Prepared For:

Market Regulation Services Inc.

145 King St. W. Suite 900 Toronto, ON

Regulating Trade-throughs in

Canada: How Can Regulators

Choose the Best Course?

Prepared By: Mark Neumann CRA International

80 Bloor Street West, Suite 1501 Toronto, Ontario M5S 2V1 Date: October 13, 2005

TABLE OF CONTENTS

1. INTRODUCTION... 1

2. INNOVATION AND COMPETITION ... 4

2.1. KEY ECONOMIC CONCEPTS... 4

2.1.1. Liquidity Externalities and Adverse Selection ...4

2.1.2. Fragmentation and Market Power ...5

2.1.3. Principal-Agent Problems ...7

2.1.4. Static and Dynamic Efficiency ...7

2.2. AN OVERVIEW OF USSTUDIES OF CAPITAL MARKET COMPETITION... 8

2.3. STRUCTURING THE TRADE-THROUGH RULE... 12

2.3.1. Innovative Products and the Trade-through Rule ...13

2.3.2. Marketplace Linkages and the Trade-through Rule...16

2.4. THE EFFECT OF A TRADE-THROUGH RULE ON COMPETITION IN CANADA... 19

3. MEASURING THE INCIDENCE AND COST OF TRADE-THROUGHS... 22

3.1. INCIDENCE OF TRADE-THROUGHS... 23

3.1.1. Interpretation ...27

3.2. MEASURING THE DOLLAR COSTS OF TRADE-THROUGHS... 29

3.3. MEASURING THE BENEFITS OF A TRADE-THROUGH RULE... 30

3.4. OTHER EMPIRICAL ANALYSIS CONDUCTED BY THE OEA... 31

4. APPLYING COST-BENEFIT ANALYSIS TO TRADE-THROUGH REGULATIONS ... 32

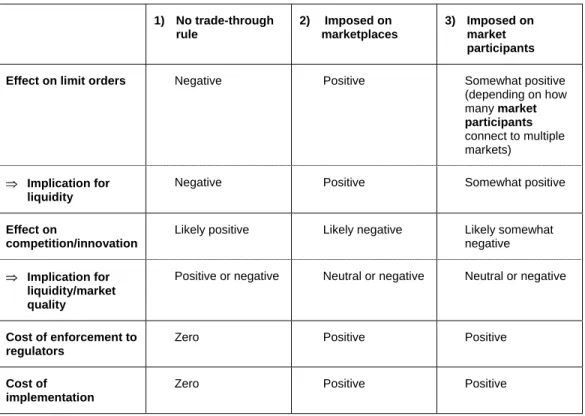

4.1. POSSIBLE TRADE-THROUGH DESIGN... 32

4.2. ESTIMATING BENEFITS... 34

1. INTRODUCTION

The Canadian Securities Administrators (“CSA”) are in the midst of determining what regulatory response, if any, to take in respect of trade-through activity on competing Canadian equity trading marketplaces.1 The current debate, as framed in the CSA

Discussion Paper, relates to whether the trade-through rule, if adopted, is best imposed on market participants (“participant-level” obligations on dealers and subscribers to alternative trading systems (“ATSs”)) or marketplaces (“marketplace-level” obligations on exchanges, QTRSs and ATSs).

With the entry of BlockBook, the issue of how to regulate inter-market trade-throughs has become a more pressing issue for regulators. Prior to the entry of BlockBook, the

opportunities for inter-market trade-throughs were limited to two securities trading on both the TSXV and CNQ. Trade-throughs are also possible for interlisted stocks on foreign and Canadian exchanges, which while technically a “trade-through” is not treated as such by regulators in Canada.2 Critics of the prohibition of trade-throughs embodied in the “trade-through rule” have cited concern that the rule impedes competition between marketplaces and reduces the extent to which ATSs are able to distinguish themselves from traditional exchanges thereby reducing innovation. In order to examine the merits of these arguments it is important to consider any potential offsetting economic benefits from the trade-through obligation, notably its role in ensuring that sub-optimal fragmentation is avoided. In addition, distribution issues need to be considered since the benefits and costs of a trade-through rule (or the lack of one) are not shared equally.

The merits of restricting trade-through activity have been hotly contested in the United States, where competing marketplaces have been operating for years. As part of the debate

surrounding Regulation NMS, a large number of empirical studies of the impact of trade-through rules on US markets were undertaken as well as studies of the anticipated costs and benefits of alternative forms of the proposed order protection rule. A number of these studies – particularly those performed by the Securities Exchange Commission (SEC) – were

criticized on methodological grounds in public comments. This US data, the conclusions of the empirical studies, and the critiques of those studies, are all relevant to the Canadian debate. At the same time, there are important differences between the US and Canadian markets that must be taken into account when considering the findings and criticisms in respect of the US reports.

In this report, we explore how the trade-through rule may affect competition and innovation

1 CSA Discussion Paper 23-403, Market Structure Developments and Trade-Through Obligations.

2 Intra-market trade-throughs have been permitted on the Montreal Exchange, though these trade-throughs occur for derivatives and not equities.

bearing in mind the importance of liquidity externalities, adverse selection and principal-agent problems that plague capital markets and the trade-offs inherent between static and dynamic economic efficiency that a trade-through rule might change. We review some of the

extensive empirical finance and economics literature on this well-researched topic. Having set out the competing influences that affect the potential impacts the trade-through rule may have on market fragmentation and innovation, we turn to an assessment of the SEC studies. Like many critics of this work, we find the SEC’s measurement of trade-through incidence to be fundamentally flawed. In addition to assessing the critical commentary that this study elicited, we also provide examples of how the SEC estimates are flawed by reference to simulations that we conducted.

Notwithstanding the flaws in the SEC study, given the complicating and opposing influences that a trade-through rule may have on overall market efficiency, the net benefits from the rule are ultimately an empirical question. We do not attempt to measure the potential costs and benefits from the trade-through rule in Canada, but instead provide the framework for such analysis.

Where there are found to be net benefits from the trade-through rule, the final issue to be addressed is the optimal form for trade-through regulations – as the CSA Discussion Paper notes, to whom should they apply and to what extent? For example, if the motivation is strictly one of upholding a dealer’s fiduciary duty to its client then there is no need to impose a through rule on investors who are trading on their own behalf. Alternatively if the trade-through rule is to be imposed universally on all market participants as a duty to the market in general, the question arises as to whether it is more efficient to apply the rule to marketplaces or market participants. Cost-benefit analysis can seek to directly measure the differential costs of implementation and the expected benefits under each approach.

As discussed herein, regulators need to be concerned about both the positive and negative effects of enhanced competition/fragmentation. Only focusing on the impact of a trade-through rule on the incentive to supply limit orders is likely to be short-sighted since it ignores the fact that while a trade-through rule may increase competition among orders it may also reduce competition between marketplaces. In this vein, the trade-through rule may result in lost benefits to those investors, typically institutions, who make use of trade-throughs when considerations other than the price of individual transactions (such as speed or certainty) are important. In respect of competition, it is important to take the existing levels of international competition into account, especially for the largest securities issuers. Further entry by ATSs in Canada is incremental to this. While greater levels of competition are not always

beneficial, generally the evidence suggests that increased competition improves market quality. A trade-through rule could hinder entry and innovation by limiting the ability of entrants to appeal to a diverse set of customers with different needs. Establishing this conclusively, however, is difficult. Once again, it is important to determine the incremental impact the trade-through rule would have on the entrant’s profitability.

