Small Business Administration 7(a) Loan

Guaranty Program

Robert Jay Dilger

Senior Specialist in American National Government

January 14, 2013

Congressional Research Service

7-5700 www.crs.gov R41146

Summary

The Small Business Administration (SBA) administers several programs to support small businesses, including loan guaranty programs designed to encourage lenders to provide loans to small businesses “that might not otherwise obtain financing on reasonable terms and conditions.” The SBA’s 7(a) loan guaranty program is considered the agency’s flagship loan guaranty

program. It is named from Section 7(a) of the Small Business Act of 1953 (P.L. 83-163, as amended), which authorized the SBA to provide business loans and loan guaranties to American small businesses.

In FY2012, the SBA approved 44,377 7(a) loans amounting to more than $15.1 billion. Proceeds from 7(a) loans may be used to establish a new business or to assist in the operation, acquisition, or expansion of an existing business.

Congressional interest in the 7(a) program has increased in recent years because of concerns that small businesses might be prevented from accessing sufficient capital to enable them to assist in the economic recovery. Some, including President Obama, argue that the SBA should be provided additional resources to assist small businesses in acquiring capital necessary to start, continue, or expand operations with the expectation that in so doing small businesses will create jobs. Others worry about the long-term adverse economic effects of spending programs that increase the federal deficit. They advocate business tax reduction, reform of financial credit market regulation, and federal fiscal restraint as the best means to assist small business economic growth and job creation.

This report discusses the rationale provided for the 7(a) program; the program’s borrower and lender eligibility standards and program requirements; and program statistics, including loan volume, loss rates, use of proceeds, borrower satisfaction, and borrower demographics. It examines issues raised concerning the SBA’s administration of the 7(a) program, including the oversight of 7(a) lenders and the program’s lack of outcome-based performance measures. It also examines congressional action taken during the 111th Congress to enhance small

businesses access to capital. For example, P.L. 111-5, the American Recovery and Reinvestment Act of 2009 (ARRA), provided $375 million to temporarily subsidize the 7(a) and 504/CDC loan guaranty programs’ fees and to temporarily increase the 7(a) program’s maximum loan guaranty percentage to 90%. P.L. 111-240, the Small Business Jobs Act of 2010, provided $505 million to extend the fee subsidies and 90% loan guaranty percentage through December 31, 2010;

increased the 7(a) program’s gross loan limit from $2 million to $5 million; and established an alternative size standard for the 7(a) and 504/CDC loan programs. P.L. 111-322, the Continuing Appropriations and Surface Transportation Extensions Act, 2011, authorized the fee subsidies and 90% loan guaranty percentage through March 4, 2011, or until available funding was exhausted (which occurred on January 3, 2011).

This report also examines three bills introduced during the 112th Congress that would have

changed the 7(a) program. S. 1828, a bill to increase small business lending, would have reinstated for a year following the date of its enactment ARRA’s fee subsidies and 90% loan guaranty percentage for the 7(a) program. H.R. 2936, the Small Business Administration Express Loan Extension Act of 2011, would have extended a one-year increase in the SBAExpress program’s maximum loan amount from $350,000 to $1 million, which expired on September 27, 2011, for an additional year. S. 532, the Patriot Express Authorization Act of 2011, would have

provided the Patriot Express Pilot Program statutory authorization and increased its loan guaranty percentages and maximum loan amount from $500,000 to $1 million.

Information concerning the 7(a) program’s SBAExpress, Patriot Express, Small Loan Advantage, and Community Advantage programs is also provided.

Contents

Small Business Administration Loan Guaranty Programs ... 1

Borrower Eligibility Standards and Program Requirements ... 3

Borrower Eligibility Standards ... 3

Borrower Program Requirements ... 4

Use of Proceeds ... 4

Loan Amounts ... 5

Loan Terms, Interest Rate, and Collateral ... 5

Lender Eligibility Standards and Program Requirements ... 6

Lender Eligibility Standards ... 6

Lender Program Requirements ... 7

The Application Process ... 7

SBA Guaranty and Servicing Fees ... 10

Lender Packaging, Servicing and Other Fees ... 11

Program Statistics ... 12

Loan Volume ... 12

Loss Rate and Appropriations for Subsidy Costs ... 14

Administrative Expenses ... 15

Use of Proceeds and Borrower Satisfaction ... 15

Borrower Demographics ... 16

Congressional Issues ... 16

Access to Capital ... 16

Program Administration ... 18

Oversight of 7(a) Lenders ... 18

Outcome-Oriented Performance Measures ... 20

Legislative Activity During the 111th Congress ... 21

The Obama Administration’s Proposals ... 22

Arguments for Increasing the SBA’s Maximum Loan Limits ... 22

Arguments Against Increasing the SBA’s Maximum Loan Limits ... 23

P.L. 111-5, the American Recovery and Reinvestment Act of 2009 (ARRA) ... 23

P.L. 111-240, the Small Business Jobs Act of 2010 ... 24

Legislative Activity During the 112th Congress ... 25

Concluding Observations ... 25

Tables

Table 1. 7(a) Loan Guaranty Program, Loan Volume, FY2007-FY2012 ... 13Appendixes

Appendix. 7(a) Specialized Programs... 27Contacts

Small Business Administration Loan

Guaranty Programs

The Small Business Administration (SBA) administers programs to support small businesses, including loan guaranty programs to encourage lenders to provide loans to small businesses “that might not otherwise obtain financing on reasonable terms and conditions.”1 The SBA’s 7(a) loan guaranty program is considered the agency’s flagship loan program.2 It is named from Section

7(a) of the Small Business Act of 1953 (P.L. 83-163, as amended), which authorizes the SBA to provide business loans to American small businesses.

The SBA also administers several 7(a) subprograms that offer streamlined and expedited loan procedures for particular groups of borrowers, including the SBAExpress, Patriot Express, Small Loan Advantage, and Community Advantage Pilot programs (see the Appendix for additional details). Although these subprograms have their own distinguishing eligibility requirements, terms, and benefits, they operate under the 7(a) program’s authorization.3

Proceeds from 7(a) loans may be used to establish a new business or to assist in the operation, acquisition, or expansion of an existing business. Specific uses include to acquire land (by purchase or lease); improve a site (e.g., grading, streets, parking lots, and landscaping); purchase, convert, expand, or renovate one or more existing buildings; construct one or more new

buildings; acquire (by purchase or lease) and install fixed assets; purchase inventory, supplies, and raw materials; finance working capital; and refinance certain outstanding debts.4

In FY2012, the SBA approved 44,377 7(a) loans amounting to more than $15.1 billion.5 As will

be discussed, the total number and amount of SBA 7(a) loans approved declined in FY2008 and FY2009, increased during FY2010 and FY2011, and then declined somewhat in FY2012. The SBA attributed the decreased number and amount of 7(a) loans approved in FY2008 and FY2009 to a reduction in the demand for small business loans resulting from the economic uncertainty of the recession (December 2007 - June 2009) and to tightened loan standards imposed by lenders concerned about the possibility of higher loan default rates resulting from the economic slowdown. The SBA attributed the increased number and amount of 7(a) loans

1 U.S. Small Business Administration, Fiscal Year 2010 Congressional Budget Justification, p. 30.

2 U.S. Congress, House Committee on Small Business, Subcommittee on Finance and Tax, Subcommittee Hearing on Improving the SBA’s Access to Capital Programs for Our Nation’s Small Business, 110th Cong., 2nd sess., March 5,

2008, H.Hrg. 110-76 (Washington: GPO, 2008), p. 2.

3 U.S. Small Business Administration, “Express and Pilot Programs,” at http://www.sba.gov/content/express-programs.

The SBA also administers four special purpose loan guaranty programs that address particular business needs: the Community Adjustment and Investment Program (CAIP), CAPLines Program, Employee Trusts Program, and Pollution Control Program (currently not funded). See U.S. Small Business Administration, “Special Purpose Loans Program,” at http://www.sba.gov/category/navigation-structure/loans-grants/small-business-loans/sba-loan-programs/ 7a-loan-program/special-purpose-loans-program.

