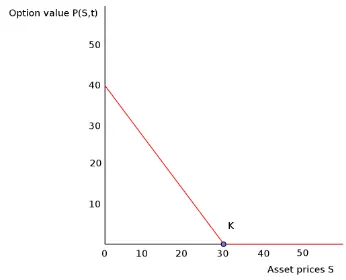

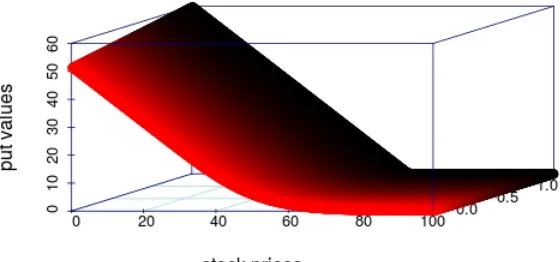

Pricing a European Put Option by Numerical Methods

Full text

Figure

Related documents

(15) Park means to stop, or to cause to permit, or to remain stopped, any vehicle or combination of vehicles, or any portion thereof, on any street, off-street parking facility, or

In concurrent work (Streeter & McMahan, 2010), we showed that for some problem families, a per-coordinate learning rate for online gradient descent provides asymptotically

OSG needs to be able to support "higher-level services" that require network metrics to make decisions regarding data transfers and higher-level workflow optimizations

ALPA CIRP recommends a critical incident stress debriefing with an ALPA-‐‑approved mental health professional after an incident or accident resulting

Information technology centre” basic need, types and operations of the centre; I.T policy/guidelines: legal perspective; Different approaches to office procedure

Second, we use this symmetric form to find natural analogues of the Okamoto equation (1.11) for 2 × 2 Schlesinger systems with an arbitrary number of simple poles.. Our approach

On each trial, the stimuli (S1, S2, O) were presented simultaneously in a horizontal sequence on the screen. Each stimulus was followed by a question mark and the presence or

The supplementary terms and conditions based on which this contract is concluded are contained in the general terms and conditions of sale Sande Varieties and apply to the