On the competitive effects of mobile virtual network operators

Philip Kalmus

a, Lars Wiethaus

b,,1a

LECG Ltd, London, UK b

ESMT Competition Analysis, Berlin, Germany

a r t i c l e

i n f o

JEL classification: L13 L42 L96 Keywords: Competition Mobile telecommunication MVNO Regulationa b s t r a c t

Mobile virtual network operators (MVNOs) offer mobile telecoms services by purchasing capacity from mobile network operators (MNOs) and competing with the latter at the retail level. This paper employs a two stage model and analyses to what extent MVNOs may exert a competitive constraint on MNOs. In the first stage MNOs determine both their wholesale and retail capacities. In the second stage MNOs and MVNOs compete in the retail market. It is found that MNOs host MVNOs if and only if the latter do not exert a competitive constraint on MNOs’ retail businesses. Thus, absent access regulation, MVNO entry may happen but is unlikely to reduce consumer prices. The results do not depend upon the scarcity of capacity.

&2010 Elsevier Ltd. All rights reserved.

1. Introduction

‘‘Mobile Virtual Network Operators (MVNOs) offer mobile telecoms services to customers by purchasing capacity or wholesale minutes from a Mobile Network Operator (MNO) and selling it under their own brand to end-customers. In this way, MVNOs avoid the need to own and operate their own end-to-end mobile radio access networks. The number of MVNOs in Europe has increased substantially over the last three years, with seven new operators launching in the UK alone over this period. Many wellknown consumer brands have launched services, or have publicly announced their intent to enter the market’’ (Ofcom, 2006, p. 76).

MVNOs are interesting both from a regulatory and a competition policy perspective. TheEuropean Commission (2006)

has considered MVNO entry as a remedy for unsatisfying market performance. Yet, in light of numerous commercial agreements between MVNOs and MNOs, theEuropean Commission (2007)removed the market for wholesale access to mobile networks (market 15) from the list of markets to be looked into by national regulatory authorities. In the proposed takeover of Portugal Telecom through Sonaecom, MVNO entry was discussed as a remedy for the loss of one MNO in the Portuguese market for mobile communication.2These proceedings raise the question under what circumstances MVNOs

may exert a competitive constraint on MNOs. Of course, regulated access prices may well allow MVNOs to constrain MNOs.3However, whether MVNOs are also able to exert a competitive constraint on MNOs if access conditions are left to commercial negotiations is a different question.

Contents lists available atScienceDirect

URL:www.elsevierbusinessandmanagement.com/locate/telpol

Telecommunications Policy

0308-5961/$ - see front matter&2010 Elsevier Ltd. All rights reserved. doi:10.1016/j.telpol.2010.04.002

Corresponding author.

E-mail addresses:[email protected] (P. Kalmus), [email protected], [email protected] (L. Wiethaus). 1The work contained in this paper was conducted when the author was a consultant with LECG Ltd., London. 2

SeeAutoridade da Concorrencia (2006). 3

Kim and Seol (2007) review MVNO access regimes and estimate the competitive impact of mandated MVNO entry into the Korean telecommunications sector.

Indeed, the question of whether MVNOs exert a competitive constraint on MNOs bears no obvious answer. One might conjecture that an increased number of operators at the retail level increases competitive intensity and reduces prices for end-customers. MNOs might refuse to offer wholesale capacity to MVNOs for this reason. Yet, the threat that one’s rival might offer capacity rather than oneself could create a prisoners’ dilemma of hosting MVNOs and induce competition in the retail market.

This paper offers a simple analytical framework to shed some light on these questions, employing a two-stage Cournot model with endogenous wholesale price determination. In the first stage two MNOs decide how much capacity they allocate both for their retail business and their wholesale supply. Wholesale capacity is a homogeneous product, i.e. operators’ networks do not differ in scope and connection quality. In the second stage MVNOs decide how much capacity to purchase from MNOs whilst MVNOs and MNOs compete in the retail market. Retail services are differentiated.

The findings suggest that the mere introduction of MVNOs does not increase the intensity of competition in the retail market. Consumer prices do not decrease, irrespective of the number of MVNOs and the degree of service differentiation. The reason is that MNOs choose wholesale capacities sufficiently low, such that MVNOs’ retail services do not compromise MNOs’ own retail business. In the extreme, if MVNOs’ services are a perfect substitute to the MNOs’ services, the latter offer no wholesale capacity at all. If MVNOs’ services are differentiated from those of MNOs’, MNOs will offer a limited amount of wholesale capacity to MVNOs. Yet in this case service differentiation secures stable retail prices for MNOs.