If Canada were to have comparable trade-through rates as those in the United States, these are likely to be small overall, though large enough that they cannot be ignored. To

understand the reasons behind trade-throughs, it would be useful to have greater analysis done. Overall, the US experience is such that it is unclear whether Regulation NMS will have a net positive impact.

Given the various influences that the trade-through rule may have on competition,

fragmentation and innovation, a cost-benefit analysis is likely the only means by which the merits of the rule may be properly assessed. To this end, greater rigor should be brought to the cost-benefit analysis than was taken by the SEC. Of course, this makes the analysis more involved and if it is not executed well, it may attract criticism. While challenging, a cost-benefit analysis is nonetheless needed if effective policies in respect of trade-throughs are to be developed in Canada. We outline how this work might be done in the final section of the report.

2. INNOVATION

AND

COMPETITION

In this section we investigate how a trade-through rule might affect innovation and competition among financial marketplaces in Canada. Many US commentators critical of Regulation NMS argued the trade-through rule would hinder innovation, thereby reducing the benefits to be had from dynamic competition. The potential losses from less competitive and innovative marketplaces were viewed as sufficiently large to more than offset any potential gains that the trade-through rule might bring in the form of greater limit orders. Those commentators in favour of the trade-through rule believed it would enhance competition among orders and reduce the deleterious effect of market fragmentation.

There are two lines of arguments on how a trade-through rule affects competition and innovation. The first argument focuses on the interconnections that a trade-through rule could force on market participants, which leads to interdependence on a given technology that may limit the ability of a marketplace to adopt a better technology that is incompatible with the technology that supports the interconnection. The interconnectedness also leads to a related problem of the lowest common denominator where, for example, the speed of a transaction is limited to the slowest link in the network so that there is no incentive for any but the slowest marketplace to invest in faster information technology systems. The second line of argument stresses that the trade-through rule limits the set of business models available and this could foreclose a profitable business strategy for a new entrant.

2.1. K

EYE

CONOMICC

ONCEPTSIn considering this debate, it is useful to bear in mind several fundamental economic principles, which we discuss below. As the discussion of the economic issues indicates, understanding the impact of a trade-through rule on competition and innovation is

complicated. There are a variety of conflicting influences at play, which makes it very difficult to specify a conceptual framework or a mathematical model for empirical testing.

The first economic concept relates to market failure, which refers to distortions that exist within a market such that markets free of all regulation would not lead to efficient outcomes. In such circumstances regulation is imposed to move the market closer to an efficient outcome. In the securities industry there are several market failures at play. These include network effects or liquidity externalities, adverse selection and principal-agent problems. The second economic concept relates to static versus dynamic efficiency.

2.1.1. Liquidity Externalities and Adverse Selection

Capital markets are influenced strongly by liquidity externalities. At its simplest, a liquidity externality arises because as one trader comes to a market he increases the chance of profitable trade for all other traders. This tends to bring traders together in one place and at one time. The liquidity externality can also be described as a positive network effect where the value of the system to any individual increases with the number of individuals using it.

This type of liquidity externality just as much characterizes a farmers’ market as it does a capital market.

Unlike a farmers’ market, however, asymmetric information is an important feature of capital markets and a significant component of the liquidity externality. Asymmetric information then leads to adverse selection problems. As a result, if there are multiple markets rational informed traders will split up their trades across these markets in order to maximize the information rent they can extract. Uninformed liquidity traders have an incentive to pool together to increase their chance of trading with each other and reduce their chance of trading with an informed trader. This reduces the cost of adverse selection. The difficulty in trying to measure the relationship between adverse selection costs and pooling liquidity is that in equilibrium we would generally not expect to observe much variation across marketplaces in the adverse selection cost. If there were large differences, then the marketplace with the high adverse selection costs would be forced out or at least forced to change to bring adverse selection costs in line with other marketplaces. We discuss an empirical study of this issue below when examining the US market.

2.1.2. Fragmentation and Market Power

The benefits of pooling trading activity together can be undone by fragmentation. Given the strong measured benefits of pooling there is good reason for regulators to be nervous about too much fragmentation. A more fragmented market results in fewer opportunities for mutually beneficial trades and increases the adverse selection costs. Fragmentation is associated with reduced liquidity, higher overall trading costs, weaker price discovery and the incentive to provide private information (Cohen, Maier, Schwartz and Whitcomb (1982), Cohen, Conroy and Maier (1985), Mendelson (1987), Amihud, Lauterbach and Mendelson (2003)).

But if the liquidity externality were the only economic characteristic of capital markets then there would never be fragmentation, and in this case regulators would not have to intervene because markets would take care of themselves. However, competitive forces are also at play and they tend to fragment markets. As Blume (2002) points out “A national market system abhors fragmentation…Yet, fragmentation is at the heart of competition.” If there is only one marketplace then it is a monopoly and like any unregulated monopoly it will earn economic rents by limiting the supply of its services, except in the rare case where demand is perfectly elastic. For example, a monopoly market may reduce the number of liquidity suppliers that can use the exchange in order to drive up prices (see Pirrong (2001)). If there is free entry then other marketplaces can develop to compete for those rents. The profitability of entry, and thus the amount of entry, depends on how intense competition is and the magnitude of the fixed costs associated with entry. The intensity of competition depends on the heterogeneity in traders and on regulations. The more variation there is in trader preferences the greater the opportunity for profitable entry. Incumbents have an incentive to “plug up” niches where profitable entry could occur, especially if the ensuing competition

would be strong. However, an incumbent may be reluctant to fragment its own marketplace since reducing the benefit of the liquidity externality reduces the value of its services, which in turn reduces the rents it can extract. As well, the decrease in the value of the incumbent marketplace’s services could leave it more vulnerable to entry in other niches.

Rational investors who switch to a new entrant’s system act in their own self-interest. Thus at the time of making the switch they consider themselves better off. Yet to understand the full impact of entry we need to compare the economic efficiency of the new equilibrium with the old equilibrium. By reducing the liquidity externalities, the increased fragmentation from entry reduces the benefits of trading on the incumbent marketplace for both informed and liquidity traders. As a result, there can be feedback effects where the increase in adverse selection costs reduces the amount of information gathered, which in turn increases the volatility of stocks, which in turn causes the most risk adverse investors to substitute to other investment vehicles, which further reduces liquidity. Operating in the opposite direction is competition that reduces rents arising from market power, and in turn acts to increase liquidity as more trading occurs. It is unclear which effect will dominate.