4 13 C.F.R. §120.120.

5 U.S. Small Business Administration, “SBA Lending Statistics for Major Programs (as of 9/30/2012),” at

http://www.sba.gov/about-sba-info/317721. The number of 7(a) loans approved annually is typically about 10% to 20% higher than the number of loans disbursed (e.g., some borrowers decide not to accept the loan or there is a change in business ownership). The amount of 7(a) loans approved annually is typically about 10% to 15% higher than the amount disbursed.

approved in FY2010 and FY2011 to legislation that provided funding to temporarily reduce the 7(a) program’s loan fees and temporarily increase the 7(a) program’s loan guaranty percentage to 90% for all standard 7(a) loans from up to 85% of loans of $150,000 or less and up to 75% of loans exceeding $150,000.6 The fee subsidies and 90% loan guaranty percentage were in place during most of FY2010 and the first quarter of FY2011.7

Historically, one of the justifications presented for funding the SBA’s loan guaranty programs has been that small businesses can be at a disadvantage, compared with other businesses, when trying to obtain access to sufficient capital and credit.8 Congressional interest in the 7(a) loan program has increased in recent years because of concerns that small businesses might be prevented from accessing sufficient capital to enable them to assist in the economic recovery.

Some, including President Obama, argue that the SBA should be provided additional resources to assist small businesses in acquiring capital necessary to start, continue, or expand operations with the expectation that in so doing small businesses will create jobs. Others worry about the long-term adverse economic effects of spending programs that increase the federal deficit. They advocate business tax reduction, reform of financial credit market regulation, and federal fiscal restraint as the best means to assist small business economic growth and job creation.

This report discusses the rationale provided for the 7(a) program; the program’s borrower and lender eligibility standards and program requirements; and program statistics, including loan volume, loss rates, use of the proceeds, borrower satisfaction, and borrower demographics. It also

6 U.S. Small Business Administration, Press Office, “Recovery Loan Incentives Spurred Continued Rebound in SBA

Lending in FY2010,” October 4, 2010, at http://www.sba.gov/about-sba-services/7367/5527; and U.S. Small Business Administration, “Jobs Act Supported More Than $12 Billion in SBA Lending to Small Businesses in Just Three Months,” January 3, 2011, at http://www.sba.gov/content/jobs-act-supported-more-12-billion-sba-lending-small-businesses-just-three-months.

7 P.L. 111-5, the American Recovery and Reinvestment Act of 2009 (ARRA), enacted on February 17, 2009, provided

the SBA $375 million to temporarily reduce fees in the 7(a) and 504/CDC loan guaranty programs, and increase the 7(a) program’s maximum loan guaranty percentage to 90% for all standard 7(a) loans through September 30, 2010, or until available funds were exhausted. Due to the increased demand for 7(a) loans, available funding was anticipated to be exhausted in early January 2010. P.L. 111-118, the Department of Defense Appropriations Act, 2010, provided the SBA $125 million to continue the fee subsidies and 90% maximum loan guaranty percentage through February 28, 2010. P.L. 111-144, the Temporary Extension Act of 2010, provided the SBA $60 million to continue the fee subsidies and 90% maximum loan guaranty percentage through March 28, 2010. P.L. 111-150, an act to extend the Small Business Loan Guarantee Program, and for other purposes, provided the SBA authority to reprogram $40 million in previously appropriated funds to continue the fee subsidies and 90% maximum loan guaranty percentage through April 30, 2010. P.L. 111-157, the Continuing Extension Act of 2010, provided the SBA $80 million to continue the SBA’s fee subsidies and 90% maximum loan guaranty percentage through May 31, 2010. The fee subsidies and 90% loan guaranty percentage expired on May 31, 2010. P.L. 111-240, the Small Business Jobs Act of 2010, enacted on September 27, 2010, provided the SBA $505 million (plus an additional $5 million for related administrative expenses) to reinstate the fee subsidies and 90% maximum loan guaranty percentage through December 31, 2010, or until available funds were exhausted. P.L. 111-322, the Continuing Appropriations and Surface Transportation Extensions Act, 2011, authorized the SBA to use any funds remaining from the Small Business Jobs Act of 2010 to continue the fee subsidies and the 7(a) program’s 90% maximum loan guaranty percentage through March 4, 2011, or until the available funding was exhausted. The funds were exhausted on January 3, 2011.

8 U.S. Government Accountability Office, Small Business Administration: 7(a) Loan Program Needs Additional Performance Measures, GAO-08-226T, November 1, 2007, pp. 3, 9-11, at http://www.gao.gov/new.items/d08226t.pdf; and Veronique de Rugy, Why the Small Business Administration’s Loan Programs Should Be Abolished, American Enterprise Institute for Public Policy Research, AEI Working Paper #126, April 13, 2006 at http://www.aei.org/files/ 2006/04/13/20060414_wp126.pdf. Proponents of federal funding for the SBA’s loan guarantee programs also argue that small business can promote competitive markets. See, P.L. 83-163, §2(a), as amended; and 15 U.S.C. §631a.

examines issues raised concerning the SBA’s administration of the 7(a) program, including the oversight of 7(a) lenders and the program’s lack of outcome-based performance measures. It then examines congressional action taken during the 111th Congress to help small businesses

gain greater access to capital. For example, P.L. 111-5, the American Recovery and Reinvestment Act of 2009 (ARRA), provided $375 million to temporarily subsidize the 7(a) and 504/CDC loan guaranty programs’ fees and to temporarily increase the 7(a) program’s maximum loan guaranty percentage to 90%. P.L. 111-240, the Small Business Jobs Act of 2010, provided $505 million to extend the fee subsidies and 90% loan guaranty percentage through December 31, 2010;

increased the 7(a) program’s gross loan limit from $2 million to $5 million; and established an alternative size standard for the 7(a) and 504/CDC loan programs to enable more small businesses to qualify for assistance. Also, P.L. 111-322, the Continuing Appropriations and Surface

Transportation Extensions Act, 2011, authorized the SBA to continue the fee subsidies and the 7(a) program’s 90% maximum loan guaranty percentage through March 4, 2011, or until available funding was exhausted (which occurred on January 3, 2011).

This report also examines three bills introduced during the 112th Congress that would have

changed the 7(a) program. S. 1828, a bill to increase small business lending, and for other purposes, would have reinstated for a year following the date of its enactment the fee subsidies and 90% loan guaranty percentage for the 7(a) program, which were originally authorized by ARRA. H.R. 2936, the Small Business Administration Express Loan Extension Act of 2011, would have extended a one-year increase in the maximum loan amount for the SBAExpress program from $350,000 to $1 million for an additional year. That temporary increase was authorized by P.L. 111-240 and expired on September 27, 2011. S. 532, the Patriot Express Authorization Act of 2011, would have provided statutory authorization for the Patriot Express Pilot Program and increase its loan guaranty percentages and its maximum loan amount from $500,000 to $1 million.

Information concerning the SBAExpress, Patriot Express, Small Loan Advantage, and Community Advantage programs is also provided.

Borrower Eligibility Standards and Program

Requirements

Borrower Eligibility Standards

To be eligible for an SBA business loan, a small business applicant must

• be located in the United States;

• be a for-profit operating business (except for loans to eligible passive companies);

• qualify as small under the SBA’s size requirements;9

9 For further analysis, see CRS Report R40860, Small Business Size Standards: A Historical Analysis of Contemporary Issues, by Robert Jay Dilger.