Brito and Pereira (2008), too, analyse competitive effects of MVNOs.4 They assume Bertrand rather than Cournot

competition. Consistent to the present paper, they establish a wide parameter space in which MVNOs will not exert a competitive constraint on network operators. Unlike in the present study they also identify cases in which MNOs face a prisoner’s dilemma of hosting a MVNO, so that the latter may decrease retail prices. The successive duopoly set-up chosen in this paper presumes that multiple MVNOs are price takers visa vis MNOs. This assumption keeps the analysis simple but

ignores possible stronger bargaining power of MVNOs. Brito and Pereira’s set-up, in contrast, supposes a single MVNO, having strong bargaining power. The stronger position of the MVNO likely explains different results (rather than price versus quantity competition, per se). Very much in the vein of theBrito and Pereira (2008)framework,Ordover and Shaffer (2007)allow for the MVNO selecting its position opportunistically so as to harm primarily its own host. As a consequence

Ordover and Shaffer (2007)established more cases in which MNOs grant no access to MVNOs.

Armstrong (2006)reviews the theory of access pricing and interconnection. This literature, however, is distinct from the present approach as it either considers one-way access through a monopolist or two-way access in which each operator relies on its competitor’s access.Foros, Hansen, and Sand (2002)argue that MVNO entry increases welfare if, subsequently, MNOs jointly invest in infrastructure. They do not discuss whether MVNOs increase competition as such. Assuming Cournot competition,Dewenter and Haucap (2006)find that MNOs grant access to their networks even if MVNOs’ services are not at all differentiated from MNOs services. The assumption driving their result is that MNOs can extract the entire surplus from MVNOs and, given MVNOs’ output quantities, MNOs maximize profits through the number of MVNOs. Their analysis hence abstracts from the problem of double marginalisation and the result resembles the findings on divisionalisation under Cournot competition (Baye, Crocker, & Ju, 1996; Corchon, 1991; Polaski, 1992). Under similar assumptions they also show that MNOs are less likely to grant access under Bertrand and Stackelberg competition.

This paper is also related to the literature on successive oligopolies and vertical mergers (Greenhut & Ohta, 1979).

Salinger (1988) analyses how retail prices change if vertical integration among a fixed number of upstream and downstream firms changes. This paper differs in considering retail price changes, holding the number of integrated firms constant (at two), and varying the number of non-integrated downstream competitors. Within a successive duopoly frameworkOrdover, Saloner, and Salop (1990)analyse incentives for vertical integration and vertical foreclosure.5In their

model, due to lack of own retail facilities, the integrated upstream firm will always have an incentive to supply non-integrated downstream firms. In the present model each upstream firm is vertically non-integrated which tends to lower upstream supply and competition from downstream entry. McAfee (1999) and Economides (2005)analyse upstream integration in a bilateral duopoly. Their settings, however, do not involve non-integrated downstream firms relying solely on integrated firms’ supply.Boots, Rijkers, and Hobbs (2004)apply a successive oligopoly approach to the European natural gas market. In this market, (upstream) producers supply gas to (downstream) traders who compete in the market for end-customers. This structure is similar to MNOs supplying capacity to MVNOs who sell minutes in the retail market. Their model yields results that are consistent with ours. The model of this paper differs, however, as not only non-integrated downstream suppliers (MVNOs) compete in the retail market but also integrated upstream suppliers (MNOs).

Empirical evidence on the competitive effects of MVNOs telecommunication markets is scarce and inconclusive. In a report commissioned by the Israel Ministry of Communications and Ministry of Finance, Attenbourough, Dippon, and Sorensen (2007)provide case studies on the effects of MVNO entry in various international markets. By and large the authors do not attribute substantial price reductions to MVNOs. In particular they conclude that ‘‘MVNOs tend to serve previously unserved market segments rather than competing with MNOs, and they deepen and widen the market.

y[They] are complementing, rather than competing with, the MNOs’ offerings.’’ (p. 74). These conclusions are consistent

4

In their most recent version of their working paper they do not refer explicitly to a MNO–MVNO setting anymore. 5

