise not have happened at all because of customer apathy.

making it rElEvant hElpS to makE it a SuccESS One user of Portrait’s Uplift Modelling reports that even in demand-generation applications (cross-selling, deep-selling and up-selling) there are almost always material negative effects in the last one or two deciles by uplift score, and on this basis would never advocate a 100 per cent mailing, no matter how unarguably attractive the offer seems.

Even for those in our persuadables segment, marketing campaigns that deliver relevant, individual offers are much more likely to result in success with ad fatigue and do-not-call lists making customers unwilling to interact with companies that present irrelevant messages. They expect relevance. They expect to be

known, remembered and understood. Unfortunately, their expectations often go unmet. While many organisations are able to “personalise” their direct marketing campaigns by incorporating the customer’s name into communications or targeting specific segments, few companies have yet reached this level of individualised “one-to-one” marketing and cross-channel communication.

The key issue in getting from personalisation to individualisation is the ability to be relevant at all times, across all channels with co-ordinated, customer-specific marketing that is built around the individual’s circumstances, not just their name.

Why are companies failing to interact with customers in a relevant fashion? To a great extent, they are challenged by the limitations of today’s customer management technology which is constrained in its ability to custom-fit interactions to the customer. Echoing this, analyst firm Gartner states, “CEOs are turning to customer-centric strategies, and most of the deployed, back-office systems were not optimised for that.”6

To meet today’s growth objectives and remain competitive, leading marketers and customer experience managers are investing in smart systems and building the capabilities necessary to interact with their customers in a relevant and truly personal manner – the relevance revolution.

thE BattlEground of thE rElEvancE rEvolution

This revolution goes far beyond the mass marketing that has dominating the mass production economy. Instead, this revolution will occur in the intimacy of one’s customer interactions – whether they are outbound or inbound. It will encompass all channels of communication and all interactive media.

In sectors such as retail, telecommunications and financial services, companies now provide powerful experiences by taking action – in real-time – based on the preferences, priorities, needs and concerns of the individual customer. Leveraging a full view of customer data and information, these companies are able to dynamically communicate with their customers and:

l Present the right message, right when the customer is engaged

l Automatically create a connected customer experience – across all channels

l Create an experience that drives positive word-of-mouth across social networks

l Ensure campaigns are targeted for optimal results l Reduce customer attrition rates

Unfortunately, few companies possess these rich capabilities. They face several shortcomings and challenges. Marketers and other customer-facing managers are undermined by:

‘Mass personalisation’ of outbound messages. Marketing performance erodes when outbound campaigns do not speak to the real concerns of customers. In many cases, companies are hampered by data schemes and technical hurdles that make it difficult to rapidly launch timely campaigns to highly targeted segments. While their competitors may be moving to campaign turnaround times measured in days or even hours, some corporate marketers must plan campaigns months ahead given

the coding requirements and data limitations associated with their existing manual and brute-force approaches. The effectiveness of outbound marketing depends on being able to rapidly act and deliver relevant recommendations that will truly effect a change in behaviour.

Limited insight undermines inbound interactions. Particularly damaging to customer relationships is the inability to effectively handle inbound or customer-initiated interactions in an individualised fashion. When a customer calls a company with a specific interest or concern in mind, it is off-putting to be given a generalised product pitch. Lacking insight into the customer’s preferences or intelligent prompts to suggest appropriate messages, customer representatives are prone to turn a valuable inbound opportunity into a poor experience. Such mistakes have costly consequences. Not only do companies miss an opportunity to cross-sell and up-sell, they run the risk of undermining customer loyalty.7

Misaligned cross-channel communications. As media and channels proliferate, companies are struggling to present a unified image to their customers and manage them in a way that is consistent with prior interactions. For instance, they may respond to a television or radio advertisement by researching a product online. They may then contact a call centre to ask further questions or request suggestions. They may then actually purchase the product in a retail store or online at the corporate web site. Given the array of possible scenarios, marketers and customer-facing managers are challenged to ensure the messages and offers that are presented in these different channels are clear, compelling and, most importantly, consistent.8

Islands of disconnected data. The fragmentation of data represents a key problem in terms of channel consistency. If customer interaction data is locked in different databases (dependent on where an interaction or transaction occurs), then it becomes

impossible to manage interactions in a seamless manner. Customers that deal with companies that are incapable of learning and remembering what transpired in the past are liable to feel neglected and mistreated. What’s needed is a true “customer portrait” – one that draws on all appropriate data. individualiSEd cuStomEr campaignS:

thE markEtEr’S nEW WEapon in thE rElEvancE rEvolution

To differentiate themselves and create more profitable customer relationships, companies increasingly are relying on Intelligent Customer Interaction.