• demonstrate a need for the desired credit; and

• be certified by a lender that the desired credit is unavailable to the applicant on reasonable terms and conditions from non-Federal sources without SBA assistance.10

To qualify for an SBA 7(a) loan, applicants must be creditworthy and able to reasonably assure repayment. SBA requires lenders to consider the applicant’s

• character, reputation, and credit history;

• experience and depth of management;

• strength of the business;

• past earnings, projected cash flow, and future prospects;

• ability to repay the loan with earnings from the business;

• sufficient invested equity to operate on a sound financial basis;

• potential for long-term success;

• nature and value of collateral (although inadequate collateral will not be the sole reason for denial of a loan request); and

• affiliates’ effect on the applicant’s repayment ability.11

Borrower Program Requirements

Use of Proceeds

Borrowers may use 7(a) loan proceeds to establish a new business or to assist in the operation, acquisition, or expansion of an existing business. 7(a) loan proceeds may be used to

• acquire land (by purchase or lease);

• improve a site (e.g., grading, streets, parking lots, landscaping), including up to 5% for community improvements such as curbs and sidewalks;

• purchase one or more existing buildings;

• convert, expand, or renovate one or more existing buildings;

• construct one or more new buildings;

• acquire (by purchase or lease) and install fixed assets;

• purchase inventory, supplies, and raw materials;

• finance working capital; and

10 13 C.F.R. §120.100; and 13 C.F.R. §120.101. A list of ineligible businesses, such as non-profit businesses, insurance

companies, and businesses deriving more than one-third of gross annual revenue from legal gambling activities, are contained in 13 C.F.R. §120.110.

• refinance certain outstanding debts.12

Borrowers are prohibited from using 7(a) loan proceeds to

• refinance existing debt where the lender is in a position to sustain a loss and the SBA would take over that loss through refinancing;

• effect a partial change of business ownership or a change that will not benefit the business;

• permit the reimbursement of funds owed to any owner, including any equity injection or injection of capital for the business’s continuance until the loan supported by the SBA is disbursed;

• repay delinquent state or federal withholding taxes or other funds that should be held in trust or escrow; or

• pay for a non-sound business purpose.13

Loan Amounts

As mentioned previously, P.L. 111-240 increased the 7(a) program’s maximum gross loan amount for any one 7(a) loan from $2 million to $5 million (up to $3.75 million maximum guaranty). In FY2012, the average loan amount was about $340,000.14

Loan Terms, Interest Rate, and Collateral

Loan Terms

7(a) loans are required to have the shortest appropriate term, depending upon the borrower’s ability to repay. The maximum term is 10 years, unless the loan finances or refinances real estate or equipment with a useful life exceeding 10 years. In that case, the loan term can be up to 25 years, including extensions.15

Interest Rate

Lenders are allowed to charge borrowers “a reasonable fixed interest rate” or, with the SBA’s approval, a variable interest rate.16 The SBA uses a multi-step formula to determine the maximum

allowable fixed interest rate and periodically publishes that rate and the maximum allowable variable interest rate in the Federal Register.17

12 13 C.F.R. §120.120.

13 13 C.F.R. §120.130; and U.S. Small Business Administration, “Use of 7(a) Loan Proceeds,” at http://www.sba.gov/

content/use-7a-loan-proceeds.

14 U.S. Small Business Administration, “SBA Lending Statistics for Major Programs (as of 9/30/2012),” at

http://www.sba.gov/about-sba-info/317721.

15 13 C.F.R. §120.212. A portion of a 7(a) loan used to acquire or improve real property may have a term of 25 years

plus an additional period needed to complete the construction or improvements.

16 13 C.F.R. §120.213.

17 For fixed interest rates, the SBA first calculates a fixed base rate using the 30 day London Interbank Offered Rate

The maximum allowable fixed interest rates in January 2013 for 7(a) loans with maturities less than seven years are 6.84% for loans greater than $50,000, 7.84% for loans over $25,000 but not exceeding $50,000, and 8.84% for loans of $25,000 or less. The maximum allowable fixed interest rates in January 2013 for 7(a) loans with maturities of seven years or more are 7.34% for loans greater than $50,000, 8.34% for loans over $25,000 but not exceeding $50,000, and 9.34% for loans of $25,000 or less.18

The 7(a) program’s maximum allowable variable interest rate may be pegged to the lowest prime rate (3.25% in January 2013), the 30 day LIBOR rate plus 300 basis points (3.21% in January 2013), or the SBA optional peg rate (2.25% in the second quarter of FY2013).19 The optional peg

rate is a weighted average of rates the federal government pays for loans with maturities similar to the average SBA loan.20

Collateral

The SBA requires lenders to collateralize the loan to the maximum extent possible up to the loan amount. If business assets do not fully secure the loan, the lender must take available personal assets of the principals as collateral. Loans are considered “fully secured” if the lender has taken security interests in all available assets with a combined “liquidation value” up to the loan amount.21

Lender Eligibility Standards and

Program Requirements

Lender Eligibility Standards

Lenders must have a continuing ability to evaluate, process, close, disburse, service, and liquidate small business loans; be open to the public for the making of such loans (and not be a financing

(...continued)

(LIBOR) in effect on the first business day of the month as published in a national financial newspaper published each business day, adds to that 300 basis points (3%) and the average of the 5-year and 10-year LIBOR swap rates in effect on the first business day of the month as published in a national financial newspaper published each business day. For 7(a) fixed loans with maturities of less than seven years, the SBA adds 2.25% to the fixed base rate to arrive at the maximum allowable fixed rate. For 7(a) fixed loans with maturities of seven years or longer, the SBA adds 2.75% to the fixed base rate to arrive at the maximum allowable fixed rate. Lenders may increase the maximum fixed interest rate allowed by an additional 1% if the fixed rate loan is over $25,000 but not exceeding $50,000, and by an additional 2% if the fixed rate loan is $25,000 or less. See, U.S. Small Business Administration, “Business Loan Program Maximum Allowable Fixed Rate,” 74 Federal Register 50263, 50264, September 30, 2009.

18 Colson Services Corp., “SBA Base Rates,” New York, at http://www.colsonservices.com/main/news.shtml. 19 Ibid.

20 U.S. Small Business Administration, “7(a) Loan Program: Terms and Conditions,” at

http://www.sba.gov/content/7a-terms-conditions.

21 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), pp. 188-189, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf. Liquidation value is the amount expected to be realized if the lender took possession after a loan default and sold the asset after conducting a reasonable search for a buyer and after deducting the costs of taking possession, preserving and marketing the asset, less the value of any existing liens.

subsidiary, engaged primarily in financing the operations of an affiliate); have continuing good character and reputation; and be supervised and examined by a state or federal regulatory authority, satisfactory to SBA. They must also maintain satisfactory performance, as determined by SBA through on-site review/examination assessments, historical performance measures (such as default rate, purchase rate, and loss rate), and loan volume to the extent that it affects

performance measures.22 There are currently about 3,500 active lenders providing SBA loans.23

Lender Program Requirements

The Application Process

Borrowers submit applications for a 7(a) business loan to private lenders. The lender reviews the application and decides if it merits a loan on its own or if it has some weaknesses which, in the lender’s opinion, do not meet standard, conventional underwriting guidelines and requires additional support in the form of an SBA guaranty.The SBA guaranty assures the lender that if the borrower does not repay the loan and the lender has adhered to all applicable regulations concerning the loan, the SBA will reimburse the lender for its loss, up to the percentage of the SBA’s guaranty. The small business borrowing the money remains obligated for the full amount due.24

If the lender determines that it is willing to provide the loan, but only with an SBA guaranty, it submits the application for approval through the mail, website, or e-mail to the Standard 7(a) Loan Guaranty Processing Center operating out of two locations: Citrus Heights, CA, and Hazard, KY.25 This center has responsibility for processing 7(a) loan guaranty applications for

lenders who do not have delegated authority to make 7(a) loans without the SBA’s final approval.26 The application must include the following documentation and forms:

• SBA Form 4, Application for Loan, which includes specific requirements for providing financial assistance to a small business located in a floodplain or a wetland, the use of lead-based paint, seismic safety of federal and federally assisted or regulated new building construction, coastal barrier protections, laws prohibiting discrimination on the grounds of race, color, national origin, religion, sex, marital status, disability or age, and rights under the Financial Privacy Act of 1978 (P.L. 95-630);

• SBA Form 4, Schedule A—Schedule of Collateral, or the lender may use their own form to list collateral and label it “Exhibit A”;

22 13 C.F.R. §120.410.