These conflicting influences are ultimately at the heart of the debate over the trade-through rule. To some commentators, the trade-through rule acts to reduce the extent of

fragmentation by forcing greater interaction between orders of different marketplaces. To other commentators, the rule acts to inhibit the ability of marketplaces to optimally

differentiate their service from incumbent exchanges, which reduces the profitability of entry and innovation. With less competition and less threat of future competition the incentives to innovate are less for the incumbent marketplace and the inefficiencies arising from the exercise of market power by the incumbent marketplace increase.

Using a theoretical model Pirrong (2001) shows that the benefits of enhanced competition outweigh the costs of increased fragmentation.3 In his model, entry is driven by a

marketplace that skims of some of the uninformed traders. Uninformed traders are profitable because they do not pose an adverse selection risk. Skimming off these traders increases the costs of trading on the incumbent exchange because adverse selection costs go up on the incumbent exchange. However, in Pirrong’s model the benefits of additional liquidity from competition outweigh the costs of this fragmentation. The model is useful for identifying the various trade-offs; however, it has the usual disadvantage associated with theoretical modeling of representing a significant simplification of reality and as a result the generality of its conclusions are unknown in a more complex (i.e., real) environment.

3 The fact that making one market failure worse—market fragmentation—can be welfare improving when there are other market failures—imperfect competition—is an example of the theory of the second best.

2.1.3. Principal-Agent Problems

Trading securities often requires brokers to work on behalf of clients. Brokers are agents of investors and, thus, the principal-agent problem arises. Investors cannot costlessly monitor the actions of brokers and since brokers’ interests are only imperfectly aligned with clients brokers may not always operate in the interest of their clients. While imposing a legal obligation of fiduciary duty helps reduce the problem, because enforcement is costly and imperfect itself the principal-agent problem persists. The broker-client relationship is not the only one where principal-agent problems arise. Institutional investors are also agents of their clients and the actions of institutional investors are only imperfectly monitored. These

principal-agent problems can create incentives for marketplace entry as a means of exploiting the information disadvantage of investors.

If the incentive to enter acts to dissipate monopoly rents, this generally has a beneficial effect on overall market efficiency; however, as Macey and O’Hara (1999) note fragmentation can occur because of free-riding on information generated in the primary market or to take advantage of principal-agent problems, and thus subverts the duty of best execution. In such circumstances, fragmentation offers no benefits.

2.1.4. Static and Dynamic Efficiency

Standard economic models of competition assume that large numbers of firms and no barriers to entry are required to provide efficient outcomes. Static economic efficiency is obtained when firms price at (or near) the marginal cost of producing the product or service with a sufficient margin above marginal cost to recover the costs of any sunk fixed cost of initial investment. If this is not the case, market power exists. A firm that has some market power can use pricing in different ways to generate as much profits as possible. The simplest case is simply to raise prices until the point where the revenue loss from selling to fewer customers net of the additional revenue from selling at a higher price to existing customers is equal to marginal cost. A more sophisticated strategy is to price discriminate among

consumers by charging the less price sensitive group of consumers a higher price than more price sensitive customers.

Dynamic efficiency is concerned with innovation that takes place over time. Innovation leads to the adoption of new goods and services that can provide substantial benefits to

consumers. Typically, in order to obtain dynamic efficiency there must be some departure from static efficiency. In essence, firms need to earn sufficient profits (and hence price far enough above short-run marginal cost) to justify the investments required to innovate. The consumer benefits obtained from access to new products and services arising from

innovation justify the short-term static inefficiency losses from pricing above short-run marginal cost.

As the above discussion should clearly indicate, there are numerous influences at work, often with opposite effects. Theoretically, there is no clear answer in terms of whether the potential influences in one direction from a trade-through rule will dominate influences in the other direction. The issue can only be resolved by empirical testing. To this end, much empirical research has been undertaken in the United States to better understand the importance of these economic influences on market microstructure and the interaction of marketplaces. This research provides important insights on how trade-through rules impact on innovation and competition, notwithstanding differences in market structure and regulatory regimes between Canada and the United States. In the next section, we discuss the relevant empirical US studies.

2.2. A

NO

VERVIEW OFUS

S

TUDIES OFC

APITALM

ARKETC

OMPETITIONUS capital markets are arguably the most competitive in the world. Roughly speaking the US market for equity exchange services is composed of the New York Stock Exchange (NYSE) (which now uses a hybrid model of a traditional manual-based floor system and a modern electronic auction), regional floor based exchanges, the Nasdaq market makers (a dealer market), Electronic Communication Networks (ECNs) and Crossing Systems. The NYSE, Nasdaq and the regional exchanges are traditional marketplaces while the ECNs and Crossing Systems are Alternative Trading Systems (ATSs). ATSs – and ECNs in particular – gained substantial market share starting in the 1990s mostly at the expense of Nasdaq dealers. ATSs have captured about 10% of the volume of equity trading on the NYSE and 30% of Nasdaq volumes.4 This has prompted both short- and long-term competitive

responses by Nasdaq (e.g. better quotes, SuperMontage). In contrast, the NYSE has held is dominant position, retaining over 80% share in trading of its listed stocks, and, according to some, has been slower to innovate.5

The US marketplaces do not operate as silos. Linkages exist among them that allow orders to be routed between marketplaces, which are also linked by information. For example, the Best Bid and Offer is published continuously by markets and collectively forms the National Best Bid and Offer (NBBO). The combination of links between markets and the NBBO facilitates competition for orders between existing marketplaces. Both self-interest and regulatory structure (i.e. the National Market System) have been responsible for creating these linkages.

4 Deutsche Bank Research, “Economics: Digital Economy and Structural Change”, January 2005.

5 Some commentators equate the NYSE’s slow move to electronic trading as evidence of a lack of incentive to innovate. Lucas et al (2002) note that NYSE’s share of market value of NYSE, Nasdaq and Amex listed companies was 82.3% in January 1998 and 83.0% in July 2002. However, they argue that the NYSE’s dominant position has not created a disincentive to innovate and that in fact the evidence indicates that the NYSE has in the past been able to use IT investments to reinforce its competitive advantage.

To appreciate the details of competition in the United States, it is important to understand the prominent role of information in capital markets generally, and how information flows affect market structure. Taking the economic issue of liquidity externalities as a starting point, Barclay and Hendershott (2004) find extremely large benefits from pooling, as do various other studies noted above. Barclay and Hendershott also obtain interesting results in respect of the relationship between adverse selection and liquidity externalities. As noted in the economic discussion above, if adverse selection costs were very large we expect few (or one) marketplaces to dominate given the existence of liquidity externalities. This may explain why the NYSE remains the dominant exchange notwithstanding increased competition from other marketplaces.

Barclay and Hendershott noticed that this need not be the case, however, as demonstrated by the after-hours market where trading occurs on ECNs. ECNs electronically match traders with each other rather than rely on a dealer to intermediate trades. As a result, an ECN can continue to match trades after other markets close as long as the ECN systems are kept running. Barclay and Hendershott found that volumes drop substantially in the after hours market with only 1/20 as many trades. Thus the liquidity externality is substantially reduced. They then measured the cost of adverse selection. They found the adverse selection costs were 15 times larger (in dollar terms) in the pretrade period and seven times larger in the postclose than during the trading day. Given this, why would any investor want to trade after hours? If a trader has valuable information that he does not expect to last into the trading day then he would rather trade now than later even if the bid-ask spread is large. The supplier of liquidity will still be willing to trade against the informed trader if the supplier’s bid-ask spread is wide enough. In other words, liquidity demanders are willing to pay a large price to be able to benefit from the value of their information and liquidity suppliers still break even. As a result, trading occurs.

