Performance Based Budgeting

and

Performance Based Costing

By

Lieutenant General Tome H. Walters, Jr., USAF

Defense Security Cooperation Agency

Introduction

In its lead article of December 15, 2000, the Federal Financial Management News

indicated that, in the upcoming years, “performance-based government” would be a central element with the Congress and the new Bush administration. Two financial management initiatives are currently underway in the security cooperation community that will move us significantly in this direction. These two initiatives are performance based budgeting (PBB) and performance based costing (PBC).

The key to both PBB and PBC is that they will give us the tools to understand where our foreign military sales (FMS) administrative budget dollars are currently spent and an opportunity to decide where they should be spent. Together with a new resource allocation process to work trade-offs, PBB and PBC will significantly improve FMS financial management. Performance based budgeting provides us with a multi-year process that links budgets to corporate strategy, planning, performance measures, and program execution. It will permit us to take the initiative with the Office of Management and Budget (OMB) and the Congress in explaining our basic program, as well as in requesting increases to the out year annual funding ceiling, if these are required.

Performance based costing is the natural complement to PBB. It would be shortsighted in the extreme to improve our FMS administrative budget process without simultaneously developing a better understanding of how the funds are actually spent. Performance based costing provides us with a costing infrastructure of the various organizations that receive FMS administrative funds. Inherent in this visibility is the ability to better account for our costs and improve program management. Significantly, it allows us to better explain our costs to our foreign customers who have often asked how the funds were spent.

While the Defense Security Cooperation Agency (DSCA) leadership recognized the need for implementing PBB and PBC, and championed these initiatives, major elements of PBB and PBC originated in the military departments (MILDEPs). For sometime, both the Army and Navy have cross-walked their traditional object class budgets to categories that better explain annual budgets on a program basis. Similarly, the Air Force and Navy Inventory Control Point (NAVICP) were early pioneers in costing initiatives that seek to improve cost information and operational data-each of which utilize activity based costing (ABC) models.

Background

For over three decades, the FMS trust fund has been run, by most accounts, on a solid financial basis. In recent years, the FMS administrative account has operated with healthy balances-sufficient to provide prudent increments to our annual budgets, while still reserving a margin for unforeseen adverse situations. At the same time as we have been fiscally sound, we have been informationally poor i.e., we have not had sufficient information to explain the

programs supported by our annual budgets, the results generated by these funds, or where precisely our costs are incurred.

This situation is no one’s fault. Essentially, it stems from the historical way security cooperation developed, particularly in two areas.

• First, the FMS administrative account is not appropriated by Congress. Obligation of

these funds is not required to conform to the Department of Defense planning, programming and budgeting system (PPBS) or the program objective memorandum (POM) cycle. As a consequence, we have not historically operated within a structure that links planning, programming, budgeting, and strategy to program execution.

• Second, we are required to fully recoup the costs of the FMS program as a pro rata

recovery applied to each sale. We have performed this mission successfully for over three decades. Operating on the basis of a pro rata recovery, however, has not forced us to do a bottoms-up analysis of our costs, nor provided us with needed insights into the types of activities on which our funds were being spent. This cost visibility is an essential element of what constitutes “best practices” today in both the private and public sectors.

It will come as a surprise to many people, including people in or own security cooperation community, that increases in sales through the FMS process do not automatically translate into increased FMS administrative budgets. Rather, a congressional ceiling that appears in the annual

Foreign Operations and Related Programs Appropriations Actcontrols our FMS administrative budgets. Whatever our sales levels, however, this requirement places a premium on our being able to articulate to Office of Management and Budget (OMB) and the Congress what programs our baseline budgeting is funding, what requirements are unfunded, and how, specifically, budgetary increases would be used. This situation came home to us as recently as November 1999 when the General Accounting Office (GAO) reported that, “the Department of Defense does not have sufficient information to determine the administrative costs associated with the FMS program.”

