Research Article

January

2018

Computer Science and Software Engineering

ISSN: 2277-128X (Volume-8, Issue-1)

The Historical Market Analysis and Rationale of Electric

Vehicles Batteries

Majid A. Dehkordi

Starlight Group, Tokyo, Japan

Graduate School of Commerce and Management, Hitotsubashi University, Tokyo, Japan

Seiichiro Yonekura

Graduate School of Commerce and Management, Hitotsubashi University,

Tokyo, Japan [email protected]

Abstract - The aim of this paper is to analyze the market structure of rechargeable batteries, and the importance of battery production cost on the commercialization of Electric Vehicles. In this regard, the two generations of electric vehicle penetration in the society, in the period of 1996 to 2012, are concerned. It is argued that a combination of pre-production factors such as raw materials and technology breakthroughs, as well as post-pre-production factors such as rise of East-Asian competitors will define the next market trend of EV batteries. Among the implications of this study, the competition between Korean, Chinese and Japanese battery suppliers is also explained.

Keywords - EVs, Li-ion, NiMH, Lead-Acid, Battery

I. INTRODUCTION

Electric Vehicles’ battery development has been the main obstacle in the EV’s fight for consumer market share in the past two decades. The largest cost item in an EV is the battery pack needed to run the vehicle, but even with the higher capacities of batteries, EVs cannot dominate the competition against fuel vehicles. Indeed, today’s battery technologies have advantages, but they also bring new challenges. For example, compared to Lead-Acid battery (invented in 1859), the Li-Ion technology (developed in 1980s) gives a more reliable and steady current, but still is highly sensitive for under and over voltage.

Speaking of which, the history of electric cars is closely related to the history of batteries [1-2]. In 1800, the Italian scientist, Alessandro Volta showed that electric energy could be stored chemically. The battery designed by Volta is credited to be the first electrochemical cell. In 1821, Michael Faraday demonstrated the principles of the electric motor-or generator- while applying Volta’s chemical pile as a component of his experiments. By the mid 1830's, both Volta's invention of the battery and the electric motor by Faraday had been engineered into the first electric road vehicle [3]. Extensive progresses in electrochemistry and battery development took place later on. In 1859, Gaston Plante´ made a path-breaking demonstration of the first rechargeable lead-acid battery. Lead-acid battery made a great influence on the later development of ICE cars and also EVs. In 20st century, Nickel-metal-hydride (NiMH), lithium-polymer (Li-Poly), and lithium-ion (Li-ion) batteries are the main breakthroughs in the EV development. They have put electric cars and hybrids into the marketplace and continue to evolve into smaller size with higher storage capacity [4].

It is correct that with the current technologies, EV batteries increase storage capacity with less weight, decline life time cost of the vehicle, achieve higher level of safety and reliability, and promote clean energy sources for stopping global warming; meanwhile they are still the largest cost item in an EV. Today, in average, EV battery runs as high as US$ 16,000, more than one-third of the total price of electric cars. Marketing specialists state that with more sales of EVs, economy of scale make the production cost less than before.

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44 In this sense, this paper aims to explain the effect of battery development on the two generations of EV production. In other words, comparing the first generation of EVs with the second one, what pitfalls and limitations in the way of battery development were eliminated?

II. HISTORY AND TECHNOLOGICAL BACKGROUND

The battery technology itself, its reaction to severe heat and cold, its recharging ease and capability and its weight are keys to the success or failure of electric vehicles. The impact of EV batteries slow technological development, when compared to improvements in the current internal combustion engines, cannot be ignored or minimized. In this section, the regular battery types, along with their advantages and faults will be discussed. Several popular combinations that are currently used in EVs include lead-acid, NiMH, Li-ion, NiCd, Li-ion polymer batteries.

