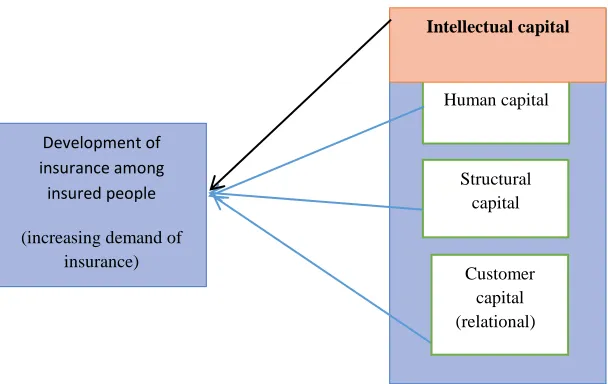

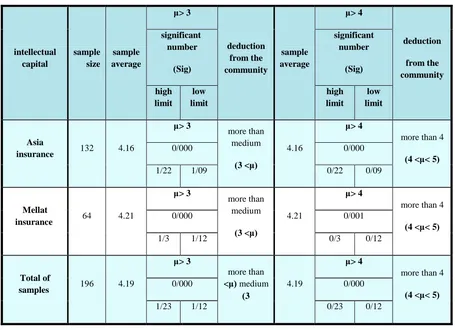

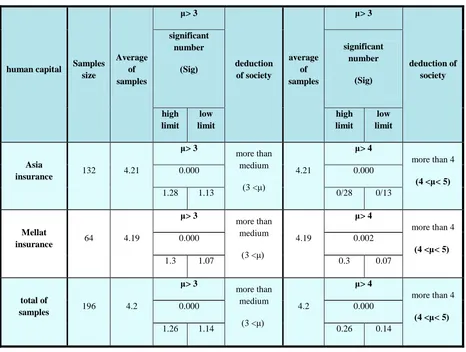

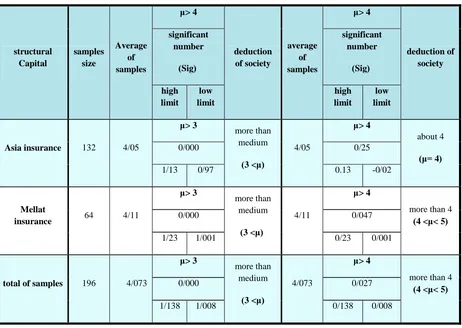

THE STUDY OF THE IMPACT OF INTELLECTUAL CAPITAL ON THE DEVELOPMENT OF INSURANCE AMONG INSURED PEOPLE

Full text

Figure

Related documents

There are infinitely many principles of justice (conclusion). 24 “These, Socrates, said Parmenides, are a few, and only a few of the difficulties in which we are involved if

drag variation with respect to angle of attack and Reynolds number, (B) coefficient of lift variation with respect to angle of attack and Reynolds number, and (C) aerodynamic

Results showed that increase in urban waste compost and manure increased corn dry matter, height, stem diameter, leaf area, leaf number, SPAD meter readings and leaf N..

In summary, neither DRD2 A1+ status nor verbal fluency moderated the (partial) mediation effect of rash impulsiveness on dependence severity through perceived impaired

Again in 2015, several surveys and stakeholder meetings organized at international level defined four basic products expected from the current EO systems ( Bontemps et al., 2015 ):

UN/EDIFACT Trade Data Interchange Directory (UNTDID)!. UN Standard Message

Tablica „Pacijenti“ (slika 23.), koja se nalazi u bazi podataka korištenoj za potrebe izrade ovoga diplomskog rada, pohranjuje podatke koji se unose na stranici unos

Mon Integrated Care (Center City) Tues Traditional MH (N Knox) Wed* (July-Mar) Traditional MH (N Knox) Wed* (Apr-July) Psychosoc Rehab (5 th St) Thurs Integrated Care