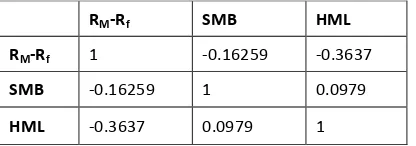

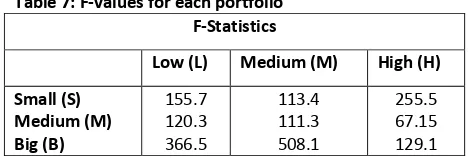

Fama and French Three-Factor Model: Evidence from Istanbul Stock Exchange

Full text

Figure

Related documents

[ 18 ], the main objective of this study is to estimate areal reduction factors based on the storm-centred approach and to derive a methodology for considering areal rainfall in

In spite of the fact that RCFs are predicted for sphere and rectangular cavity with perfectly conducting walls, it is rea- sonable to expect, as for the case of parallel plates,

call mpi_recv(buf, count, datatype, send_rank, send_tag, comm, status, ierror) where send_rank and send_tag come from the send_info in the handshake. Also notice that in this

If a member suffers a different insured illness a second claim may be payable subject to the terms described in this section, Section 3 - Optional additional cover and

In summation, we created an event portfolio deliverable that provides information about the capacity of each room to hold events, a materials list for upcoming purchases, and

This helps to ensure what is produced meets international regulatory testing and trade requirements, brand specifications, and social compliance standards with

unacceptable damage on Soviet society after absorbing an all-out Soviet surprise counterforce attack) and perhaps also had a first-strike counterforce capability (the capacity