Lead-Acid battery

Lead-acid battery is rechargeable, the most widely available and the least expensive battery in the market. EVs that use lead-acid batteries usually have a range of 80 miles per charge. First Lead-acid battery was invented by Gaston Planté in 1859. Although lead-acid batteries are the cheapest energy storage products to manufacture, they have an exceptionally large footprint and heavy weight. They are not as reliable in cold weather, easy to corrode, and also have a fast discharge. Lead-acid batteries contain harmless emissions, and need to be replaced every three years. Compared to other batteries, recycling it is more expensive, but the companies who recycle it, get a rate as high as 98 percent.

Their application is from golf carts, electric wheelchairs and scooters to hybrid and electric vehicles. Figure 1 shows the first Lead-acid battery invented by Planté and a Lead-acid battery produced in late 2010s.

This kind of battery was usually used between 1890 and 1925 in early EVs. This period of time was called “the Golden Ages of Electric Vehicles”. Later in the 1960s and 70s, EVs which were manufactured by major companies also had used Lead-acid as their main energy source. In the last two decades, original models of EVs such as Toyota RAV4 EV I (1997) and General Motors EV1 (1996) had used this type of battery. Figure 1 shows two electric cars with ninety years production time difference, both used Lead-acid battery.

Figure 1. First re-chargeable Lead-acid battery invented by Planté, a Lead-acid battery produced in late 2010s, Detroit Electric Car 1907, and Toyota RAV4 EV I 1997

Nickel Metal-Hydride battery (NiMH)

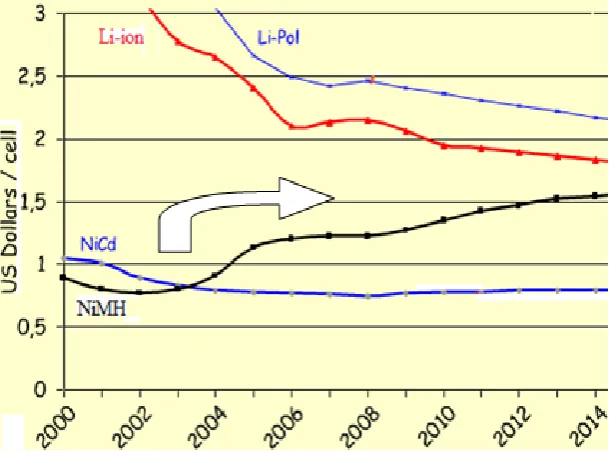

NiMH battery appeared on the market in 1989. Original patent belongs to Daimler-Benz that had sponsored the battery development project for over two decades [5]. Later, Stanford R. Ovshinsky altered and improved the Ti-Ni alloy structure and composition of the NiMH battery. He patented the new NiMH battery, founded Ovonic Battery Company in 1982, and licensed NiMH batteries to over 50 companies worldwide. Regarding the market structure, Boschert (2006) described the difficulties that EV developers encounter when they try to obtain Nickel Metal hydride (NiMH) batteries. She details the series of events which ultimately resulted in Chevron Oil [Cobasys LLC] gaining control of the patents covering most NiMH batteries and the combined strength of the oil/automotive industrial complex, now controls the production of these batteries. Figure 2 shows that in spite of the decline in all rechargeable batteries price, NiMH battery is still getting more expensive.

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44

Figure 2., Price comparison of popular rechargeable batteries

Source: [7]

Compared to Lead-acid battery, NiMH has a higher energy density than lead-acid batteries and can deliver a range of up to 120 miles per charge. NiMH batteries have a long life span; they are environmentally safe and recyclable. Meanwhile, they have a poor performance in cold weather and a high self-discharge.

Between 1996 and 2003, these batteries had been used in most electric vehicles including the Toyota RAV4 EV I, GM EV1, Ford Ranger EV and Honda EV Plus. The story is that after the original models of Toyota and GM electric cars were produced and sold, these two companies recognized superior energy and power density of this battery and changed their Lead-acid to NiMH battery pack. NiMH has also been used in hybrid vehicles including the Toyota Prius and the Honda Civic Hybrid. Today, they are still widely used in hybrid vehicles like Prius family, Ford Escape and Honda Insight II. Currently, more than two million hybrid cars worldwide are running with NiMH batteries [8] and the main manufacturers of the market are Panasonic and Sanyo.