As discussed earlier the liquidity externality while important is not the only factor at play in capital market structure. When pooling benefits lead to a single marketplace, monopoly profits are earned which encourages entry of new marketplaces. Entry has been made all the more attractive with dramatically declining costs of computer and communications technology which has greatly reduced execution costs and the fixed costs associated with entry. This is amply demonstrated by US experience. For example, the crossing system POSIT grew at an annual rate of 45% between 1988 and 1999 and ECNs now account for 40% of the dollar volume of trading of Nasdaq securities (Conrad, Johnson and Wahal (2003)). Weston (2002) documents the dramatic increase in ECN market share in the late 1990s and finds that ECNs have resulted in lower spreads, greater depth and improved overall liquidity on Nasdaq. At the same time, Schwartz and Steil (2002) suggest that principal-agent problems have prevented more institutional trading from shifting to ECNs from Nasdaq dealers. The argument is that a fund manager would prefer to offload services such as research and computer systems that support the sell-side to the intermediaries and pay for these through higher bid-ask spreads (“soft dollar commissions”) than pay for them directly with client assets where such costs would show up as explicit expenses in management fees. As a

result, the fund manager relies more on broker-dealers than on ECNs, which, since the Nasdaq broker-dealer system is not anonymous, increases the potential for information leakage and thus increases the need for immediacy to reduce the cost of such leakages. All this is added expense and affects market structure.

Turning back to the NYSE, the US experience indicates that competition between the NYSE and the regional exchanges is typically of the cream skimming variety where a regional exchange attempts to select for less informed traders. Competition with the NYSE is also seen as a search for profitable niches. Lipson (2004) examines competition among six market centers for NYSE listed stock. Market centers differentiate themselves by specializing based on the stock, the order type or order size. Lipson finds that order flow routed to the NYSE is substantially more informed than orders routed to other marketplaces (other than ECNs). Order difficulty and order timing are found to be important components of

competition. Lipson’s results highlight the fact marketplaces will seek to differentiate themselves in order to reduce competitive pressures as much as possible. His results also indicate that it is difficult to be competitive against the NYSE’s large liquidity advantage, which limits the extent to which other marketplaces can supplant it as the dominant marketplace. As already noted, the NYSE has maintained over an 80% share of trading notwithstanding the rapid decline in entry costs.

Conrad, Johnson and Wahal (2003) find that most ATS competition with the NYSE comes from crossing systems. A crossing system (e.g. POSIT) crosses orders several times a day (at given times plus a random component) using the price in the primary market. The liquidity available to the crossing system is confined to its members. There is no price discovery. Thus a crossing system appeals to investors with low immediacy requirements. For a crossing system to work well there needs to be considerable liquidity in the stocks traded and price discovery in the primary market needs to be strong. Conrad et al. argue that this is precisely what the NYSE offers as a primary market. The crossing networks design of low immediacy attracts uninformed traders – informed traders usually have high immediacy requirements since they are concerned with information leakages. Thus like Lipson’s

findings, competition for NYSE listed stocks take the form of cream skimming. The execution costs are much lower (13 cents a share or 30 basis points) on the crossing network, though this does not account for the opportunity cost of unfilled orders. Easley, Kiefer and O’Hara (1996) similarly find that orders sent to the Cincinnati Stock Exchange are mostly uninformed. The fact that crossing networks do not contribute to price discovery is not much of a cost since more of the trading is not informed. The bigger potential cost is that skimming off uninformed trading may increase adverse selection costs on the NYSE. Whether this is the case or not is unclear as it is very difficult to determine the volumes that would have been traded absent the crossing networks. Moreover, crossing networks, like other ATSs, put pressure on the NYSE to innovate, at least over the longer term.

The Nasdaq market provides an interesting contrast where the welfare effects of competition from ATSs appear to be less ambiguous. Conrad et al. show that unlike the NYSE most competition with Nasdaq comes from ECNs. Huang (2002) shows that ECN quotes are

typically informative, are posted faster, are more often at the inside, and the spreads are often smaller. Huang suggests that ECNs may do more to promote quote quality than to fragment markets. Similarly, Barclay, Hendershott and McCormick (2003) find that ECNs attract informed investors and contribute more to price discovery and Conrad, Johnson and Wahal (2003) find execution costs are generally much lower on ECNs.

The success of ATSs is not entirely attributable to technological innovation in communication technology that has facilitated their entry. ATSs also provide a bundle of services distinct from exchanges. As Macey and O’Hara (1999) state, “In a nutshell, by acting exclusively as agent for their customers, ATSs solve the conflict-of-interest problem that exists between customer and broker-dealer firms.” ATSs provide anonymity to their customers (and thus protection of customers’ property rights) by giving up the liquidity services that exchanges provide.

It is useful to understand why the nature of competition is different for Nasdaq compared with that impacting on the NYSE.6 Unlike the monopoly of the specialist on the NYSE floor,

Nasdaq dealers compete with each other for order flow by posting quotes. They employ order preferencing arrangements. For example, as described in Huang, orders sent to Nasdaq may be preferenced to a specific dealer who provides payment in cash or service to the broker or they may be preferenced via internalization where orders are sent to captive market makers. Market makers contract with brokers to attract more profitable orders (see, for example, Barclay, Hendershott, and McCormick (2003), Smith, Selway, and McCormick (1998)). To some extent market makers are able to price discriminate based on whether the order is likely uninformed or not. Price discrimination on large trades is made possible through repeated relationships with institutional traders, which allows market makers to use the threat of future retaliation to keep traders honest about the information in the trade. Those traders that cannot identify themselves as uninformed are offered worse prices. This creates an entry opportunity for ECNs.

Trading on ECNs is typically anonymous and, as mentioned above, does not require a market marker since trades are matched directly. The order book is also typically available, which allows subscribers to see the full depth of trading interest. ECNs are also typically fast, offering immediate execution, whereas traditional orders must be first sent to a broker who then determines the market where to send the order for execution. As Barclay et al. (2003) note “immediate execution and anonymity are closely related and both appeal to those investors who may have short-lived information about future price changes.” Of course, since an ECN attracts more informed trades the ex ante price must be higher to offset the

contraparty for higher adverse selection costs. However, just as some traders with

6 Competition of course also occurs between Nasdaq and the NYSE. Khullar (2004) notes that since Nasdaq’s introduction in 1971 it has been gaining market share at the expense of the NYSE. In 1970 69% of trades were executed on the NYSE while by 2002 NYSE’s share has dropped to 37%. Despite this long-term trend, Khullar finds lower daily volatility and firm ownership rates are lower on the NYSE and this enables the NYSE to differentiate itself from Nasdaq in attracting listings from larger companies.

lived information are willing to accept large spreads in the preopen and postclose markets some traders will also be willing to accept higher adverse selection costs during the trade day.

