3

INTERIM

FINANCIAL REPORT

AVINOR

Avinor has two primary business areas, operation of a

nationwide network of airports, and the national air

navigation services for civil and military aviation. In total, this

includes 46 airports as well as control towers, control centres

and other technical infrastructure for safe air navigation.

In addition to the aviation-operative activities, commercial

earnings are facilitated through airport hotels, parking

facilities, tax-free stores, restaurants and other

services for air passengers.

Avinor is a group where the operational activities are

partly organised in divisions and in partly in legal entities

(subsidiaries). Financially, the airport operations are run as

a single aviation system. The air navigation services finance

themselves by pricing the services in accordance with

international provisions. The Group has approximately 3,300

employees and annual operating revenues of NOK 9 billion.

The shares in Avinor AS are wholly owned by the Norwegian

state as represented by the Ministry of Transport

and Communications. The Ministry of Transport and

Communications manages the Norwegian state’s ownership

of Avinor, and stipulates e.g. the tasks imposed on the Group

to safeguard the general interests of Norwegian society, the

required rate of return and dividends. In addition, the Ministry

of Transport and Communications regulates the aviation fees.

The Ministry of Transport and Communications is the highest

authority for Norwegian aviation and also stipulates the Civil

Aviation Authority’s regulations, which have consequences for

Avinor’s operations.

Avinor has issued bonds that are listed on the Oslo Stock

Exchange. The Group’s corporate governance must adhere to

the Oslo Stock Exchange’s recommendations for corporate

governance to the extent applicable. The principles

complement the government’s focus on corporate governance

in the management of the Norwegian state’s shareholdings.

Avinor’s head office is located in Oslo.

Group main figures

4

Board of directors report

5

Balance sheet

10

Income statement

11

Statement of comprehensive income 12

Statement of changes in equity

13

Statement of cash flows

14

MAIN FIGURES AVINOR GROUP

Avinor Group - Main figures

Amounts in MNOK Year

2013 2012 2013 2012 2012

794,1

755,7 Traffic income 2 238,5 2 168,0 2 860,2

310,6

246,3 Security (cost based) 857,5 726,3 948,7

1 333,3

1 191,6 Other income 3 479,4 3 141,6 4 245,5

48,1

50,8 Inter-group income 140,4 149,3 201,4

2 486,1

2 244,4 Total income airport operations 6 715,8 6 185,2 8 255,8

261,7

242,5 En route charges 704,9 718,2 947,0

183,0

198,1 Inter-group income approach and control tower services 548,5 593,9 745,9

58,6

61,3 Other income 178,1 114,4 144,2

503,3

501,9 Total income air navigation services 1 431,5 1 426,5 1 837,1

131,4

213,6 Other group income (a) 397,6 444,9 474,1

-360,3

-459,7 Elimination of inter-group income -1 083,3 -1 185,5 -1 414,9

2 760,5

2 500,2 Total group income 7 461,6 6 871,1 9 152,1

-1 375,1

-1 415,9 Operating expenses airport operations (a) -4 043,8 -3 962,8 -5 255,2

-491,9

-455,4 Operating expenses air navigation services -1 336,1 -1 239,3 -1 715,5

-198,6

-149,5 Other operating expenses group -567,8 -476,1 -678,1

360,3

459,7 Elimination of inter-group expenses 1 083,3 1 185,5 1 414,9

-1 705,3

-1 561,1 Total group expenses -4 864,4 -4 492,7 -6 233,9

1 111,0

828,5 EBITDA airport operations 2 672,0 2 222,4 3 000,6

11,4

46,5 EBITDA air navigation services 95,4 187,2 121,6

-67,2

64,1 EBITDA others -170,2 -31,2 -204,0

1 055,2

939,1 EBITDA group 2 597,2 2 378,4 2 918,2

-336,6

-322,7 Depreciation, amortisation and impairment charges -1 008,9 -991,2 -1 335,7

8,7

-1,7 Changes in value and other (losses)/gains, net 2,4 -17,2 -20,3

727,4

614,7 Operating profit/(loss) 1 590,7 1 370,0 1 562,2

-88,1

-109,3 Net finance income/(costs) -257,1 -277,7 -355,9

639,3

505,4 Profit/(loss) before income tax 1 333,6 1 092,3 1 206,3

-179,1

-141,6 Income tax expense -373,8 -306,7 -351,6

460,2

363,8 Profit/(loss) after tax 959,8 785,6 854,7

44,7 % 36,9 % EBITDA-margin airport operations 39,8 % 35,9 % 36,3 %

2,3 % 9,3 % EBITDA-margin air navigation services 6,7 % 13,1 % 6,6 %

38,2 % 37,6 % EBITDA-margin others 34,8 % 34,6 % 31,9 %

1 059,9

1 098,3 Investments airport operations 2 777,0 2 822,2 3 883,1

22,5

4,7 Investments air navigation services 71,8 37,5 78,1

52,3 14,2 Investments others 149,4 79,3 123,4 1 134,7 1 117,2 Total investments 2 998,2 2 939,0 4 084,6 -463,4 -421,8 Distributed dividends -463,4 -421,8 -421,8 -373,7

-505,6 Cash flow before borrowings -1 001,7 -1 403,1 -2 229,6 Net interest-bearing debts 13 388,6 10 761,0 11 187,8 Total assets 30 721,7 27 491,8 28 146,0

Equity ratio 38,8 % 36,7 % 36,8 %

Return on total capital after tax 5,8 %

13 293,0

12 583,6 Number of passengers (in 1000) 36 585,1 35 041,8 46 357,0

190,5

182,3 Number of aircraft departures (in 1000) 547,6 538,6 669,0

567,4

493,2 Number of service units (in 1000) 1 531,9 1 381,1 1 845,0

Punctuality (b) 86 % 87 % 89 %

Regularity (b) 98 % 98 % 98 %

(a) Exclusive of inter-group leases on land

5

HIGHLIGHTS

The Group had a financially strong third quarter with

growth in traffic measured in numbers of passengers of

5.6 per cent, and growth in operating income of 10.4 per

cent compared with the corresponding reporting period

last year. Year to date growth in traffic was 4.4 per cent

and growth in operating income was 8.6 per cent at the

end of the third quarter. The Group’s operating margin

improved by 1.4 percentage points compared with the

corresponding period last year.

At the end of September, the Group’s operating income

totalled NOK 7,462 million, and the profit after tax was

NOK 960 million. Capitalised project costs totalled

NOK 2,998 million at the end of the third quarter. Before

changes in debt, the Group had a negative cash flow of

NOK 1,002 million.

