Retail banking in the UK is at an inflection point. As banks face a variety of internal and external challenges, 2015 presents a real opportunity for banks to reassess their operating models, allowing them to initiate business and customer experience improvements. Banking Series 2015 presents Elixirr’s assessment of the key

challenges facing the market, and proposes viable ways to overcome them.

Banking Series 2015:

The landscape

as we see it

It is clear to all that retail banking has beenthrough turbulent times on a scale never seen before, stemming from the crisis of 2008. In the fallout, we have witnessed intense media attention - government bailout, enquiries into market mergers and acquisitions, severe scrutiny after high profile technology outages and money laundering scandals. These major events meant the regulators - locally, across Europe and the rest of world – are now paying meticulous attention to the detail of banking operations. Banks are being forced to adhere to a plethora of new local and global regulations. This, coupled with resulting underinvestment in the very operational structures and technology backbones that keep them

alive and the ever-increasing demands of their customers, means that retail banking is right in the eye of a perfect storm.

There is severe external pressure on banks from political manoeuvring, low customer confidence in the banking system as a whole, and their internal operational challenges at an individual level. This means deciding how to address these challenges is an enormous strategic crossroads for them all. But for those that are prepared, comes huge opportunity. Digital disruption and new technologies have brought new entrants to the industry. Many have been surprised by the alternative service providers who are now nibbling away at what was traditional core banking territory. This makes it more important than ever to put addressing key internal challenges across product, operating model costs, technology and people, right to the top of every CEOs agenda. This disruption is threatening the dominant position of the major banks, and now is the time for them to act to ensure their survival.

banks need to decide what they want their core capabilities to be. Are they core banking engines, or front to back banks?

Who to play with and what business to be in: partnering with some of the new entrants could be a way forward. For example, Santander has started a relationship with Funding Circle, differentiating them and crucially, allowing them to maintain a primary banking relationship with their customers (while they earn basis points on the referral). However, they still retain Know Your Customer (KYC) and Anti Money Laundering (AML) responsibilities - one of the more costly customer processes.

Which products to sell: do existing retail banking products really suit today’s customer? There has been little to no change in the

products available since the launch of the offset mortgage in the late 90’s. Today, the pace of change is more rapid than at any other time in history. Consider this: it only took Apple three years to launch Apple Pay after Google gave us the first digital wallet – just one tenth of the time between the charge card (1920’s) and the credit card (1950’s). With people living longer, living different lifestyles and the evolution of pensions giving customers more varied options, now is the time for retail banks to seriously rethink their product sets.

Which customers to attract: which set of customers drive the most income for banks and how much do they cost to serve? Are there other market segments being underserved and could they help incumbent banks restore their profitability? With recent changes to pension legislation, we can already see one market segment that is clearly underserved: the post

Key internal and external challenges:

