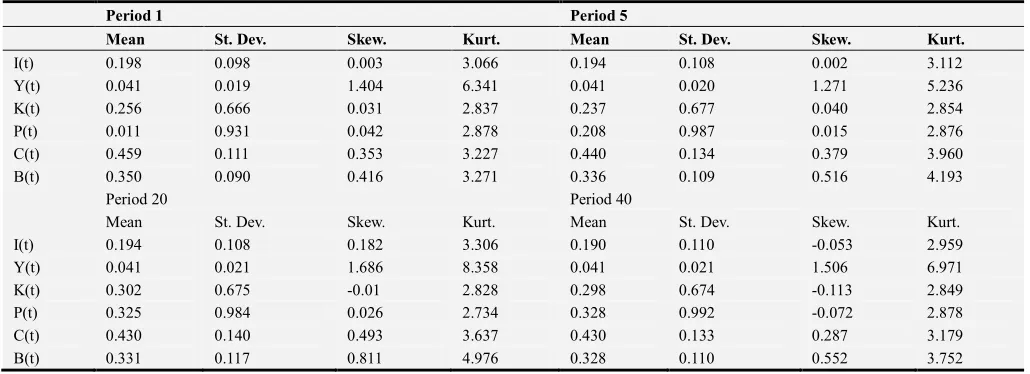

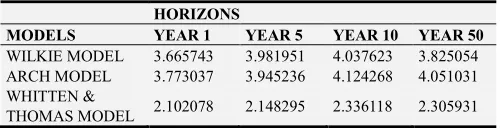

Stochastic Asset Models for Actuarial Use in Ghana

Full text

Figure

Related documents

I argue that positive global coverage of Jamaica’s outstanding brand achievements in sports, music and as a premier tourism destination, is being negated by its rival brands –

innovation in payment systems, in particular the infrastructure used to operate payment systems, in the interests of service-users 3.. to ensure that payment systems

Discrete particle CFD sub-model development for black liquor droplet combustion, TEKES, Akademy of Finland, Andritz, Metso, International paper, UPM, Åbo Akademi, project

quer cetin, t etrah ydr ox ymetho xyfla vone , apigenin meth yl ether , dimeth ylquer - cetigetin, lut eolin Alum W ool Quer cetin, lut eolin meth yl ether , t etrah y- dr ox

Locally advanced prostate cancer (LAPC), androgen deprivation therapy (ADT), androgen receptor (AR), dose-escalation, external beam radiotherapy (EBRT), conformal radiotherapy

Requisitos: Java Runtime Environment, OpenOffice.org/LibreOffice Versión más reciente: 1.5 (2011/09/25) Licencia: LGPL Enlaces de interés Descarga:

The NTSB report stated that the high velocity of the diesel in the tank fill piping and the turbulence created in the sump area resulted in the generation of increase static charge

The encryption operation for PBES2 consists of the following steps, which encrypt a message M under a password P to produce a ciphertext C, applying a