553

Volume 66 57 Number 2, 2018

https://doi.org/10.11118/actaun201866020553

TAX LITERACY

Michaela Moučková¹, Leoš Vítek¹

¹ Department of Public Finance, Faculty of Finance and Accounting, University of Economics, Prague, W. Churchill Sq. 4, 130 67 Prague 3, Czech Republic

Abstract

MOUČKOVÁ MICHAELA, VÍTEK LEOŠ. 2018. Tax Literacy. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 67(2): 553 – 559.

Presented paper focuses on measuring tax literacy among bachelor degree students at the University of Economics, Prague, along with analysis of the two factors that influence it. Based on the 150 collected questionnaires (63 % response rate), we measured tax literacy of students (personal income tax and VAT) and examined whether it depends on (i) previous passing of tax courses and (ii) previous practical experience with filing tax returns. More than half of the students were well to excellently-versed in tax matters, including those who have not completed any more advanced tax courses apart from the elementary tax course. For VAT, the results of statistical tests show that students’ knowledge depends on passing a more advanced course on consumption taxation. On the other hand, the link between experience with tax returns and results of tax literacy tests cannot be unambiguously confirmed or rejected. Within the first statistical test (personal income tax), it was established that students’ knowledge does not depend on previous filing of tax returns; the second test (value added tax) led to the opposite conclusion.

Keywords: tax literacy, financial literacy, personal income tax, value added tax

INTRODUCTION

Specificity and attractiveness of tax education relates mainly to the linkage of theoretical knowledge with subsequent experience. Tax education typically takes the form of either a bachelor degree university education of the law & taxes or accounting & taxes type, or proceeds as a vocational training. With respect to increasing attention paid to the issue of financial literacy in young (OECD 2017) but also adult populations (Hündl 2015; OECD, 2016; for Slovakia e.g. Gavurová et al., 2017), there were developed methodologies of its measurement which may be linked also with European activities, such as EU legislation in the area of consumer protection related to financial services (2014 / 92 / EU and 2014 / 17 / EU). European Commission actions in the field of financial education included e.g. Dolceta online education tool, the Expert Group on Financial Education or the Financial Services User Group. Nevertheless, all EU activities in the field of financial education and financial literacy remain only at the level of recommendations because of subsidiarity in the field of education in the EU.

When looking for financial literacy, queries in international studies standardly focus on the general overview of family finances and knowledge of their planning and management (budget, sources of household income, ability to control expenditure, indebtedness, financial products and their construction or risks, etc.) and there exists a broad international consensus on how to measure financial literacy.

Tax literacy is a specialised branch of financial literacy. There is currently no uniform methodology of tax literacy measurement and assessment. Surveys and programs for improving tax literacy are still very limited and carried out rather as a marginal topic of financial literacy surveys.

the discussion and analysis of psychological aspects of taxation and tax evasion, including the context of motivation and demotivation to pay taxes.

Kamaluddin and Madi (2005), Madi et al. (2010) and Latiff et al. (2005) measured tax literacy among taxpayers in Malaysia. Bhushan and Medury (2013) focus on measuring tax literacy of employees in India and try to quantify the impact of various socio-economic variables on tax literacy. They found that the level of tax literacy varies significantly among respondents and it is affected by their gender, age, education, income, nature of employment and place of work.

Blechová and Sobotovičová (2013) were the first to investigate tax literacy among university students in the Czech Republic and surveyed the difference between full-time and combined study mode students. Cvrlje (2015) deals with a literature review on tax literacy and its connection with tax evasions in the Croatian framework. Nichita (2015) briefly and generally discusses potentials of tax literacy impact on improving tax compliance.

OECD deals with the issue of tax literacy rather marginally, e.g. in the OECD / FIIAPP (2015) publication it devotes also to several more advanced countries (Estonia, Turkey, Korea).

The presented paper aims to provide an overview of tax literacy research, obtain primary data on tax literacy of students of the University of Economics, Prague and analyse the impact of tax education and tax practice on the results of tax literacy testing. The paper is concluded by a discussion and conclusions.

