CHAPTER 6

CHAPTER 6

Level Cash Flows: Annuities and Perpetuities

Quick Links

Quick Links

Multiple Cash Flows

Cash Flows That Grow at a Constant Rate

Future Value of Multiple Cash Flows

Solving future value problems with multiple cash flows.

1. Draw timeline to ascertain each cash flow is placed in correct time period.

2. Calculate future value of each cash flow for its time period.

3. Add up the future values.

Exhibit 6.1: Future Value of

Exhibit 6.1: Future Value of

Two Cash Flows

Exhibit 6.2: Future Value of

Exhibit 6.2: Future Value of

Three Cash Flows

Multiple Cash Flows

Multiple Cash Flows

Many business situations call for computing

present value of a series of expected future cash flows.

Determining market value of security.

Deciding whether to make capital investment

Process similar to determining future value of

multiple cash flows.

Next, calculate present value of each cash flow

using equation 5.4 from the previous chapter. Present Value of Multiple Cash Flows

Finally, add up all present values.

First, prepare timeline to identify magnitude and

timing of cash flows.

Exhibit 6.3: Present Value of

Exhibit 6.3: Present Value of

Three Cash Flows

The Value of a Gift to the

The Value of a Gift to the

University

University

Suppose that you made a gift to your

university, pledging $1,000 per year for four

years and $3,000 for the fifth year, for a

total of $7,000. After making the first three

payments, you decide to pay off the final

two payments of your pledge because your

financial situation has improved. How much

should you pay to the university if the

Buying a Used Car

Buying a Used Car

For a student—or anyone else—buying a used car

The Investment

The Investment

Decision

Decision

You are thinking of buying a business, and your investment adviser presents you with two possibilities. Both businesses are priced at $60,000, and you have only $60,000 to invest. She has provided you with the following annual and total cash flows for each business,

along with the present value of the cash flows discounted at 10 percent:

Cash flow ($ thousands)

Annuities and Perpetuities

Individual investors may make constant payments on

home or car loans, or invest fixed amount year after year saving for retirement.

Many situations exist where businesses and

individuals would face either receiving or paying constant amount for a length of period.

Level Cash Flows

Annuity: any financial contract calling for equally

spaced level cash flows over finite number of periods.

Annuities and Perpetuities

Perpetuity: contract calling for level cash flow

payments to continue forever.

Ordinary annuities: constant cash flows occurring

at end of each period.

Level Cash Flows

Present Value of an Annuity

Can calculate present value of annuity same way

present value of multiple cash flows is calculated.

Instead, simplify equation 5.4 in chapter 5 to

obtain annuity factor.

Results in equation 6.1 that can be used to

calculate the annuity’s present value.

Level Cash Flows

Exhibit 6.3: Present Value of

Exhibit 6.3: Present Value of

Three Cash Flows

(6.1) i i) (1 1 1 CF i factor) value Present (1 CF annuity an for factor value Present CF PVA n n

Level Cash Flows

Level Cash Flows

Level Cash Flows

A financial contract pays $2,000 at the end of each year for three years and the appropriate discount rate is 8% percent? What is the present value of these cash flows?

Present Value of Annuity example

n 3

1 1

Present value factor = = = 0.7938 (1+i) (1+0.08)

Finding Monthly or Yearly Payments Example

Level Cash Flows

Level Cash Flows

You have just purchased a $450,000 condominium. You were able to put $50,000 down and obtain a 30-year

fixed rate mortgage at 6.125 percent for the balance. What are your monthly payments?

n 360

Monthly interest rate = 6.125 % / 12 months = 0.51042 %

1 1

Present value factor = 0.1599589 (1+i) (1.0051042)

