THE REAL ESTATE INVESTMENTS AND THE

FINANCIAL CRISIS IN ROMANIA

Prof. Ana POPA, PhD

Assoc. Prof. Laura GIURCĂ VASILESCU, PhD University of Craiova

1. Introduction

The real estate sector in Romania has a great importance in the economy and banking system as well as in all developed economies.

In 2002-2008 period, the real estate investments were the most attractive investments for the population, mainly due to price developments by 2008. It can be said that it has occurred in Romania as a phenomenon of speculation in the property sector, namely the speculative ”bubble”.

The companies operating in construction and real estate sectors fall into the "vicious cycle" of economic growth – crisis relationship, so that during the boom, they have a growing role for the economy and banking system, but during crisis, any disturbance on the real estate asset market is likely to have an increasing impact on financial stability.

In the same time, the crisis in Romania is based on two principal factors that may constrain the pace of the recovery, namely: the restrictive bank lending and the weak job market.

2. The real estate ”bubble” and the global financial crisis

The wide range of researches and statistics data shows an enormous real estate stock boom that started around 1982 and picked up incredible speed after 1995.

First of all, many economists argue that this boom represents a speculative

”bubble”, because it is not grounded in sensible economic fundamentals.

Secondly, this boom must be placed it in the context of financial crisis starting in 2007. In fact, the global financial crisis has begun with the north-American subprime mortgage debacle in 2007.

As of 2006, several areas of the world are thought by some to be in a bubble state, although the subject is highly controversial. As the boom progressed, buying prices become high (in relation to rents and financing costs) in many countries, leading to decisions by some buyers to rent instead of buying. Mortgage-holders also came under extreme pressure as interest rates rose.

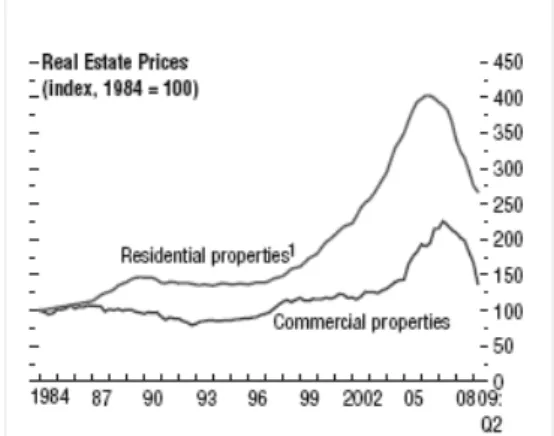

Figure 1. Real estate prices in US

Source: World Economic Outlook, October 2009, IFM, p.26.

House prices continue to decline across a broad range of economies.

An analysis of past house price cycles suggests that for most economies, there could still be significant corrections to come given the stronger-than average upturn in house prices that preceded the present downturn. Moreover, the global recession has put pressure on commercial property markets, where increasing vacancy rates and decreasing rents drove down nonresidential construction investment.

Leveraged commercial real estate investors are likely to face difficulties in refinancing the loans that are coming due, and soaring delinquencies therefore have the potential to create a second wave of financial distress in exposed financial institutions.

The ongoing effects on the real economy of house price corrections and increasing stress in commercial property markets are being amplified in economies where construction has been an important contributor to growth in recent years, where consumption was driven by house price appreciations, and where commercial real estate markets have been placed in a precarious position by the weakening of the real economy.

One such trend might be the rapid growth of developing economies such as the BRIC (Brazil, Russia, China, India) group. This has caused significant growth in monetary reserves and savings in those countries, which in turn has made possible extension of credit elsewhere.

The subprime mortgage crisis, with its accompanying impacts and effects on economies in various nations, has given some credence to the idea that these trends might have some common characteristics.

The problems of the real estate sector are placed in the financial crisis and these are explained by following chain: first, the substantial increase in the rate of personal bankruptcies, which could lead to a secondary string of bankruptcies of financial institutions as well.

Table 1. Announced bank losses Periods Total Billions of US dollars Of witch: Real estate % of total T3-T4 2007 206.0 3.2 1.6 T3-T4 2007 435.8 55.9 12.8 T1 2009 93.7 3.0 3.2

Source: Bank for International Settlements, 79th Annual Report, 1 April 2008– 31 March 2009, Basel, 29 June 2009, p.41.

The main long-run consequence could be a decline in consumer and local business confidence, and another, possibly worldwide, recession.

3. The trend of the real estate sector to the Romanian economy and

speculative ”bubble”

The evolution from the Romanian real estate market was an atypical trend in the transition period.

The real estate market from Romania reappeared and developed quickly after 1990, with the mention that the transactions from the real estate market took over the rhythm of legal settlement and of international harmonization.

In 1990-2000 periods, the real estate assets have a low level price, in comparison with Europe, but with a high price increase.