The model ofOrdover et al. (1990)also differs in proposing Bertrand competition upstream and differentiated price competition downstream rather than successive quantity competition.

with this model’s predictions. The European Regulators Group (ERG, 2006) reports national regulatory authorities’ views on whether MVNOs had an effect on competition. The anecdotal evidence is mixed. Countries such as Belgium, Estonia, Sweden, France and Germany did not report strong competitive effects from MVNOs, whereas Denmark, Finland, The Netherlands and Sweden did. Indeed, as pointed out by the ERG, observed (and non-observed) competitive effects might be due to many other reasons. This renders an econometric study that controls for factors such as mobile penetration and regulatory pressure highly desirable, disentangling the competitive effects caused by MVNOs from those caused by other factors.6

The paper is organized as follows. Section 2 presents the model and comparative statics results. Section 3 concludes and provides suggestions for future research.

2. The model

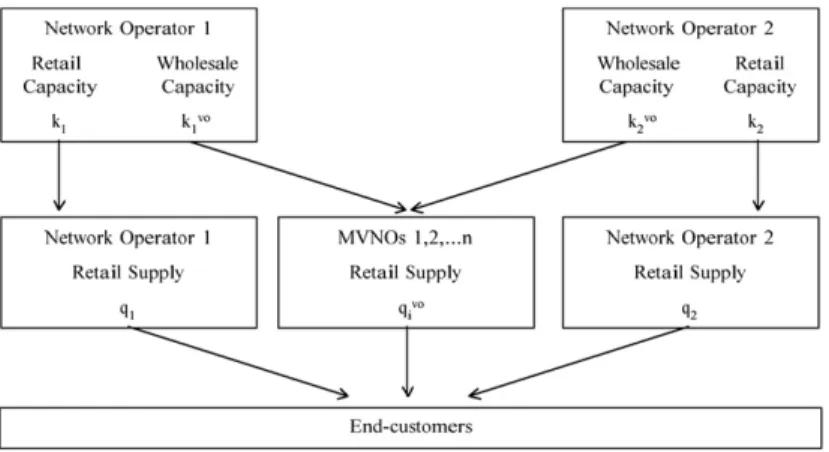

Consider a market for mobile telecommunication services with two MNOs,i= 1,2, andnmobile virtual MNOs (MVNOs),

vo¼1,2,. . .,n. MNOs and MVNOs compete for end-costumers in quantities,qiandqvo. Quantitiesqiandqvoare the amount

of voice minutes supplied to end-customers.7 Prior to quantity competition at the retail stage, MNOs simultaneously

determine infrastructure capacity alongside two dimensions. First they build up capacity,ki, to satisfy their intended own

retail supply,qi. Second MNOs expand infrastructure capacity,kivoto compete with each other in the supply of wholesale

minutes for MVNOs (seeFig. 1).

It is assumed that there exists a direct and trivial relationship between infrastructure capacity,kiandkivo, and output

quantities (voice minutes),qiandqivo, of the formkiqiandkvoi qvoi . One unit of infrastructure capacity relates to one unit

of output quantity. Capacity refers to base stations, glass fibre cables, microwave transmitters and additional transmission equipment rather than to radio spectrum. While the amount of the latter might be fixed and excessive even in the longer run, the former has to be adjusted regarding actual mobile traffic. Costs of capacity take the following linear form:

Ci(ki,kivo) =c(ki+kivo). If lumpy investments result in non-utilized capacity,c= 0 and MNOs only determine the amount of

wholesale capacity,kivo.

The demand for capacity by MVNOs is derived from the MVNO’s maximization problem in the second stage. In the second stage, given capacity installed in the first stage, the MNOs and the MVNO supplyqiand qvominutes of mobile

communication services to end-customers. For simplicity, operating costs are neglected at the retail level. In the second stage, only the MVNO bears costs in terms of purchasing capacity from the MNOs at the wholesale pricew.8

At the retail level, thei’th MNO faces a linear inverse demand function:

Pi¼aqiqj

g

Xvo

qvo, i¼1,2, iaj, ð1Þ

Fig. 1.Mobile communication industry structure with network operators and MVNOs.