Central to individualised customer campaigns is an approach that leverages sophisticated customer analytics to engage in relevant and continuous customer dialogs. Best-in-class marketers are now putting superior customer intelligence at the heart of all marketing campaigns and customer interactions. This enables them to ensure that messages and offers are tightly linked to the individual preferences and priorities of their customers. Consistent relevance changes the way companies communicate with their prospects and customers, laying the foundations for far greater marketing performance and customer outcomes. Consider some of the benefits and advantages:

l Higher Response Rates and Conversions. By engaging customers in an individualised fashion, marketers increase response rates. The right offer at the right time to the right person turns a marketing action into a sales conversion. In other words, more frequent campaigns to smaller, focused audiences. l Enhanced Cross-Selling and Up-selling. By presenting relevant and individualised offers, companies achieve higher acceptance rates, greater share of wallet and new opportunities to drive organic growth.

Volume 3 Number 1 2009 a Financial Standard publication l Stronger Retention and Loyalty. By rapidly identifying

and executing the appropriate action, particularly for a customer that has a problem, companies can retain customers more effectively. Higher customer loyalty translates into greater profitability and higher customer lifetime value. l Stronger Marketing Performance. By leveraging

customer insight to take appropriate actions, best-in-class companies now generate far greater returns on their marketing investments than their rivals. At a time when marketing budgets have ceased to grow (and may be shrinking), high marketing productivity is a clear competitive differentiator. l Turning Contact Centres into Profit Centres. By enabling

service reps to rapidly identify the core needs of customers and make relevant recommendations, contact centre managers can drive profitable revenue and deepen loyalty.

rEal World SuccESS: rEaching thE nExt lEvEl of individualiSEd markEting intEractionS Best-in-class companies are differentiating themselves in financial services through individualised and intelligent customer interaction.

In a study by Forrester Research, the UK’s Nationwide Building Society was judged by 49 per cent of its customers to be an “advocate that puts their interests ahead of its profits” – putting it well ahead of the 22 per cent average for other UK banks. What differentiates Nationwide from its banking rivals is its commitment to individualised and intelligent customer interactions.9

Recognising that highly individualised service was the key to reducing churn and strengthening profitability, it launched an extensive Customer Relationship Management program to more powerfully engage its 11 million customers.

With the introduction of a powerful customer interaction optimisation solution, Portrait Interaction Optimizer, the organisation not only had a comprehensive customer view, but actionable prompts to help employees make the most of each interaction. Cross-selling and customer care were both enhanced by real-time guidance. Whether customers engaged the company from a branch, the Web site or via the call centre, they experienced a seamless and individualised interaction.

The program has delivered spectacular results. With 12,000 customer-facing staff members in branches and contact centres relying on the solution, Nationwide has reduced attrition while improving up-selling and cross selling. Intelligent prompting that looks at the unique data points of a particular customer has generated positive responses of up to 40 per cent and generates a new sale 15 per cent of the time. As a result, the organisation is 220 per cent ahead of predicted sales targets.10

Impressive gains of this sort are also being repeated in Spain. Banco Popular is the third-largest banking group in Spain with more than €125 billion in assets and 15,000 employees. The bank implemented Portrait Campaign Manager to target its 6.7 million customer base. It recouped its investment in just three months based on a single campaign.