In this period, another problem was the manifestation of a demand increase underlined by a lack of a supply for new constructions and especially by a lack of a true mortgage market in the first years of transition. In 1990-2000 periods, it can appreciate that it was got to the “seller market” stage, when the sellers establish the prices and the sales.

In 2001-2007 periods, many developers, especially foreign investors have increased the supply of the real estate market (residential or commercial real estate).

In 2001-2007 periods, there is a sharply increase of the prices, but these increase was without any relation between the general development level or the standing level of houses and the market value; with other words, there is an unnatural report low quality (most constructions was old) – high price for majority transactions.

Prices for residential units in projects launched in the first half of the year 2007 raised an average of 20%. For example, in 2006 the average construction price was Є600/sqm and in 2007 it rose to Є750/sqm. The market remained at an average of Є1,500/sqm. The lowest average price for a 2-bedroom apartment in a new project with over 200 units stands at about Є

133,000+VAT(19%) in the western part of the city Bucharest.

Also, in Bucharest, the average rents in shopping centers in 2007 registered levels of Є24- 27/sqm/month, decrease of 4% compared to 2006. In the rest of the country, there was a slightly lower and wider range, of Є15- 25/sqm/ month, compared to the Є18- 25/sqm/ month in 2006.

One can appreciate that the year 2007, especially for residential, was characterized as a speculative “bubble”, sustained on the active mortgage market and easy.

In 2008, the financial crisis affected also the Romanian economy. The problems of the real estate sector are placed in the financial crisis, and Romanian financial system was also affected by real estate exposures.

One of the problem is that Romania does not publish official house price statistics. General economics statistics are offered by National Institute of Statistics (NIS) and the National Bank of Romania (NBR).

But, there is different unofficial information. For example, Business Monitor International has elaborated the Romania Real Estate Report. Last Report, July 2009, has been researched

at source, and features latest-available data covering commercial and residential construction (value and growth), bank lending growth, bank lending rates, house price growth, rental prices and yields, real GDP growth, inflation, exchange rates and other key macroeconomic data; 5-year industry forecasts through end-2013, company rankings and competitive landscapes covering leading multinational and national Real Estate companies; and analysis of latest industry news, trends and regulatory developments in Romania.

Also, Colliers International’s annual Real Estate Review has prices of exclusive, middle and lower classes of apartments, mainly in Bucharest.

4. Net Romanian household wealth and real estate exposures in the

Romanian financial system After 1990, the real estate sector plays an increasing role for the Romanian economy and the banking sector.

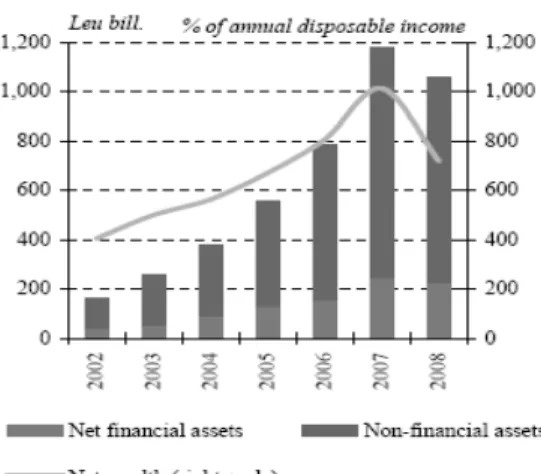

Especially, in 2002-2008 periods, the Non-financial assets (including only real estate, the most important assets) are increased in total net household wealth (Fig.2).

Figure 2.Net household wealth

Source: NBR, Financial stability report, Bucharest, 2009, p.88.

The wealth of Romanian population has increased by over 6 times the period 2002-2007.

Financial assets were in late 2008, about 15% of the wealth of population and non-financial assets remaining 85%, including the value of buildings.

In this period, the real estate investments were the most attractive investments for the population, mainly due to price developments by 2008.

The real estate sectoraccounts for a mere 1 percent of the overall turnover, yet it holds 12 percent (as of June 2008) of total assets economy-wide, as against 3 percent in December 2004.

Banks’ exposure to construction and real estate sectors is relatively high; it is on the rise compared to their importance in the economy (21 percent of the outstanding loans in March 2009); and it has a heterogeneous nature as far as credit institutions are concerned.

Table 2. Number of finished dwellings, by financing sources -thou Total of finished dwellings Private

funds Public funds 2001 27,0 25,3 1,3 2002 27,7 24,4 3,0 2003 29,1 22,9 6,1 2004 30,1 25,2 4,9 2005 32,9 27,5 3,8 2006 39,6 34,8 4,8 Sorces: NIS, Yearbook statistics of Romania, 2007,

p.276.

