ITG Smart Limit Algorithm

Low latency algorithm for

passive trading

InTroducTIon

The new ITG Smart Limit Algorithm, or “SLimit”, algorithm addresses the challenge of trading passively in fragmented equity markets. SLimit can be thought of as a “one-sided market maker”, updating prices in real-time to balance spread capture and adverse selection risk. To avoid information leakage, SLimit sizes its orders appropriately given current market conditions and intelligently manages time priority when resizing orders. SLimit’s routing decisions are based entirely on performance, without regard for fees/rebates. SLimit considers queue lengths and expected consumption rate at each market to determine the allocation that maximizes the probability of filling. To do all this, SLimit leverages a new state-of-the-art low latency platform to implement its dynamic strategy effectively. Below, we provide details on SLimit’s four main components – pricing, sizing, routing, and technology – and highlight how these components lead to superior trading performance.

LImIT order PrIcInG

Fair Value, edge, Adverse Selection and Gaming

SLimit borrows concepts from the high frequency market making world when determining its limit price. Market makers will typically try to buy at prices below and sell at prices above the “fair value” of the stock. The difference between their quoted prices and fair value is often referred to as “edge”. This edge is the main source of profit for market makers since market makers are generally not trying to establish a position in a given asset. Instead, they hold inventory only as a means to service incoming orders and earn edge. Market makers must set edge sufficiently wide to earn a risk-adjusted return that covers their cost, including losses due to adverse selection.

SLimit takes a similar approach to pricing when executing orders for clients. Since posting at a lit exchange means giving up the immediacy of execution and bearing additional risk, limit orders should be priced to earn fair compensation for the liquidity they provide. To do this, SLimit first determines the “fair value” of the stock, and then determines fair compensation for liquidity provision, i.e., edge. SLimit then combines these two to determine the limit price: if we are buying, the limit price will be fair value minus edge; if selling the limit price will be the fair value plus edge. AuThorS

Jeff Bacidore

Managing Director, Head of Algorithmic Trading

rana Goyal

Vice President, Algorithmic Trading

Ben Polidore

Managing Director, Algorithmic Trading

Alak Vasa

Director, Algorithmic Trading

cindy Y. Yang

Assistant Vice President, Algorithmic Trading conTAcT Asia Pacific +852.2846.3500 Canada +1.416.874.0900 EMEA +44.20.7670.4000 United States +1.212.588.4000 [email protected] www.itg.com

Like market makers, SLimit also must take precautions against adverse selection. Without them, limit order trading is not much better than sending market orders. In fact, a limit buy order that fills when the offer crosses its limit price has the same performance (excluding fees) as a hypothetical market order sent at that precise point in time since both effectively pay the offer price. SLimit addresses adverse selection risk by first ensuring that the edge is sufficiently large to compensate for natural adverse selection in the market. It then continuously monitors the market and adjusts its “fair price” and “edge” as real-time market conditions change to ensure its prices do not become fodder for opportunistic traders, e.g., high frequency traders.

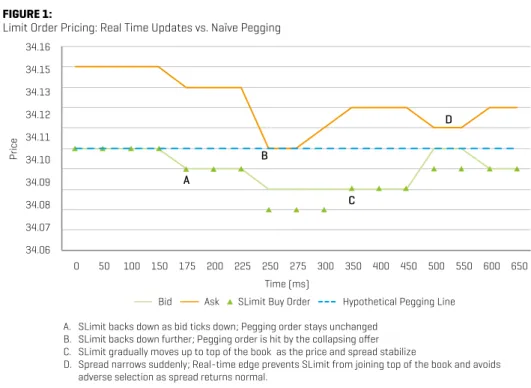

Figure 1 is an illustration of how SLimit outperforms a naïve pegging strategy by reacting to real-time information. A naïve pegging strategy simply matches the best bid as it moves upward, but never moves backward since the order itself establishes the bid, effectively preventing itself from moving downward. By contrast, SLimit is free to move as it sees fit since it is driven entirely off of its own fair value and edge calculations and is not anchored to the bid. In the example below, SLimit responds to falling prices by reducing its price to maintain edge, while the pegged order’s price by contrast would remain unchanged, eventually executing at the offer and effectively paying the spread. And when the best bid rises, SLimit does not mechanically increase its limit price to match the bid as a pegging strategy would. Rather, it sets its limit price to maintain the appropriate edge, which in the example below occurs at a price below the best bid.