1 - Present value factor PV annuity factor =

i

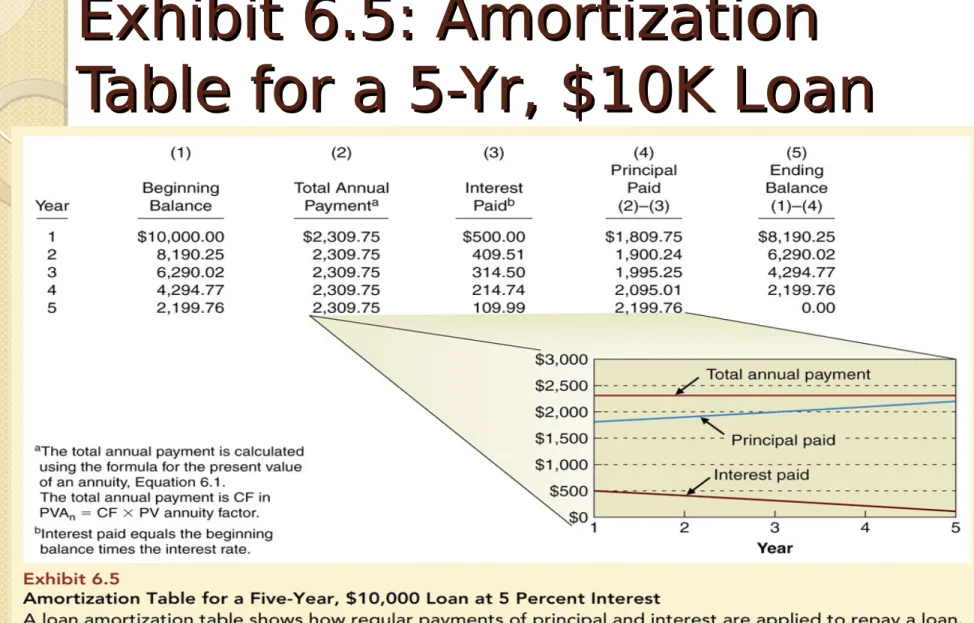

Preparing a Loan Amortization Schedule

Amortization: the way the borrowed amount

(principal) is paid down over life of loan.

Monthly loan payment is structured so each

month portion of principal is paid off; at time loan matures, it is entirely paid off.

Level Cash Flows

Exhibit 6.5: Amortization

Exhibit 6.5: Amortization

Table for a 5-Yr, $10K Loan

Amortized loan: each loan payment contains

some payment of principal and an interest payment.

Preparing a Loan Amortization Schedule

Loan amortization schedule is a table showing: loan balance at beginning and end of each

period.

payment made during that period.

Level Cash Flows

Future Value of an Annuity

Future value annuity calculations usually involve

finding what a savings or investment activity is worth at some future point.

E.g. saving periodically for vacation, car,

house, or retirement.

We can derive the future value annuity equation

from the present value annuity equation (equation 6.1). This results in equation 6.2.

Level Cash Flows

Future Value of an Annuity Equation (6.2) i 1 i) (1 CF i 1 -factor value Future CF annuity an for factor value Future CF FVA n n

Level Cash Flows

Exhibit 6.6: Future Value of

Exhibit 6.6: Future Value of

4-Yr Annuity

Level Cash Flows: Annuities

Level Cash Flows: Annuities

and Perpetuities

and Perpetuities

Finding the Interest Rate

◦

The present value of an annuity equation

can be used to find the interest rate or

discount rate for an annuity

◦

To determine the rate-of-return for an

annuity, solve the equation for

i

◦

Using a calculator is easier than a

Perpetuities

A perpetuity is constant stream of cash flows that

goes on for infinite period.

In stock markets, preferred stock issues are

considered to be perpetuities, with issuer paying a constant dividend to holders.

Equation for present value of a perpetuity can be

derived from present value of an annuity equation with n tending to infinity.

Level Cash Flows

Perpetuities CF i 0) (1 CF i i) (1 1 1 CF annuity an for factor value Present CF PVA

Level Cash Flows

Perpetuities - Example

Level Cash Flows

Level Cash Flows

Suppose you decided to endow a chair in finance. The goal of the chair is to provide the chair holder with $100,000 of additional financial support per

year forever. If the rate of interest is 8 percent, how much money will you have to give the university

foundation to provide the desired level of support?