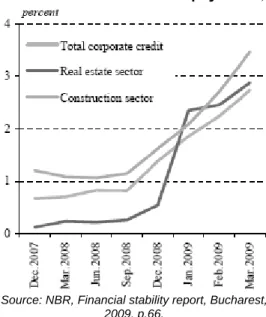

As shown in Fig.3, the default rate generated by real estate and construction companies (3.2 percent in March 2009) is higher than the economy wide rate (2.7 percent, March 2009).

Figure 3. Default rate (excluding off balance sheet overdue payments)

Source: NBR, Financial stability report, Bucharest, 2009, p.66.

Bank loans to companies are

primarily collateralised by real estate assets (about 75 percent of total loans, as of March 2009). The default rate on these loans has registered a significant rise in recent months, particularly in the case of the forex - denominated component. There does not seem to be any difference in terms of default behaviour between mortgage-backed loans and unsecured ones, the default rate is approximately the same, namely 2.6 - 2.8 percent as of March 2009. However, the balance of overdue credit reached 9.4 percent in March 2009 against 3.2 percent in December 2007, so that the default rate looks poised for an increase.

Bank loans to households are being

increasingly collateralised by real estate assets (47 percent in March 2009 versus 42 percent in December 2007). Both the default rate and the volume of overdue loans have risen considerably over the past year, although they remain still at manageable levels (the default rate stood at 0.32 percent in March 2009).

Loans collateralised by real estate assets in Romania consist of two categories:

-mortgage loans

-mortgage-backed consumer loans Table 3. Loans collateralised by real

estate assets in Romania in 2009 % Romania EU Total, of witch: 100 100 I. Mortgage loans 42 71 II. Mortgage-backed consumer loans 58 29

Source: NBR, Financial stability report, Bucharest, 2009.

I.Mortgage loans hold a low share in total household credit, i.e. 21.7 percent as of January 2009). Compared to other EU countries, Romania’s situation is strongly atypical, which could currently prove beneficial to financial stability if conditions on the real estate market deteriorated further. As a matter of fact, the consequences of this risk materialising might be less severe than in other Member States, because the intentions to purchase a dwelling within the next 12 months – albeit on a downtrend – have stood above the EU average since the beginning of 2009.

The mortgage loans represent 42 percent of total (as of March 2009). The number of mortgage-backed loans in Romania is subdued (around 0.3 million of 7.6 million loans to households) with an average value of about EUR 38,000. Mortgage loans account for 71 percent of total household credit in the euro area as of December 2008.

II. Mortgage-backed consumer loans have seen their share rise to 36.7 percent of consumer credit as of March 2009, with the related risk heightening as well.

Mortgage-backed consumer loans represent 58 percent of total (March

2009). These loans do not have a precise destination, as they are either consumption-oriented or real estate investment oriented.

The default rate has multiplied almost ten times since December 2007, but its level remains modest (0.42 percent as of March 2009).

5. Conclusions

In the banks’ opinion, the real estate sector, followed by construction, witnessed the most visible deterioration in credit risk over the past year.

Atypical, in Romania, although risks stemming from real estate lending have been on the rise, there are elements offsetting the negative influence.

I. Major risk factors are:

(i) the large share in company funding of loans having real estate assets as collateral (adverse developments in the value of this collateral could deteriorate the quality of banks’ portfolio);

(ii) a sharp uptrend in the default rate (albeit from a low initial level);

(iii) banks’ large exposure to real estate and construction companies.

II. Risk mitigating factors include: (i) the subdued weight (compared to other EU countries) of mortgage credit to households in banks’ portfolio;

(ii) the fairly prudent level of the loan-to-value ratio;

(iii) the relatively small drop in households’ intention to purchase a real estate asset over the upcoming 12 months.

But, the main long-run consequence of the real estate crisis could be a decline in consumer and local business confidence, and another, possibly worldwide, recession.

REFERENCES Claessens, S.,

Kose, A., Terrones, M., (2008)

“What Happens During Recessions, Crunches and Busts”, IMF

Working 08/274, December; Robert J. Shiller

(2005

Irrational Exuberance, Second Edition, Princeton University Press's; Bank for

International Settlements (2009)

79th Annual Report, 1 April 2008– 31 March 2009, Basel, 29 June

2009; Business Monitor

International Romania (2009)

Real Estate Report Published: July 15 2009 Quarterly; Colliers

International (2009) Romania 2009,

Real estate Review;

Global Property Guide. (2008)

The end of the global house price boom

http://www.globalpropertyguide.com/press-relations/; Global Property

Guide. (2009)

House Prices Worldwide

http://www.globalpropertyguide.com/real-estate-house-prices/A; International

Monetary Fund (2009)

World Economic Outlook Sustaining the Recovery, October 2009, http://www.imf.org;

National Bank of Romania (2009)