Changes in the US regulations provide an opportunity to empirically test the regulation’s effect on competition. In particular, the SEC implemented Order Handling Rules (OHR) in 1997 to enhance the level of competition. The Limit Order Display Rule and the ECN Rule make it possible for customers and ECNs to compete directly with dealers’ quotes. The Limit Order Display Rule requires that a customer’s limit order quotes replace the dealer’s quotes if they are at or better than the dealer’s quote and the ECN Rule requires that quotes offered by ECNs to dealers be included in the Nasdaq NBBO montage. Conrad, Johnson and Wahal (2003) document how changes in these regulations have affected competition. They find that the OHRs, which reduced fragmentation between ECNs and Nasdaq, as well as the reduction in tick sizes on Nasdaq, which reduced the ECNs quote size advantage, resulted in a decline in institutions’ relative use of ECNs and reduced the cost advantage of using an ECN. In this case, an argument could be made that ECNs were helping to offset the undesirable effects of fragmentation on Nasdaq and the lack of transparency but when regulations directly

addressed the issue the competitive need for the ECNs was reduced. While this might be interpreted as better regulation reduces the need for competition, this is not necessarily so. For instance, these regulatory changes might not have been made had ECNs never been in the market. Without the regulatory changes and without ECNs the market would not be as efficient as it is with these events.

In summary, the US empirical studies are useful in gaining a better understanding of the trade-off between competition and fragmentation. They also identify the complexities involved in such analysis. At the moment, there are no clear answers as to whether the extent of competition in the United States is close to optimal levels. Instead, we know it is possible for unregulated marketplaces to have either too much or too little entry relative to an efficient outcome. While this suggests some need for regulatory intervention, it is unclear how much regulation is required. In particular, it is unclear whether the trade-through rule is the best regulatory response given other regulatory instruments that may be available or in place to achieve other policy objectives.

2.3. S

TRUCTURING THET

RADE-

THROUGHR

ULEThere are two important dimensions along which a trade-through rule could vary. One is whether the rule applies to the top of the book or the depth of the book. The second is whether it is observed by exchanges or by market participants (and in that case it would apply to only the marketplaces to which the market participant is connected). For those who believe that the benefits of encouraging limit orders through enhanced liquidity – the anti-fragmentation proponents – a depth-of-book alternative and enforcement between markets to maximize interaction of orders is preferred. For those commentators who are more

A trade-through rule that is enforced at the market participant level could have quite different effects on competition and innovation. As discussed below, given the costs of making connections, fewer traders would interact with each other since not all market participants will connect directly to all marketplaces. The market participant ignores the positive liquidity externality and therefore underinvests in making connections to multiple marketplaces. Thus fragmentation increases if trade-through is enforced at the market participant level compared to marketplace implementation. On the other hand, the disincentive that a trade-through rule creates to increase speed and reliability is reduced since a market participant that becomes dissatisfied with the performance of one marketplace can cancel its subscription and exempt itself from its trade-through obligation.

We elaborate on these issues below.

2.3.1. Innovative Products and the Trade-through Rule

A trade-through rule might hamper the development of innovations, especially those that appeal to institutional investors. For example, a trade-through rule would reduce the incentive for an institution to develop algorithms (and for an ATS to develop an interface to support the institutions efforts) to find and execute a block order to maximize the total value of the order. The trade-through rule, at least to some extent, forces the algorithm on the

institution. Of course, if trading through is considered socially harmful then the innovation is not desirable from a social welfare perspective.

A depth-of-book rule where all limit orders are protected from trade-through (regardless of where the market order originated) and time priority is respected is tantamount to a central limit order book (CLOB) and thus turns order execution into a commodity. This would be the most restrictive version of a trade-through rule. It reduces incentives to develop innovations to enhance order execution quality (such as greater execution speed) or to offer new differentiated service for institutional clients. If one marketplace finds a way to attract more liquidity, much of this liquidity could be captured by other marketplaces. On the other hand, a CLOB maximizes order interaction and thus generates the benefits associated with reduced fragmentation.

Removing time priority, a depth-of-book rule is no longer equivalent to a CLOB and is thus less restrictive. However, it still reduces the ability for marketplaces to attract order flow with some feature other than just price and this could make entry less profitable. Under a price-priority trade-through rule, for an innovative marketplace to retain the order flow its innovation attracts it must match better bids and offers of other marketplaces, which reduces the

profitability of the innovation. The trade-through rule may enhance short-run competition, but if entry reduces the return to innovation or limits entry then long-run competition and

innovation could suffer. However, the effect on entrants of such a trade-through rule need not be negative. For instance, if a trade-through rule is implemented at the marketplace level, it forces connections to be made between marketplaces and this could give an entrant access

to market orders that it would not otherwise have been able to access.7 If the entrant is

more efficient and can attract aggressively priced limit orders then it has a greater chance of stealing market share from the incumbent. However, if the entrant’s strategy is to compete by offering a differentiated service the trade-through rule could undermine the entrant’s ability to differentiate its execution services and make it difficult for it to compete against an incumbent with a huge liquidity advantage.8

If the trade-through rule only protects the top of the book then there is greater flexibility in the strategy used for executing a large block order since once the top of the book is cleared, the trader is free to route remaining volume according to his preferences. This gives an entrant marketplace more opportunity to attract orders by offering other features, such as speed or greater certainty of execution. Of course, the amount of order interaction is reduced relative to a depth-of-book implementation.

When considering the extent to which the trade-through rule may affect incentives to develop new products or services, it is important to note that not all innovations may be socially desirable. To the extent innovations represent a competitive response to improve upon a poorly designed or poorly regulated market, they may be more a symptom of regulatory failure than the benefits of innovation. Consider the competition between ECNs and Nasdaq dealers. If the Order Handling Rules and reduction in tick size improved transparency and increased competition on Nasdaq, thereby reducing the competitive advantage of ECNs and their incentive to innovate, that does not mean that the Order Handling Rules and ECN Rule were not desirable, notwithstanding the negative impact on ECNs.

As well, the trade-through rule may have no impact on some innovative activity. For example, Instinet has a tool that allows large orders to be exposed anonymously in the upstairs market while simultaneously sending slices of the order for execution in the downstairs market. As each slice gets filled another slice is sent until the entire order is executed downstairs or until whatever is left in the upstairs market executes. In 2003 Instinet was working on making the tool available to institutional customers to use directly on their own terminals.9 There does not seem to be any specific reason why such an innovation

would not be desirable if a trade-through rule is in effect.10

7 As a competitive strategy, an incumbent marketplace may want to make it costly for an entrant to access orders sent to the incumbent marketplace.

