Currency Portfolio Risk Measurement with Generalized Autoregressive Conditional Heteroscedastic Extreme Value Theory Copula Model

Full text

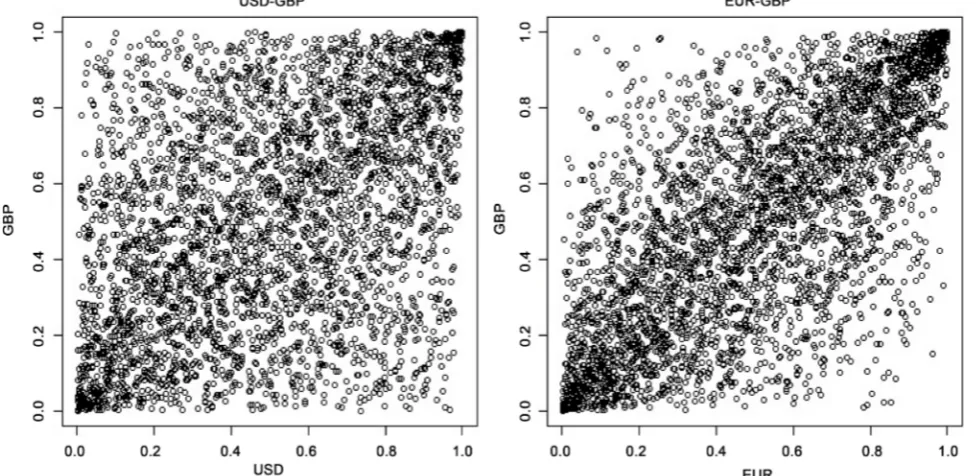

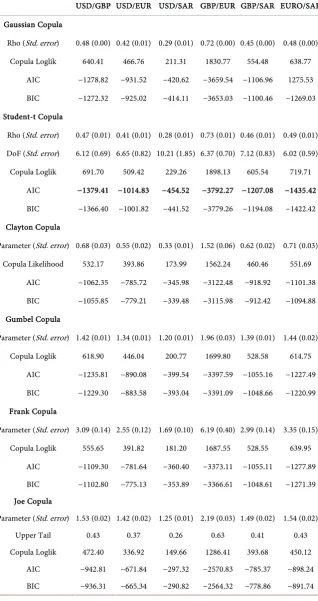

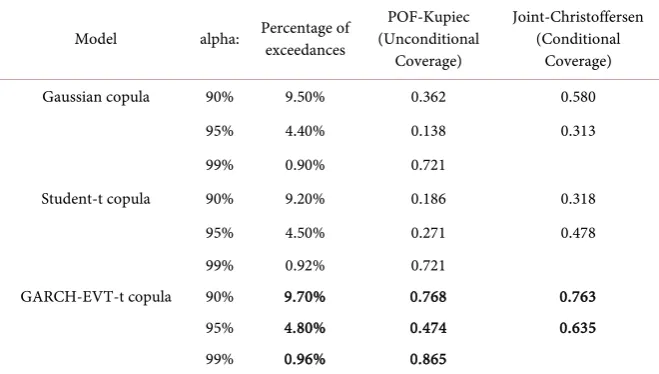

Figure

Related documents

• Personal & family goals are like the strategic planning section of your business plan.. – Mission, vision,

Once SAProuter is in place, clients have to specify a route string to connect to target servers... – All

The bias score (Figure 10b) further proves the significant improvement of the adjusted CMOPRH data, which exhibit better consistency with radar rainfall than either WRF or

Design: This study protocol describes a systematic review that intends to (i) identify methods to objectively assess clinical masticatory performance and (ii) evaluate

The original Harmony in Life Scale from Kjell and col- leagues (2016) was translated into Turkish by five ex- perts using the parallel blind technique, and then it was

Data processing speed, high real time requirement is the one big characteristic of data processing, and it is also the difficulty of this thesis, a large amount of data data greatly,

Data reduction method can include simple tabulation ,aggregation (computing descriptive statistics) or more sophisticated technique like principle component analysis. Since