Additionally, the current emphasis in government accountability and reform has pushed us in

the direction of PBB and PBC. The Government Performance and Results Act (GPRA) of 1993

is meant to encourage a results, oriented culture of performance in government operations, and one that clearly links resources to programs and measurable results.

The culmination of these events prompted DSCA to work with the military departments to develop and implement a new budget process i.e., performance based budgeting (PBB). On November 8, 2000, a memorandum officially implementing the PBB process was signed. This was done in fiscal year 2001 and was used to develop the fiscal year 2002 operating budget and the fiscal year 2003 presidential budget (PB) request. The initial PBB cycle addresses the FMS administrative budget, but it is our intention to include the remaining funding sources, particularly the foreign military financing (FMF) administrative budget in the new planning and budgeting process over time. Also, implementation of PBB in the first year has focused on DSCA and the military departments. DSCA is aware that the first year of a new process is one of significant transition, and has spoken of fiscal year 2001 as a practice year to encourage an open and positive environment. Various points in fiscal year 2001 are intended to allow for assessment, feedback and adjustment to the PBB process.

Coupled with PBB, we have also embarked on a major project to create a cost infrastructure of our security cooperation organizations i.e., PBC. Beginning in the fall 2000, assessments were done of DSCA and the military departments to determine our current ability to track the costs of our FMS administrative program. Based on this assessment and recommendations for an

optimum cost environment, the DSCA director authorized the PBC project. In a memorandum dated March 30, 2001, I indicated that my target was to have 80 percent of the cost infrastructure mapped over a twenty-four month period through April 2003. This would allow the PBB process to use actual cost data in developing the fiscal year 2004 budget.

PBB Core Functions

One of the more significant changes of the new PBB process was to realign our requirements from solely an object class basis, salaries, travel, contracts, etc., to one that attempts to capture expenditures in program-like categories. Accordingly, the PBB process is built around six FMS core functions that were developed collaboratively with the military departments and DSCA. The core functions essentially parallel our FMS business life cycle, and thereby allow us to budget and collect cost in major program areas. The six core functions have been progressively broken down into several sub-functions, which in turn will be broken down into discrete activities in our PBC models. The core functions serve as a bridge that transforms our traditional-somewhat static-budget outlook from one of discrete lines of expenditure to a more programmatic outlook. Performance measures are a natural adjunct to the core functions. These measures will help us assess how well we are doing in executing the budget, and the results we are getting for our budgeted dollars. Figure 1 provides an overview of the six FMS core functions and a complete breakdown can be obtained from the PBB website. http://www.dsca.osd.mil/_vti_script/ SEARCH.htm0.idq.

Figure 1 Core Functions Core Function Definition

Pre-Letter of Request (LOR) Efforts expended prior to receipt of a LOR, includes responding to inquiries, pre-requirements determination, developing a total package approach (TPA), if required, or specifying the mix of FMS and direct commercial sales (DCS) under a hybrid approach. Case Development Efforts required to process customer request,gather, develop

and integrate price and availability data for preparation of a letter of offer and acceptance (LOA). These efforts continue from receipt of a customer’s LOR through case preparation, staffing and customer acceptance.

Case Execution Overall coordination to initiate case implementation efforts required to conduct and execute case management, security assistance, team management, technical, logistical, and financial support, and the contractual efforts under acquisition and contracting. Case Closure All actions required to perform logistical reconciliation, certify

line, and case closure.

Other Security Cooperation All efforts involved in the administration and management of special programs and projects associated with security cooper-ation requirements, particularly, the non-FMS security

cooperation programs authorized under the Foreign Assistance

Act, such as International Military Education and Training (IMET),

the foreign military financing (FMF) program, the grant

excess defense articles (EDA) program, and direct commercial sales.

Business Sustaining Efforts required in providing employee supervision, leadership, and guidance including personnel management, workload manage-ment, and secretarial support that cannot be traced directly to one of the other five core functions or specific cost objectives.