6

No econometric study on the competitive effects of MVNOs has been undertaken so far. YetHastings and Gilbert (2005)carried out an econometric study of wholesale pricing of vertically integrated gasoline refiners in the U.S. They found higher wholesale prices for independent gasoline retailers in regions close to refiner-retailers. In the present context this translates into MNOs setting higher wholesale prices the less differentiated MVNOs’ services. To that end the econometric evidence is consistent with the theory presented here in that less service differentiation between the MNO and the MVNO results in less (equilibrium) wholesale supply.

7Here, Cournot competition is considered as an approximation for imperfect competition in the market for mobile call origination.Parker and R ¨oller (1997)confirm the appropriateness of this simplification empirically.Foros et al. (2002),Wright (2002)and,Dewenter and Haucap (2006)likewise consider quantity competition as an appropriate approximation for mobile markets.

8

AsOfcom (2006, p. 78)states it is essentially this cost-asymmetry that distinguishes a MVNO from a network operator: ‘‘MVNOs can avoid many of the fixed costs incurred by MNOs such as spectrum licenses, network infrastructure, and platforms for new services.. . .However, since MVNOs pay out a large proportion of their revenues in fixed-agreement wholesale fees to network operators, their operating margins are far lower than those of MNOs.’’

wherea4cis the reservation price and

g

, 0rg

r1,measures the degree of service substitutability between thei’th MNO’s service and MVNOs’ services from the end-customers point of view. In particular a low value forg

means that the MVNOs’ services do not constitute a close substitute toi’s service, whereas a high value refers to a high degree of substitutability. Different degrees of substitutability may reflect, for instance, customers’ preferences for certain types of pricing, marketing or brand image. Also a low value forg

could be interpreted that the MVNO targets customer segments through specific distribution channels which are (a) not available to the MNOs and (b) attractive to the MVNO’s customer segment. For example, supermarket MVNOs (e.g. Tesco) may attract unique customer segments. Belgium MVNO ‘‘Ay Yildiz’ with a Turkish language website is another example of low substitutability between MNO and MVNO. In order to focus on the impact of the substitution parameter on the hosting decision, it is assumed that end-customers consider MNOs’ services as perfect substitutes (i.e. a substitutability parameter of value one). MNOs serve the (same) mass market.The corresponding inverse demand function facing the MVNOs can be written as

Pvo¼a

g

ðqiþqjÞ Xvo

qvo, vo¼1,. . .,n: ð2Þ

The MNOs’ profit functions take the form

p

i¼Piqi Retail revenues þwX vo kvo i Wholesale revenues c kiþ X vo kvo i ! Costs of capacity , i¼1,2, ð3ÞwherePiis given by (1). As displayed by (3) the MNOs’ profits consist of revenues through their retail activity as well as

through their wholesale activity. In order to generate revenues in the retail market and in the wholesale market, capacity in terms of infrastructure is required.

The MVNO’s profit function is

p

vo¼Pvoqvo Retail revenues wqvo Costs of wholesale minutes , vo¼1,. . .,n, ð4ÞwherePvois given by (2). A comparison of (4) with (3) highlights the main differences between the MVNO and MNO

business models. First, MNOs generate revenues through both the retail and the wholesale markets; whereas the MVNO only operates at the retail level. Second, MNOs have lower marginal costs at the retail level, i.e. no wholesale pricew, whereas MVNOs do not have to incur capacity (infrastructure) costs.

Firms’ decisions within the above outlined two stage competition process are analysed in turn, proceeding backwards. That is, first, firms’ equilibrium output quantities at the retail level are derived. With these results at hand, second, MNOs’ equilibrium capacity instalments are determined.

2.1. Competition at the retail level (2nd stage analysis)

At the retail level the MNOs,i,i=1,2, and the MVNOs,vo,vo¼1,. . .,n, simultaneously compete in quantities. As will be clear below, however, the two stage game in which MNOs first set capacities and then engage in Cournot competition at the retail level reduces to one in which MNOs set capacities and output quantities in the first stage (as Stackelberg leaders), whereas the MVNOs set output quantities in the second stage (as Stackelberg followers). The reason is the asymmetric cost structure of MNOs and MVNOs where MNOs incur costs of capacity, if any, in the first stage but have no such costs at the second stage (retail level). In contrast, MVNOs have operating costs in the second stage equal to the wholesale price set by the MNOs.