There has been a significant earnings improvement

for airport operations due to the growth in traffic and

increased commercial income per passenger. The

cost level per passenger remains unchanged from the

corresponding period last year. The largest airports

are operating beyond what is normally regarded as

full capacity for parts of the day. Beyond the ongoing

projects for establishment of the necessary capacity in

the long term, a continuous effort is made to streamline

the operations for both the airlines and the passengers.

Progress of the T2 project at Gardermoen is proceeding

as planned. Total budget is NOK 14.1 billion. New

taxiways and airside parking stands are now in use,

while extensive construction work is in progress for the

new Terminal 2 and the new North Pier. Preparatory

groundwork for a new terminal has started in Bergen.

There was underlying strong growth in the traffic for the

air navigation service measured in number of service

units, which was counteracted by reduced prices. To

facilitate adaptation to new national and international

performance requirements for the air navigation service,

it has been decided to change the Group’s legal structure

by separating the air navigation service into a limited

company that will be wholly owned by Avinor. The plan is

to implement the change during the first half of 2014.

No aviation accidents have been registered, with

or without personal injury, in which Avinor was a

participant, year to date this year. Over the last 12

months, the Group has had a lost time injury frequency

rate (H1 value) of 2.6 (internal target is 3 or less) and

absence due to illness of 4.4 per cent (internal target is

4.5 per cent or lower).

3

RDQUARTER 2013

1MNOK

Per Q3 2013

Q3 2012

Change

Operating income

2 760,5

2 500,1

10,4 %

EBIT

727,4

614,7

18,3 %

Profit for the year

460,2

363,8

26,5 %

Investments

1 134,7

1 117,2

1,6 %

Table 1: Key financial figures

In the third quarter of 2013, the Group had a profit after

tax of NOK 460 million, compared with NOK 364 million

for the corresponding accounting period last year.

This earnings improvement is primarily due to higher

operating income. A total of 13.3 million air passengers

travelled via Avinor’s airports in the third quarter,

which is an increase of 5.6 per cent compared with the

corresponding period last year.

The Group’s operating income in the third quarter

increased by 10.4 per cent to NOK 2,761 million. This

growth reflects a continued good development for the

Group’s commercial offers at the airports and a positive

trend in passenger volume.

Total operating expenses, excluding depreciation and

write-downs, totalled NOK 1,705 million in the third

quarter. This is a change of 9.2 per cent compared

with the corresponding reporting period last year. The

increase in expenses are linked to workforce growth at

the major airports, contracted security services and a

change in the invoicing routines for the air navigation

services to the Norwegian Armed Forces.

Depreciation and write-downs on the Group’s property,

plant and equipment totalled NOK 337 million in the

third quarter, compared with NOK 323 million for the

corresponding period last year.

The Group’s net finance costs in the third quarter were

NOK 88 million, compared with NOK 109 million for

the corresponding period last year. The profit is affected

by greater recognition of interest expenses related to

development projects in the balance sheet.

AS AT 3

rdQUARTER OF 2013

1The Group’s net finance costs in the second quarter were

NOK 90.1 million, compared with NOK 92.8

million for the corresponding period last year. The profit

is affected by greater recognition of interest

expenses on the balance sheet.

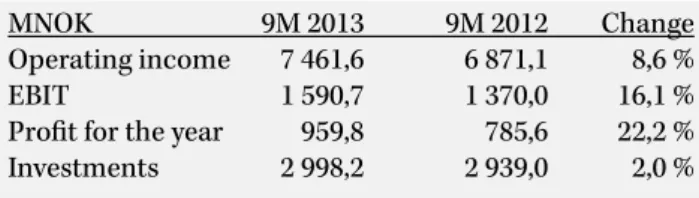

MNOK

9M 2013

9M 2012

Change

Operating income

7 461,6

6 871,1

8,6 %

EBIT

1 590,7

1 370,0

16,1 %

Profit for the year

959,8

785,6

22,2 %

Investments

2 998,2

2 939,0

2,0 %

Table 2: Key financial figures

1

Investments are defined as additions to the balance sheet for property, plant and equipment.

As at third quarter of 2013, the Group had a profit after

tax of NOK 960 million, compared with NOK 786 million

for the corresponding accounting period last year.

OPERATING INCOME

Operating income during the period 1 January to

30 September 2013 totalled NOK 7,462 million. In

comparison with the same period the prior year, this

represents a growth of 8.6 per cent and a growth in

operating income per passenger of 4.0 per cent.

Airport operations reported operating income of NOK

6,716 million, which is an increase of 8.6 per cent. The

growth was caused by continued business-related

development of commercial products and services. In

comparison with the corresponding period the prior year,

commercial income per passenger increased by 6.7 per

cent, whereas aviation income per passenger (excluding

security) decreased by 1.1 per cent.

The air navigation service reported an increase in

operating income of 0.4 per cent to NOK 1,432 million.

There was underlying growth in the traffic in number of

service units for the air navigation service, which was

counteracted by reduced prices. As at the third quarter,

traffic income per service unit was approximately 11.5

per cent lower, compared with the corresponding period

last year. This is attributed to a reduction in the fee rates.

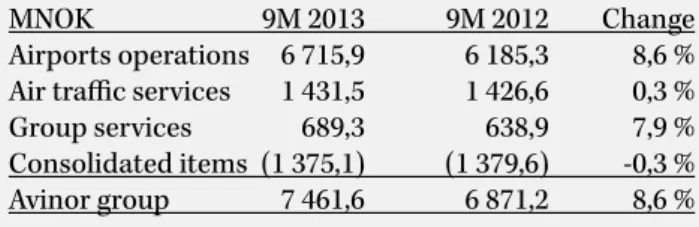

Operating income per business area is shown in table 3

below:

MNOK

9M 2013

9M 2012

Change

Airports operations 6 715,9

6 185,3

8,6 %

Air traffic services

1 431,5

1 426,6

0,3 %

Group services

689,3

638,9

7,9 %

Consolidated items (1 375,1)

(1 379,6)

-0,3 %

Avinor group

7 461,6

6 871,2

8,6 %

Table 3: Operating income

OPERATING EXPENSES AND DEPRECIATION

Operating expenses excluding depreciation and

write-downs totalled NOK 4,864 million, year to date this

year, in comparison with NOK 4,493 million last year.

Additional cost amounting to NOK 104 million related

to ensuring normal operation during construction of

Terminal 2 at Oslo Airport, have been reflected in the

accounts year to date this year. The corresponding figure

last year was NOK 111 million.

Depreciation and write-downs on the Group’s property,

plant and equipment totalled NOK 1,009 million year

to date, in comparison with NOK 991 million for the

corresponding period last year. The accounts reflect

NOK 80 million in accelerated depreciation year to

date in connection with the terminal 2 project. The

corresponding figure last year was NOK 101 million.