Lithium-ion battery (Li-ion)

First commercial Li-ion battery was released by Sony and Asahi Kasei in 1991. From the first proposal of Lithium battery by M. S. Whittingham in 1976 [9], many scientists worked on this technology. As result, the current Li-ion battery is far superior to the original ones. Li-Ion cells can be produced in different shapes and have a higher energy density than many other battery technologies [3]. Li-ion is widely used in laptops, electronic tools and due to their superior range per charge (at around 250-300 miles) it currently is the best candidate for EV implementation.

Li-ion battery has a low self-discharge rate, approximately 5 to 10 percent of its capacity per month. It’s environmentally safe, reusable and has much lighter weight than other battery types. However, the Li-ion technology has its disadvantages: it has a high production cost, adding between $8,000 and $18,000 to the price of vehicles, depending on the size of the packs that makes final EV price expensive for the customer. It needs temperature monitoring and protection against under and over voltage. Li-ion batteries can ignite or explode when exposed to heat.

Nickel-Cadmium (NiCd) and Li-ion polymer (Li-Poly) batteries

First Flooded cell NiCd battery was invented in 1899. This battery has been always more costly than other types such as the lead-acid battery; besides, the cells have higher self-discharge rates. It is correct that the recent advances in battery-manufacturing technologies have made batteries extremely cheaper to produce, but NiCd battery is losing its popularity in the market. For example, in the European countries, sales of NiCd batteries for portable use have been greatly restricted.

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44

Figure 3. Popular rechargeable batteries, from left to right: NiMH, Li-ion, NiCd, Li-Poly

Technology comparison

Many different battery technologies have evolved since the 1800s. Today, we have over 22 different types of secondary cells or rechargeable batteries and over 31 different types of primary cells or non-rechargeable batteries in the market. Secondary cells are rechargeable and can be re-used. This makes them a better candidate for portable electronic devices and EVs. Table 1 shows the comparison of the main in use rechargeable batteries in the market.

Table 1., Popular rechargeable batteries comparison

Efficiency (%)

Charging time

Self discharge per month (%)

Energy density Applications

Lead-acid 80 8-16 h 5 60-75 Wh/L Vehicles, Golf carts, EV & HEV, Grid

storages

NiMH 66 2-4 h 30 140-300 Wh/L EV & HEV, Backup service power

Li-ion 80-95 1-4 h 8-30 250-730 Wh/L Cell phones, Laptops, EV & HEV,

Aviation and Marine

NiCd 70-90 1 h 20 50-150 Wh/L EV, Toys, Portable devices

Li-poly 99.8 6 h 5 300 Wh/L Future applications

Source: [10], [11], [12]

discharge is a loss of capacity over time due to parasitic reactions in the chemicals of a cell [13]. Self-discharge rate is mainly dependent on the temperature affecting the cell. In terms of Self-Self-discharge, maybe Lead-acid batteries are still one of the best options available, but they have a very low energy density and high charging time. Lower energy density means that EV driver needs to recharge its EV battery more often. A normal gasoline vehicle has a higher energy density than any of the battery technologies used today.

Regardless of the type for using in EVs and HEVs, the current battery cost when distributed over the life cycle of the vehicle is in a range of 700 to 1000 $/kWh. In the current state and compared with ICV, an EV must have at least 7000 recharging cycle to make its cost equal with 10 years life span of ICV. In reality, even if we recharge an EV everyday, for 10 years, it will be 3650 recharge cycle and it takes 19 years to make it equal. In this regard, Simonsen [25] stated that lithium batteries will need to double their energy density and bring down the price from $500 (2010) to $100 per kW*h capacity in order to make an impact on petrol cars. consistent with the above argument, Kammen et al. (2008) [14] stated that they would become cost efficient to consumers if battery prices would decrease from $1300/kWh to about $500/kWh (so that the battery may pay for itself).