To start, assume that, in the second stage, there are no capacity constraints at all. Then MNOs and MVNOs would maximize (3) and (4) with respect toqiandqvoleading to,

q i ¼ að1þnð1

g

ÞÞ þng

w 3þnð32g

2Þ , i¼1,2 ð5Þ and q vo¼ að32g

Þ3w 3þnð32g

2Þ, vo¼1,. . .;n, ð6Þwhereqi*andqvo* denote the (hypothetical) 2nd stage Nash equilibrium in the absence of capacity constraints.

Next consider capacity constraints and distinguish the following cases: I:q

ioki, i¼1,2,

II:q

iZki, i¼1,2:

In case I, capacity constraints are non-binding and MNOs set quantities according to (5). In case II, capacity constraints are binding and MNOs have to supply less thanqi*. In fact it is optimal for them to supplykiin this case.9

9

Note that profit functions are strictly concave inqi, i.e.@2pi=@qi2¼ co0. Hence for anyqioqithe first-order-condition to the network operators’ second stage maximization problem are positive.

In case I, the MVNO sets its output quantity according to (6). In case II, the MVNO knows that the MNOs setkioqi.

Given this it is optimal for the MVNOs to maximize

p

0 vo¼ ag

ðkiþkjÞ X vo qvo ! qvowqvo, vo¼1,. . .n ð7Þwith respect toqvoleading to

qr vo¼

a

g

ðkiþkjÞwðnþ1Þ , vo¼1,. . .n ð8Þ

whereqvor denotes the MVNOs optimal response as a function of the MNOs capacities,ki,i=1,2.

To determine the second stage Nash equilibrium it thus crucial to know whether case I or case II holds in stage 2. If it is case I then firms play (qi*,qj*,q*vo) in the second stage, whereas in case II firms play (ki,kj,qvor ). Yet it is easy to see that case I

would not constitute a subgame perfect Nash equilibrium of the first stage because this would leave thei’th firm with unused but costly capacity (seeDixit, 1980). Rather thei’th firm could profitably reduce its capacity which is true as long as case I holds. Thus case II must hold in stage 2. If capacity is not costly in the first stage, c= 0, then MNOs could still determine how much of their capacity they offer in the wholesale market,kivo,i=1,2.10

Given case II one can derive the MVNO’s demand curve for wholesale minutes using (8). Keeping in mind the assumption that one output unit q requires one unit of capacity k and hence that the supply of qvor requires that

qr

voZkvoi þkvoj ,one obtains

w¼a

g

ðkiþkjÞðnþ1Þðkvoi þkvoj Þ, ð9Þwherewis the wholesale price that clears the wholesale market, given the MNOs’ supply ofn(kivo+kjvo).

2.2. Capacity competition (1st stage analysis)

Upon substitution ofkiforqiand (kivo+kjvo) forqvoin (3) and (1) thei’th MNOs first stage profit function can be written as

p

i¼Pikiþwk vo i cðkiþnk vo i Þ, i¼1,2, iaj, ð10Þ where Pi¼akikjng

ðkvoi þkvoj Þ, i¼1,2 iaj: ð11ÞThe MNOs maximize their objective function with respect tokiandkivo. The first-order-conditions are

@

p

i @ki ¼a2kikjng

ð2kvoi þkvoj Þc¼0, i¼1,2, iaj ð12Þ and @p

i @kvo i ¼nðaðnþ1Þð2kvo i þk vo j Þg

ð2kiþkjÞcÞ ¼0, i¼1,2, iaj: ð13ÞSolving (12) and (13 ) simultaneously forkiandkivo,i=1,2, yields the (unique) subgame perfect Nash equilibrium in the

MNOs’ capacity strategies:

k i¼ ðacÞð1þ ð1

g

ÞnÞ 3þ3ð1g

2Þn , i¼1,2 ð14Þ and kvo i ¼ ðacÞð1g

Þ 3þ3ð1g

2Þn, i¼1,2: ð15ÞAn immediate implication from (15) is the following

Claim 1. If MVNOs’services constitute a perfect substitute to MNOs’services,i.e.

g

¼1,the MNOs do not offer wholesale minutes to the MVNO,kivo=0,i= 1,2.MNOs have no incentive to offer wholesale capacity to MVNOs as long as MVNOs offer services which are undifferentiated from those of the MNOs. An alternative interpretation of this result is that MNOs would set their wholesale price prohibitively high such that no wholesale minutes would be demanded. Notably this result does not depend upon the cost of capacity,c. Even if there is idle capacity,c=0, MNOs would not compromise their own retail

10

The remaining question is just whether there exists a closed form solution to the network operators’ first stage maximization problem,ki*, such that

k

irqi or, else, that the closed loop solution implieski4qi. It will be seen below (see footnote 10) that the closed form solution to the first stage maximization problem,ki*, indeed satisfieskirqi.

profits through competitive MVNOs. Accordingly one would not expect MVNOs to offer a perfect substitute to the MNOs’ services.