OPERATING PROFIT

The Group’s operating profit for the period from 1

January to 30 September 2013 totalled NOK 1,591 million,

compared with NOK 1,370 million for the corresponding

period in 2012. This results in an operating margin of

21.3 per cent this year, compared with 19.9 per cent last

year. Adjusted for the additional costs associated with

the Terminal 2 project, as well as changes in the value of

financial derivatives, the Group’s operating margin year

to date has been 23.8 per cent, in comparison with 23.0

per cent for the same period last year. This is attributed

primarily to the commercial activity that compensates

for the lower margins for the air navigation service.

FINANCIAL ITEMS AND TAX

The Group’s net financial costs for the period from

1 January to 30 September 2013 were NOK 257 million,

compared with NOK 278 million in the corresponding

period in 2012.

Increased borrowing expenses are partly compensated

for by increased capitalisation of borrowing cost on

investment projects.

Based on the expected tax rate on an annual basis, the

tax costs year to date are computed as being NOK 374

million.

INVESTMENTS

Recognised additions to property, plant and equipment

in the first nine months of the year amounted to NOK

2,998 million, compared with NOK 2,939 million for the

corresponding period last year.

The investments can be broken down into business areas

as follows:

MNOK

9M 2013

9M 2012

Change

Airports operations 2 777,0

2 822,2

-45,3

Air traffic services

71,8

37,5

34,3

Joint items, group

41,0

16,3

24,7

Consol idated items 108,4

63,0

45,4

Group

2 998,2

2 939,0

59,2

Table 4: Addition to PPE recognised in the balance sheet

A significant part of the investments undertaken year to

date this year are associated with the expansion project

for increased terminal capacity at the Oslo Airport

Gardermoen. Progress in the project is proceeding as

planned.

CASH FLOW AND FINANCING

Due to the investments exceeding the contribution

from ongoing operations, the Group had a cash flow for

the period from 1 January to 30 September 2013, prior

to changes in debt, of minus NOK 1,002 million. The

7

corresponding period last year was minus NOK 1,403

million. The Group’s total capital as at 30 September 2013

amounted to NOK 30.7 billion. Equity as a percentage of

the sum of equity and interest-bearing debt was 47.1 per

cent as at 30 September 2013. At the same point in time

last year, this ratio was 48.3 per cent.

The Group changed its assumptions for calculation

of the carrying amount of its pension obligations

as of 30 September 2013. In accordance with the

recommendation from the Norwegian Accounting

Standards Board, an interest rate based on covered

bonds has been chosen as the basis for the discount rate

that is applied to the calculation. New life expectancy

assumptions were also applied. This has had a net

positive effect of NOK 1,058 million on the book equity.

Interest-bearing debt as at 30 September 2013 totalled

NOK 13,389 million, and the debt has increased by

NOK 2,628 million since the end of the third quarter last

year.

As at 30 September 2013, the Group’s cash reserves

amounted to NOK 7,440 million, distributed between

NOK 2,540 million in bank deposits and NOK 4,900

million in unutilised bank overdrafts.

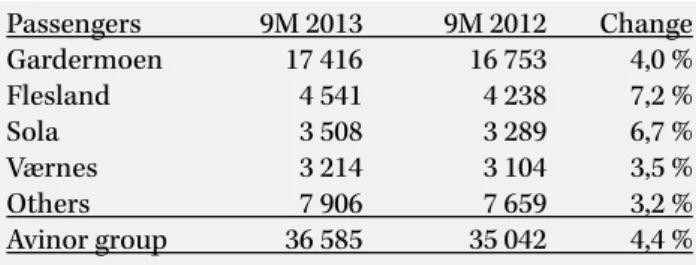

TRAFFIC DEVELOPMENT AND SERVICE GOALS

A total of 36.6 million passengers travelled through

Avinor’s airports during the first nine months of the year,

which is an increase of 4.4 per cent compared with the

corresponding period in 2012. The figure below shows the

trend in traffic on a quarterly basis for 2010–2013:

Passengers

(millions)

14

12

10

8

6

4

2

Q1 Q2 Q3 Q4

2010

2011

2012

2013

Since the financial crisis in 2008–2009, the air traffic has

experienced evenly balanced growth up to now. Traffic

volume as per third quarter has increased by 28 per cent

during the period 2009–2013.

In comparison with the corresponding period last

year, domestic traffic increased by 1.1 per cent, while

international traffic increased by 9.6 per cent. Domestic

traffic totalled 61.1 per cent of the total traffic volume as

per the third quarter. The volume of offshore helicopter

traffic increased 7.9 per cent compared with last year.

Passenger volume was distributed between the airports

as follows:

Passengers

9M 2013

9M 2012

Change

Gardermoen

17 416

16 753

4,0 %

Flesland

4 541

4 238

7,2 %

Sola

3 508

3 289

6,7 %

Værnes

3 214

3 104

3,5 %

Others

7 906

7 659

3,2 %

Avinor group

36 585

35 042

4,4 %

Table 5: No. of passengers

The number of commercial aircraft movements,

including offshore helicopters, increased by 1.6 per cent

in comparison with the corresponding period last year.

The traffic volume for the en route service measured

by the number of service units increased year to date

by 11.0 per cent in comparison with the corresponding

period for the preceding year. Punctuality for the past 12

months aggregated over all aircraft movements was 86

per cent. There is a continuous effort, in cooperation with

the airlines, to ensure a high degree of punctuality for

the passengers. The regularity was 98 per cent, which is

within the Group’s defined target. Avinor and the airlines

SAS, Norwegian and Widerøe have made provisions

for closer cooperation, and have signed an agreement

in which they have made commitments with regard to

regularity and punctuality.

AIR SAFETY AND HSE

No aviation accidents have been registered, with

or without personal injury, in which Avinor was a

participant year to date this year.

Overall, at the end of the third quarter of 2013 the Group

had an H1 value (lost time injury frequency rate) for the

past 12 months of 2.6. Avinor’s goal is to have an H1 value

of 3.0 or less.

Sick leave absences for the past 12 months for the Group

were 4.4 per cent, which is lower than the corresponding

period last year. The Group’s Inclusive Working Life target

for absence due to illness is 4.5 per cent or lower.

Through its own routines, Avinor discovered

unacceptable working conditions for a group of

construction workers working on the T2 development

project at Oslo Airport Gardermoen. Avinor has reported

this matter to the Labour Inspection Authority in

accordance with its internal routines and the current

legislation. The Labour Inspection Authority has

launched its own investigation. In addition, Avinor has

launched its own internal - survey to clarify whether it

is necessary for Avinor to prepare better routines and

guidelines in order to avoid such incidents in the future.

All known unfortunate living conditions are straightened

out with the general contractor.