Weight of batteries is one of the important strains toward EV commercialization. A range of 100 km for an electrical vehicle requires over 400 kg of lead-acid batteries, about 200 kg of nickel-metal hydride (NiMH) batteries or about 120 kg of Lithium-Ion (Li-ion) batteries [3].

Based on the above arguments, Li-ion cells have a higher energy density, a lower self-discharge rate, and lower life cycle cost of the same weight than lots of other battery technologies. In other words, when we compare the two most popular batteries used for HEVs and EVs, NiMH and Li-ion; they are comparable in cost per kW*h but Li-ion is one half the weights. In this sense, NiMH makes more sense in HEVs than EVs, because HEVs do not only rely on their battery pack to determine the ultimate range, and Li-ion would be more suitable for EVs.

III. MARKET STRUCTURE

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44 electric vehicle production stopped and all the companies taken out their EVs from the market. Later in 2008, EV production started again and more companies joined the race. In this section, the market structure of battery manufacturers for the both mentioned waves will be discussed.

First generation (1996 - 2003)

In the late 1990s, considerable R&D work has been devoted on declining the extremely high cost of batteries. Table 1 shows the active providers of the EV battery in the market.

Table 1., Active EV Battery providers between 1996 and 2003

Provider Manufacturers Battery type Head Quarters

Delco electronics (subsidiary of GM, later transferred to Delphi)

Chevrolet S-10 1997*

GM EV1 1996*

Lead-acid US

Delphi (GM’s branch) GM EV1 1998*

GM EV1 1999 re-design

Lead-acid NiMH

US

Panasonic EV Energy (PEVE) (joint venture between Toyota and Matsushita)

GM EV1 1999*

Chevrolet S-19 EV 1998*

Ford Ranger EV 1999 Toyota RAV4 EV 1997 Honda EV plus

Toyota Prius I-II-III Honda Insight I Honda Civic I

Lead-acid

NiMH

Japan

Ovron Chevrolet S-19 EV 1998 NiMH US

Trojan Ford Ranger EV 1996* Lead-acid US

Sony Nissan Altra EV 1998

Nissan Prairie Joy EV 1996

Li-ion Japan

Sanyo (joint with Honda to

compete with PEVE)

Honda Hybrid vehicles (from 2002) Ford Hybrid Vehicles (from 2001)

NiMH Japan

* the first models of mentioned vehicles used Lead-acid, but later they changed their battery pack to NiMH

Between 1996 and 2003, the major battery manufacturers were such as Ovron, Sony, Sanyo, Panasonic EV Energy, Varta, SAFT, Hydro Quebec, NEC, 3M, Shin Kobe (a joint between Hitachi and Maxwell), Delphi and Trojan. Alliance between Japanese companies later helped them to improve the quality of their products faster. For example, by establishing EV Energy and combining the advantages of both Toyota and Matsushita in manufacturing, Matsushita Battery's capability improved by several levels [15]. But out of all these manufacturers, Japanese companies’ market share was more 75 to 85 percent of the global sales. It should be noted that in this period of time, almost all of the Li-ion batteries were produced in Japan. Figure 1 shows the cumulative rechargeable battery production trend during the first generation of green fleet.