34.06

A. SLimit backs down as bid ticks down; Pegging order stays unchanged B. SLimit backs down further; Pegging order is hit by the collapsing offer C. SLimit gradually moves up to top of the book as the price and spread stabilize

D. Spread narrows suddenly; Real-time edge prevents SLimit from joining top of the book and avoids adverse selection as spread returns normal.

34.07 34.08 34.09 34.10 34.11 34.12 34.13 A B C D 34.15 34.16 0 50 100 150 175 200 225 250 275 300 350 400 450 500 550 600 650 Price Time (ms)

Bid Ask SLimit Buy Order Hypothetical Pegging Line

Source: ITG

FIGURE 1:

oPTImAL order SIzInG

Blend-In, Information leakage and order Time Priority

Once the limit price is determined, SLimit then determines the appropriate sizing for the order. Placing an order on an open order book risks leaking information to other market participants so sizing must be done carefully. For instance, in seeing an oversized buy order, sellers may infer that there is a large buyer in the market and price less aggressively in anticipation of the excess buy volume. On the other hand, sizing too cautiously can result in missed fill opportunities. SLimit balances the two effects by posting only quantities that it thinks can be readily absorbed by the market, which it does by incorporating real-time depth information in sizing decisions.

SLimit also proactively manages order queues to maintain time priority. SLimit does not simply “cancel and resubmit” orders whenever it decides it wants to adjust its quantities, since doing so not only loses time priority on existing orders but also because it takes more time than sending a single “correct” message. Figure 2 shows how SLimit reacts when it wants to increase its quantity. In this example, SLimit initially has 800 shares outstanding at three markets: a 200-share order at market A, two 100-share orders at market B, and a 400-share order at market C. When SLimit decides to correct up its quantity to 1100 shares, SLimit calculates the incremental quantity it wants to expose and sends out two additional child orders for that incremental quantity: one 200-share order to market B and one 100-share order to market C. Had SLimit simply “corrected up” its existing orders at markets B and C, those outstanding shares would have lost time priority.

200

A

200 300 200B

200 100 100 100 400C

400 100 100 200 200B

400 100 100 100 100 400C

500 100 100Existing orders New orders

200

A

200

300 FIGURE 2:

Maintain Time Priority by Effectively Managing Existing/New Orders

Correction up to 1,100 shares

eFFIcIenT order rouTInG

Queue Length, Queue consumption rate, and optimal Allocation

SLimit considers both queue length and the queue consumption rate at each exchange to determine which market (or markets) to route to. Figure 3 shows a simplified example of how SLimit balances queue length and consumption rate to optimally allocate shares among markets. In this example, SLimit is determining how to allocate 6500 shares across three potential venues. Market A has the longest queue (12000 shares), but has a higher consumption rate than other markets (i.e., the highest expected volume). Market B, on the other hand, has a relatively short queue, but a much lower consumption rate. Interestingly, SLimit actually allocates the most shares to market A, even though market A has the longest queues. It does this because market A has a higher consumption rate and is expected to exhaust its queue more rapidly. Similarly, it sends the least quantity to market B despite its smaller queue, because SLimit expects market B’s queue to be exhausted much more slowly. SLimit didn’t simply ignore market B entirely due to its low

consumption rate. Rather, it mathematically determined that putting 500 shares at market B is better than placing an even larger order at markets A or C. Of course, this need not always be the case – SLimit may or may not route to multiple venues. It all depends on the quantity it wants to expose and the current state of the market.

In this example, the issue of fees was never addressed. This is because SLimit never explicitly considers fees or rebates when routing. Rather, it routes based entirely on performance. SLimit will route to “inverted” venues (i.e., venues where it pays a fee to post a passive order) whenever it thinks doing so will maximize the probability of filling, despite the higher cost. Conversely, SLimit does not blindly route to inverted venues since it knows that trading volume often executes away from those venues despite the economic incentives for marketable orders to be routed there. This can be confirmed simply by watching how liquid names like Bank of America trade, where trades will execute at non-inverted venues (e.g., NYSE, Nasdaq) even when inverted venues are posting quotes at the best bid or offer. Therefore, routing exclusively to inverted venues would not only lead to higher exchange fees, it would also degrade performance by missing a lot of execution opportunities.