23 U.S. Small Business Administration, Fiscal Year 2013 Congressional Budget Justification and FY 2011 Annual Performance Report, p. 31.

24 U.S. Small Business Administration, “7(a) Loan Program: How the Program Works,” at http://archive.sba.gov/

financialassistance/borrowers/guaranteed/7alp/FINANCIAL_GLP_7A_WORK.html.

25 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), p. 225, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

26 U.S. Government Accountability Office, Small Business Administration: Opportunities Exist to Build on

Leadership’s Efforts to Improve Agency Performance and Employee Morale, GAO-08-995, September 24, 2008, p. 3, at http://www.gao.gov/new.items/d08995.pdf.

• SBA Form 912, Statement of Personal History—required of all principals, officers, directors and owners of 20% or more of the small business applicant;

• 7(a) Eligibility Questionnaire;

• Personal Financial Statement, dated within 90 days of submission to the SBA, on all owners of 20% or more (including the assets of the owner’s spouse and any minor children), and proposed guarantors. SBA Form 413 is available. However, lenders may use their own form;

• Business Financial Statements dated within 90 days of submission to the SBA, consisting of (1) year end balance sheets for the last three years, (2) year-end profit and loss statements for the last three years, (3) reconciliation of net worth, (4) interim balance sheet, (5) interim profit and loss statements, (6) affiliate and subsidiary financial statement requirements, and (7) cash flow projection— month-by-month for one year if less than three fiscal years provided and for all loans with a term of 18 months or less;

• history of the business, résumés of principals, and copy of lease, if applicable;

• detailed listing of machinery and equipment to be purchased with loan proceeds and cost quotes;

• if real estate is to be purchased with loan proceeds an appraisal, lender’s environmental questionnaire, cost breakdown, and copy of purchase agreement;

• if purchasing an existing business with loan proceeds a (1) copy of buy-sell agreement, (2) copy of business valuation, (3) pro forma balance sheet for the business being purchased as of the date of transfer, (4) copy of seller’s financial statements for the last three complete fiscal years or for the number of years in business if less than three years; (5) interim statements no older than 90 days from date of submission to SBA, and (6) if seller’s financial statements are not available the seller must provide an alternate source of verifying revenues;

• Equity Injection Form—explanation of type and source of applicant’s equity injection;

• Franchise Form—if listed on http://www.franchiseregistry.com a certification of material change or certification of no change or non-material change is required. If not listed on the registry, a copy of the Franchise Agreement and Federal Trade Commission Disclosure Report of Franchisor must be submitted;

• SBA Form 159 (7a), Fee Disclosure and Compensation Agreement, must be completed for each agent compensated by the applicant or lender and retained in lender’s loan file;

• a copy of Internal Revenue Service (IRS) Form 4506-T, Request for Copy of Tax Return—lender must identify the date IRS Form 4506-T was sent to IRS;

• for non-citizens, a copy of the U.S. Citizenship and Immigration Services (USCIS) Form G-845, Document Verification Request—prior to disbursement, lenders must verify the USCIS status of each alien who is required to submit USCIS documents to determine eligibility. The lender must document the findings in the loan file;

• SBA Form 4-I, Lender’s Application for Guaranty—must be completed in its entirety, including pro forma balance sheet and submitted with (1) explanation of use of proceeds and benefits of the loan, (2) lender’s internal credit

memorandum, (3) justification for new business, including change of ownership. For new businesses and change of ownership where historical repayment ability is not demonstrated, lender must provide a narrative addressing the business plan and cite any areas of concern and justification to overcome them, and (4)

business valuation must be supplied by lender for change of ownerships;

• SBA Form 1846, Statement Regarding Lobbying, must be signed and dated by lender; and

• SBA National 7(a) Authorization Boilerplate language on-line “wizard” must be completed.27

The SBA established the Certified Lenders Program (CLP) on February 26, 1979, initially on a six-month pilot basis.28 It is designed to provide expeditious service on 7(a) loan applications

received from lenders who have a successful SBA lending track record and a thorough

understanding of SBA policies and procedures. In recent years, CLP lenders have approved about 4.8% of the number of 7(a) loans approved each year and 7.4% of the amount of 7(a) loans approved each year.29 For loan applications of $350,000 or less, CLP lenders must submit all

forms and exhibits listed above for a standard 7(a) loan application and a draft authorization. For loan applications greater than $350,000, in addition to all of the standard 7(a) forms and exhibits, CLP lenders must submit a copy of its written credit analysis and must discuss SBA eligibility issues.30

The SBA started the Preferred Lenders Program (PLP) on March 1, 1983, initially on a pilot basis.31 It is designed to streamline the procedures necessary to provide financial assistance to

small businesses by delegating the final credit decision and most servicing and liquidation authority and responsibility to carefully selected PLP lenders.32 In recent years, PLP lenders have

27 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), pp. 217-220, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

28 U.S. Congress, Senate Select Committee on Small Business, SBA Loan Oversight, hearing on SBA loan oversight,

96th Cong., 1st sess., September 18, 1997 (Washington: GPO, 1997), p. 31; and U.S. General Accounting Office, SBA’s Pilot Programs to Improve Guaranty Loan Procedures Need Further Development, CED-81-25, February 2, 1981, p. 7, at http://www.gao.gov/assets/140/131789.pdf; and U.S. General Accounting Office, SBA’s Certified Lenders Program Falls Short of Expectations, RCED-83-99, June 7, 1983, p. 1, at http://www.gao.gov/assets/150/140126.pdf.

29 U.S. Small Business Administration, Office of Congressional and Legislative Affairs, correspondence with the

author, September 17, 2012.

30 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), p. 221, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf. CLP lenders are expected to perform a complete analysis of the application and, in return, the SBA promises a faster loan decision. The SBA still makes the final credit and eligibility decision, but by completing a credit review instead of an independently conducted analysis, the SBA attempts to arrive at its decision in three working days. See, U.S. Small Business Administration, “The Certified Lenders Program (CLP),” at http://www.sba.gov/content/ steps-participating-clp.

31 U.S. General Accounting Office, SBA’s Certified Lenders Program Falls Short of Expectations, RCED-83-99, June

7, 1983, p. 3, at http://www.gao.gov/assets/150/140126.pdf.

32 U.S. General Accounting Office, Small Business: Analysis of SBA’s Preferred Lenders Program,

approved about 22.5% of the number of 7(a) loans approved each year and about 55% of the amount of 7(a) loans approved each year.33 PLP lenders must complete and retain in the lender’s file all forms and exhibits listed above for the Standard 7(a) application. They must submit the following forms to the SBA for review: (1) a copy of page 1 of SBA Form 4, Application for Business Loan, (2) a copy of page 1 of SBA Form 4-I, Lender’s Application for Guaranty or Participation (signed by two authorized officials of the lender), (3) a copy of Form 1920SX (Part B) “Supplemental Information for PLP/SBA Express Processing,” and (4) a copy of Form 7, “Eligibility Information for Preferred Lender Participation (PLP) Loans.” If the PLP loan is to refinance debt (not same institution debt), a fully completed business indebtedness schedule must be attached. If the PLP loan is to finance change of ownership and a business valuation is

performed by the lender, a synopsis of the analysis must be submitted.34

SBA Guaranty and Servicing Fees

To offset its costs, the SBA charges lenders an upfront, one-time guaranty fee and an annual, ongoing servicing fee for each loan approved and disbursed. The maximum guaranty fee for 7(a) loans with maturities exceeding 12 months is set by statute. Also, the servicing fee cannot exceed 0.55% per year of the outstanding balance of the SBA’s share of the loan.