MATERIALS AND METHODS

Data for the analysis were acquired using a questionnaire survey that was carried out among all students of the study field Taxation and Tax Policy in the bachelor degree program. Two very similar questionnaires were circulated; the first one focused on personal income tax and the second one dealt with value added tax. Both questionnaires included analytical questions focused on identification of the respondents, their characteristics and questions of merit focused on the examined subject (tax literacy). Most questions were closed ones, using both alternative questions (choosing between two options) and selective questions (choosing from more than two options). The questionnaire focusing on personal income tax was distributed to students of the first and third year, the second questionnaire

which focused on value added tax was sent to all students of the bachelor study.

The questions were chosen so as to examine both the knowledge that students acquired during their study, but also the students’ ability to understand the tax-related text (either study text or legal excerpts). Most of the questions were focused on practical knowledge and skills: there was given an example of a situation and students picked the right answer so as to see if they could apply their theoretical knowledge to solving practical tasks. The text questions took within the PISA classification in terms of reading literacy the format of non-continuous texts and the text types are descriptions or instructions.

OECD (TUM, 2017) defines reading literacy as “understanding, using, and reflecting on written texts in order to achieve one’s goals, to develop one’s knowledge and potential, and to participate in society”. This methodology analyse how children / adolescents are able to understand and integrate texts. The methodology developed by OECD for PISA measures (i) retrieving texts, (ii) interpreting and integrating texts and (iii) reflecting and evaluating texts. Analysed texts could be classified by (i) type of medium, (ii) text format, (iii) text type or (iv) for electronic texts context.

Following table lists the most important quantitative characteristics of the questionnaires.

For evaluation of the acquired data were adopted methods of descriptive statistics and hypothesis testing (Wooldridge 2016, Hindls et al., 2007) in order to determine, on which individual variable is the students’ knowledge dependent.

From the descriptive statistics we choose mainly characteristics of the degree of level, namely the mode and arithmetic mean, respectively, weighted arithmetic mean (1):

1 1 k i i i k i i x n x n = = =

∑

∑

(1)Next, we will focus on degrees of variability, especially to see if the statistical set is homogeneous or not. For this we make use of variance (2)

(

)

22 1 n i i x x x s n = −

=

∑

(2)I: Quantitative characteristics of questionnaires

PIT VAT

Number of addressed students 117 125

Number of returned questionnaires 67 83

Number of questions identifying the respondent 6 5

Number of questions verifying the knowledge 14 10

and in relative terms also the variation coefficient (3)

x x s

V x

= (3)

In order to reveal on what depends the knowledge of students, we will test several hypotheses, namely: • H01: Knowledge of students does not depend on

passing the course Taxation of Consumption, respectively, Taxation of Income.

• H02: Knowledge of students does not depend on

previous experience with filing of tax returns. To test these hypotheses, we chose the χ2– test

of independence in the contingency table. We compare actual frequencies with the theoretical ones (n′ij) that are expected in the case of independence.

These are obtained using the formula (4) ´

. .

i ij n n j

n n

= ′ (4)

As the test criterion, we choose the quantity (5):

(

,)

2, 1 1

R S ij ij

ij i j

n n

G

n

= =

−

=

∑∑

(5)which has, in the case of independence and assuming a sufficiently large number of observations, approximately χ2 – distribution with

v = (r – 1) (s — 1) degrees of freedom.

We will test all hypotheses at 5 % level of significance.

RESULTS

Data acquired from the questionnaires make it possible to assess the structure of respondents according to their tax knowledge and furthermore whether the respondents have already completed any tax return or not. Students’ tax literacy is assessed according to the scale listed in the table below. The respondent who answered at least 71 % of the questions correctly has got an excellent knowledge. On the contrary, the respondent who answered just 40 % and fewer questions correctly has got insufficient tax knowledge.

Descriptive statistics

In the following table, we see how many students fall into each category: most students are in the second category (good knowledge), which corresponds to 41 % to 70 % of the correct answers.