With Portrait Campaign Manager, Banco Popular is automating the customer relationship throughout the customer lifecycle. The bank is talking to its customers on their terms right from the start of the relationship with a multi-step customer on-boarding process. A prospect is tracked and traced through the various steps until he

or she becomes a customer. The process enables the individual to move from being an anonymous visitor of a web page, to requesting product information, signing a contract, depositing money on an account and eventually, trading stocks. In every step, triggers are defined so that the customer is contacted at the right time, through the right channel and with the right message. By automating intelligent dialogues with its customers, the bank maximises customer value while proactively managing risk.

rElEvancE, thE laSt frontiEr of compEtitivE advantagE

Customer relationships, like all relationships, must be nurtured and developed. Through empathy, engagement and thoughtful actions – or simply, intelligent interactions – companies can build customer relationships that endure and deliver compelling rewards. As products become increasingly commoditised, such relationships may even prove to be the last frontier of competitive advantage and differentiation.

Customer expectations will only increase as they encounter new and higher levels of service in today’s hyper-competitive markets. If companies are to meet these growing expectations, they must stand in the vanguard of the imminent relevance revolution and harness the benefits of intelligent interactions with more efficient targetting built-in.

A final thought from John Wanamaker US department store merchant:

‘Half the money I spend on advertising is wasted; the trouble is I don’t know which half.’

At least with uplift modelling you can identify your wayward 50 per cent – and use that 50 per cent extra budget to add intelligence to every customer interaction, at the point of interaction regardless of channel. That’s a better story for the chief executive officer or board. l

notES

1 Whether weighted by spend or not

2 Models are often validated by dividing a single historical dataset into two random subsets, building on one and measuring the quality of the predictions on the other. With a longitudinal validation, data from two different time periods is used. Models are built using data from the older time period and validated using data from the more recent time period. This constitutes a stronger validation because it verifies that the models identify patterns that are stable over time and really can be used to improve targeting in real-world situations.

3 When not treated.

4 Of course, everyone’s probability of being saved is limited to their probability of leaving, so the disparity can never be huge. In reality, therefore, a portion of the top left part of this schematic is empty.

5 Ideally, two control groups should be used. The first, which we call the “mailing” or “action” control group, is the normal one – a randomly chosen group of people who meet the selection criteria but who are omitted from the campaign to allow the uplift to be assessed. The second, which we call the “targeting” control group, is a randomly-selected group of people who do not meet the targeting criteria but are treated as part of the campaign. This second form of control group is critical to allowing the effectiveness of the targeting – as opposed to the treatment action – to be assessed and improved.

6 Michael Maos, Ed Thompson, Gartner, “Why Software Is Failing in CRM Initiatives,” Dec 2007.

7 Suresh Vittal, Forrester Research, “How Technology Enables Inbound Marketing,” January 8, 2007.

8 Adam Sarner, Gartner, “World-Class Building Blocks for Multichannel Campaign Management,” February 8, 2006.

9 Benjamin Ensor, Forrester Research, “The UK’s Nationwide Pits its Members First,” August 15, 2007.

10 Portrait Software White Paper, “The Profit-Minded Contact Centre: Building an ROI Case for Customer Interaction Solutions in Financial Services,” Summer 2007.

Volume 3 Number 1 2009

Published by

a Rainmaker Information company

Level 2, 151 Clarence Street, Sydney NSW 2000 Australia Telephone (02) 8234 7500 Facsimile (02) 8234 7599

www.financialstandard.com.au

— • —

The Journal of

Financial Services Technology

The Journal of Financial Services Technology ISSN 1833-9174. Copyright © 2009 Rainmaker Information Pty. Ltd. ABN 86 095 610 996. All rights reserved. This work is copyright. Apart from any use as permitted under the Copyright Act 1968 of the Commonwealth of Australia, no part of this journal may be resold, reproduced, stored in a retrieval system or transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of the publisher. Rainmaker Information Pty. Ltd. gives no warranty other than any warranty that may be implied pursuant to the Trade Practices Act 1974 that the information in this report is correct or complete. Rainmaker Information Pty. Ltd. shall not be liable for any loss or damage howsoever caused due to negligence arising from the use of this report. The views and opinions expressed in this journal are provided for information purposes only and should not be taken as constituting advice. Persons concerned with the issues raised in this journal should seek their own professional advice. No responsibility is accepted by the publishers, its employees, agents or associates for the accuracy of the information contained in this journal. The opinions expressed in this journal do not neccessarily represent the views of the publisher.