RISKS

The Group’s operations are focused on safe air traffic

management with procedures and measures to minimise

both the risks and consequences of accidents and serious

incidents. In addition to aviation-related operating

conditions, the business is exposed to financial risk.

Regulatory developments are occurring continuously

in domestic and international aviation. The Group’s

continuous updating of operations to comply with new

provisions has financial consequences.

The Norwegian state has defined Avinor as a “category

4” company, i.e. a company with national sectoral policy

objectives. This entails, for example, that the Norwegian

state sets guidelines for a number of conditions,

including airport structure, emergency preparedness,

aviation fees and duties imposed by society. Depending

on the various political priorities, the scope and

organisation of sectoral policy guidelines may change

over time.

Avinor’s operations are characterised by long-term

investments in infrastructure. The management of

operations and emergency preparedness are largely

regulated by provisions and regulations. The Group

therefore has a high percentage of fixed operating costs

that vary to a limited extent with changes in traffic

volumes. The Group’s financial earnings and value

are therefore sensitive to traffic fluctuations, and for

downturns in traffic there is a risk of an impairment in

value with regard to property, plant and equipment on

the Group’s balance sheet.

Experience has shown that there is a correlation between

the general economic development and the demand

for air travel over time, while there may be significant

deviations in the short term.

Oslo Airport Gardermoen accounts for almost 50 per

cent of the Group’s operating income and is a key source

of funding for the rest of the airport network in Norway.

The airport’s earnings are exposed to economic cycles

and competition from other domestic and international

airports.

The Group’s traffic income and earnings are exposed to

future changes in the airlines’ schedules and production.

The majority of the Group’s receivables are from the

airlines and are not hedged.

Revenues from commercial offerings at the airports

are very important to the Group’s funding. Changes in

the framework conditions for these activities will have

a major impact on the Group’s earnings and financial

value.

The Group has financial risk in connection with foreign

currency, interest rates and energy prices. Financial

hedging instruments (derivatives) are used to limit risk.

The Group’s long-term debt to the Norwegian state is

exposed to changes in the interest rate on long-term

government bonds. A significant portion of the Group’s

other debt has fixed interest rates or is hedged by means

of financial derivatives.

When investing the Group’s surplus cash, emphasis

is given to the issuer’s solidity and the liquidity of the

investment. The Group’s liquid assets are deposited in a

bank on negotiated terms.

On 18 February 2011 a cooperation agreement was

signed between the Norwegian Armed Forces and Avinor,

which, with effect from 2 January 2010, will regulate the

distribution of costs and other conditions between the

parties where the Norwegian Armed Forces and Avinor

operate jointly. There continues to be disagreement

between the Norwegian Armed Forces and Avinor on the

understanding of the central points of the cooperation

agreement. In accordance with the provisions of the

cooperation agreement, disagreement may entail the

matter going to arbitration.

A petition for a discretionary court assessment to

determine the purchase price or an annual user fee for

aviation-critical areas that are owned by the Norwegian

Armed Forces at Flesland and Værnes airports has been

submitted to the court of appraisement.

Following the recommendation from the Government

(Proposition 73 S (–2011), the Storting resolved that

new fighter planes are to be based in Ørland with

the advanced base in Evenes. It has been resolved to

close down Bodø’s main air station. The change in the

Norwegian Armed Forces’ base structure alters the

present joint operations between civil and military

aviation in Bodø, and it will have considerable financial

consequences for Avinor’s future operating and

investment costs.

In connection with capacity expansions at Oslo Airport

Gardermoen, there is disagreement between the

Norwegian National Rail Administration and Avinor

regarding the development of the railway station and the

principles for the distribution of costs. Avinor is working,

in cooperation with The Ministry of Transport and

Communications, to find a solution to the disagreement.

9

In connection with the pension settlement in 2005, it was

determined that public service pensions shall be adjusted

for life expectancy and made subject to the new pension

adjustment rules. The life expectancy adjustment will

entail that employees will have to work longer in order

to achieve pension benefits corresponding to what has

been the case up until now. The rules for those who were

born after 1953 have, however, not been clarified, and are

therefore not accounted for.

The airports have discharge permits that require risk

assessments to identify potential sources of acute

pollution that represent a risk of damage to the external

environment.

Work is continuing on reducing the risk of incidents

that harm the environment occurring, while at the

same time existing pollution is being surveyed and

cleaned up. Environmentally hazardous additives in fire

extinguishing foam, which has spread to the natural

environment, have been detected at all the airports.

Work is currently being conducted to clarify the scope of

measures that will need to be implemented. As a basis for

this work, risk assessments have been conducted of the

potential harm to persons and the external environment

from these pollutants. The economic consequences of

this work depend on the extent of the localities that

require measures to be implemented, as well as the

authorities’ requirements and the measures available.

FUTURE PROSPECTS

Even though short-term incidents and traffic volume

fluctuations may arise, a continued strong demand for

air transport is expected in the long term in Norway.

For Avinor it is important to make provisions for an

infrastructure with a capacity and services that are

adapted to the needs of society so that our public

service mission is fulfilled in a satisfactory manner.

Future required investments exceed contributions from

on-going operations. To strengthen the Group’s financial

capacity and reduce financial risk, Avinor has previously

requested an equity issue. In order to ensure robust

financial conditions adapted to required investment,

Avinor will continue the dialog with The Ministry of

Transport and Communications.

Focus on customer orientation and earnings

improvement is important to Avinor. Strengthened

financial earnings are required in order to ensure a stable

basis for continuous operations.

Oslo, 21 November 2013

Board of Directors of Avinor AS

Avinor Group

Balance sheet

31 December 31 December

2012 2012 2013 All amounts in MNOK Notes 2013 2012 2012

ASSETS

Non-current assets

2 238,9

2 130,5 1 719,1 Deferred tax assets 9 1 782,6 2 342,4 2 577,4 46,4

50,1 35,1 Other intangible assets 4 35,1 50,1 46,4 10 851,3

10 325,8 11 813,0 Property, plant and equipment 4 24 807,4 22 011,5 22 807,8 22,7

12,2 - Derivative financial instruments 7,8 12,4 22,9 3 877,0

3 269,9 4 969,8 Other financial assets 130,9 64,5 79,0 17 036,3

15 788,5 18 537,0 Total non-current assets 26 763,8 24 480,9 25 533,5

Curent assets

1 255,9

983,8 1 108,3 Inventories, trade and other receivables 1 417,7 1 291,3 1 258,6 0,2