The 7(a) program’s guaranty fee is based on loan maturity and the amount of the guaranty portion of the loan. For loans with a maturity of 12 months or less, the SBA charges the lender a 0.25% guaranty fee, which the lender is required to submit with the application. The lender may charge the borrower for the fee when the loan is approved by the SBA.35

For loans with a maturity exceeding 12 months, the SBA charges the lender a 2% guaranty fee for the SBA guaranteed portion of loans of $150,000 or less, a 3% guaranty fee for the SBA

guaranteed portion of loans exceeding $150,000 but not more than $700,000, and a 3.5% guaranty fee for the SBA guaranteed portion of loans exceeding $700,000. Loans with an SBA guaranteed portion in excess of $1 million are charged an additional 0.25% guaranty fee on the guaranteed amount in excess of $1 million.36 These fees are the maximum allowed by law.37 The

33 PLP lenders approved 12,496 7(a) loans amounting to $8.4 billion in FY2012, 15,167 7(a) loans amounting to $10.7

billion in FY2011, and 13,168 7(a) loans amounting to $6.9 billion in FY2010. See U.S. Small Business

Administration, “SBA Lending Statistics for Major Programs (as of 9/30/2012),” at http://www.sba.gov/about-sba-info/ 317721.

34 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), p. 221, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf. Lenders are considered for PLP status based on their record with SBA, and must have demonstrated a proficiency in processing and servicing SBA-guaranteed loans. The SBA continues to review the submitted materials to check loan eligibility criteria. See U.S. Small Business Administration, “The Preferred Lenders Program (PLP),” at http://www.sba.gov/content/preferred-lenders-program-plp. Of the 3,537 active lenders in the 7(a) program in FY2011, 545 participated in the Preferred Lenders Program.

35 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), pp. 83, 163, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf. The fee is refundable if the loan application is withdrawn prior to SBA approval, the SBA declines to guarantee the loan, or the SBA substantially changes the loan terms and those terms are unacceptable to the lender. Also, because the SBA does not approve or decline the credit for PLP loans, PLP lenders are required to send the guaranty fee directly to the SBA Denver Finance Center within 10 business days from the date the loan number is assigned and before the lender signs the Authorization for SBA.

36 15 U.S.C. 636(a)(18)(a).

37 U.S. Small Business Administration, “Small Business Jobs Act: Implementation of Conforming and Technical

lender must pay the SBA guaranty fee within 90 days of the date of loan’s approval and may charge the borrower for the fee after the lender has made the first disbursement of the loan. Lenders are permitted to retain 25% of the up-front guaranty fee on loans with a gross amount of $150,000 or less.38

The annual ongoing servicing fee for all 7(a) loans is required to be no more than the “rate necessary to reduce to zero the cost to the Administration” of making guaranties and, as

mentioned previously, cannot exceed 0.55% of the outstanding balance of the guaranteed portion of the loan.39 The current rate is the maximum allowed by law—0.55% of the outstanding balance of the guaranteed portion of the loan.40 The lender’s annual service fee to the SBA cannot be

charged to the borrower.41

Lender Packaging, Servicing and Other Fees

The lender may charge an applicant “reasonable fees” customary for similar lenders in the geographic area where the loan is being made for packaging and other services. The lender must advise the applicant in writing that the applicant is not required to obtain or pay for unwanted services. These fees are subject to SBA review at any time, and the lender must refund any such fee considered unreasonable by the SBA.42

The lender may also charge an applicant an additional fee if, subject to prior written SBA approval, all or part of a loan will have extraordinary servicing needs. The additional fee can not exceed 2% per year on the outstanding balance of the part requiring special servicing (e.g., field inspections for construction projects). The lender may also collect from the applicant necessary out-of-pocket expenses, including filing or recording fees, photocopying, delivery charges, collateral appraisals, environmental impact reports that are obtained in compliance with SBA policy, and other direct charges related to loan closing.43 The lender is prohibited from requiring

the borrower to pay any fees for goods and services, including insurance, as a condition for obtaining an SBA guaranteed loan, and from imposing on SBA loan applicants processing fees, origination fees, application fees, points, brokerage fees, bonus points, and referral or similar fees.44

(...continued)

Amendments,” 76 Federal Register 63544, 63545, October 13, 2011.

38 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), p. 163, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

39 15 U.S.C. 636(a)(23)(a).

40 U.S. Small Business Administration, “SBA Information Notice: 7(a) and 504 Fees Effective On October 1, 2012,” at

http://www.colsonservices.com/main/news/5000-1253%20-%207(a)%20and%20504%20Fees%20Effective%20On%20October%201%202012.pdf.

41 15 U.S.C. 636(a)(23)(b). 42 13 C.F.R. §120.221.

43 Ibid.; and U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan

Programs,” (effective June 1, 2012), p. 171, at

http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

44 13 C.F.R. §120.222. A commitment fee may be charged for a loan made under the Export Working Capital Loan

The lender is also allowed to charge the borrower a late payment fee not to exceed 5% of the regular loan payment when the borrower is more than 10 days delinquent on its regularly scheduled payment. The lender may not charge a fee for full or partial prepayment of a loan.45

For loans with a maturity of 15 years or longer, the borrower must pay to the SBA a subsidy recoupment fee when the borrower voluntarily prepays 25% or more of its loan in any one year during the first three years after first disbursement. The fee is 5% of the prepayment amount during the first year, 3% the second year, and 1% in the third year.46

Program Statistics

Loan Volume

The SBA generally uses the number and amount of loans approved each fiscal year, as opposed to the number and amount of loans disbursed, for making comparisons of lending volume among its loan guaranty programs. Although loan disbursement data can be useful, loan disbursements in one fiscal year typically include significant amounts approved in previous fiscal years. For example, in FY2012, 38% of 7(a) loan disbursements were from loans approved prior to FY2012.47

The number of 7(a) loans approved annually is typically about 10% to 20% higher than the number of loans disbursed (e.g., some borrowers decide not to accept the loan or there is a change in business ownership.). The amount of 7(a) loans approved annually is typically about 10% to 15% higher than the amount disbursed.48

As shown in Table 1, the total number and amount of SBA 7(a) loans approved declined in FY2008 and FY2009, increased during FY2010 and FY2011, and then declined somewhat in FY2012.

As mentioned previously, the SBA attributed the decreased number and amount of 7(a) loans approved in FY2008 and FY2009 to a reduction in the demand for small business loans resulting from the economic uncertainty of the recession (December 2007 - June 2009) and to tightened loan standards imposed by lenders concerned about the possibility of higher loan default rates resulting from the economic slowdown. The SBA attributed the increased number of loans approved in FY2010 and FY2011 to legislation that provided funding to temporarily reduce the

45 13 C.F.R. §120.221; and U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company

Loan Programs,” (effective June 1, 2012), p. 172, at

http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

46 13 C.F.R. §120.223; and U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company

Loan Programs,” (effective June 1, 2012), p. 172, at

http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

47 U.S. Small Business Administration, Office of Congressional and Legislative Affairs, correspondence with the

author, September 17, 2012. The SBA maintains selected disbursement data and will provide that data to congressional offices by request.

48 U.S. Small Business Administration, “SBA Lending Report for Major Programs, Fiscal Year 2010,” October 4,

2010, at http://archive.sba.gov/idc/groups/public/documents/sba_homepage/serv_fa_lending_major_progs.pdf; and U.S. Small Business Administration, Office of Congressional and Legislative Affairs, correspondence with the author, September 17, 2012.