Figure 1., the market trend of rechargeable batteries between 1996 and 2003

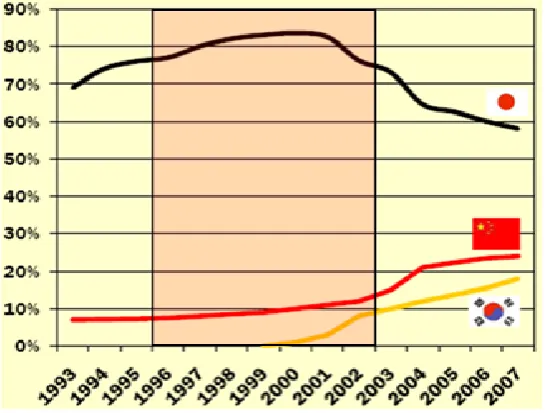

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44 From early 2000s, the domination of Japanese companies declined and rivals from East Asian countries tried to grab a piece of this sophisticated battery market. As result, Japanese market share from 82 percent in 2001 decreased to less than 75 percent in 2003 and 56 percent in 2008.

Second generation (2008 - 2012)

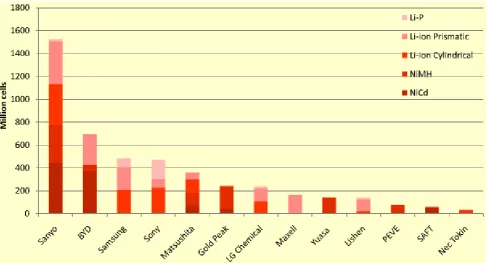

From the late 2006, as result of high raw material costs and the shutdown of most of lead-acid battery capacities in China, the cost of batteries increased very rapidly. From 2008, companies from China, Korea, France, Germany, UK and US also entered the brutal competition for battery sales. Companies such as LG Chem and Samsung from Korea, BYD, Li Shen and GP from China were competing in the ten top battery manufacturers against Japanese companies. In 2008, from group of tenin the global market, still five companies belonged to Japan (Sanyo, Sony, Matsushita, GS Yuasa and Maxell), with Sanyo battery production share is somehow equal as all the other non-Japanese manufacturers. In case of Li-ion in 2009, Japan and South Korea held about 80% of the global market share of advanced Li-ion batteries; China, 12%; others, nearly 6%; and the United States, about 2% [16]. Figure 2 shows the top battery suppliers in 2008.

Figure 2., Top battery OEMs in 2008

Source: [7]

As far as the structure of hybrid vehicles’ battery market is concerned, according to US Department of Energy (2010), out of all battery manufacturers, Primearth EV Energy held about 74 percent, Sanyo held about 25 percent, and SB LiMotive, Saft, Johnson Controls, and APS together held less than a percent of the market share.

In the past few years, lots of new ventures also entered the global competition for battery production. Between 2008 and 2012, companies such as Hitachi, NEC, AESC, Lithium Energy Japan, Blue Energy and Toshiba from Japan; Tesla, Ener1, Johnson Controls and A123 from US; E-one Moly Energy from Canada; Axeon from UK; and SB Limotive from Korea just got serious about the battery production. Many of them are new ventures or joint alliances between major companies to ease the production and decrease the cost of batteries. Just in the Li-ion battery market, currently there are more than 138 manufacturers active in the market [e.g. 17].

From early 2012, a blizzard of heavy competition from Asian companies hit the western ventures who were active in battery production. As result, some of fresh startups failed and went bankrupt. In Jan 2012 Ener1 Inc, Li-ion battery maker filed for bankruptcy (later recovered through a grant from Department of Energy, US). In Oct 2012, A123 systems filed for bankruptcy and sold to Chinese auto parts conglomerate Wanxiang Group. In July 2012, Valence Technology Inc, Lithium battery maker also filed for bankruptcy protection.