0,1 - Derivative financial instruments 0,1 0,1 1,4 1 289,3

1 694,5 2 503,2 Cash and cash equivalents 2 540,1 1 719,5 1 315,7 2 545,4

2 678,4 3 611,5 Total current assets 3 957,9 3 010,9 2 575,7 19 581,7

18 466,9 22 148,5 TOTAL ASSETS 30 721,7 27 491,8 28 109,2

EQUITY AND LIABILITIES Equity 5 400,1 5 400,1 5 400,1 Restricted equity 5 400,1 5 400,1 5 400,1 3 169,9 2 724,9 4 048,0 Retained earnings 6 533,9 4 686,2 4 956,6 8 570,0 8 125,0 9 448,1 Total equity 11 934,0 10 086,3 10 356,7 Provisions 3 315,0

3 552,7 2 256,8 Retirement benefit obligations 2 521,0 4 127,9 3 875,1 159,1 159,8 159,1 Other provisions 190,1 190,8 190,2 3 474,1 3 712,5 2 415,9 Total provisions 2 711,1 4 318,7 4 065,3 Non-current liabilities - - State loan 5 4 082,6 4 527,0 4 304,8 22,4

23,1 18,2 Derivative financial instruments 112,1 144,0 142,8 4 345,8

4 379,6 6 317,1 Other non-current liabilities 5 7 589,7 5 718,1 5 662,2 4 368,2

4 402,7 6 335,3 Total non-current liabilities 11 784,4 10 389,1 10 109,8

Current liabilities

700,0

- 1 200,0 Commercial papers 1 200,0 - 700,0 4,9

5,5 13,3 Derivative financial instruments 17,9 11,1 11,2 2 464,5

2 221,2 2 735,9 Other current liabilities 5 3 074,3 2 686,6 2 866,2 3 169,4

2 226,7 3 949,2 Total current liabilities 4 292,2 2 697,7 3 577,4 11 011,7

10 341,9 12 700,4 Total liabilities 18 787,7 17 405,5 17 752,5 19 581,7

18 466,9 22 148,5 TOTAL EQUITY AND LIABILITIES 30 721,7 27 491,8 28 109,2

Avinor Group

30 September

Avinor AS

30 September

11

Avinor Group

Income statement

Year All amounts in MNOK Notes 2013 2012 2013 2012 2012

Operating income

Traffic income 1 366,5 1 244,5 3 800,5 3 612,5 4 755,8 Other operating income 1 394,0 1 255,8 3 661,1 3 258,6 4 396,3

Total operating income 2 760,5 2 500,3 7 461,6 6 871,1 9 152,1

Operating expenses

Raw materials and consumables used 42,7 51,5 118,2 111,0 142,6 Employee benefits expense 7,8 897,1 836,2 2 470,7 2 301,1 3 172,8 Depreciation, amortisation and impairment charges 4,7 336,6 322,7 1 008,9 991,2 1 335,7 Other operating expenses 7 765,4 673,5 2 275,5 2 080,6 2 918,5

2 041,8

1 883,9 5 873,3 5 483,9 7 569,6

718,7

616,4 1 588,3 1 387,2 1 582,5 Changes in value and other (losses)/gains, net 8,7 (1,7) 2,4 (17,2) (20,3)

Operating profit/(loss) 727,4 614,7 1 590,7 1 370,0 1 562,2

Net finance income/(costs) (88,1) (109,3) (257,1) (277,7) (355,9)

Profit/(loss) before income tax 639,3 505,4 1 333,6 1 092,3 1 206,3 Income tax expense 9 179,1 141,6 373,8 306,7 351,6

Profit/(loss) for the third quarter 460,2 363,8 959,8 785,6 854,7

Avinor AS

Income statement

Year All amounts in MNOK Notes 2013 2012 2013 2012 2012

Operating income

Traffic income 858,5 784,3 2 401,9 2 305,4 3 041,9 Other operating income 725,6 651,7 1 939,0 1 691,3 2 275,8

Total operating income 1 584,1 1 436,0 4 340,9 3 996,7 5 317,7

Operating expenses

Raw materials and consumables used 29,1 41,3 82,8 76,8 96,7 Employee benefits expense 8 760,4 703,4 2 078,1 1 936,3 2 665,2 Depreciation, amortisation and impairment charges 155,3 153,6 469,7 456,2 624,1 Other operating expenses 536,9 444,8 1 556,1 1 358,3 1 946,3

1 481,7

1 343,1 4 186,7 3 827,6 5 332,3

102,4

92,9 154,2 169,1 (14,6) Changes in value and other (losses)/gains, net 5,4 (0,5) 4,5 (12,6) (13,5)

Operating profit/(loss) 107,8 92,4 158,7 156,5 (28,1)

Net finance income/(costs) (0,9) (0,3) 541,9 38,3 438,0

Profit/(loss) before income tax 106,9 92,1 700,6 194,8 409,9 Income tax expense 9 30,0 25,8 196,2 54,5 16,2

Profit/(loss) for the third quarter 76,9 66,3 504,4 140,3 393,7 Nine months ended September

Nine months ended September

Total operating expenses before changes in value and other losses/gains, net

Operating profit/(loss) before changes in value and other losses/gains, net

Total operating expenses before changes in value and other losses/gains, net

Operating profit/(loss) before changes in value and other losses/gains, net

Third quarter

Third quarter

Avinor Group

Statement of comprehensive income

Year Year

2012 2012 2013 All amounts in MNOK 2013 2012 2012 393,7

140,3 504,4 Profit/(loss) for the first quarter 959,8 785,6 854,7 (560,4)

(826,6) 1 163,0 Actuarial gains/(losses) on post employment benefit obligations 1 470,0 (957,4) (677,5) 156,9

231,4 (326,0) Tax effect (412,0) 268,1 189,7 19,3

19,3 - Cash flow hedges 31,8 (3,4) (3,7) (5,4) (5,4) - Tax effect (8,9) 0,9 1,1 (389,6) (581,2) 837,0 1 080,9 (691,8) (490,4) 4,1 (440,9) 1 341,4 2 040,7 93,8 364,3 Attributable to: 4,1

(440,9) 1 341,4 Owners of the parent 2 040,7 93,8 364,3

Avinor Group

Statement of changes in equity

Other Other

All amounts in MNOK Share capital reserves equity Total equity Balance at 1 Januar 2012 5 400,1 (828,7) 5 842,9 10 414,3

(691,8)

785,6 93,8 Dividends provided for or paid (421,8) (421,8) Balance at 30 September 2012 5 400,1 (1 520,5) 6 206,7 10 086,3

Balance at 1 Januar 2013 5 400,1 (1 319,2) 6 275,8 10 356,7 1 080,9

959,8 2 040,7 Dividends provided for or paid (463,4) (463,4) Balance at 30 September 2013 5 400,1 (238,3) 6 772,2 11 934,0