2.3. Comparative statics

Equilibrium capacities: Consider how MNOs’ supply capacities change in the degree of service substitutability. The derivation of (14) and (15) with respect to

g

yields@k i @

g

¼ ðacÞnð1þnð1g

Þ22g

Þ 3ð1þ ð1þg

2ÞnÞ2 w0, i¼1,2, ð16Þ and @kvo i @g

¼ ðacÞð1þnð1g

Þ2Þ 3ð1þ ð1þg

2ÞnÞ2o0, i¼1,2: ð17ÞEqs. (16) and (17) lead to

Claim 2. (a)A higher degree of service substitutability,

g

,decreases(increases)MNOs’supply in the retail market,ki*,if theproduct substitutability is low(high).

(b)A higher degree of service substitutability,

g

,decreases MNOs’ supply in the wholesale market,kvoi . Proof. First claim: Eq. (16) is negative iff 1þnð1

g

Þ22g

40. Second claim: obvious by (17). &Higher service substitutability has an ambiguous effect on MNOs own retail capacity. As a direct effect, higher service substitutability leads the MNO to decrease retail capacity because it increases retail competition and, hence, lowers marginal returns from additional capacity. As an indirect effect, higher service substitutability results in less wholesale supply (see below) and thereby decreases competitive intensity in the retail market. According to claim (a), the direct effect dominates if service substitutability is low whilst the indirect effect dominates if product substitutability is high. As regards MNOs’ incentives to supply wholesale capacity, claim (b) confirms the intuition developed in the previous section: MNOs offer more capacity in the wholesale market when MVNO’s services are differentiated at the retail level.

Next consider the change in the MNOs’ capacities due to a change in the number of MVNOs. The derivation of (14) andn

times (15) with respect tonyields

@k i @n ¼ ðacÞð1

g

Þg

3ð1þ ð1þg

2ÞnÞ2r0, i¼1,2, ð18Þ and @nkvoi @n ¼ ðacÞð1g

Þ 3ð1þ ð1þg

2ÞnÞ2Z0, i¼1,2: ð19ÞEqs. (18) and (19) imply the following:

Claim 3. If the number of MVNOs increases,MNOs reduce their own retail supply and increase their wholesale supply. The intuition behind Claim 3 is that the effect of double marginalisation decreases if the number of MVNOs increases. MVNOs become more competitive, lower their retail price to the competitive level (i.e. at the level of the wholesale price), and hence, ceteris paribus, wholesale offers become more attractive for the MNOs as they can capture (more of) the complete margin themselves or, respectively, can increase output with less distortions of the retail price.

Equilibrium retail prices: Upon substitution of (14) and (15) in (11) one obtains MNOs’ retail prices:

Pi¼aðkiþkjÞ

g

nðkvo

i þkvo

j Þ ¼13ðaþ2cÞ, ð20Þ

and substitution of (14) and (15) forqi,qjandqvo,whereqvo¼kv

i þkv

j , in (2) gives the MVNO’s retail prices:

Pvo¼a

g

ðkiþkjÞnðkvo i þkvo j Þ ¼ 2cðg

þnð1þg

2ÞÞ það3þ2g

þnð1g

2ÞÞ 3þ3ð1þg

2Þn , ð21Þ where lim n!1Pvo¼ 1 3ðaþ2cÞ:Eqs. (20) and (21) imply the following

Claim 4. (a)The MNOs’equilibrium retail prices are constant in the degree of service substitutability and the number of MVNOs.

(b)The MVNOs’retail price is decreasing in the degree of service substitutability and the number of MVNOs in the market.