presenting opportunities

STRATEGY

STRATEGY

STRATEGY

STRATEGY

STRATEGY

t r u s t

regula

t i on

d i g i t a l

d i s r u p t i o n

n e w entra

n ts

c u s t omer exper

i e n c

e

COST OF OPERATING MODEL

PEOPLE

PRODUCT DEVELOPMENT

TECHNOLOGY

c ustomer behaviour

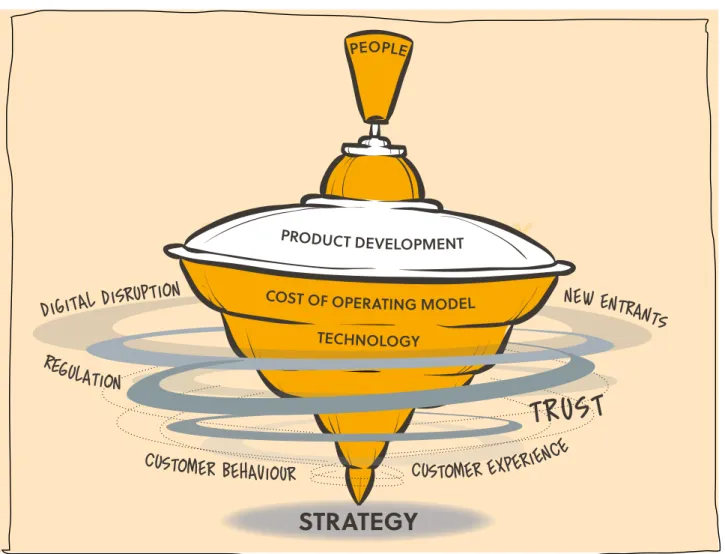

FIGURE 1: Key internal and external challenges presenting the biggest opportunities for the retail banking industry. Digital disruption, new entrants, regulation, customer experience, behaviour and trust are putting retail banks into a spin, as they struggle to transform their business models and generate enough momentum to keep upright. Banks must address their overall strategy, technology, operating models (including ensuring that they have the right people who are appropriately skills), and develop new products. If they don’t, they will fall over, only able to watch from the ground as new, non-traditional competitors become the new incumbents dominating the retail banking industry.

The crisis of 2008 has given rise to significant and ever-increasing external pressure on banks. Global and local regulation, the shattering of customer trust, political manoeuvring, the rise of digital channels and payments, changing customer behaviours and expectations set by other industries are driving the expectation for change. These factors are also opening the doors for new and innovative players to enter the market, threatening the market share that the incumbents have enjoyed for so long.

DIGITAL DISRUPTION

Banking service is not about bricks anymore, it’s about clicks. Customers now hold the power, having become increasingly empowered by digital progress, and customer-centricity now holds the key to profitability. However, simply digitising existing processes does not go far enough. Banks now need to redesign their operating models for the digital age, optimising them for the online world as opposed to the branch-based world. So what should the proposition of the big retail banks be in this rapidly changing landscape? How do they apply and operationalise the success stories of companies in other markets to the banking industry? How can banks engage better with up-and-coming, or indeed, already established FinTech companies to build a truly future-proof business model? And can they learn lessons from these smaller, more agile companies to create a sustainable innovation engine inside their own businesses?

NEW ENTRANTS

From full service digital banks and new payment providers, through to P2P and B2B lenders, there are new entrants attacking what was once solely the domain of the incumbent banks. These new

External factors:

market pressures

do not have the weight of legacy systems holding them back

are really meeting customer needs – they are targeted, omni-channel and customer-centric The new entrants are starting slowly, winning meaningful business from the traditional banks in profitable and strategically important areas. Right now they are relatively small, but they are growing rapidly and cannot be underestimated. Many of them are a very real threat - they have the potential to expand overnight, or, could seek strategic alliances, generating a much bigger player in the market. Analyst and consumer confidence in bank alternatives is increasing – you just have to look at Lending Club’s IPO as an indication of this. Traditional banks are in danger. To survive, they need to get their competitive advantage back. Is there a way traditional banks can leverage advancements and changing customer service models from other industries? And how can new entrants build operating models designed for the future to further accelerate progress in the industry?

CUSTOMER BEHAVIOUR & EXPERIENCE

The relationship between banks and their customers has changed forever – the power has irreversibly shifted. Customers are much more savvy, have a heightened ability for self-service and they are fickle - they have quickly lost trust in the institutions they have banked with for years. They have embraced the new technology and channels given to them by brands in other industries and wholeheartedly embraced social networking. They are always connected and expect to be able to access all their information in real-time anytime, anywhere. And they expect this from their banks as a basic hygiene factor. So it is no surprise that

External factors:

market pressures

Outside of their banking relationships, customers are well informed. They can easily find, compare and view information so they can get the best deal, and feel more in control. Furthermore, they are getting used to having their needs anticipated across product offerings, being presented with other products they may be interested in, and are used to engaging quickly and directly with retailers and service providers across the channel that is convenient for them.

Retailers like Amazon have set the digital capability bar high, and the majority of others have quickly followed suit just to keep up. Customer journeys are now acutely personalised when shopping online. Those same customers are left wondering why these positive and seamless experiences are not being replicated by their banks. Other industries are clearly signposting what retail banking propositions will look like in the future and are an indisputable argument that banks need to focus on building the seamless experience their customers want.

