The Ctrack Vehicle Tracking Survey 2011 was

conducted amongst 250 fleet influencers and

decision makers within the UK who are

responsible for car, van, truck or mixed fleet

operations.

The survey is designed to provide insight into

the uptake of vehicle tracking amongst

UK-based businesses, how the technology is

being used, what benefits are being

achieved and what barriers are preventing

more companies adopting a solution.

EXECUTIVE SUMMARY

Key findings include:

l Vehicle tracking is becoming a critical operational tool for many fleets, especially van and commercial

vehicle operators, with more than 70% of those utilising the technology having used it for more than four years.

l Fleet operators are achieving measurable cost efficiencies with significant reductions in fuel usage (8.6%), overtime claims (15.3%) and communications overheads (13.3%).

l The reputation of the vehicle tracking industry is generally good according to 70% of respondents, but some concerns remain around the financial viability of providers, overselling and the reliability of the industry.

l There is still a proportion of fleet operators not currently using vehicle tracking that are unconvinced about the potential benefits, but more than half of those yet to adopt the technology believe it can provide return on investment.

l Fuel costs and pressures to reduce operational overheads are currently the key challenges for a large number of fleet operators, with many using vehicle tracking to help overcome these issues.

Key findings in the report included:

There is considerably greater use of vehicle tracking for vans,and to a lesser extent heavy goods vehicles, than cars according to the respondents utilising the technology. In fact, four fifths of respondents tracked vans compared to just a third for cars, perhaps reflecting a more established and proven business case for van operators. Elsewhere, there still remains a low level of uptake for unpowered assets such as trailers and plant. (Fig 1)

The findings suggest that vehicle tracking has become embedded within many companies’ fleet operations, with over 70% having used the technology for more than four years and almost 5% for over 10 years. Just under 5% of fleets have adopted vehicle tracking in the past 12 months representing continued year-on-year growth in uptake. Meanwhile, the advances in the functionality of web-based tools, combined with the affordability of this type of system when compared to server-based solutions, has meant that they now account for more than half of all active tracking systems. A further 25% of tracking solutions now use a combination of server-and web-based systems, often to achieve added flexibility and support multi-user requirements. (Fig 2)

It seems that fleet operators are increasingly combining their tracking solutions with in-vehicle tools to maximise the operational performance of the system. In

particular, integrated satellite navigation is now used in 53% of all tracking systems to support improved routing, reduced mileage and enhanced workflow. Elsewhere, Driver Identification (24%), handheld PDAs or terminals (7%) and panic alarms (7%) are also being utilised to a lesser extent.

In addition, many companies are integrating vehicle tracking with other back office management systems in order to streamline their operations and automate internal processes. (Fig 3)

37%

3%

33%

4%

9%

37% 13%

11%

Fleet

Supply chain

Workflow

Contract

Fuel

Routing & scheduling

Personnel/HR

Accounting

34%

82% 53%

4%

7%

2%

Car

Van

Commercial vehicle

Trailers

Plant

Other

1

The adopters

Figure 3

Integration with back office

management systems

(% of VT users)Figure 2

Tracking system types in use

(% of VT users)

Figure 1

Tracked assets and vehicles in the UK

(% of VT users)Web-based (access via the Internet with no software) 55.4%

Server-based (access via software on internal IT system)

19.6%

Mix of both

In terms of the primary purpose for using vehicle tracking, productivity (36%), cost reduction (16%), asset management (15%) and customer service (14%) are the most common reasons, although security, health and safety and legislative compliance also featured in the responses. However, fleets are now achieving a wide range of business and operational benefits that are delivering real return on investment. (Fig 4)