8 Setting adverse selection issues aside, a market with more traders is more attractive since the chance of finding a trading partner is higher. Even if an entrant is much more cost efficient than the incumbent, the equilibrium can get stuck at a suboptimal level with most trading occurring on the incumbent marketplace because of its liquidity. 9 Schmerken (2003)

10 The tool called ProActive SmartRouter is currently available through Instinet Trading Portal®, NewportTM portfolio trading system, Instinet Workstation and Instinet OMS, Direct-FIX connections and is compatible with third-party order management systems. See http://www.instinet.com/dma_ecn/proactive_smartrouter.shtml.

More generally, arguments against trade-through rules stress that price is not the only characteristic important to traders and forcing all marketplaces to compete on price reduces their ability to compete on other characteristics. One counterargument is that price is almost always the most important factor and that non-price considerations are secondary. This raises an empirical question: just how important are price and non-price characteristics? Bessembinder (2003) provides some evidence. He examines quotations, order routing and trade execution costs of large-capitalization NYSE-listed stocks. Bessembinder finds that order routing strategies respond to quote placement and quotations respond to market conditions and that while quote competitiveness and size is a significant determinant of execution venue, other characteristics, including size and the information content, are also important. Bessembinder notes that while quote-based competition is substantial, it is also incomplete “as trade characteristics affect execution venue, many trades are executed away from the market posting the best quote, and average trade execution costs vary across markets when trades are routed to markets with noncompetitive quotes.” Price appears not to be everything, and hence the debate over the merits of the trade-through rule is not resolved by these arguments.

As mentioned above, a trade-through rule could interfere with an entrant’s ability to price discriminate and thus lower the profitability of entry. If entry still occurs, then this could make competition more intense by forcing marketplaces to compete more directly on price. However, if regulating the pricing structure of an entrant causes entry not to be profitable, then this will reduce competition. To some extent then a trade-through rule is likely to interfere with pricing by the marketplace. Why is this so? To be effective, a trade-through rule must address all components of price (such as commissions and access fees) and not only quotes. Otherwise, marketplaces would have an incentive to artificially narrow their spreads and increase the other fees (the so-called “outlier” business model). The SEC recognized this and thus set a cap on the fee for accessing a quote of $0.003 per share.11

Limiting the way prices can be set can increase short-run competition but it also may reduce the profitability of entry or the return to innovation, and so negatively impact on dynamic competition.12

Notwithstanding these general arguments it should be noted that we have found few specific examples where a trade-through rule would directly interfere with a possible innovation. The exception is noted by Amihud and Mendelson (2005) who provide an example of how a

11 An alternative that has been suggested would be to force all relevant fees to be included in the bid and ask quotes so that only a net price would be displayed allowing quotes to be more easily compared and removing the need to regulate the individual components of price.

12 The Deutsche Bank (2005) noted:

The setting of maximum access fees will mean that ATSs can no longer subsidize their discount prices for members out of the fees for non-members. The security price quoted by ATSs will therefore be higher in order to compensate the fall in revenues due to lower access fees. This will reduce the competitive advantage of ATSs.

depth-of-book trade-through rule would directly interfere with the ability of a marketplace to use uniform pricing.13

2.3.2. Marketplace Linkages and the Trade-through Rule

Depending on how it is applied, a trade-through rule could force marketplaces to link together, which may be an advantage to the entrant if it can compete on bids since it gets access to all possible trades on the larger exchanges without having to build links to many investors. However, it could be a disadvantage if the linkages force standardization of information flows that undermine some proprietary mechanism of the entrant.14 Also, if the

incumbent exchanges are able to undercut the entrant then forcing the entrant to link to the incumbents and forcing the entrant to match the bids charged by the incumbent without giving the entrant some way to earn additional revenue to fund innovative features may drive the

13 Limit orders are usually executed under discriminatory pricing during the trading day. Under discriminatory pricing, if the size of a market order (or marketable limit order) being executed is greater than the size of the best priced limit order, the remaining size is executed against the next-best limit order, and so on. The prices for each step of the execution are set by the individual limit prices. Under a uniform pricing rule (at least one version of it), all the limit orders are executed from best to worst price until the size of the market order is exhausted or there are no more limit orders. The price is determined by the worst-priced limit order that is executed and all executed limit orders receive this price. In the case of a market order to sell, the proceeds to the seller would be lower under uniform pricing and the cost to the investors posting limit orders to buy would be lower than under discriminatory pricing, assuming limit orders did not adjust in response to uniform pricing. However, limit orders would generally be different since a trader who places the limit order under uniform pricing would anticipate that the order could be filled at a better price. Whether uniform pricing would be better than discriminatory pricing is debatable, however Amihud and Mendelson point out that under a depth-of-book limit order rule, if a market order, say, to buy, executes against limit orders deeper in that market’s limit order book then the uniform price would be set above the best offer. A trade-through rule would force the market order to first execute against all the protected orders on other markets using discriminatory pricing.

As an example, suppose that there is one limit order on market A to sell 1,000 shares for $10 and another to sell 1,000 shares for $11. A market order to buy 2,000 shares arrives and executes against both limit orders. The uniform price is set to $11; thus, both limit orders execute at this price. Now suppose there is a second market B and two limit orders posted in that market, one to sell 1,700 shares for $10.20 and another to sell 300 shares for $10.50. Under a trade-through rule, since the worst price on B of $10.50 is better than the uniform price of $11 on A, all the execution would be done on B. If A switched to discriminatory pricing then at least the first 1,000 shares would have executed on market A at $10.

14 The SEC chose not to mandate a collective linkage facility and instead requires marketplaces to connect using private linkages. Private linkages help avoid problems associated with a public system, such as inflexibility and the lack of ownership. However, it also introduces other problems where some marketplaces may find it in their interests to increase the costs of their rivals. The SEC has prohibited imposing unfairly discriminatory terms, though such a rule needs to be actively enforced, which is costly and imperfect.

entrant out of business and discourage other potential entrants from trying to enter the market.

If entry under a trade-through rule is not profitable then there are fewer firms from which innovations can emerge. A Schumpeterian view of innovation assumes a competitive environment from which new ideas are born.15 For example, if a trade-through rule reduced

an ECN’s speed advantage and prevented it from charging differential prices then beneficial after-hours trading might not have emerged.

As soon as there is more than one marketplace trading a given security, consideration must be given to how or if the marketplaces should be linked and what type of information should be made public. In terms of information, in the United States the NBBO system was implemented to ensure that all investors know the best quotes in the country. This offers tremendous advantages in a fragmented market since the NBBO reflects the best estimates of the value of a security and so reduces uncertainty, which increases the benefit of investing to risk averse investors. The NBBO also facilitates competition by increasing price

transparency allowing investors to seek out the best prices, depending on their access to various marketplaces.

As noted earlier, US marketplaces are linked. Generally, linkages between marketplaces increase accessibility by allowing orders to be routed according to whatever rules are in place or the preferences of those trading.16 In a fully connected network anyone who is connected

to one marketplace is connected to all marketplaces. This reduces the number of linkages that need to be made, possibly by a substantial amount. For example, if there are 10 market participants and two markets, 20 linkages are required for all market participants to have access to all quotes whereas only 11 linkages are required when the marketplaces are

15 Krishnamurti, Sequeira, and Fangjian (2003) provide some interesting insight into the relationship between organizational structure and innovation. They examine the market quality of the Bombay Stock Exchange (BSE), which is mutualized, and the National Stock Exchange (NSE), which is demutualized. They find the latter’s market quality is better and they attribute this to better governance. The NSE was able to enter partly because of advances in communication and computing technologies. The “NSE dramatically improved the quality of trading services and thereby challenged the dominant position held by the BSE until that time.” The BSE lost significant market share to the NSE which forced the former to try to catch up by improving services.