It’s not all bad news for the big retail banks. They have something incredibly valuable: an unrivalled amount of customer data. This means they are very well placed to make the most of what customers are demanding, as they can access the preferences of their customers to drive innovation and new propositions.

So how can the retail banking industry best serve the financial needs of customers in the future? There is a clear need for a new approach to retain competitive advantage. If Google or Amazon were to build a bank, what would it look like? And what happens if they do?

REGULATION

There is a plethora of UK, European and global regulation that banks are expected to implement processes to meet, and proactively demonstrate their adherence to. This regulation is designed to make banking operating models more secure, and to protect their customers. However, there are many different instigators of this regulation, which constrains innovation in the market. In addition, the numerous implementation timelines enforced by the regulators can seriously disrupt other change activities that banks may wish to prioritise to drive their own business objectives, meaning the end customer sometimes misses out.

The impact from regulatory breaches is at an all-time high - from the mis-selling of PPI and Libor rate-fixing through to money laundering and offshore account issues. These breaches have resulted in substantial multi-year financial impact and reputational damage to the banks involved. Regulators currently have a number of key focus areas that are driving changes in approach and scrutiny. These include increasing competition in the market, transparency around fees and charges and the resilience of core banking technology systems. Clarity of business strategy and choosing where to play, alongside navigating the regulatory implications and requirements of the business models required to achieve that strategy is key. Only by clearly understanding these things can banks effectively invest in developing the right capabilities and in using their organisational resources effectively.

“If Google or Amazon were to build

a bank, what would it look like? And

what happens if they do?”

Internal factors:

getting your house in order

Investment in internally driven change has suffered greatly since the crisis, with external pressures from the likes of the regulator winning priority. For years, there has been huge underinvestment in the underlying technology backbone and infrastructure of banks. Returning value to shareholders, adhering to regulatory change and creating a digital front end have been prioritised over remediation of the core. With this in mind, how can banks secure investment to optimise their business model, so that they satisfy the demands of today’s ‘anytime, anywhere’ customer?

PRODUCT DEVELOPMENT: BANKING PRODUCTS DESIGNED FOR TODAY’S WORLD

Traditional retail banking hasn’t seen much in the way of innovation since its inception, and has had a fairly narrow view to date. We have seen only incremental changes, with bolt-ons added to products that already exist. We believe that there are three key issues with the common retail banking product set as it stands today:

1. Where is the innovation? Offset mortgages were the last notable development in the

retail banking product set, in the 90’s. Product development in retail banking has been woefully poor to date.

2. Products fit for today’s world? Are retail banking products actually fit for today’s world? Or are we trying to shoehorn products designed to work inside a physical branch-based environment, into an online and real-time world?

3. Products fit for today’s life stages? We are fast becoming a cashless society and we are living longer, so our needs are changing. Do current retail banking products actually reflect what we need?

Product innovation in banking is far behind other industries, and it needs to catch up. New market entrants are already winning customers by offering better service and product through multiple channels – and some are rapidly gaining market share. The big retail banks need to take action now to retain or win back these customers, maintain their market share, and even to ensure their survival.

Internal factors:

getting your house in order

OPTIMISING RETAIL BANKING BUSINESS MODELS

Decreasing margins and increasing capital

adequacy ratios are driving banks toward lower cost operating models.

Now is the time for banks to think through what their end-to-end operating model should look like, and how to best optimise that model. Should they be combining their core capabilities through strategic partnerships with other platform providers or utility services? Maybe. This would certainly remove some of the administrative burden from their operating models. Or, should banks instead become service providers for other brands or products? Could the government drive the thinking around an industrywide capability, or could other industry bodies start to build core banking utilities that all of the major banks could leverage? This would indeed reduce barriers to entry and reduce the cost to serve their customers.

TECHNOLOGY

Relentless service outages across some major UK banks have been directly affecting their customers’ ability to access their current account information and complete transactions. These outages have highlighted the difficulties banks are facing when looking to upgrade or transform their core banking platforms.