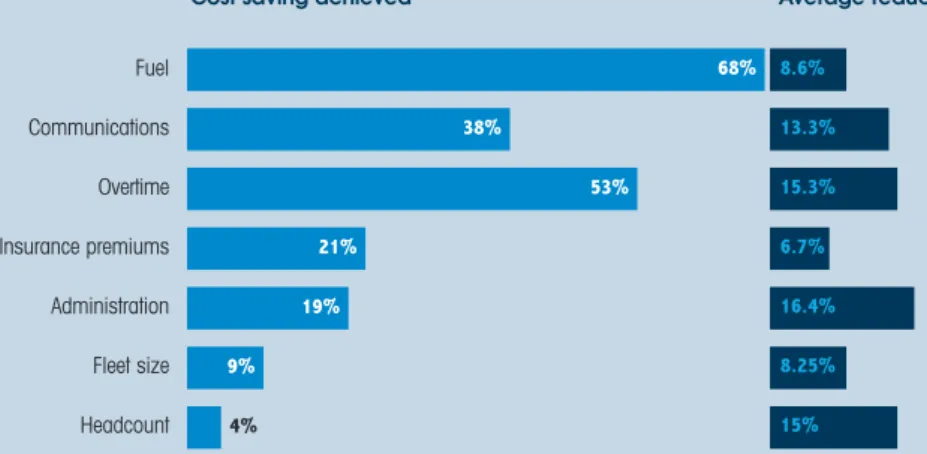

Of the respondents that stated that their fleet operations had achieved reduced costs, a wide range of savings are consistently being achieved. For example, more than two-thirds have lowered fuel costs by an average of 8.6%, whilst over half have reduced overtime claims by an average of 15.3%. (Fig 5)

2

Vehicle tracking in action

1%

9% 12%

33% 13%

No value added to the business

Meeting tender requirements

Reduced environmental impact

Improved duty of care

Reduced accidents

47%

Added understanding of driver behaviour

46%

Increased security

43%

Proof of delivery or completion of work

17%

Greater business insight

42%

Improved customer service

43%

Enhanced workflow management

59%

Increased productivity

70%

Reduced costs

Figure 4

Business and operational benefits

(% of VT users)68% 38%

53% 21%

19% 9%

4%

Fuel

Communications

Overtime

Insurance premiums

Administration

Fleet size

Headcount

8.6% 13.3% 15.3% 6.7% 16.4% 8.25% 15%

Figure 5

Operational savings

(VT users that have reduced costs)In the main, businesses are satisfied with their vehicle tracking partner, with 83% saying they are happy with the service and technology provided by their current supplier. In fact, more than three quarters of those using vehicle tracking have only used a single provider to date. (Fig 6)

However, more than one in five fleet operators have used multiple providers with some having switched as many as five times. Of those that have used more than one tracking company, 60% have changed in the past two years, whilst a further 32.5% have switched in the last three to five years. There are a mix of reasons for businesses changing their tracking partners, with the most common being linked to poor service delivery (37.5%). Other reasons included cost (15%), functionality (15%), supplier went out of business (15%) and technology (12.5%).

Meanwhile, when asked about the reputation of the vehicle tracking industry, 70% of all respondents thought it was good. Despite this seemingly positive perception, more than 40% of those not using tracking technology disagreed and believed the sector overall had a poor image. The main reasons for this was the financial viability of providers (34%), reliability (25%), overselling (21%) and credibility of technology (18%). (Fig 7)

3

Vehicle tracking industry

74% 26% 57% 43%

70% 30%

VT user

Non-VT user

Overall

Figure 6

Number of tracking partners used

(% of VT users)

Figure 7

Reputation of vehicle tracking industry

(%) Good Bad1 77.7%

2–3

18.5%

4–5

3.3%

>5

28% 10%

17% 28% 15%

No benefits

Meeting tender requirements

Reduced environmental impact

Improved duty of care

Reduced accidents

39%

Added understanding of driver behaviour

35%

Increased security

33%

Proof of delivery or completion of work

20%

Greater business insight

26%

Improved customer service

25%

Enhanced workflow management

35%

Increased productivity

39%

Reduced costs

Figure 9

Potential benefits of vehicle tracking

(%) The respondents outlined a range of reasons that werepreventing them from adopting vehicle tracking with almost 30% claiming it did not meet business or operational needs. Other reasons include lack of budget (18.8%), too expensive (8.7%), need for more information (8.7%) and employee concerns (5.8%).