Proof. (a) is obvious. For (b), note that the derivative of (21) with respect to

g

,@Pvo=@g

¼ ðacÞð22g

þg

2Þ=ð2þg

2Þ2o0The fact that the MVNOs’ retail price decreases in the degree of service substitutability to the MNOs is not surprising. The less the MVNO manages to target distinct customer segments, say due to specific tariff plans or unique distribution channels, the more it competes directly with the service operators. Therefore the more intense is the competition and the lower its retail prices. Also not surprisingly, the MVNOs retail price decreases in the number of MVNOs and approaches the wholesale price level (22) if the MVNO segment becomes perfectly competitive (i.e.n!1).

In contrast, MNOs’ retail prices remain constant in the degree of service substitutability. Even if MNOs supplied capacity to a (differentiated) MVNO, prices for MNOs’ end-customers remain as high as if there would be no MVNO at all. In other words MNOs support MVNOs as long as the latter do not exert competitive pressure on the former.

Equilibrium wholesale prices: Substitution of (14) and (15) into (9) yields the wholesale price determined by the MNOs’ equilibrium retail and wholesale supply,ki*andkv

i : wðk i,k v i Þ ¼a

g

ðk iþk jÞðnþ1Þðk v i þk v j Þ ¼13ðaþ2cÞ: ð22ÞClaim 5. The equilibrium wholesale price,wðk

i,kv

i Þ,is equal to the MNOs’retail prices and hence constant in the number of

MVNOs,n,and the degree of service substitutability,

g

.The intuition behind Claim 5 is that MNOs strictly prefer allocating capacity to that business, wholesale or retail, that yields higher returns in terms of higher prices. Hence as long asw4Pi, MNOs would only install wholesale capacity,

whereas, ifwoPi, MNOs would only install retail capacity. In any equilibrium with positive wholesale and retail capacities

the wholesale and the retail price must be equal.11That said, in reality one may well observe wholesale prices being lower

than retail prices. This is because the simple model ignores distribution costs. With distribution costs one would have that wholesale prices should equal retail prices net of distribution costs; i.e. one observes wholesale prices lower than retail prices.

3. Conclusion

This paper clarifies several effects related to the introduction of MVNOs. In the simple model, absent access regulation, MVNOs do not exert a competitive constraint on MNOs. MVNOs that have similar business plans to MNOs are rejected by them. MVNOs with differentiated business plans do not exert competitive pressure on them. MNOs make sure that they balance their wholesale offer finely with the degree of substitutability of the MVNOs business model.

Notwithstanding the limitations of a stylized and simplified model the analysis may provide some guidance for practitioners. First, successful MNO–MVNO business relationships appear to hinge on MVNOs’ superior access to certain customer segments. Without such access either the MNO or the MVNO incurs some opportunity losses. Second, regulators may not expect MVNOs, as such, to stimulate competition in mobile communication markets. By the same token, third, a simple pledge of hosting MVNOs may turn into a poor remedy for MNO mergers. It appears likely that competition authorities and regulators would need to determine access conditions if they aim at to increase competition.

As mentioned in the introduction, in light of the alternative approaches byBrito and Pereira (2008)andOrdover and Shaffer (2007)the analysis of MVNO access seems to hinge on the (implicit) assumptions on the underlying bargaining power of MNOs and MVNOs. Future research should address parties’ bargaining power more explicitly. The present analysis, for example, could be extended through a preliminary (Nash-) bargaining stage whereby parties’ bargaining powers depend on the number of MNOs and MVNOs as well as the extent of MNOs’ excess capacity. A further extension regards potential upstream integration by MVNOs. While MVNOs may enter with little or no infrastructure, they could develop their own infrastructure over time and reduce their dependency on MNOs. This might increase the competitive pressure they impose on MNOs, but on the other hand decrease the likelihood of obtaining favorable access conditions in the first place.

11

It remains to be shown thatq

iZki. By (5), (14) and (22) this amounts to showing that

að1þnð1gÞÞ þngw 3þnð32g2Þ Z ðacÞð1þ ð1gÞnÞ 3þ3nð1g2Þ , where w¼1 3ðaþ2cÞ:

Substitution forwand rearranging terms gives

ð1þnÞ½að1þgÞgnþcð3þ ð3þgþ2g 2ÞÞn 3ð1þ ð1þg2ÞnÞð3þ ð3þ2g2ÞnÞ Z0

Acknowledgements

The paper benefited substantially from discussions with Matthew Bennett. Moreover, thanks to Nuno Ruiz and Len Waverman for useful suggestions. Thanks are also due to participants of the annual conference of the European Association of Research in Industrial Organization (EARIE) 2007. Two anonymous referees and the editor, Warren Kimble, provided very useful comments. Financial support from Portugal Telecom is gratefully acknowledged.