Experience with filling tax returns for the respondents is shown in the following table. These data are further used for testing the H02

hypothesis when we assume that respondents who have previous experience with filing tax returns will have better tax literacy compared to other respondents.

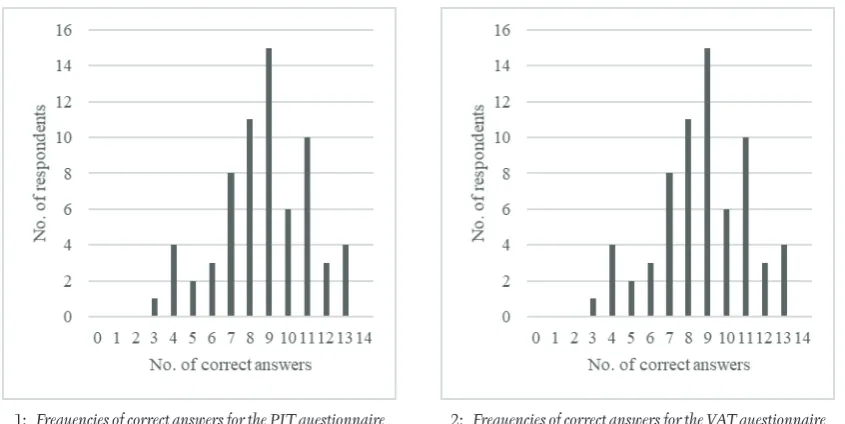

Frequencies of correct answers for both questionnaires are shown in Fig. 1 and Fig. 2. For personal income tax, respondents answered only just 9 questions correctly (arithmetic mean 8.7). Absolute rate of variability shows variance (5.5), relative variation coefficient (26.95 %). The results point at heterogeneity of the dataset. In a similar way, we may proceed with the value added tax (Fig 2). The mode of correct answers for VAT is 7, arithmetic

II: Tax knowledge – methodology

Percentage of correct answers Tax knowledge

0 % – 40 % Insufficient

41 % – 70 % Good

71 % – 100 % Excellent

Source: own processing.

III: Structure of respondents according to knowledge

PIT VAT

absolutely relatively absolutely relatively

Excellent 23 0.343 27 0.325

Good 37 0.552 46 0.554

Insufficient 7 0.104 10 0.120

Source: own processing.

IV: Structure of respondents according to experience with tax returns

PIT PIT VAT VAT

absolutely relatively absolutely relatively

Yes 29 0.433 41 0.494

No 38 0.567 42 0.506

average 6.7. Variance 2.5 and variation coefficient (23.76 %) point towards greater homogeneity than was the case of personal income tax; nevertheless, the dataset is also heterogeneous.

Summary results of the descriptive statistics are shown in the following tab. V.

Testing Hypotheses

First, we will look at exploring the question whether students’ tax literacy does or does not depend on prior passing specialised tax courses. These are Income Taxation or Consumption Taxation courses, teaching this tax area at already a relatively detailed level.

• H01: Knowledge of students does not depend on

passing specialised courses

We assume that at the time of testing, all students have already completed the entry-level course on taxation (Taxation in the Czech Republic), i.e. each student in the group of respondents has already acquired basic knowledge in the area of taxation. This has the effect of balancing knowledge among students coming from various secondary schools (some secondary schools do not teach specialised courses focused on taxation – typically grammar schools, in contrast to secondary business schools or business academies, where accounting education combined with the basics of taxation is taking

place). By testing H01, we learn how teaching

has contributed to the literacy of students and therefore we may identify the so-called added value of the education process – for the concept of value-added modelling, value-added analysis or value-added assessment, see e.g. Harris (2011).

Results of both questionnaires were analysed using contingency tables of the observed frequencies and theoretical (expected) frequencies. The values were subsequently compared and the test criterion G was calculated. One of the assumptions for using the Chi-square test of good fit is that none of the values in the contingency table should be 0 (Hindls et al., 2007). In the case of personal income tax, the assumption is violated even twice, so from these data we cannot verify the hypothesis.