Despite reluctance amongst some fleet operators, 57% believed that vehicle tracking did offer return on investment and 86% were familiar with the benefits the technology can achieve. When asked how vehicle tracking could help their fleets, the respondents gave a range of benefits, with

reduced costs, increased productivity, enhanced security and added understanding of driver behaviour coming out top. (Fig 9)

Amongst those respondents not using vehicle tracking within their fleet operation, 64% had previously considered using the technology and 51% believed that it could benefit their business. This split in the perceived value of vehicle tracking is further underlined by the expected timescale for the

adoption of the technology. Almost 45% of these respondents thought they would implement a tracking solution within two years, whilst just under 50% had no plans to do so in the next five years. (Fig 8)

4

The non-adopters

23.1% 21.8%

5.9%

21.7% 27.5%

<1 year

1–2 years

3–5 years

>5 years

Never

5

Related fleet issues

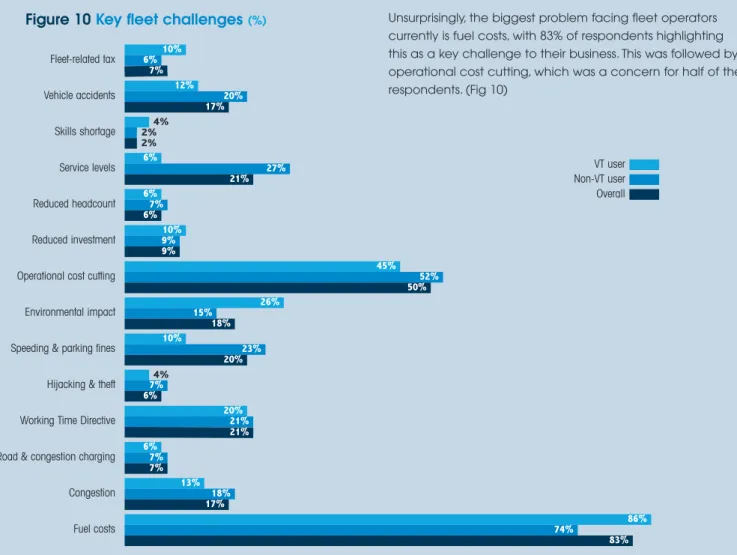

Unsurprisingly, the biggest problem facing fleet operators currently is fuel costs, with 83% of respondents highlighting this as a key challenge to their business. This was followed by operational cost cutting, which was a concern for half of the respondents. (Fig 10)

The difficult economic climate has had a mixed impact on fleet operations with more than half believing it has had a negative impact. In particular, only 15% had seen their fleet budget increase during 2011, with the remainder

experiencing a reduction or staying the same. However, 46%

of respondents overall thought telematics could help them overcome the challenges caused by the downturn, although this percentage dropped dramatically amongst those not currently using vehicle tracking to just 26%. (Fig 11)

Figure 10

Key fleet challenges

(%)10% 6% 7% Fleet-related tax 12% 20% 17% Vehicle accidents 4% 2% 2% Skills shortage 6% 27% 21% Service levels 6% 7% 6% Reduced headcount 10% 9% 9% Reduced investment 45% 52% 50%

Operational cost cutting

26% 15% 18% Environmental impact 10% 23% 20%

Speeding & parking fines

4% 7% 6%

Hijacking & theft

20% 21% 21%

Working Time Directive

6% 7% 7%

Road & congestion charging

Non-VT user Overall VT user 13% 18% 17% Congestion 86% 74% 83% Fuel costs Yes No Increased Decreased Stayed the same

Do you think your telematics systems could help you to overcome the fleet challenges created by the financial crisis and economic downturn?

50% 50% 28% 72% 46% 54% VT user Non-VT user Overall

What has happened to your fleet budget in 2011?

25% 23% 52%

26% 29% 45%

25% 25% 50%

VT user

Non-VT user

Overall

Has the financial crisis and economic downturn had a negative impact on your fleet operation?