Source: ITG

FIGURE 3:

TrAdInG TechnoLoGY enhAncemenT

Low Latency, direct connectivity, and colocation

SLimit’s sophisticated pricing, sizing and routing logic hinges on its ability to respond dynamically to changing market conditions. This requires SLimit to have the ability to respond to new information quickly. The underlying technology driving SLimit is “event-based” and therefore able to respond to any quote change or trade in the market. This is a dramatic shift from how algorithms have behaved

historically, where passive trading agents operated on timers, waking up every few seconds to reevaluate the market conditions. Clearly, timer-based passive trading is suboptimal since market conditions might change while the algorithm is “sleeping”, making its prices stale and exposing the order to greater adverse selection risk. When designing SLimit, ITG decided to abandon this approach entirely, giving SLimit the ability to respond in real time as markets change, not well after the fact when it may be too late.

Having a high performance, event-based platform though is only one component. For such a platform to be effective requires low latency market data and market connectivity. SLimit utilizes direct market data feeds and has direct connectivity to markets so that once it decides to take action, it can get to market as quickly as possible. The end result is that SLimit can identify and respond quickly to changing market conditions.

concLuSIon

Smart Limit, ITG’s low latency algorithm for passive trading, is a “one-sided market making” solution optimized exclusively for buy-side clients’ performance. Its goal is to effectively supply liquidity in a highly competitive, fragmented environment. SLimit features low latency infrastructure, real-time decision making, an optimal routing mechanism and intelligent adverse selection management.

We believe this quantitative algorithmic framework can maximize the chances of filling a client’s order passively, while avoiding adverse section and information leakage. By leveraging low latency infrastructure to compete in a marketplace crowded with HFTs, it improves the efficacy of passive trading, which ultimately improves overall trading performance.

SLimit is currently available to ITG clients in multiple ways. Clients get the benefits of SLimit when using ITG algorithms, such as VWAP, Active, Dynamic IS, etc. ITG’s SMART routers also employ SLimit whenever a client routes a passive order or whenever a marketable order leaves a residual which a client would like posted passively. Or clients can even route to SLimit directly, giving ITG price and size discretion when working the order.

© 2013 Investment Technology Group, Inc. All rights reserved. Not to be reproduced or retransmitted without permission. 91113-17056 Broker-dealer products and services are offered by: in the U.S., ITG Inc., member FINRA, SIPC; in Canada, ITG Canada Corp., member Canadian Investor Protection Fund (“CIPF”) and Investment Industry Regulatory Organization of Canada (“IIROC”); in Europe, Investment Technology Group Limited, registered in Ireland No. 283940 (“ITGL”) and/or Investment Technology Group Europe Limited, registered in Ireland No. 283939 (“ITGEL”) (the registered office of ITGL and ITGEL is Block A, Georges Quay, Dublin 2, Ireland). ITGL and ITGEL are authorised and regulated by the Central Bank of Ireland; in Asia, ITG Hong Kong Limited (SFC License No. AHD810), ITG Singapore Pte Limited (CMS Licence No. 100138-1), and ITG Australia Limited (AFS License No. 219582). All of the above entities are subsidiaries of Investment Technology Group, Inc. MATCH NowSM is a product offering of TriAct Canada Marketplace LP (“TriAct”), member CIPF and IIROC. TriAct is a wholly owned subsidiary of ITG Canada Corp.

These materials are for informational purposes only, and are not intended to be used for trading or investment purposes or as an offer to sell or the solicitation of an offer to buy any security or financial product. The information contained herein has been taken from trade and statistical services and other sources we deem reliable but we do not represent that such information is accurate or complete and it should not be relied upon as such. No guarantee or warranty is made as to the reasonableness of the assumptions or the accuracy of the models or market data used by ITG or the actual results that may be achieved. These materials do not provide any form of advice (investment, tax or legal). ITG Inc. is not a registered investment adviser and does not provide investment advice or recommendations to buy or sell securities, to hire any investment adviser or to pursue any investment or trading strategy. All functionality described herein is subject to change without notice.