Table 2., Active EV Battery providers from 2008

Provider Manufacturers Battery type Head Quarters

A123Systems

(filed for bankruptcy in Oct 2012,

GM, Daimler buses, BMW hybrid cars, Mercedes-Benz, Chevrolet Spark EV,

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44 sold to Chinese Wanxiang group

and newly emerged as

A123Systems LLC)

Fisker Karma PHEV, VIA Motors VTRUX

Axeon* (acquired by Johnson Matthey)

Rollz-Royce, Jaguar, Land Rover

Lithium iron phosphate

UK

E-One Moli Energy BMW Mini-E Li-ion Canada

Electrovaya Tata, future Chrysler plug-ins Li-ion Canada

EnerDel (subsidiary of Ener1 - Filed for Bankruptcy on Jan 2012)

Think Global Li-ion US

Primearth EV Energy (joint between Matsushida and Toyota – until 2010 known as Panasonic EV Energy)

Toyota’s future EVs, Prius & Camry Hybrids, GM Hybrids

Prius plug-in hybrid Ford Hybrids Tesla

NiMH Li-ion

(provide Battery cells for

assembly in Palo Alto)

Japan

Sanyo (now subsidiary of Panasonic)

Honda Insight-CR/Z-Civic hybrids, Ford Fusion-Mariner-MKZ hybrids, Suzuki Swift, VW hybrid, Prius PHEV

NiMH Japan

LG Chem GM -Chevrolet Volt, Ford Focus EV,

Hyundai Sonata/Optima Hybrids

Li-ion Korea

Automotive Energy Supply

Corporation (AESC-Joint

between Nissan Motor and NEC Corp)

Nissan Leaf/Infiniti, Renault Li-ion Japan

Tesla (power train provider) Toyota, Daimler Li-ion US

Johnson Controls BMW, Mercedes, ford, Daimler AG Li-ion US

SB LiMotive (joint of Bosch and Samsung SDI**, disbanded on Sep 2012)

BMW, Chrysler Fiat EV Li-ion Korea

Lithium Energy Japan (joint between GS Yuasa and Mitsubishi)

Mitsubishi, Peugeot and Citroen spin-offs

Li-ion Japan

Blue Energy (second joint of GS Yuasa with Honda)

Honda Civic Hybrid Li-ion Japan

Toshiba Honda Fit EV, Mitsubishi MiEV Li-titanate Japan

Valence Technology (filed for bankruptcy in july 2012)

Mercedes eVito Li-ion US

NEC Nissan Leaf Li-ion Japan

Li-Tec Daimler AG Li-ion Germany

JC Saft GM and Ford hybrids Li-ion France

BYD BYD e6, F3DM & S6DM hybrids Li-iron

Phosphate

China

Hitachi GM Buick, Li-ion Japan

Robert Bosch Battery Systems (new joint of Bosch and Cobasys)

Fiat 500e Li-ion Germany

*Axeon was the largest European Li-ion supplier

**Samsung SDI is also active in producing Li-ion and other rechargeable batteries but its products are not used in the current EVs

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44

Figure 2., Expanding market of Korean battery manufacturers

Source: IIT, KISTI, Daishin Securities Research center (2012), [18]

In 2012, based on factors such as market share, product quality, financial resources, geographic reach, non-automotive applications and product strategy, out of 17th major battery manufacturers, Pike Research demonstrated the front runners for EV battery production: LG Chem of Korea is at the top EV battery supplier ($8.5 billion share), following it are Johnson controls, GS Yuasa Corp, Automotive Energy Supply, A123 Systems (before bankruptcy), Panasonic (Primearth), SB LiMotive, Hitachi Vehicle Energy, BYD, and Electrovaya; with the last three companies not to currently have the manufacturing capacity in place to produce the volumes necessary to become a global leader. For example, Hitachi completed its mass-production line just in 2009. Figure 3 shows the top ten EV battery manufacturers’ positioning in the market.

Figure 3., Top ten battery manufacturers’ positioning in the global market

Source: [19]

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44 More over, the importance of growing market for Chinese suppliers shouldn’t be ignored. Today, there are a great number of cheap brands of rechargeable batteries that are mostly manufactured in China. Made-in-China.com, a website developed by Focus Technology Co, lists more than 650 rechargeable battery suppliers located in China. However, in spite of their lower price, the poor battery design is both dangerous and ineffective. It should be noted that still China is expected to be the largest market for lithium-ion automotive batteries in 2016 (40% of the market), due to strong government incentives for EV’s [21]. But, China has not attained a trusted brand name, which is essential for success in the battery industry.