For the questionnaire that tested knowledge of VAT, the test can be performed because the contingency table does not contain zero values. The test criterion G = 14.985, the critical value for the given significance level and the given degree of freedom is

χ = 5.991. Given that the test criterion is greater than the critical value, we reject the H01 hypothesis and

therefore we may accept the alternative hypothesis, i.e. knowledge of the students depends on passing the course Consumption Taxation.

• H02: Knowledge of students does not depend on

experience with tax return filing

1: Frequencies of correct answers for the PIT questionnaire 2: Frequencies of correct answers for the VAT questionnaire

Source: own processing, data Moučková (2015), Kracík (2015).

V: Results of descriptive statistics

PIT VAT

Number of questions 14 Number of questions 10

Mode 9 Mode 7

Arithmetic average 8.7 Arithmetic average 6.7

Variance 5.5 Variance 2.5

Standard deviation 2.3 Standard deviation 1.6

Variation coefficient 26.95 % Variation coefficient 23.76 %

By testing this hypothesis we will try to find out whether knowledge of students is influenced by their practice. Therefore, we will follow whether students who already have acquired some experience with filing tax returns have better tax literacy or not.

The analysis is again based on contingent tables of actual and theoretical frequencies. For Personal Income Tax, the test criterion is G = 6.886, the critical value for the given significance level and the given degree of freedom χ = 5.991. The test criterion is larger than the critical value and therefore at the given level of significance we reject the H02 hypothesis and establish that there exists

a dependency and tax knowledge of respondents in the domain of PIT depends on whether they have ever filled out some tax returns.

We will choose the same procedure also for VAT, where the test criterion G = 1.921, the critical value for the given significance level and the given degree of freedom χ = 5.991. The test criterion is less than the critical value, therefore at the given level of significance we do not reject the H02 hypothesis and

we assert that students’ knowledge of VAT does not depend on whether or not they have ever filled out a tax return.

Based on the above-mentioned results on tax literacy dependence on previous tax experience it can be stated that a summary conclusion cannot be clearly established. In the first test it was found that knowledge of students does not depend on filing tax returns, the second test points towards the opposite direction.

DISCUSSION

Students did not respond much to the first round of data collection and so it was necessary to repeat the data collection in multiple rounds using school mail and social networks. Gradually, all students in the study field Taxation and Tax Policy of the bachelor program were approached. In total, students had to be approached five times and then the overall rate of return on the questionnaires was 62 %, which is a very solid result. Surprisingly, there was achieved a lower response rate on the personal income tax questionnaire (57 %), although it may be expected that students have more experience with this tax (they encounter it in practice more frequently when completing tax returns of their own or for their close relatives) and overall it is for students “more attractive” and more interesting. The rate of return on VAT questionnaires was 66 %.

Apart from the theoretical knowledge of students, the questionnaires should also determine students’ ability to apply their knowledge to practical examples. Several questions also tested whether respondents understand the text, there were used excerpts either directly from the law or from textbooks relevant to the subject. Questions formulated in such a way are also important due to the fact that within literacy surveys there is often explored

the ability to comprehend the presented text (reading literacy) – see, for example, Artelt et al. (2001), Kreiner (2014) or OECD (2017). However, understanding the text in adopted questions is at the borderline between tax and reading literacy and complicates assessment of the results because a wrong answer may be caused either by misunderstanding of the text or by unawareness of tax issues.

When assessing results of this study, it should be also taken into account that the research was conducted only among students and the group of students was not identical, but there were two different groups (it was not possible to ensure that the same students would answer both questionnaires for personal income tax and VAT). For a more quality analysis of the educational process’s added value, it would be appropriate to observe one group of students during the entire time of their study (retrospective or prospective longitudinal studies). The results obtained using longitudinal studies may in turn serve as a feedback tool for management of educational institutions and their curricula.

For further research in the field of literacy dependence on practical experience (in this case filling out tax returns in the past), it will be necessary to better specify in the questionnaire what kind of tax return was completed. If we suppose the respondents filled most frequently e.g. personal income tax returns, then it would be logical that there is dependence between PIT knowledge and filling of the tax return and, contrariwise, that there is no impact on the knowledge of VAT. However, this could not be verified using the given data structure.