Core banking systems are at the heart of a bank’s service offering and play a critical role in their customer experience. Yet, they are typically the oldest systems in the bank - in some cases, they have been in place for over 40 years and are increasingly challenging to maintain, let alone update to serve the needs of today’s customer. Changing platforms is a huge decision, fraught with massive operational and cost implications. This makes it incredibly challenging to get backing from the Board for a new platform, never mind the complexities of implementation.

Today’s customer expects that banks will meet their needs 24/7, always responding effectively wherever they are. This has been driven by the rapid expansion of real-time channels – ATMs, contact centres, online, mobile and the service they get from other industries. Any slight IT outage that disrupts a customer’s banking service is immediately disseminated across social media, where customers are free to vent their frustrations in real-time - and publicly. What this means for the bank in question is immediate reputational damage and increased scrutiny from the regulators.

PEOPLE

As banks redefine their target customers and the products and services that they will offer to them, the most important strategic decision is what operations they will reshape and how they will reskill their workforce in support of these changes. Branch closures have hit the headlines of late, as banks move more and more of their customer interactions online, to call centres or live chat. The need for traditional branch counter services is seemingly declining, but thought must be given to when face-to-face contact is valuable for the customer and for the bank.

With new objectives in mind, banks should consider how they incentivise success, manage performance, train, and assess the skills of the current workforce. They must do this at the same time as ensuring that they attract and retain the right talent. Organisational design must also be addressed, so that management hierarchy does not undermine or threaten implementation of the required changes and so that teams can effectively operate cross-functionally throughout the organisation.

Summary:

so what next?

It is a very exciting time for the retail banking market and only time will tell exactly when the inevitable inflection point will occur. Whether you are a traditional bank or a new entrant or payment provider, no organisation in this industry can afford to be complacent.

Elixirr’s Banking 2015 Series will present practical, operational solutions to conquering today’s market challenges. We will present our view on product development, changing operating models and underpinning technology, and appropriately analysing regulation.

Retail banks cannot

afford to stand still.

They must find a way

to innovate before it’s

too late, or they will be

seeing a brand new set of

incumbent players in the

very near future.

Banking Series 2015:

future publications

PRODUCT DEVELOPMENT: BANKING PRODUCTS FIT FOR THE MODERN WORLD?

Starting with a blank sheet of paper, how would you design banking products for the modern, but regulated world?

UTILITY BANKING: OPTIMISING OPERATING MODELS THROUGH INDUSTRY PARTNERSHIPS.

Which banking capabilities are non-differentiating and don’t provide strategic advantage? Are industry-wide utilities a cost effective answer?

RESILIENCE: CORE BANKING SYSTEMS INFRASTRUCTURE – CHALLENGES AND OPPORTUNITIES.

How do you optimise resilience across core banking platforms while addressing the challenges and opportunities presented by today’s environment?

WORKFORCE 2020: DESIGNING MODERN ORGANISATIONS

How do banks create a service-led organisation committed to innovation that best serves their customers?

REGULATION: ANALYSING THE WHOLE

How do banks optimise the regulatory change required, taking implementation timelines, competing priorities and potential overlaps into account?

KY WHO? – THE COST OF GETTING IT WRONG

The potential for abuse of the banking system by criminals is shining a new regulatory interest on Know Your Customer (KYC) obligations. How do banks put the necessary controls in place to better understand their customers, but avoid a negative impact on the customer experience?

OPTIMISING AML

The key to Anti-Money Laundering (AML) is data. Banks must consolidate discrete data points in order to identify abuse within their systems. How do they define a clear AML strategy to enable them to do this?

BANK DIGITECH

The only route for a retail banks’ success is to fully embrace digital. It is not enough to digitise existing processes, banks must redesign their core processes to operate efficiently in the digital age. How can banks make this happen?

RETAIL BANK’ATION: SOLVING THE IDENTITY CRISIS IN BANKING

With a plethora of new entrants, and other providers nibbling away at the traditional core of banks, now is the time to decide what is a bank and what purpose do they serve in the market.