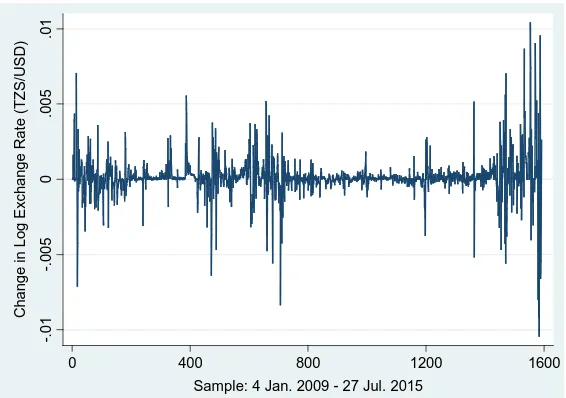

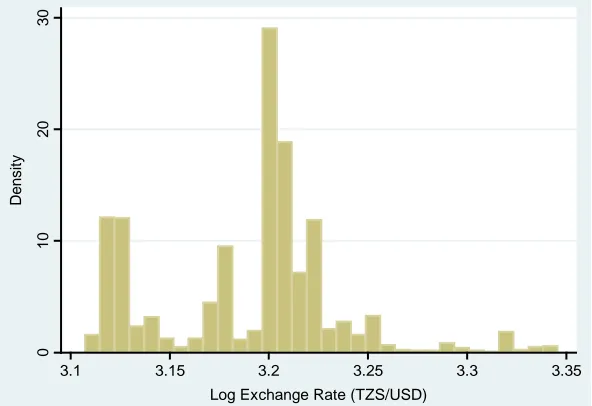

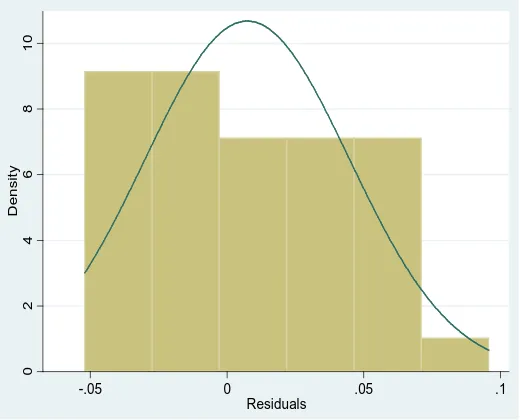

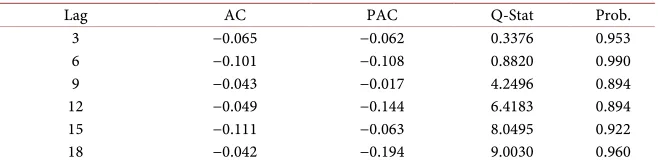

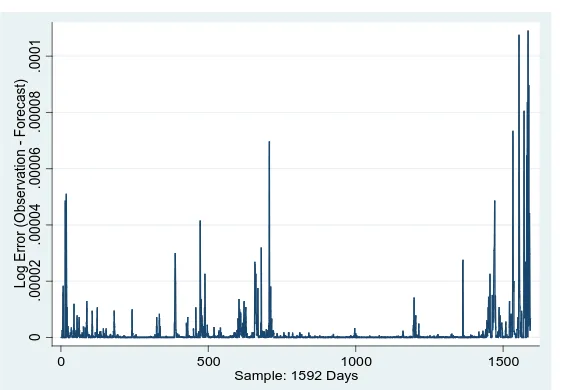

Modeling Exchange Rate Volatility: Application of the GARCH and EGARCH Models

Full text

Figure

Related documents

Introduction to Environmental Engineering (course code KH2173) is a course for civil engineering students with the main purpose is to ensure that the students understand the

• Some are easy to understand in and to find examples, others are less immediate, easy to understand in theory, but hard to come up with an example.. Dimensions

We’re really sorry.” It’s just more confirmation that the criminal justice system is not set up to facilitate safety and securi- ty for victims (much less rehabilitation for those

The argument set forth in this paper asserts that the attempts by British Officials to effectively respond to the consequences of the emergence of shell-shock as a

Essentially, both formoterol and salmeterol synergistically enhance glucocorticosteroid- dependent transcription in human airway epithelial and smooth muscle cells [60] which may

E = Endangered: Any species of plant in danger of extinction throughout all or a significant portion of its range (including, but not limited to, species listed from time

The Institute for International Monetary Affairs (IIMA) decided to newly compile a Global Market Volatility Index (IIMA-GMVI) that measures global investors’ appetite or tolerance for

The dg hyparchive Support Assistant copies all log files, configuration settings and event logs in one zip file, which then may easily be provided to the dataglobal support team as