53% 47% 54% 46% 53% 47% VT user Non-VT user Overall

Figure 11

6

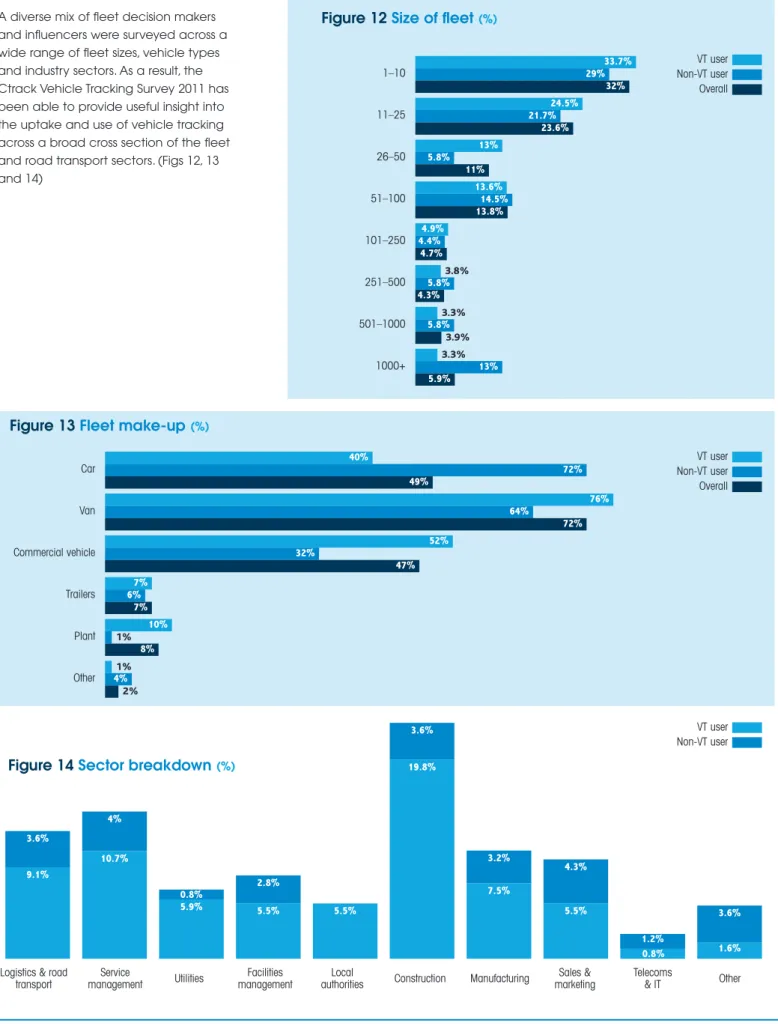

Breakdown of respondents

Logistics & road transport Service management Utilities Facilities management Local

authorities Construction Manufacturing

Figure 12

Size of fleet

(%)33.7% 29% 32% 1–10 24.5% 21.7% 23.6% 11–25 13% 5.8% 11% 26–50 13.6% 14.5% 13.8% 51–100 4.9% 4.4% 4.7% 101–250 3.8% 5.8% 4.3% 251–500 3.3% 5.8% 3.9% 501–1000 3.3% 13% 5.9% 1000+ 40% 72% 49% Car 76% 64% 72% Van 52% 32% 47% Commercial vehicle 7% 6% 7% Trailers 10% 1% 8% Plant 1% 4% 2% Other

Figure 13

Fleet make-up

(%)Figure 14

Sector breakdown

(%)Non-VT user Overall VT user Non-VT user Overall VT user Non-VT user VT user 9.1% 3.6% 10.7% 4% 5.9% 5.5% 2.8% 5.5% 19.8% 3.6% 7.5% 3.2% 5.5% 4.3% 1.2% 1.6% 3.6% Sales & marketing Telecoms

& IT Other

A diverse mix of fleet decision makers and influencers were surveyed across a wide range of fleet sizes, vehicle types and industry sectors. As a result, the Ctrack Vehicle Tracking Survey 2011 has been able to provide useful insight into the uptake and use of vehicle tracking across a broad cross section of the fleet and road transport sectors. (Figs 12, 13 and 14)

0.8% 0.8%