IV. CONCLUSION AND DISCUSSION

EV batteries are evaluated with a focus on the weight, cost of the battery and energy density. In the previous section, the market structure of rechargeable batteries, mainly with the focus on EV batteries was explained. The lithium-ion market grew dramatically over the past decade. Furthermore, it seems that the HEVs that previously used nickel-metal hydride (NiMH) technology are now shifting to Li-ion. Avicenne report [7] forecasted that by 2020, between all the rechargeable battery types, the market sales of Li-ion batteries will double in volume, while the cumulative sales of NiCd and NiMH batteries will stay the same.

In the next decade, the cost reduction of batteries will still be the main challenge and it will have a huge influence on the acceptance of EVs. USABC (United States Advanced Battery Consortium) emphasized that the target cost of batteries must be $3500 for EVs to gain market acceptance. Depending on the size, today’s EV batteries price range from $8,000 to $18,000. In the current state of the market, the most important factor for the cost reduction on batteries is the economy of the scale. Battery manufacturers are hardly trying to tackle this cost challenge by increasing production volume, improving production process efficiency, and finding other feasible applications for the batteries to improve economies of scale.

Another factor that may help with the cost of batteries is that auto manufacturer's financing for the batteries can be done separately from EV. It may benefit the battery manufacturers by permitting large-volume production, but may also tie the battery manufacturer’s fate to the success of a single vehicle manufacturer [22]. This is the strategy that Nissan is pursuing for EV production. “A battery needs total balance. If we don’t make it ourselves to our precise level, then we won’t be able to make a reality the new mobility we are aiming for”, said Nissan’s EV Energy Development Department project leader Takeshi Miyamoto. Therefore, cutting the cost of the battery is the key to reducing the overall costs of the car [23].

Another concerns is, while huge Asian companies have a cost advantage over the newer companies, the startup companies once championed as America’s leading lights in a manufacturing resurgence are now stumbling, cutting costs and scaling back production just to keep afloat [24]. For example, A123's cost of building batteries is about $1,000 per KW/h, while some Asian manufacturers are bidding as low as $400 (Ibid). Historically, East Asian companies could remain competitive by keeping investing in the innovation and offering lower prices.

It is useful to understand that since the new efforts of auto manufacturers to promote EVs in the society from 2008, EV adoption hasn’t quite taken off as quickly as investors had imagined. In other words, with the slow roll out of electric vehicles, finding more mature and reliable battery markets makes a lot of sense. In these terms, the prospect won’t be too much bright for the future startups. In the next decade; just few major global players will survive. The industry has seen a number of nascent players went bankrupt and it seems that only the companies with full complimentary assets (from entire value chain to marketing expertise) will survive with a challenging unbalanced margin.

REFERENCES

[1] Westbrook, M.H. (2001). The Electric Car: Development and Future of Battery, Hybrid and Fuel-CellCars. Society ofAutomotive Engineers Inc.,Warrendale, PA, USA.

[2] Sperling, D. (1995). Future Drive. Island Press, Washington, DC, USA.

[3] Teratani, T., Mizutani, R., Yamamoto, K., & Anegawa, T. (2008). Energy-saving Technologies for Automobiles.

IEEJ Trans Elec Electron Eng, 3: 162–175.

[4] Anderson, J., Anderson, C.D. (2005). Electric and Hybrid Cars: A History. McFarland & Co., London, UK.

[5] Beccu, K. (1974). Negative Electrode of Titanium-Nickel Alloy Hydride Phases. United States Patent Office. Patent 3824131

[6] Orion, M. (2005). Cobasys and Panasonic EV Energy Extend Cooperation and Agree to Expanded License Terms. Cobasys press release.