16 Rather than connect every marketplace to each other one could connect all marketplaces to a central limit order book (CLOB). The CLOB shows all limit order submitted on any connected exchange and ensures price-time priority. All market orders interact with all orders on the CLOB. While this maximizes the amount of order interaction there are many critics. A CLOB eliminates any basis for differentiation and essentially monopolizes the process of trade executions. As such, it needs to be regulated like a utility which brings with it all the concomitant issues, such as how to control costs, price access, and encourage optimal levels of innovation. For examples, see Stoll (2001), Pirrong (2005), Amihud and Mendelson (2005).

connected. If there are three marketplaces, then full access requires 30 linkages if marketplaces are not connected but only 13 linkages if marketplaces are connected.17

Linking marketplaces together also removes the decision from individual market participants on which marketplaces to link to. If marketplaces do not connect then market participants must connect on their own to the new entrant. Each market participant that connects to the entrant increases liquidity available on the entrant’s marketplace making it a more desirable place to trade. However, since each market participant incurs a cost to connect and does not capture all the benefits of making the connection (assuming more competition is beneficial), too few connections will be made. Market participants would be better off coordinating their activities, which could be accomplished by the regulator forcing marketplaces to interconnect. On the other hand, if entry has a net harmful effect because of excessive fragmentation, then the externality arising from forcing individual market participants to connect can reduce the profitability of entry and thus limit the amount of competition. The generally accepted wisdom in the United States is competition is desirable and, in any case, the US capital market is sufficiently large that there will be entrants even if marketplaces are not all connected.18

In the absence of a trade-through rule that mandates linkages what incentives would exist for competing marketplaces to connect to each other? An exchange has no incentive to facilitate cream skimming of its order flow. In a market with specialists the specialist is given an information advantage (a monopoly on the limit order book) that offsets the costs of providing liquidity and maintaining an orderly market, but nonetheless needs to manage inventory and other costs. In a dealer market, dealers need to trade off risk with each other and manage their inventory positions. Thus with either specialists or dealers, there is some interest in forming linkages.

A trade-through rule implemented at the market level requires linkages between markets. Stoll (2001) lists several problems with linking downstairs markets together. First, if a linkage mechanism is imposed then each market must conform to the specified mechanism and this could impair the adoption of new technology that is not compatible. Second, a common linkage mechanism is common property resulting in underinvestment. Stoll points to the Inter-market Trading System (ITS) failure to keep pace with technology as an example. Moreover, he argues that the routing should be done by the broker in the upstairs market and that as long as the broker has access to all market quotes the routing will be in the best

17 The same type of reasoning applies to the costs of regulating a trade-through rule. If implemented at the marketplace level only the marketplaces need to develop rules to ensure trade-throughs do not occur. If implemented at the market participant level, many more entities would be required to develop rules and make sure they do not break them. The differences are obviously small when there are not too many participants or marketplaces but increase quickly as more participants join.

18 In the late 1960s when trading settlement and clearing was manual a crisis developed where the system could not keep pace with growth in trading. The “Back Room Crisis” prompted an SEC study that led to the recommendation of creating essentially a national market system. See Oesterle (2005).

interest of the customer (assuming best execution is enforced). Stoll also notes that under a strict time priority rule a limit order with a competitive price will execute in an illiquid market, and this could contribute to fragmentation.

The common ownership problem does not arise when linkages are between market

participants and marketplaces. In the United States many online brokers have implemented "smart order routing" technology, which searches for the best place to execute a customer's order. If routing is all done at the exchanges based on price-priority then smart-routing is unnecessary.

Another potential effect of the trade-through rule on routing and linkages between markets is that markets that are slow to quote, have high latency in their connections, or have more failures have little incentive to improve since they would get order flow as long as they post the best quotes. Hudson River Trading LLC (2004) argues that these incentives may give rise to perverse outcomes where a marketplace that can attract orders through stale quotes gives it an incentive to slow down its public quotations. The revised Regulation NMS addressed such problems by allowing the trade-through protection to be dropped if a

marketplace was not performing adequately. A regulatory solution, however, will generally be inefficient – either the regulation is highly prescriptive, which means that it will be slow to account for technological improvements or it may be imprecisely defined resulting in

regulatory uncertainty and the need to settle disputes. Amihud and Mendelson (2005) argue that a trade-through rule that requires tight coupling (e.g. highly prescriptive rules for linking) between market centers can restrict the ability to innovate and that looser coupling that reduces fragmentation but allows for flexibility is preferred.

2.4. T

HEE

FFECT OF AT

RADE-

THROUGHR

ULE ONC

OMPETITION INC

ANADA The conditions in Canada are much different from those in the United States. Thereorganization and consolidation of Canadian exchanges resulted in almost all inter-market competition coming from outside the country’s borders. As in many other industries, Canada has typically tolerated much higher domestic concentration levels than exist in the United States. Part of the reason for this is that minimum efficient scale dictates how many firms can operate in a market of a given size while achieving minimum costs and the simple fact that the Canadian market is much smaller than the American market means fewer firms can profitably operate in Canada.19

19 To understand the importance of market size in determining the potential number of successful marketplaces, we obtained a list of equity marketplaces (including derivative markets) operating in 111 countries and correlated the number of marketplaces in operation against GDP (measured in US dollars) for each country. The source of the data on exchange listings is http://www.tradingresource.com/ content/exchanges/exchanges.html. While there are many other factors that influence the number of marketplaces beyond size of a country (e.g., in some cases the relevant economic market may be larger or smaller than a country), we obtain the very high correlation coefficient of 0.93 between the number of marketplaces and the GDP of the country. If the United States is excluded from the data set, the correlation falls to 0.76, though this is still quite high.

Apart from the much smaller size of the Canadian market, extrapolating from the US experience to Canada is made more difficult by regulatory differences. For example, while the TSX more closely resembles the structure of the NYSE than the Nasdaq dealer market, because both the TSX and NYSE function as continuous auction markets after opening as call markets, would this mean that crossing systems are more likely to successfully compete with the TSX than ECNs, as Conrad, Johnson and Wahal found for the NYSE? Smith, Turnbull and White (2000) describe another critical difference related to the regulation of the upstairs markets in the two countries that make upstairs trading more attractive on the TSX.20

The upstairs market is effective at screening out informed trades via repeated relationships and the reputation capital built up by market makers (Smith, Turnbull and White (2001)). A crossing network would have to compete with the TSX upstairs market, which given its advantages over the NYSE and the smaller size of the Canadian market may make entry of a crossing system difficult.

