Nominal Income and Inflation Targeting

27

0

0

Full text

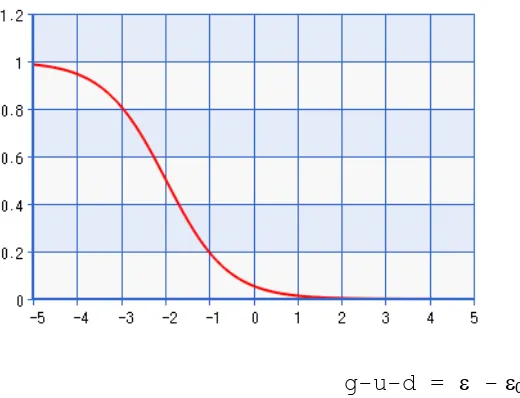

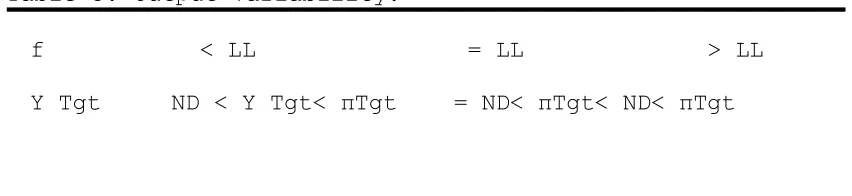

Figure

Related documents