A similar test was conducted for the Czech Republic by Blechová and Sobotovičová (2013), who examined the tax knowledge of students in postgraduate magistrate studies in all forms and ascertained whether students’ knowledge depended on the form of study. Their research has confirmed the dependence, which the authors explained by the fact that the students of combined studies already work. This explanation, however, challenges our research because most students who completed tax returns (see hypothesis H02) are working or actively

doing business, but still no dependence has been proven.

CONCLUSIONS

The aim of this paper was to assess students’ tax literacy, namely their knowledge of personal income tax and VAT, and to determine whether it depends on (i) the previous passing of tax courses and (ii) previous experience in filling out tax returns in practice. The relatively high rate of survey’s return (62 %) and a set of respondents amounting to 242 members (university graduate students of the B.Sc. degree in Taxation and Tax Policy, University of Economics, Prague) make it possible to conclude that more than half of the students are well to excellently-versed in tax matters, including those who have not completed more advanced taxation courses apart from the elementary course (junior students). Undertaking taught courses which focus on a deeper realm of the given domain of taxation (income or consumption tax courses) broadens the overall knowledge of respondents. While assessment of hypotheses for personal income tax was not possible due to the data constraint reasons, there nevertheless holds that students who have completed the advanced course did not get into a group with insufficient knowledge. For VAT, the test results show that students’ knowledge depends on passing a more advanced course on consumer taxation.

The second part of the analysis has shown that the link between experience with tax returns and results of tax literacy tests cannot be unambiguously confirmed or rejected. The first test (personal income tax) found that knowledge of students did not depend on the previous filing of tax returns; in the case of the second test (value added tax), the opposite was found.

To further refine the above presented results, there come forward several steps with respect to further research: (i) resolve more clearly the borderline nature of text questions (reading vs. tax literacy), (ii) analyse the data based on retrospective or prospective longitudinal studies, (iii) specify in more detail what previous experience with tax returns do the respondents have (type of tax). For further research, it would also be interesting to link broader analyses of financial literacy with knowledge within the domain of taxation. It would be interesting to compare results achieved by the general public with those attained by students of specialised universities and also to compare the results among different universities. Based on the results it would be in turn possible to strengthened public tax literacy by, for example, organising seminars and information campaigns or via personalised information support of taxpayers, which could contribute to an increase in voluntary compliance.

Acknowledgement

The article has been developed as one of the outcomes of the IGA project no. VŠE IGS F1 / 01 / 2016 “Public Finance in the CR and EU“ and institutional support IP100040.

REFERENCES

ARTELT, C., SCHIEFELE, U. and SCHNEIDER, W. 2001. Predictors of reading literacy. European Journal of Psychology of Education, 16(3): 363–383.

BHUSHAN, P. and MEDURY, Y. 2013. Determining Tax Literacy of Salaried Individuals – An Empirical Analysis. IOSR Journal of Business and Management, 10(6): 76–80.

BLECHOVÁ, B. and SOBOTOVIČOVÁ Š. 2013. Tax Education as a Part of Financial Literacy [in Czech: Daňová vzdělanost jako součást finanční gramotnosti]. Trendy ekonomiky a managementu, 7(14): 17–24.

CVRLJE, D. 2015. Tax Literacy as an Instrument of Combating and Overcoming Tax System Complexity, Low Tax Morale and Tax Non-compliance. The Macrotheme Review, 4(3): 156–167.

EC. 2014. Directive 2014/92/EU of the European Parliament and of the Council of 23 July 2014 on the comparability of fees related to payment accounts, payment account switching and access to payment accounts with basic features Text with EEA relevance. Brussles: European Comission. Available at: http://eur-lex.europa.eu/eli/dir/2014/92/oj [Accessed: 2018, January 10].

