FAIR VALUE ACCOUNTING under FAS 157 and IFRS 13: EVIDENCE from BOR

Full text

Figure

Related documents

A number of the Company’s accounting policies and disclosures required the determination of fair value, both for financial and non-financial assets and liabilities. Fair values

Si è individuato, su una cartografia aerea, l’asse stradale di progetto con l’indicazione delle fermate del sistema del trasporto pubblico urbano su gomma, i percorsi

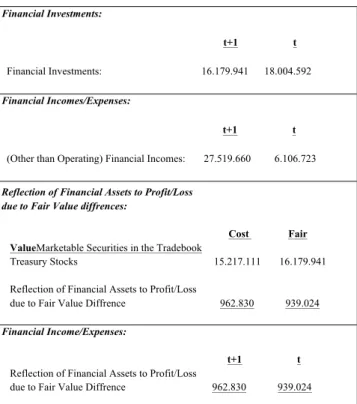

Gains and losses arising from changes in the fair value of the 'financial assets or financial liabilities at fair value through profit or loss' category are presented in the

Specifically, under IFRS 9 Financial Instruments, for financial liabilities that are designated as at fair value through profit or loss, the amount of change in the fair value of

9 The Financial Accounting Standards Board ( The Financial Accounting Standards Board ( “ “ FASB FASB ” ” ) issued FAS 141 (Business ) issued FAS 141 (Business Combinations) and

CRKC7004 Information Management Compulsory entry module (offered every month) Formative assessment at six weeks, final summative assessment at 12 weeks. Twelve weeks after

Principles (GAAP) and other guides, such as Government Accounting Standards Board (GASB) and Financial Accounting Standards Board (FASB) issuances, and professional

Fair Value Measurement - The Organization follows accounting standards consistent with the Financial Accounting Standards Board (FASB) codification which defines fair