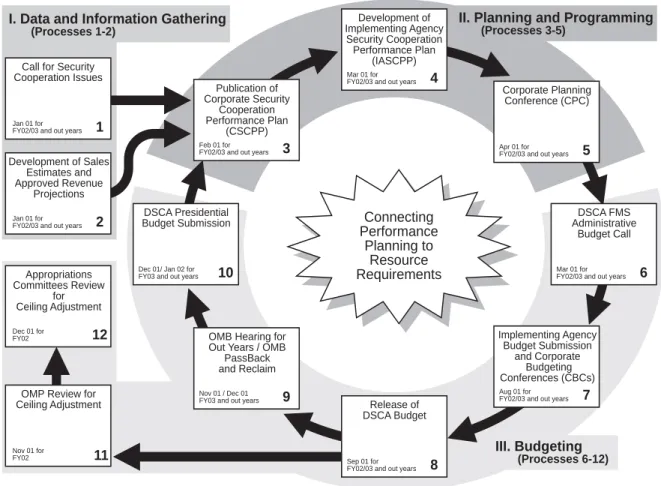

PBB Cycle

PBB is a twelve-step process built around three stages:

• Data and information gathering;

• Planning and programming; and

• Budgeting.

Emphasis was placed on integrating these stages into a coherent cycle of events. Each process in the cycle is designed to channel information in a way that links resources to program execution. The PBB cycle is a multi-year process that includes some of the key elements of the Department of Defense’s PPBS process. For example, on February 14, 2001, DSCA published its fiscal years 2002 and 2003 Budget and Programmatic Guidance. This guidance encapsulates the major issues and trends impacting the security cooperation community and sets the stage for the ongoing budget dialogue between DSCA and the military departments. “Fiscal Years 2002 and 2003

Budget and Programmatic Guidance” was highlighted in the spring issue of the DISAM Journal,

23:3, page 31 and can be obtained from the PBB website http://www.dsca.osd.mil/_vti_script/ SEARCH.htm0.idq. This document is analogous to the Defense Guidance, an integral part of the PPBS process. Figure 2 portrays the overview of the PBB cycle.

Call for Security Cooperation Issues

Jan 01 for

FY02/03 and out years 1

Development of Sales Estimates and Approved Revenue

Projections

Jan 01 for

FY02/03 and out years 2

Appropriations Committees Review for Ceiling Adjustment Dec 01 for FY02 12

OMP Review for Ceiling Adjustment Nov 01 for FY02 11 Development of Implementing Agency Security Cooperation Performance Plan (IASCPP) Mar 01 for

FY02/03 and out years 4

DSCA Presidential Budget Submission

Dec 01/ Jan 02 for FY03 and out years 10

Release of DSCA Budget

Sep 01 for

FY02/03 and out years 8

DSCA FMS Administrative

Budget Call

Mar 01 for

FY02/03 and out years 6

Publication of Corporate Security Cooperation Performance Plan (CSCPP) Feb 01 for

FY02/03 and out years 3

OMB Hearing for Out Years / OMB

PassBack and Reclaim

Nov 01 / Dec 01 FY03 and out years 9

Implementing Agency Budget Submission and Corporate Budgeting Conferences (CBCs) Aug 01 for

FY02/03 and out years 7

Corporate Planning Conference (CPC)

Apr 01 for

FY02/03 and out years 5

Connecting Performance Planning to Resource Requirements III. Budgeting (Processes 6-12)

II. Planning and Programming

(Processes 3-5)

I. Data and Information Gathering

(Processes 1-2)

• The first stage in the PBB cycle is data and information gathering. It includes the following process steps.

•• Call for security cooperation issues; and

•• Development of sales estimates and approved revenue projections. The purpose of this stage is to provide an opportunity for DSCA and the military departments to discuss internal and external issues important to the FMS environment as a whole. It is also the stage in which the fiscal environment for FMS in terms of sales and revenues is outlined in detail. It is within this overall environment that our budgetary estimates will take form.