Smith et al. (2001) obtain another interesting result: the upstairs and downstairs TSX markets are complementary. The upstairs orders are more likely to occur when spreads are greater and depth on the opposite side of the limit order book is low. In other words, upstairs orders are executed when downstairs liquidity is low. Thus the upstairs market adds liquidity when it is needed. Market makers trading in the upstairs market obtain liquidity that can be

transferred to the downstairs market. Since the value of the upstairs and downstairs market is internal to the TSX, there is an incentive for the TSX to design rules to maximize the value for traders in both markets. If the upstairs and downstairs market were separately owned, fragmentation might be more of a problem as the individual marketplaces would not internalize the effect that their trading rules have on the other marketplace.

While Canada will likely never have as competitive an environment as exists in the United States, Canadian marketplaces do face competition from US marketplaces, which acts to force Canadian marketplaces to remain innovative. Figure 1 shows that competition for order flow of interlisted Canadian stocks has increased substantially over the years, though it has recently stabilized. Any fragmentation that skims off valuable liquidity from the TSX increases the adverse selection costs on the TSX, which benefits US exchanges trading Canadian stocks.

20 Crosses on the TSX observe price (but not time) priority rules whereas with the NYSE a price at the inside quote is not enough to ensure the cross will proceed without having to match any of the other downstairs orders. Prices outside the quote are more expensive to execute on the NYSE since the clean up price must be announced and then all limit orders (up to that price) in the book, in the crowd and all better-displayed ITS quotes must be filled whereas on the TSX only the better-priced limit orders must be filled and at the standing price of the limit orders.

Figure 1: Canadian and U.S. shares of dollar volume traded in inter-listed Canadian stocks 0% 20% 40% 60% 80% 100%

Jan-97 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05

Traded in the U.S.

Traded in Canada

Source: TSX Review (various editions) and CRA analysis.

Competition with US marketplaces only occurs for interlisted securities. Thus Canadian regulators must contend with the trade-off between the costs of fragmentation and the benefits of competition. Amihud and Mendelson (2005) argue that a properly implemented trade-through rule must balance off these two principles of order/market interaction and market center competition.

3. MEASURING

THE

INCIDENCE AND COST OF

TRADE-THROUGHS

Measuring the incidence and cost of trade-throughs is central to any analysis of the costs and benefits of a trade-through rule. In Canada, since the reorganization of the exchanges, the opportunities for trade-throughs are much less than in the United States. There are two securities listed on the CNQ and the TSXV providing a limited opportunity for inter-market trade-throughs to occur. The recent entry of Blockbook provides additional opportunities for inter-market trade-throughs . In terms of intra-market trade-throughs, the TSX enforces an internal trade-through rule but trade-throughs by large blocks are permitted on the Montreal Exchange. Trade-throughs on stocks interlisted on the US marketplaces may also provide some information on the incidence of through activity, although inferring likely trade-through rates within Canada from those occurring on interlisted stocks may be complicated by the additional costs of trading across national boundaries. Given the lack of relevant historic data in Canada we look to the extent of trade-through activity in the United States for guidance.

The SEC’s Office of Economic Analysis (OEA) has measured the incidence and cost of trade-throughs across US marketplaces. Unfortunately, as we discuss in this section, the OEA’s analysis is flawed in several respects, such that little faith should be attached to their findings. The OEA’s estimates of trade-through activity have attracted much attention and much

criticism. While criticism was probably inevitable regardless of how good a job the OEA did to estimate trade-through rates and costs, it is unfortunate that the OEA did not undertake a more rigorous analysis. If they had, they may have been able to show that the rate of trade-throughs is sufficiently small that regulation was unnecessary regardless of what one thinks about the benefits and costs of trade-throughs.21 Establishing the converse, that trade-throughs are harmful, would be more difficult and require more than an empirical analysis of trade-through rates. On this front, the best one would expect is that an argument could be made that trade-throughs occur sufficiently often that they may be worth preventing. In this section and the following section, we discuss the difficulties that beset efforts to establish the costs of trade-throughs.

At a general level, the OEA’s attempt to estimate costs was woefully inadequate and almost certainly overstated the component of costs that the OEA was trying to measure. While the magnitude of the estimate is suspect, the ensuing debate and discussion of the OEA analysis

21 In fact, conservative estimates of trade-through rates of less than 2% led the dissenting commissioners Glassman and Atkins to conclude that “The minimal trade-through results reflected in the OEA Study do no support the conclusion that trade-throughs are a significant problem – certainly not one that justifies regulatory intervention on the scale of Regulation NMS” (Dissent of commissions Cynthia A. Glassman and Paul S. Atkins to the Adoption of Regulation NKS at 14). Of course, those taking the other position point to a 2% rate as problematic.

provides insights as to how one should analyze the cost of trade-throughs. While this debate was too late to alter US regulations, it should inform the Canadian regulatory response. We first address the issue of measuring the trade-through incidence. While there are many issues with the OEA’s estimates, a reasonable estimate is that the rate of trade-throughs is 1% to 2% of trades. However, even if this range is correct, what it means in terms of the need for a trade-through rule is not clear.

3.1. I

NCIDENCE OFT

RADE-

THROUGHSTo measure the incidence of trade-throughs is simple on its face. It requires counting the number of times the trade price is worse than the best offer and best bid on all accessible marketplaces and then dividing this by the total number of trades.22 The incidence might be

further analyzed by determining if the rate of trade-throughs differs by marketplace, by trading volume, or by stock prices. As well, the data might be examined to determine if any patterns emerge which help inform when trade-throughs are more likely and why. This is essentially what the OEA sought to undertake.

The OEA estimated a range of trade-through rates, ranging from 2% to 10% of total trades. The conservative estimate, which is likely the more accurate, is a trade-through incidence of 2% to 3%. Weighted by volume, the conservative range is between 2% and 8%. The OEA found variation in the incidence of trade-throughs across exchanges and by size of the trade. The OEA found that trade-through rates tended to be larger, the greater the size of the trade. In addition to the limited set of data, commentators found that the OEA failed to fully account for mismatches between the recorded time of trades and the recorded time of the best quotes. The result is that trade-through rates are measured with error and hence are likely over-estimated. Other criticisms include how the OEA estimated the number of shares affected by the trade-through, double counting, and failing to account for inaccessible and stale quotes.23 These criticisms identify fundamental problems with the OEA analysis. As a

result, little weight can be given to the estimated values.

The main complication in measuring the incidence of trade-throughs is that while the reported times of the limit prices are more or less accurate, the reported times for the trades are not accurate. This means that one cannot accurately match trades with the best quotes

22 Since data used for the OEA’s analysis do not show if a trade was buyer or seller initiated one counts only those trades outside the best bid and best quote as a trade-through.

23 Evidence of the problems with the analysis include the lack of complaints about trade-throughs on the exchanges where a trade-through rule under ITS allows redress, the lack of difference in trade-through rates between a set of markets where they are prohibited (under ITS) and where they are, or have been, allowed (Nasdaq), and positive estimates of trade-throughs on ArcaEx where there should be none (except due to stale quotes or inaccessible quotes).