EC. 2014a. Directive 2014/17/EU of the European Parliament and of the Council of 4 February 2014 on credit agreements for consumers relating to residential immovable property and amending Directives 2008/48/EC and 2013/36/EU and Regulation (EU) No 1093/2010 Text with EEA relevance. Brussles: European Comission. Available at: http://eur-lex.europa.eu/legal-content/en/ALL/?uri=CELEX%3A32014L0017 [Accessed: 2018, January 10].

ERIKSEN, K. and FALLAN, L. 1996. Tax Knowledge and Attitudes towards Taxation: A Report on a Quasi Experiment, Journal of Economic Psychology, 17(3): 387–402.

FALLAN, L. 1999. Gender, exposure to tax knowledge, and attitudes towards taxation; an experimental approach, Journal of Business Ethics, 18(2): 173–184.

GAVUROVÁ, B., HUCULOVÁ, E. and KUBÁK, M. 2017. Sufficiency of Financial Literacy: A Case Study of University Students in Slovakia. In: KAPLÁNOVÁ, P. (Ed.). Contemporary Issues of Societal Development. Novo Mesto: Faculty of Organization Studies, pp. 48–70.

HARRIS, D. 2011. Value-Added Measures in Education. Cambridge, MA: Harvard Education Press.

HÜNDL, V. 2015. Results of Measuring the Level of Financial Literacy of the Adult Population of the Czech Republic [in Czech: Výsledky měření úrovně finanční gramotnosti dospělé populace České republiky 2015]. Praha: Ppm Factum Research.

KAMALUDDIN, A. and MADI, N. 2005. Tax Literacy and Tax Awareness of Salaried Individuals in Sabah and Sarawak, Journal of Financial Reporting and Accounting, 3(1): 71–89.

KIRCHLER, E. 2007. The Economic Psychology of Tax Behaviour. Oxford: Oxford University Press.

KRACÍK, J. 2015. Assessment of Tax Knowledge in Selected Groups [in Czech: Hodnocení znalostí daní u vybraných skupin]. Prague: The University of Economics in Prague.

KREINER, S. and BANG, CH. K. 2014. Analyses of Model Fit and Robustness. A New Look at the PISA Scaling Model Underlying Ranking of Countries According to Reading Literacy. Psychometrika, 79(2): 210–231. LATIFF A. R. A., NOORDIN, B. A. A., OMAR, M. R. and HARJITO, D. A. 2005. Tax Literacy Rate among

Taxpayers: Evidence from Malaysia. Jurnal Akuntansi and Auditing Indonesia, 9(1): 1–10.

MADI, N., KAMALUDDIN, A., JANGGU, T., IBRAHIM, M. B. A. and SAMAH, A. B. A. 2010. Tax Literacy among Employees: Sabah and Sarawak’s Perspective. International Journal of Economics and Finance,

2(1): 218–223.

MOUČKOVÁ, M. 2015. Tax Literacy [in Czech: Daňová gramotnost]. Prague: The University of Economics in Prague.

NICHITA, R. A. 2015. Knowledge is Power. Improving Tax Compliance by Means of Boosting Tax Literacy.

The Journal of the Faculty of Economics – Economic, 1(1): 770–774.

OECD. 2016.OECD/INFE International Survey of Adult Financial Literacy Competencies. Paris: OECD. OECD. 2017. PISA 2015 Results (Volume IV): Students’ Financial Literacy. Paris: OECD Publishing.

OECD/FIIAPP. 2015. Building Tax Culture, Compliance and Citizenship: A Global Source Book on Taxpayer Education. Paris: OECD Publishing.

ŘEZANKOVÁ, H. 2007. Analysis of Data from Questionnaire Surveys [in Czech: Analýza dat z dotazníkových

šetření]. Praha: Professional Publishing.

TUM. 2017. German PISA National Center – Domains: Reading Literacy. TUM. Munich: Technical University of Munich - German PISA National Center. Available at: https://www.pisa.tum.de/en/domains/reading-literacy [Accessed: 2018, January 10].

WOOLDRIDGE, J. M. 2016. Introductory econometrics: A modern approach. Boston: Cengage Learning.