• The second stage is planning and programming. This stage highlights the development of

goals and objectives for the upcoming fiscal year and out years. The development of these goals and objectives results from the dialogue that begins with the budget and programmatic guidance and culminates in the corporate programming conference process steps 3-5. The ultimate outcome of the planning and programming stage is a strategy for how DSCA and the military departments will allocate their resources. This stage, with its push for increased planning and collaboration, represents the most fundamental change to our historical budget practices.

• The third stage is budgeting and it comprises all of the other process steps. From issuance

of the FMS administrative budget call to allocation of resources. The significant change in the budgeting stage is in the increased emphasis on narrative and descriptive information to support the budget data. In addition, it is within this stage that DSCA requests information regarding performance measures. The performance measures were discussed and agreed upon by DSCA and the military departments in fall 2000.

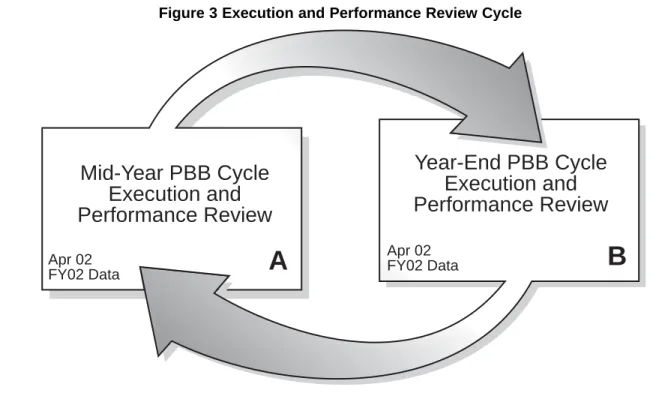

The PBB cycle also includes an execution and performance review process. The review process provides a mechanism for explicitly linking budgetary resources and performance measures, and for evaluating planned versus actual performance. Figure 3 addresses this aspect of the PBB cycle.

Year-End PBB Cycle

Execution and

Performance Review

Apr 02 FY02 DataB

Mid-Year PBB Cycle

Execution and

Performance Review

Apr 02 FY02 DataA

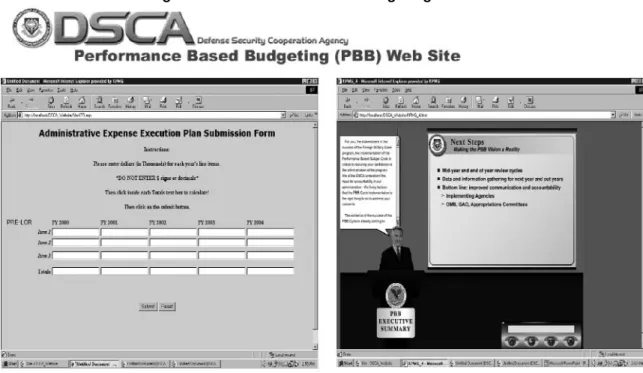

PBB Website

From the initial days of the PBB and PBC project, it was envisioned that both processes would utilize internet technology. In this regard, the web is an integral element of these processes and web technology is a key enabler of the PBB cycle in a manner that can optimize the new budgetary processes through automation. The PBB website has been operational since April 2001 and it has become the focal point for implementing the PBB cycle. The PBB website was used

to publish both fiscal years 2002 and 2003 Budget and Programmatic Guidance, and the results

of the PBB Corporate Programming Conference. In May 2001, the website was used to issue the fiscal years 2002 and 2003 FMS administrative budget call. The budget call was available for downloading by applicable persons in the security cooperation community a few hours after the memorandum was signed. In August 2001, the military departments successfully submitted their fiscal years 2002 and 2003 budget requirements via the PBB website. There is now a budget database that permits multiple levels of analysis in real time.

The PBB website is backed by a comprehensive E-Learning module that is integral to the website itself. The E-Learning module contains instruction for people at various levels involved in the budgetary process. Figure 4 contains screen shots of the PBB website.