Avinor AS

Statement of changes in equity

Other Other

All amounts in MNOK Share capital reserves equity Total equity Balance at 1 Januar 2012 5 400,1 (703,4) 4 291,0 8 987,7

(581,2)

140,3 (440,9) Dividends provided for or paid (421,8) (421,8) Balance at 30 September 2012 5 400,1 (1 284,6) 4 009,5 8 125,0

Balance at 1 Januar 2013 5 400,1 (1 093,0) 4 262,9 8 570,0 837,0

504,4 1 341,4 Dividends provided for or paid (463,4) (463,4) Balance at 30 September 2013 5 400,1 (256,0) 4 303,9 9 448,1

Other comprehensive income, net of tax

Nine months ended September

Avinor Group

Other comprehensive income

Total comprehensive income

Avinor AS

Nine months ended September

Items not to be reclassified to profit or loss in subsequent

Total comprehensive income Total comprehensive income

Total comprehensive income

Total comprehensive income

13

Avinor Group

Statement of comprehensive income

Year Year

2012 2012 2013 All amounts in MNOK 2013 2012 2012 393,7

140,3 504,4 Profit/(loss) for the first quarter 959,8 785,6 854,7 (560,4)

(826,6) 1 163,0 Actuarial gains/(losses) on post employment benefit obligations 1 470,0 (957,4) (677,5) 156,9

231,4 (326,0) Tax effect (412,0) 268,1 189,7 19,3

19,3 - Cash flow hedges 31,8 (3,4) (3,7) (5,4) (5,4) - Tax effect (8,9) 0,9 1,1 (389,6) (581,2) 837,0 1 080,9 (691,8) (490,4) 4,1 (440,9) 1 341,4 2 040,7 93,8 364,3 Attributable to: 4,1

(440,9) 1 341,4 Owners of the parent 2 040,7 93,8 364,3

Avinor Group

Statement of changes in equity

Other Other

All amounts in MNOK Share capital reserves equity Total equity Balance at 1 Januar 2012 5 400,1 (828,7) 5 842,9 10 414,3

(691,8)

785,6 93,8 Dividends provided for or paid (421,8) (421,8) Balance at 30 September 2012 5 400,1 (1 520,5) 6 206,7 10 086,3

Balance at 1 Januar 2013 5 400,1 (1 319,2) 6 275,8 10 356,7 1 080,9

959,8 2 040,7 Dividends provided for or paid (463,4) (463,4) Balance at 30 September 2013 5 400,1 (238,3) 6 772,2 11 934,0

Avinor AS

Statement of changes in equity

Other Other

All amounts in MNOK Share capital reserves equity Total equity Balance at 1 Januar 2012 5 400,1 (703,4) 4 291,0 8 987,7

(581,2)

140,3 (440,9) Dividends provided for or paid (421,8) (421,8) Balance at 30 September 2012 5 400,1 (1 284,6) 4 009,5 8 125,0

Balance at 1 Januar 2013 5 400,1 (1 093,0) 4 262,9 8 570,0 837,0

504,4 1 341,4 Dividends provided for or paid (463,4) (463,4) Balance at 30 September 2013 5 400,1 (256,0) 4 303,9 9 448,1

Other comprehensive income, net of tax

Nine months ended September

Avinor Group

Other comprehensive income

Total comprehensive income

Avinor AS

Nine months ended September

Items not to be reclassified to profit or loss in subsequent

Total comprehensive income Total comprehensive income

Total comprehensive income

Total comprehensive income

Avinor Group

Statement of cash flows

Year Year

2012 2012 2013 All amounts in MNOK 2013 2012 2012

Cash flow from operating activities

409,9

194,8 700,6 Profit before income tax 1 333,6 1 092,3 1 206,3 (13,4)

(13,4) (13,5) Income tax paid (225,8) (350,0) (351,7) 57,5

43,7 50,9 Interest received 52,5 44,2 58,2 (1,5)

(2,8) (5,7) (Profit)/loss on disposals of non-current assets (4,2) (1,9) 3,5 624,1

456,2 469,7 Depreciation 1 008,9 991,2 1 335,7 (438,0)

(38,3) (541,9) Net finance income/costs 257,1 277,7 355,9 23,1

271,4 539,2 Other changes 75,4 (274,2) (25,5) 661,7

911,6 1 199,3 Net cash generated from operating activities 2 497,5 1 779,3 2 582,4

Cash flow from investing activities

(2 074,1)

(1 384,9) (1 379,9) Investments in property, plant and equipment (PPE) (2 786,3) (2 598,9) (3 914,7) 11,0

9,2 5,3 Proceeds from sale of PPE, incl assets under construction 5,5 10,0 13,2 (1 250,0)

(650,0) (1 050,0) Loans to subsidiaries - - -108,5

(6,6) 38,2 Interest received from subsidiaries - - -451,2

- 565,9 Net group contributions - - -(7,1)

- (22,2) (22,2) - (5,9) (2 760,5)

(2 032,3) (1 842,7) (2 803,0) (2 588,9) (3 907,4)

Cash flow from financing activities

2 207,8

1 540,3 3 650,0 Proceeds from borrowings 3 650,0 1 540,3 2 207,8 (254,4) (254,0) (1 158,0) Repayment of borrowings (1 423,9) (527,5) (772,2) (207,6) (113,4) (142,1) Interest paid (203,6) (171,7) (482,9) - (29,2) Borrowing costs (29,2) -(421,8)

(421,8) (463,4) Dividends paid to shareholder (463,4) (421,8) (421,8) 1 324,0 751,1 1 857,3 1 529,9 419,3 530,9 (774,8) (369,6) 1 213,9 1 224,4 (390,3) (794,1) 2 064,1 2 064,1 1 289,3 1 315,7 2 109,8 2 109,8 1 289,3 1 694,5 2 503,2 2 540,1 1 719,5 1 315,7

Net cash used in investing activities

Net cash generated/used in financing activities

Avinor Group

Nine months ended September

Avinor AS

Nine months ended September

Net (decrease)/increase in cash, cash equivalents and bank overdrafts

Cash, cash equivalents and bank overdrafts at beginning of year

Change in other investments

Cash, cash equivalents and bank overdrafts at end of the third quarter

15

Avinor Group

Notes to the interim financial statements

Note 1 - General information

Avinor AS and its subsidiaries (together 'the group') own, manage and develop aviation infrastructure and systems by facilitating safe and efficient aviation. The group also renders services within the same areas together with other activities that add to the group's main business, including commercial development.

The Avinor group's headquarters are located in Oslo.

The interim financial information was approved for issue on 21 November 2013. The interim financial information has not been audited.