References

Autoridade da Concorrencia (2006).Portuguese competition authority clears Sonaecom/PT merger—with conditions and obligations attached. Press Release No. 28/2006.

Armstrong, M. (2006). The theory of access pricing and interconnection. In M. E. Cave, S. K. Majumdar, & I. Vogelsang (Eds.), Handbook of telecommunications economics, Vol. 1 (pp. 297–384). Amsterdam: North-Holland.

Attenbourough, N., Dippon, C., & Sorensen, S. (2007).Mobile virtual network operators (MVNOs) in Israel. Report Prepared for the State of Israel, Ministry of Communications and Ministry of Finance.

Baye, M., Crocker, K., & Ju, J. (1996). Divisionalization, franchising, and divestiture incentives in oligopoly.American Economic Review,86, 223–236. Boots, G. M., Rijkers, F. A.M., & Hobbs, B. F. (2004). Trading in the downstream European gas market: A successive oligopoly approach.Energy Journal,25,

73–102.

Brito, D., & Pereira, P. (2008).Access to bottleneck inputs under oligopoly: A prisoners’ dilemma? Working Paper no 16, Autoridade da Concorrencia. Corchon, L. (1991). Oligopolistic competiton among groups.Economics Letters,36, 1–3.

Dewenter, R., & Haucap, J. (2006). Incentives to license virtual mobile network operators (MVNOs). In R. Dewenter, & J. Haucap (Eds.),Access pricing: Theory and practice. Amsterdam: Elsevier BV.

Dixit, A. (1980). The role of investment in entry-deterrence.Economic Journal,90, 95–106.

Economides, N. (2005).The incentives for vertical integration. Working paper No. 05–01, Retrieved from The NET Institute website:/http://www.netinst. org/The_Incentive_for_Vertical_Integration.pdfS.

European Commission (2006).Commission endorses, with comments, Spanish regulator’s measure to make mobile market more competitive. Press Release IP/06/97.

European Commission (2007).Commission acts to reduce telecoms regulation by 50% to focus on broadband competition. Press Release IP/07/1678. European Regulator Group (2006).Mobile access and competition effects. ERG (06) 45.

Foros, Ø., Hansen, B., & Sand, J. Y. (2002). Demand-side spillovers and semi-collusion in the mobile communications market.Journal of Industry, Competition and Trade,2, 259–278.

Greenhut, M. L., & Ohta, H. (1979). Vertical integration and successive oligopolists.American Economic Review,69, 137–141.

Hastings, J. S., & Gilbert, R. J. (2005). Market power, vertical integration and the wholesale price of gasoline.Journal of Industrial Economics,53, 469–492. Kim, B. W., & Seol, S. H. (2007). Economic analysis of the introduction of the MVNO system and its major implications for optimal policy decisions in

Korea.Telecommunication Policy,31, 290–304.

McAfee, R. P. (1999). The effects of vertical integration on competing input suppliers.Federal Reserve Bank Cleveland Economic Review,35, 2–8. Ofcom (2006, February).The Communications Market(Interim report). Retrieved from/http://www.ofcom.org.uk/research/cm/interim/feb06_report/

comms_mkt.pdfS.

Ordover, J. A., Saloner, G., & Salop, S. C. (1990). Equilibrium vertical foreclosure.American Economic Review,80, 127–142.

Ordover, J. A., & Shaffer, G. (2007). Wholesale access in multi-firm markets: When is it profitable to supply a competitor?International Journal of Industrial Organization,25, 1026–1045.

Parker, P. M., & R ¨oller, L.-H. (1997). Collusive conduct in duopolies: multimarket contact and cross-ownership in the mobile telephone industry.Rand Journal of Economics,28, 304–322.

Polaski, S. (1992). Divide and conquer. On the profitability of forming independent rival divisions.Economic Letters,40, 365–371. Salinger, M. A. (1988). Vertical mergers and market foreclosure.Quarterly Journal of Economics,103, 345–356.