[7] Avicenne report (2009). The rechargeable battery market 2008-2020. Avicenne development.

ISSN(E): 2277-128X, ISSN(P): 2277-6451, pp. 35-44

[9] Whittingham, M.S. (1976). Electrical Energy Storage and Intercalation Chemistry. Science 192 (4244): 1126–

1127.

[10] Bergstrom, S. (1952). Nickel–Cadmium Batteries – Pocket Type. Journal of the Electrochemical Society, 99(9):

248c-a50c

[11] Battery University (2010). What’s the Best Battery?

http://batteryuniversity.com/learn/article/whats_the_best_battery (retrieved 14 Feb 2013)

[12] Valøen, L.O., and Shoesmith, M.I. (2007). The effect of PHEV and HEV duty cycles on battery and battery pack performance. Plug-in Highway Electric Vehicle Conference: Proceedings.

[13] Jungst, R.J. (2001). Recycling of electric vehicle batteries. Industrial Chemistry Library, 10: 295-327

[14] Kammen et al. (2008). Compared CV, HEV and 2 PHEVs. University of California, Berkeley.

[15] Itazaki, H. (1999). The Prius that shook the world. Nikkan Kogyo Shimbun Ltd publication.

[16] Shiau, C.N., Samaras, C., Hauffe, R., & Michalek, J.J. (2009). Impact of Battery Weight and Charging Patterns on the Economic and Environmental Benefits of Plug-In Hybrid Vehicles. Energy Policy, 37: 2653–2663. [17] IDTechEx report (2012). Batteries and Supercapacitors for Smart Portable Devices 2013-2023: Markets,

Technologies, Companies. IDTechEx Pub.

[18] Kim, R. (2012). Rechargeable Batteries: Chapter 1. Mobile device batteries. Daishin Securities rechargeable battery industry report, 1.

[19] Pike Research (2012). Pike Pulse Report: Electric Vehicle Batteries. Pike Research,

http://www.pikeresearch.com/research/pike-pulse-report-electric-vehicle-batteries (retrieved 4 March 2013).

[20] Sung-mi, K. (2012). Korean Secondary Battery Leaping 10 years, Overtaking Japan. Korea IT Times,

http://www.koreaittimes.com/story/21199/korean-secondary-battery-leaping-10-years-overtaking-japan

(retrieved 4 March 2013).

[21] Greenberger, J. (2013). Lithium-Ion Market on Verge of Dramatic Growth. The energy collective,

http://theenergycollective.com/jim-greenberger/189931/lithium-ion-battery-market-verge-dramatic-growth

(retrieved 4 march 2013)

[22] Canis, B. (2011). Battery Manufacturing for Hybrid and Electric Vehicles: Policy Issues. CRS report for Congress.

[23] Nissan Technology Magazine (2012). Why Did Nissan Develop an EV Battery?

http://www.nissan-global.com/EN/TECHNOLOGY/MAGAZINE/ev_battery.html (retrieved 5 March 2013).

[24] Chernova, Y. (2011). Battery Companies in Need of a Boost. The Wall Street Journal, JP edition.

[25] Simonsen, T. (2010). Density up, price down (in Danish). Electronic Business, 23.

ABOUT AUTHOR

Dr. Majid A. Dehkordi is Senior Director at Starlight Group, Tokyo. He is currently specializes in HR and Managerial consulting and practices in APAC market. He is graduated from Hitotsubashi University with a PhD degree in Marketing and Management. His areas of research interests include Media and Communication studies, Entrepreneurship and Innovation, Marketing, and Green technologies.

![Figure 2., Expanding market of Korean battery manufacturers Source: IIT, KISTI, Daishin Securities Research center (2012), [18]](https://thumb-us.123doks.com/thumbv2/123dok_us/7809469.2085754/8.595.109.494.387.677/figure-expanding-korean-battery-manufacturers-daishin-securities-research.webp)