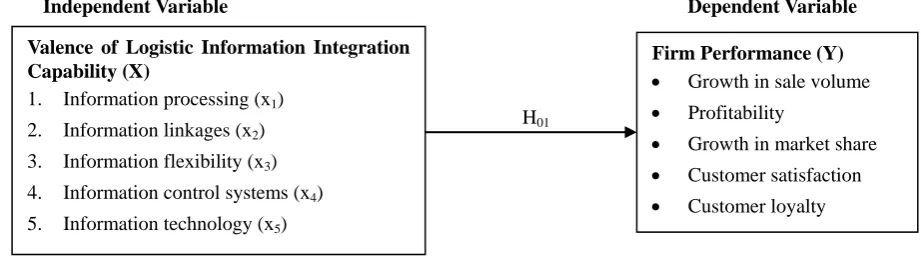

Influence of Valence of Logistic Information Integration Capability on Firm Performance in Kenya

Full text

Figure

Related documents

Twenty-five percent of our respondents listed unilateral hearing loss as an indication for BAHA im- plantation, and only 17% routinely offered this treatment to children with

Based on the growing population of language minority students who are born in the United States and systemically left behind with seemingly insurmountable

3 It expanded the scope of matters for which the operator was entirely liable (as opposed to those matters for which the non-operators and the operator share liabilitypro

Archives of 1 MSc, Department of Occupational Health Engineering, Faculty of Public Health, Kerman University of Medical Sciences, Kerman, Iran• 2 PhD, Department

This study is a systematic review and meta- analysis that was performed in clinical trial about the effect of vitamin D copmpared with placebo on CD4 count of

The cholesterol lowering drugs include statins, fibrates, bile acid sequestrants, inhibitors of intestinal sterol absorption, nicotinic acid derivatives and others

Conclusions In this paper a new method for numerical solution of ordi- nary differential equations based on pseudo differential operators and Haar wavelets is proposed.. Its

We describe the design and analysis plan for a pragmatic trial being conducted in Zimbabwe on a combination HIV prevention and treatment intervention for FSW, in which