7(a) program’s loan fees and temporarily increase the 7(a) program’s loan guaranty percentage to 90% for all standard 7(a) loans from up to 85% of loans of $150,000 or less and up to 75% of loans exceeding $150,000.49 The fee subsidies and 90% loan guaranty percentage were in place

during most of FY2010 and the first quarter of FY2011.50

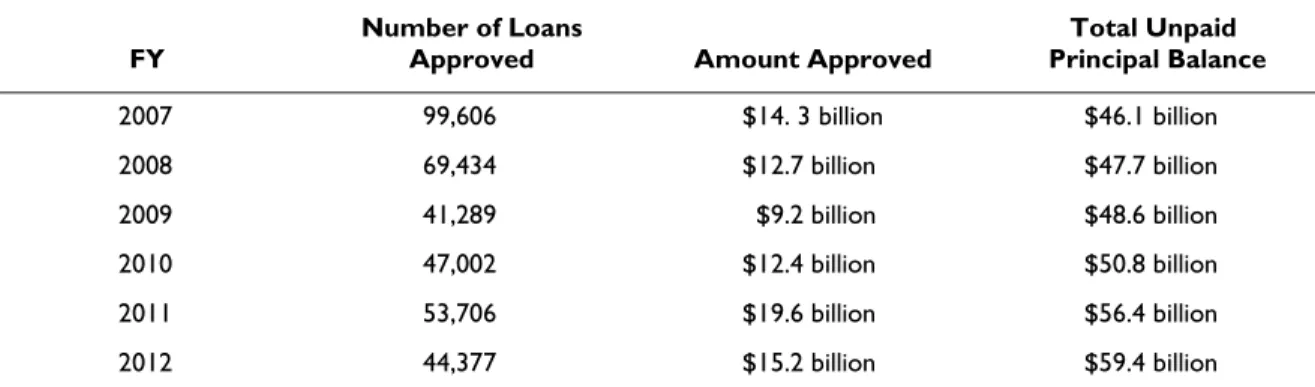

Table 1. 7(a) Loan Guaranty Program, Loan Volume, FY2007-FY2012 FY Number of Loans Approved Amount Approved Principal Balance Total Unpaid

2007 99,606 $14. 3 billion $46.1 billion

2008 69,434 $12.7 billion $47.7 billion

2009 41,289 $9.2 billion $48.6 billion

2010 47,002 $12.4 billion $50.8 billion

2011 53,706 $19.6 billion $56.4 billion

2012 44,377 $15.2 billion $59.4 billion

Sources: U.S. Small Business Administration, Agency Financial Report Fiscal Year 2010, Washington, DC,

November 15, 2010, p. 7; U.S. Small Business Administration, Fiscal Year 2011 Congressional Budget Justification and FY 2009 Annual Performance Report, Washington, DC, pp. 36, 125; U.S. Small Business Administration, “SBA Lending Statistics for Major Programs (as of 9/30/2012),” at http://www.sba.gov/about-sba-info/317721; and U.S. Small Business Administration, “Table 1 ─ Unpaid Principal Balance By Program,” Washington, DC,

http://www.sba.gov/sites/default/files/files/WDS_UPB_Report_2011Q3.pdf.

Notes: The number of 7(a) loans approved annually is typically about 10% to 20% higher than the number of loans disbursed (e.g., some borrowers decide not to accept the loan, there is a change in business ownership, etc.). The amount of 7(a) loans approved annually is typically about 10% to 15% higher than the amount disbursed. U.S. Small Business Administration, Office of Congressional and Legislative Affairs, correspondence with the author, September 17, 2012.

49 U.S. Small Business Administration, Press Office, “Recovery Loan Incentives Spurred Continued Rebound in SBA

Lending in FY2010,” October 4, 2010, at http://www.sba.gov/about-sba-services/7367/5527; and U.S. Small Business Administration, “Jobs Act Supported More Than $12 Billion in SBA Lending to Small Businesses in Just Three Months,” January 3, 2011, at http://www.sba.gov/content/jobs-act-supported-more-12-billion-sba-lending-small-businesses-just-three-months.

50 P.L. 111-5, the American Recovery and Reinvestment Act of 2009 (ARRA), enacted on February 17, 2009, provided

the SBA $375 million to temporarily reduce fees in the 7(a) and 504/CDC loan guaranty programs, and increase the 7(a) program’s maximum loan guaranty percentage to 90% for all standard 7(a) loans through September 30, 2010, or until available funds were exhausted. Due to the increased demand for 7(a) loans, available funding was anticipated to be exhausted in early January 2010. P.L. 111-118, the Department of Defense Appropriations Act, 2010, provided the SBA $125 million to continue the fee subsidies and 90% maximum loan guaranty percentage through February 28, 2010. P.L. 111-144, the Temporary Extension Act of 2010, provided the SBA $60 million to continue the fee subsidies and 90% maximum loan guaranty percentage through March 28, 2010. P.L. 111-150, an act to extend the Small Business Loan Guarantee Program, and for other purposes, provided the SBA authority to reprogram $40 million in previously appropriated funds to continue the fee subsidies and 90% maximum loan guaranty percentage through April 30, 2010. P.L. 111-157, the Continuing Extension Act of 2010, provided the SBA $80 million to continue the SBA’s fee subsidies and 90% maximum loan guaranty percentage through May 31, 2010. The fee subsidies and 90% loan guaranty percentage expired on May 31, 2010. P.L. 111-240, the Small Business Jobs Act of 2010, enacted on September 27, 2010, provided the SBA $505 million (plus an additional $5 million for related administrative expenses) to reinstate the fee subsidies and 90% maximum loan guaranty percentage through December 31, 2010, or until available funds were exhausted. P.L. 111-322, the Continuing Appropriations and Surface Transportation Extensions Act, 2011, authorized the SBA to use any funds remaining from the Small Business Jobs Act of 2010 to continue the fee subsidies and the 7(a) program’s 90% maximum loan guaranty percentage through March 4, 2011, or until the available funding was exhausted. The funds were exhausted on January 3, 2011.

Table 1 also provides, for comparison purposes, the total amount of the 7(a) program’s unpaid principal balance. Precise measurements of the total credit market for small businesses is not available. However, the SBA has estimated that the credit market for small businesses (outstanding bank loans of $1 million or less, plus credit extended by finance companies) is roughly $1.0 trillion.51 The SBA’s 7(a) program’s unpaid principal balance of $59.4 billion is

about 5.9% of that amount.

Loss Rate and Appropriations for Subsidy Costs

Since its inception in 1953 through 2008, the 7(a) program (including subprograms) experienced a 5.83% loss rate (ratio of actual losses to disbursements).52 In recent years, the loss rate for both

7(a) and 504/CDC programs has exceeded historical averages. As of June 30, 2012, the 7(a) program’s loss rate since the program’s inception in 1953 was 6.36%.53

One of the SBA’s goals is to achieve a zero subsidy rate for its loan guaranty programs. A zero subsidy rate means that the SBA’s loan guaranty programs do not require annual appropriations of budget authority for the issuance of new loan guarantees. From 2005 to 2009, the SBA did not request appropriations to subsidize the cost of any of its loan guaranty programs, including the 7(a) program. However, in recent years, SBA loan guaranty fees and loan liquidation recoveries, especially in the 7(a) loan guaranty program, have not generated enough revenue to cover loan losses, resulting in the need for additional appropriations to account for the shortfall. In FY2010 and in FY2011, the SBA was provided $80.0 million to subsidize the cost of SBA guaranteed loans. In FY2012, the SBA was provided $207.1 million for that purpose, and P.L. 112-175, the Continuing Appropriations Resolution, 2013 (which provides appropriations through March 27, 2013), provided a projected $333.6 million for the cost of SBA loan guaranty program subsidies for FY2013.

The SBA reports that most of the agency’s loan losses have occurred in the SBA’s 7(a) loan guaranty program. For example, the SBA applied all of the FY2010 and FY2011 subsidy amounts ($80.0 million each year) to the 7(a) program, anticipates applying 67.3% ($139.4 million) of the FY2012 subsidy amount ($207.1 million) to the 7(a) program, and 67.6% ($224.5 million) of the FY2013 subsidy ($333.6 million) to the 7(a) program.54

51 U.S. Small Business Administration, Office of Advocacy, “Frequently Asked Questions About Small Business

Finance,” September 2011, at http://www.sba.gov/sites/default/files/Finance%20FAQ%208-25-11%20FINAL%20for%20web.pdf.