Note 2 - Basis of preparation and accounting policies

The interim financial statement for Avinor AS and Avinor Group for the third quarter, ended 30 September 2013, has been prepared in accordance with International Financial Reporting Standards (IFRS) and encompasss Avinor AS and all its subsidiaries.

The interim financial information has been prepared in accordance with IAS 34 Interim financial reporting. The interim financial information should be read in conjunction with the annual financial statement for the year ended 31 December 2012.

The accounting policies are consistent with those of the annual financial statement for the year ended 31 December 2012, except for the adoption of new standards effective as of 1 January 2013.

New standards, interpretations and amendments adopted by the group:

IAS 1 Presentation of Items of Other Comprehensive Income.

The amendments to IAS 1 introduce a grouping of items presented in other comprehensive income (OCI). Items that could be reclassified (or recycled) to profit or loss at a future point in time now have to be presented separately from items that will never be reclassified. The amendment affected presentation only and had no impact on the Group's financial position or performance.

IAS 19 Employee Benefit (Revised 2011).

IAS 19R includes a number of amendments to the accounting of defined benefits plans, including actuarial gains and losses that are now recognised in other comprehensive income (OCI) and permanently excluded from profit and loss; unvested past service costs are now recognised in profit and loss at the earlier of when the amendments occurs or when related restructuring or termination costs are recognised, and; expected returns on plan assets that are no longer recognised in profit and loss instead, there is a requirement to recognise interest on the net defined liability (asset) in profit and loss, calculated using the discount rate used to measure the defined bebefit obligation.

In case of the Group , the transition to IAS 19R had an impact on the net defined benefit obligations due to the difference in accounting for interest on plan assets. The effect of the adoption of IAS 19R is explained in Note 8.

Note 3 - Segment information

Avinor Group

Other Medium Air Oslo large and small Navigation

All amounts in MNOK Airport airports airports Services Others Elimination Total

Nine months ended 30 September 2013:

Traffic income 1 398,6 1 028,4 669,0 704,9 (0,5) 3 800,5 Other income 2 127,6 917,0 434,8 178,1 3,5 3 661,1 Inter-segment income 60,0 60,3 20,1 548,5 686,3 (1 375,1) -Total income 3 586,2 2 005,8 1 123,9 1 431,5 689,3 (1 375,1) 7 461,6 Employee benefits expenses 392,6 253,4 609,9 996,8 218,1 2 470,7 Depreciation and amortisation 504,2 168,6 242,4 67,5 25,7 1 008,4 Other operating expenses 820,4 373,7 711,5 266,7 219,0 2 391,3 Inter-segment expenses 487,2 293,5 395,6 72,6 126,1 (1 375,1) -Total expenses 2 204,4 1 089,3 1 959,3 1 403,6 588,9 (1 375,1) 5 870,4

1 381,8

916,5 (835,4) 27,8 100,4 - 1 591,2

Group adjustments depreciation (a) 136,3 (49,4) (86,7) - (0,8) (0,5) Group adjustments lease (b) 291,9 (291,9)

-Operating profit/(loss) 1 810,0 867,1 (922,1) 27,8 (192,3) - 1 590,7

Assets* 8 502,4 4 407,7 5 470,6 599,0 136,5 19 116,2

Net income/(expense)

Avinor Group

Notes to the interim financial statements

Note 3 - Segment information continued

Avinor Group

Other Medium Air Oslo large and small Navigation

All amounts in MNOK Airport airports airports Services Others Elimination Total

Nine months ended 30 September 2012:

Traffic income 1 307,1 954,2 633,0 718,2 - 3 612,5 Other income 1 969,5 788,0 384,1 114,4 2,5 3 258,6 Inter-segment income 55,9 66,8 26,6 593,9 636,4 (1 379,6) 0,0 Total income 3 332,6 1 809,0 1 043,7 1 426,6 638,9 (1 379,6) 6 871,1 Employee benefits expenses 364,7 233,0 575,7 917,6 210,1 2 301,1 Depreciation and amortisation 487,4 156,6 233,3 68,6 32,0 978,0 Other operating expenses 822,6 349,5 593,0 239,9 203,9 2 208,8 Inter-segment expenses 480,6 278,4 464,0 81,8 74,9 (1 379,6) (0,0) Total expenses 2 155,3 1 017,5 1 865,9 1 307,9 520,8 (1 379,6) 5 487,9

1 177,2

791,5 (822,2) 118,7 118,1 - 1 383,2

Group adjustments depreciation (a) 123,6 (49,4) (86,7) - (0,7) (13,2) Group adjustments lease (b) 291,2 (291,2)

-Operating profit/(loss) 1 592,0 742,1 (908,9) 118,7 (173,8) - 1 370,0

Assets* 7 303,3 4 237,6 5 114,7 652,0 152,7 17 460,3 (a) Group adjustments due to assessment of the opening balance as at 1 January 2003.

(b) The lease on the land at Gardermoen is attributed to Oslo Lufthavn AS in the segment reporting. * Inclusive other intangible assets, exclusive assets under construction.

Note 4 - Property, plant and equipment, other intangible assets

Other intangible assets Property, plant and equipment Assets under construction Total Other intangible assets Property, plant and equipment Assets under construction Total At 30 September 2012

Opening net book amount 61,4 7 389,4 1 814,5 9 265,3 61,4 16 889,7 3 170,8 20 121,9

Additions - 883,1 1 573,1 2 456,2 - 1 508,4 2 939,0 4 447,4

Reclassification - - 883,1 883,1 - - 1 508,4 1 508,4

Disposals - 6,3 - 6,3 - 8,1 - 8,1

Depreciation charge 11,3 444,9 - 456,2 11,3 979,9 - 991,2

Closing net book amount 50,1 7 821,3 2 504,5 10 375,9 50,1 17 410,1 4 601,4 22 061,6 At 30 September 2013

Opening net book amount 46,4 8 589,6 2 261,7 10 897,7 46,4 18 255,5 4 552,3 22 854,2

Additions - 390,7 1 420,9 1 811,6 - 1 824,1 2 998,2 4 822,3

Reclassification - - 390,7 390,7 - - 1 824,1 1 824,1

Disposals - 0,7 - 0,7 - 0,9 - 0,9

Depreciation charge 11,3 458,5 - 469,7 11,3 997,7 - 1 008,9

Closing net book amount 35,1 8 521,1 3 291,9 11 848,2 35,1 19 081,0 5 726,4 24 842,5 Measurement of recoverable amount

There are no significant changes affecting the recoverable amount of the group's assets in 2013. All amounts in MNOK

Avinor AS Avinor Group Net income/(expense)

17

Avinor Group

Notes to the interim financial statements

Note 5 - Borrowings

All amounts in MNOK 2013 2012 2013 2012

Non-current 6 317,1 4 379,6 11 672,3 10 245,1 Current 1 203,2 2,7 1 716,3 515,9 Total 7 520,3 4 382,3 13 388,6 10 761,0

Movement in borrowings

Opening net book amount 5 053,6 3 100,7 11 187,9 9 752,9 Proceeds from borrowings 3 650,0 1 540,3 3 650,0 1 540,3 Repayment of borrowings (1 158,0) (254,0) (1 423,9) (527,5) Changes in value (25,3) (4,7) (25,3) (4,7) Closing net book amount 7 520,3 4 382,3 13 388,6 10 761,0 Avinor AS has issued bond loans noted on the Stock Exchange with a total nominal value of MNOK 2,450, lending date 22 April 2013. In connection with the issue, Avinor AS has redeemed parts of the bond loan from 2009, redemtion amount MNOK 453.