PVA CF $100,000

= = = $1,250,000 i 0.08

Exhibit 6.7: Ordinary

Exhibit 6.7: Ordinary

Annuity versus Annuity Due

Annuity Due

Annuity transformation method shows relationship

between ordinary annuity and annuity due.

Each period’s cash flow thus earns extra period

of interest compared to ordinary annuity.

Present or future value of annuity due is

always higher than that of ordinary annuity.

Level Cash Flows

Level Cash Flows

Annuity Due Example

The value of the annuity due shown in Exhibit 6.7B is:

Level Cash Flows

Level Cash Flows

In addition to constant cash flow streams, one

may have to deal with cash flows that grow at a constant rate over time.

These cash-flow streams called growing annuities

or growing perpetuities.

Cash Flows That Grow at a

Cash Flows That Grow at a

Growing Annuity

Business may need to compute value of multiyear

product or service contracts with cash flows that increase each year at constant rate.

These are called growing annuities.

Example of growing annuity: valuation of growing

business whose cash flows increase every year at constant rate.

Cash Flows That Grow at a

Cash Flows That Grow at a

Growing Annuity

Use this equation to value the present value of

growing annuity (equation 6.5) when the growth rate is less than discount rate.

1

i

(6.5)

g

1

1

g

-i

CF

PVA

n 1 n

Cash Flows That Grow at a

Cash Flows That Grow at a

Growing Annuity Example

Cash Flows That Grow at a

Cash Flows That Grow at a

Constant Rate

Constant Rate

A coffee shop will be in business for 50-years. It produced $300,000 this year and the discount rate used by similar businesses is 15 percent. The cash flows will grow at 2.5 percent per year. What is the estimated value of the coffee shop?

1

50

CF = $300,000 (1 0.025) = $307,500

$307,500 1.025

Growing Perpetuity

When cash flow stream features constant growing

annuity forever.

Can be derived from equation 6.5 when n tends

to infinity and results in the following equation:

Cash Flows That Grow at a

Cash Flows That Grow at a

Constant Rate

Constant Rate

1

CF

PVA = (6.6) i - g

Growing Perpetuity Example

Cash Flows That Grow at a

Cash Flows That Grow at a

Constant Rate

Constant Rate

0

1 CF ×(1+g)

CF

PVA = =

Your account reports that a firm’s cash flow last year was $450,000 and the appropriate discount

rate for the club is 18 percent. You expect the firm’s cash flows to increase by 5 percent per year and

Interest rates can be quoted in financial markets

in variety of ways.

Most common quote, especially for a loan, is

annual percentage rate (APR).

APR represents simple interest accrued on loan

or investment in a single period; annualized over a year by multiplying it by appropriate number of periods in a year.

Calculating the Effective Annual Rate (EAR)

Correct way to compute annualized rate is to

reflect compounding that occurs; involves calculating effective annual rate (EAR).

Effective annual interest rate (EAR) is defined as

annual growth rate that takes compounding into account.

Calculating the Effective Annual Rate (EAR)

EAR = (1 + Quoted rate/m)

m– 1 (6.7)

m is the # of compounding periods during a year.

EAR conversion formula accounts for number of

compounding periods, thus effectively adjusts annualized interest rate for time value of money.

EAR is the true cost of borrowing and lending.

Effective Annual Rate (EAR) Example

Effective Annual Interest Rate

Effective Annual Interest Rate

Your credit card has an APR of 12 percent (1

percent per month). What is the effective annual interest rate?

EAR = (1 + 0.12/12)12 – 1

= (1.01)12 – 1

= 1.1268 – 1

Examples: Calculating

Examples: Calculating

EAR

EAR

Lender A: 10.40% compound monthly

Lender B: 10.90% compound annually

Lender C: 10.50% compound

quarterly