52 U.S. Small Business Administration, FY 2008 Small Business Administration (SBA) Loss Report, p. 7, at

http://archive.sba.gov/idc/groups/public/documents/sba_program_office/cfo_2008_loss_report.pdf. Loans include those made through the SBA’s 7(a), 8(A), FIS 8a, Economic Opportunity, Small Business Energy, Handicap Assistance, Veterans, Pollution Control, Import Export, Foreign Trade, USCAIP (NAFTA) and Reconstruction Finance Corporation Business programs.

53 U.S. Small Business Administration, Office of Congressional and Legislative Affairs, correspondence with the

author, September 17, 2012. 7(a) program loan loss was calculated by subtracting total 7(a) loan purchases from total 7(a) program disbursements, and then adding total 7(a) loan recoveries.

54 U.S. Small Business Administration, FY 2013 Congressional Budget Justification and FY 2011 Annual Performance Report, p. 19, at http://www.sba.gov/sites/default/files/files/FY%202013%20CBJ%20FY%202011%20APR.pdf.

Administrative Expenses

In FY2011, the SBA’s spent $88.0 million on the 7(a) program for administrative expenses, including $44.2 million for loan making, $4.0 million for loan servicing, $26.8 million for loan liquidation, and $13.0 million for lender oversight. The SBA anticipates that the administrative costs for the 7(a) loan will be $89.5 million in FY2012 and $93.8 million in FY2013.55

Use of Proceeds and Borrower Satisfaction

In 2008, the Urban Institute released the results of an SBA-commissioned study of the SBA’s loan guaranty programs. As part of its analysis, the Urban Institute surveyed a random sample of SBA loan guaranty borrowers. The survey indicated that borrowers used 7(a) loan proceeds to

• purchase or install new equipment (34%);

• finance working capital (23%);

• acquire original business (21%);

• other (19%);

• expand or renovate current building (14%);

• purchase new building (10%);

• refinance existing debt (8%);

• hire additional staff (6%);

• build new building (4%);

• purchase new land (3%); and

• improve land (2%).56

The Urban Institute also reported that most of the 7(a) borrowers responding to their survey rated their overall satisfaction with their 7(a) loan and loan terms as either excellent (18%) or good (50%). One out of every five 7(a) borrowers (20%) rated their overall satisfaction with their 7(a) loan and loan terms as fair, and 6% rated their overall satisfaction with their 7(a) loan and loan terms as poor (7% reported don’t know or did not respond).57 In addition, 90% of the survey’s

respondents reported that the 7(a) loan was either very important (62%) or somewhat important (28%) to their business success (2% reported somewhat unimportant, 3% reported very

unimportant, and 4% reported don’t know or did not respond).58

55 U.S. Small Business Administration, Fiscal Year 2013 Congressional Budget Justification and FY 2011 Annual Performance Report, p. 21.

56 Christopher Hayes, An Assessment of Small Business Administration Loan and Investment Performance: Survey of Assisted Businesses (Washington, DC: The Urban Institute, 2008), p. 3, at http://www.urban.org/UploadedPDF/ 411599_assisted_business_survey.pdf. The percentage total exceeds 100 because recipients were allowed to name more than one use for the loan proceeds.

57 Ibid., p. 5. 58 Ibid.

Borrower Demographics

The Urban Institute found that about 9.9% of conventional small business loans are issued to minority-owned small businesses and about 16% of conventional small business loans are issued to women-owned businesses.59 In FY2012, 22.5% of 7(a) loan recipients were minority-owned

businesses (12.1% Asian, 7.1% Hispanic, 2.4% African-American, and 0.9% other minority) and 16.6% were women-owned businesses.60 Based on its comparative analysis of conventional small

business loans and the SBA’s loan guaranty programs, the Urban Institute concluded:

SBA’s loan programs are designed to enable private lenders to make loans to creditworthy borrowers who would otherwise not be able to qualify for a loan. As a result, there should be differences in the types of borrowers and loan terms associated with SBA-guaranteed and conventional small business loans.

Our comparative analysis shows such differences. Overall, loans under the 7(a) and 504 programs were more likely to be made to minority-owned, women-owned, and start-up businesses (firms that have historically faced capital gaps) as compared to conventional small business loans. Moreover, the average amounts for loans made under the 7(a) and 504 programs to these types of firms were substantially greater than conventional small business loans to such firms. These findings suggest that the 7(a) and 504 programs are being used by lenders in a manner that is consistent with SBA’s objective of making credit available to firms that face a capital opportunity gap.61

Congressional Issues

Access to Capital

Congressional interest in the 7(a) loan program has increased in recent years largely because of concerns that small businesses might be prevented from accessing sufficient capital to enable them to assist in the economic recovery. During the 111th Congress, several laws were enacted to

increase the supply and demand for capital for both large and small businesses.62 For example, in 2008, Congress adopted P.L. 110-343, the Emergency Economic Stabilization Act of 2008, which authorized the Troubled Asset Relief Program (TARP). Under TARP, the U.S. Department of the Treasury was authorized to purchase or insure up to $700 billion in troubled assets, including small business loans, from banks and other financial institutions. The law’s intent was “to restore liquidity and stability to the financial system of the United States.”63 P.L. 111-203, the

Dodd-Frank Wall Street Reform and Consumer Protection Act, reduced total TARP purchase authority

59 Kenneth Temkin, Brett Theodos, with Kerstin Gentsch, Competitive and Special Competitive Opportunity Gap Analysis of the 7(A) and 504 Programs (Washington, DC: The Urban Institute, 2008), p. 13, at http://www.urban.org/ UploadedPDF/411596_504_gap_analysis.pdf.

60 U.S. Small Business Administration, “SBA Lending Statistics for Major Programs (as of 9/30/2012),” at

http://www.sba.gov/about-sba-info/317721.

61 Kenneth Temkin, Brett Theodos, with Kerstin Gentsch, Competitive and Special Competitive Opportunity Gap Analysis of the 7(A) and 504 Programs (Washington, DC: The Urban Institute, 2008), p. 21, at http://www.urban.org/ UploadedPDF/411596_504_gap_analysis.pdf.

62 For further analysis, see CRS Report R40985, Small Business: Access to Capital and Job Creation, by Robert Jay

Dilger.

from $700 billion to $475 billion. The Treasury Department’s authority to make new financial commitments under TARP ended on October 3, 2010. The Department of the Treasury has disbursed approximately $389 billion in TARP funds, including $337 million to purchase SBA 7(a) loan guaranty program securities.64

In addition, as mentioned previously, in 2009, ARRA provided an additional $730 million for SBA programs, including $375 million to temporarily reduce fees in the SBA’s 7(a) and 504/CDC loan guaranty programs and increase the 7(a) program’s maximum loan guaranty percentage from up to 85% of loans of $150,000 or less and up to 75% of loans exceeding $150,000 to 90% for all standard 7(a) loans. Congress subsequently provided another $265 million, and authorized the SBA to reprogram another $40 million, to extend the fee reductions and loan modification

through May 31, 2010, and the Small Business Jobs Act of 2010 provided another $510 million to extend the fee reductions and loan modification from September 27, 2010, through December 31, 2010. Also, P.L. 111-322, the Continuing Appropriations and Surface Transportation Extensions Act, 2011, authorized the use of any funding remaining from the Small Business Jobs Act of 2010 to extend the fee subsidies and 90% maximum loan guaranty percentage through March 4, 2011, or until the available funding was exhausted.65 Funding for these purposes was exhausted on

January 3, 2011.