Performance Based Costing

Performance based costing is designed to provide decision-makers at all levels in the security cooperation community with sufficient cost and programmatic information to manage their organizations. It will also help us to better understand macro-level aspects of our business, such as the costs structure underlying our FMS administrative rate, the appropriate level of the annual FMS administrative ceiling, and so forth.

The need to better understand the costs of conducting our security cooperation operations has been evident for some time. It is doubtful that we will be successful in adjusting our annual FMS administrative ceiling unless we are able to clearly articulate to the Congress what programs our baseline is funding. Similarly, our FMS customers have placed a priority on better understanding

what costs are included in their quarterly billings. Performance based costing provides an optimum method for gathering and understanding these costs. Performance based costing assigns resource costs to activities based on the use of resources, and assigns activity costs to products based on the use of activities. These activity costs can be rolled up to the six FMS core functions at various organizational levels. Over time, this visibility will focus management action on the cost of these activities and opportunities for improvement.

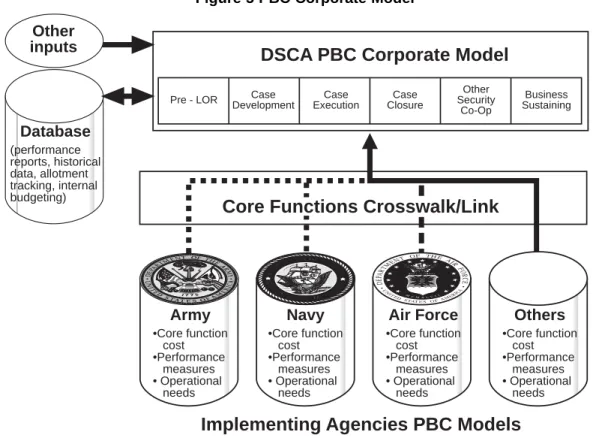

As background to the PBC effort now underway, initial assessments were done in the September 2000-February 2001 period of the existing costing infrastructure in DSCA and the military departments. The assessments were intended to show the organizational complexity of each entity; their existing cost model capability, and the role that cost data played in the budgetary process. Based on these assessments and other information, “to-be” cost models were developed. After a detailed briefing to the military departments and to the DSCA Director, it was decided to move towards these costs models. Figure 5 provides a high level schema of the PBC corporate model.

Conclusion

Performance based budgeting and performance based costing and a resource allocation process will transform major elements of security cooperation financial management. For the first time, we will have a planning framework that links our resources to shared goals and strategic objectives. We will be able to develop and monitor multi-year budgets, perform financial modeling and forecasting, and relate budgetary dollars to program execution. The PBC component will allow our organizations to determine and analyze the costs of key processes, activities and services. Appropriate performance measures will allow us to relate our planning to our actual execution. With an increased knowledge and understanding of the budget, performance levels, and goals, we will be equipped to make better decisions about security

Army •Core function cost •Performance measures • Operational needs Navy •Core function cost •Performance measures • Operational needs Air Force •Core function cost •Performance measures • Operational needs Others •Core function cost •Performance measures • Operational needs

Pre - LOR DevelopmentCase ExecutionCase ClosureCase SecurityOther Co-Op

Business Sustaining

DSCA PBC Corporate Model

Database (performance reports, historical data, allotment tracking, internal budgeting)

Core Functions Crosswalk/Link

Other inputs

Implementing Agencies PBC Models Figure 5 PBC Corporate Model

cooperation programs and activities and we will be better able to justify those decisions to all stakeholders.

About the Author

Lieutenant General Tome H. Walters, Jr., USAF is the Director of the Defense Security Cooperation Agency, Office of the Secretary of Defense. The general was born in Shreveport, Louisiana, and graduated from the U.S. Air Force Academy in 1970. He has served in command and staff positions at Air Force headquarters, the Joint Staff, Air Mobility Command, Air Training Command and Strategic Air Command. He commanded an air refueling squadron, a pilot training operations group and air refueling wing. He is a command pilot, having flown more than 3,500 hours in air refueling and trainer aircraft, including 100 combat support sorties in Southeast Asia.