Liquidity reserves

All amounts in MNOK 2013 2012 2013 2012

Cash and cash equivalents 2 503,2 1 694,5 2 540,1 1 719,5 Unused bank overdraft 800,0 300,0 800,0 300,0 Unused credit facility 4 000,0 2 000,0 4 000,0 2 000,0 Unused drawing right (Ministry of Transport and Communication) - - 100,0 100,0 Total 7 303,2 3 994,5 7 440,1 4 119,5 The group has sufficient headroom to enable it to conform to covenants on existing borrowings and sufficient funds to service this years planned investments. 30 September Avinor AS 30 September Avinor AS 30 September Avinor Group 30 September Avinor Group

Avinor Group

Notes to the interim financial statements

Note 6 - Financial instruments Fair value estimation

The fair value of foreign exchange forward contracts and financial power forward contracts is based on market value at the balance sheet date. The fair value of all interest rate swaps is confirmed by the financial institutions which are the company's opposite party in the financial contracts entered into.

The carrying amount of cash and bank overdrafts is approximately equal to the fair value of these instruments as they fall due in a short period of time. Similarly, the carrying amount of receivables and payables is approximately equal to fair value as they are entered into under "normal" conditions. The fair value of long-term debt is based on quoted market prices or on the interest rates for debt with corresponding terms and similar credit risk. The fair value of commercial papers equals principal amount as at 30 September 2013.

Below is a comparison of the carrying amounts and fair values of Avinor AS and the group's interest-bearing debt.

All amounts in MNOK

Interest-bearing debt Fair value Fair value

State loan - - 4 527,0 4 584,8 Bonds 3 246,5 3 380,9 3 246,5 3 380,9 Bank borrowings 3 025,3 3 215,2 4 366,7 4 556,7 Commercial papers 1 200,0 1 200,0 1 200,0 1 200,0

The table below shows financial instruments at fair value by level of the following fair value measurement hierarchy: *Quoted prices (unadjusted) in active markets for identical assets or liabilities (level 1).

*Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices) (level 2).

*Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs) (level 3). The following table presents the group’s assets and liabilities that are measured at fair value at 30 September 2013:

Level 1 Level 2 Level 3 Total Assets

Financial assets at fair value through profit or loss 0,0 1,3 0,0 1,3 Derivatives used for hedging 0,0 6,6 0,0 6,6

Total assets 0,0 7,9 0,0 7,9 Liabilities

Financial liabilities at fair value through profit or loss 13,4 22,7 0,0 36,1 Derivatives used for hedging 0,0 93,9 0,0 93,9

Bonds 0,0 0,0 0,0 0,0

Total liabilities 13,4 116,6 0,0 130,0

Note 7 - Impact on earnings - Terminal 2 project

As a result of the development of Gardermoen (Terminal 2 project) the income statement includes charges for extra costs related to the mainenance of normal operations during the construction period, as well as costs related to the scrapping of assets, including higher depreciation as a result of re-assessed economoc life.

Specification

Year All amounts in MNOK 2013 2012 2013 2012 2012 Employee benefits expense 12,1 10,1 32,6 26,0 35,5 Depreciation, amortisation and impairment charges 16,4 24,3 79,7 101,3 132,0 Other operating expenses 14,9 52,3 71,3 84,5 140,5 Sum 43,4 86,7 183,6 211,8 308,0

Avinor AS Avinor Group

30 September 30 September

Carrying amount Carrying amount

Nine months ended September Third quarter

19

Avinor Group

Notes to the interim financial statements

Note 8 - Employee benefits

IAS 19R has been applied retrospectively from 1 January 2012. As a result, expected returns on plan assets of defined benefit plans are not recognised in profit or loss. Instead, interest on net defined obligation is recognised in profit or loss, calculated using the discount rate used to measure the net pension obligation.

The adoption of IAS 19R results in an increased pension cost of approximately 100 MNOK for the group and 90 MNOK for the parent company in 2012.

Spesification of impact MNOK Nine months ended Nine months ended

September Year September Year

2012 2012 2012 2012

Income statement:

Employee benefits expense 67,5 90,0 75,0 100,0 Income tax expense (18,9) (25,2) (21,0) (28,0) Profit/(loss) for the first quarter/year (48,6) (64,8) (54,0) (72,0) 30 September Year 30 September Year

2012 2012 2012 2012

Equity:

Actuarial gains on post employment benefit obligations 67,5 90,0 75,0 100,0 Tax effect (18,9) (25,2) (21,0) (28,0) Net actuarial gains on post employment benefit obligations 48,6 64,8 54,0 72,0

Net impact on equity:

Other reserves 48,6 64,8 54,0 72,0 Other equity (48,6) (64,8) (54,0) (72,0) Total - - -

-at the end of the prior financial year. In this calcul-ation the discount r-ate was determined based on the interest r-ate of Norwegian St-ate oblig-ations. The Norwegian Accounting Standards Board have in their latest guidance accepted that a discount rate based on the Norwegian covered bonds market may be used as a basis for the calculation.

Based on this the Avinor group has as at 30 September 2013 used the discount rate based on the Norwegian covered bonds market in calculating the obligation. The effect of this is a reduction in the obligation. At the same time the new mortality table, called K2013, is also used in the calculation of the pension obligation. The effect of this is a increase in the obligation. The total effect is presented in the Statement of comprehensive income.

Note 9 - Income tax expense

The income tax expense is calculated using the expected annual effective tax rate.

The Norwegian Government presented on 8 November 2013 a proposal to reduce the annual tax rate from 2014. The proposal will result in a reduction of the deferred tax asset by approximately 70-80 MNOK and a an corresponding increase in the income tax expense in 2013.

Note 10 - Dividends

Dividends related to the annual financial statement for the year ended 31 December 2012 of 463,4 MNOK were disbursed in July 2013.

In accordance with IAS 34 the pension cost for the interim period is calculated at year-to-date basis by using the actuarially determined pension cost rate