The Obama Administration argued that TARP and the additional funding for the SBA’s loan guaranty programs helped to improve the small business lending environment and supported “the retention and creation of hundreds of thousands of jobs.”66 Critics argued that small business tax

reduction, reform of financial credit market regulation, and federal fiscal restraint are the best means to assist small business economic growth and job creation.67

64 U.S. Department of the Treasury, Troubled Assets Relief Program Monthly 105(a) Report – November 2010,

December 10, 2010, pp. 2-4, at http://www.financialstability.gov/docs/November%20105(a)%20FINAL.pdf. On March 16, 2009, President Obama announced that the Department of the Treasury would use TARP funds to purchase up to $15 billion of SBA-guaranteed loans to “immediately unfreeze the secondary market for SBA loans and increase the liquidity of community banks.” The plan was deferred after it met resistance from lenders. Some lenders objected to TARP’s requirement that participating lenders comply with executive compensation limits and issue warrants to the federal government. Smaller, community banks objected to the program’s paperwork requirements, such as the provision of a small-business lending plan and quarterly reports. See The White House, “Remarks by the President to Small Business Owners, Community Leaders, and Members of Congress,” March 16, 2009, at

http://www.whitehouse.gov/the_press_office/Remarks-by-the-President-to-small-business-owners/.

65 P.L. 111-240, the Small Business Jobs Act of 2010, §1111. Section 7(A) Business Loans. The Senate had adopted

H.R. 4213, the American Workers, State, and Business Relief Act of 2010, on March 10, 2010, by a 62-36 vote. It would have provided $560 million to extend the fee reductions and 90% loan guarantee limit through December 31, 2010. The House approved an amended version of the bill, renamed the American Jobs and Closing Tax Loopholes Act of 2010, on May 28, 2010, by a 245-171 vote. It would have provided $505 million to extend the fee reductions and 90% loan guarantee limit through December 31, 2010. The extension provision was subsequently removed from the bill, which became P.L. 111-205, the Unemployment Compensation Extension Act of 2010.

66 U.S. Small Business Administration, “Administration Announces New Small Business Commercial Real Estate and

Working Capital Programs,” February 5, 2010, at http://www.sba.gov/sites/default/files/ sba_rcvry_factsheet_cre_refi.pdf.

67 Susan Eckerly, “NFIB Responds to President’s Small Business Lending Initiatives,” Washington, DC, October 21,

2009, at http://www.nfib.com/newsroom/newsroom-item/cmsid/50080/; and NFIB, “Government Spending,” Washington, DC, at http://www.nfib.com/issues-elections/issues-elections-item/cmsid/49051/.

Program Administration

The SBA’s Office of Inspector General (OIG) and the U.S. Government Accountability Office (GAO) have independently reviewed the SBA’s administration of the agency’s loan guaranty programs. Both agencies have reported deficiencies in the SBA’s administration of its loan guaranty programs that they argue need to be addressed, including issues involving the oversight of 7(a) lenders and the lack of outcome-based performance measures.

Oversight of 7(a) Lenders

The SBA’s OIG has argued that the 7(a) loan guaranty program “is vulnerable to fraud and unnecessary losses because it relies on numerous third parties (e.g., borrowers, loan agents, and lenders)” to complete loan transactions for about 80% of the loans guaranteed annually by the SBA.68 It has argued that the SBA needs to strengthen oversight of 7(a) lenders to “establish more

robust controls to prevent waste, fraud, abuse, and inefficiencies.”69

The SBA OIG has argued that the results of its review of the 7(a) program’s FY2008 lending indicate the need for strengthened lender oversight. The SBA OIG found that the SBA’s estimate of improper payments for FY2008 significantly understated the level of erroneous payments in the program. The SBA reported that improper payments were 0.53% of FY2008 program outlays, whereas the SBA’s OIG estimated the improper payment rate to be 29% (approximately $248 million) of the $869 million in loan guaranties purchased between April 1, 2007, and March 31, 2008.70 In addition, the SBA OIG’s review of a sample of 30 7(a) loans issued in FY2008 found

that 14 of the loans lacked evidence to support lender compliance with SBA origination, servicing, or liquidation requirements, resulting in improper payments totaling $723,293. In contrast, the SBA reported improper payments of $4,468 on two of the sampled loans.71

In 2009, GAO also recommended that the SBA strengthen its oversight of 7(a) program lenders. GAO argued that although the SBA’s “lender risk rating system has enabled the agency to conduct some off-site monitoring of lenders, the agency does not use the system to target lenders for on-site reviews or to inform the scope of the reviews.”72 It also noted that

the SBA targets for review those lenders with the largest SBA-guaranteed loan portfolios. As a result of this approach, 97 percent of the lenders that SBA’s risk rating system identified as high risk in 2008 were not reviewed. Further, GAO found that the scope of the on-site reviews that SBA performs is not informed by the lenders’ risk ratings, and the reviews do not include an assessment of lenders’ credit decisions.73

68 U.S. Small Business Administration, Office of Inspector General, “Semiannual Report to Congress, Fall 2009,” p. 5,

at http://www.sba.gov/office-of-inspector-general/867/12348.

69 Ibid., p. 3. 70 Ibid., p. 5. 71 Ibid.

72 U.S. Government Accountability Office, Small Business Administration: Actions Needed to Improve the Usefulness of the Agency’s Lender Risk Rating System, GAO-1—53, November 6, 2009, p. i, at http://www.gao.gov/new.items/ d1053.pdf.

GAO argued that although the SBA “has made improvements to its off-site monitoring of lenders, the agency will not be able to substantially improve its lender oversight efforts unless it improves its on-site review process.”74

In a separate report concerning the SBA’s administration of the 7(a) program, GAO also argued in 2009 that the SBA needs to “improve its oversight of lenders’ compliance with the credit

elsewhere requirement.”75 The Small Business Act specifies that “no financial assistance shall be extended pursuant to this subsection if the applicant can obtain credit elsewhere.”76 The SBA

provides lenders the following six reasons for certifying in its application that the borrower meets the credit elsewhere requirement:

• the business needs a longer maturity than the lender’s policy permits (for example, the business needs a loan that is not on a demand basis);

• the requested loan exceeds either the lender’s legal lending limit or policy limit regarding the amount that it can lend to one customer;

• the lender’s liquidity depends upon selling the guaranteed portion of the loan on the secondary market;

• the collateral does not meet the lender’s policy requirements;

• the lender’s policy normally does not allow loans to new businesses or businesses in the applicant’s industry; or

• any other factors relating to the credit that, in the lender’s opinion, cannot be overcome except for the guaranty. These other factors must be specifically documented in the loan file.77

GAO argued that “SBA’s guidance to lenders on documenting compliance with the credit

elsewhere requirement is limited” because it “does not specify the amount of detail lenders should include in their explanations.”78 GAO noted that “even with the lack of detail required,” the

SBA’s own on-site reviews of 7(a) lenders over a recent six-quarter period indicated that nearly a third of the lenders reviewed had not consistently documented that borrowers met the credit elsewhere requirement.79

74 Ibid., p. 35.

75 U.S. Government Accountability Office, Small Business Administration: Additional Guidance on Documenting Credit Elsewhere Decisions Could Improve 7(a) Program Oversight, GAO-09-228, February 12, 2009, p. 3, at http://www.gao.gov/new.items/d09228.pdf.

76 15 U.S.C. 636(a)(1)(A). The act defines credit elsewhere as “the availability of credit from non-Federal sources on

reasonable terms and conditions taking into consideration the prevailing rates and terms in the community in or near where the concern transacts business, or the homeowner resides, for similar purposes and periods of time.” See 15 U.S.C. 632(h).

77 U.S. Small Business Administration, “SOP 50 10 5(E): Lender and Development Company Loan Programs,”

(effective June 1, 2012), p. 102, at http://www.sba.gov/sites/default/files/SOP%2050%2010%205(E)%20(5-16-2012)%20clean.pdf.

78 U.S. Government Accountability Office, Small Business Administration: Additional Guidance on Documenting Credit Elsewhere Decisions Could Improve 7(a) Program Oversight, GAO-09-228, February 12, 2009, pp. 25-26, at http://www.gao.gov/new.items/d09228.pdf.