Services in Regioanl Trade Agreements: Implications for India

Full text

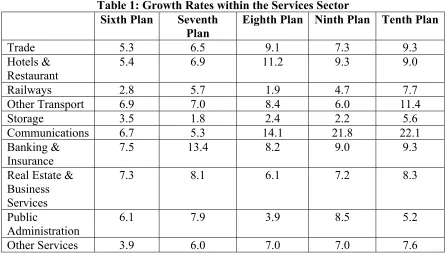

Figure

Related documents

The experimental treatments consisted of three levels of drought stress [severe drought stress (S2), moderate drought stress (S1) and no drought stress (S0)] in the

GEMSTONES Facetted Ruby Rhodolite Garnet Pink Sapphire Pink Tourmaline Citrine Peridot Tsavourite Garnet Emerald Aquamarine Irradiated Blue Topaz Sapphire Iolite Amethyst Cabochon

XRCC3 have been ablated in mice [ 29 – 32 ]. In each case, ablation of RAD51 paralogs results in embryonic lethality or early neonatal death, precluding any detailed phenotypic

Based on the database literature search, 18 studies were identified that assessed online gaming addiction by means of using adapted diagnostic criteria for pathological gambling

More specifically, we predict relatively more threat (and less challenge) when responding to negative differentiation than to positive differentiation or “random” rejection

InterMedia Financial Inclusion Insights Program - Kenya Report www.finclusion.org 28 With respect to bill payments,, only 1 percent of active mobile money account

a 15-week randomized controlled trial of the alpha-1 adrenoreceptor antagonist prazosin for combat trauma nightmares, sleep quality, global function, and overall symptoms

Dengan demikian dilihat dari hasil dan dibandingkan dengan penelitian yang pernah ada penelitian ini sesuai dengan teori yang ada dan sejalan dengan penelitian yang pernah