STOCK EXCHANGE OPTIONS

by

J. G. DAY

A 'CALL' OPTIONT H E best known and most common type of option is that where an investor pays money (option money) for the call—that is for the right to buy shares at the current price in 3 months time.

This is best explained by an example. Suppose share A stands at 50s. (market price 49s. 10½d.-50s. I½d.) and the option rate is 4s. Then the investor pays:

Option money

Commission (as for buying a share at 50s. I½d.) 4s,

os. 7½d.

4s. 7½d.

This payment gives him the right to buy the share at the 'striking price' on any 'declaration day' within the term of the option.

The 'striking price' at which the investor may buy share A is made up as follows:

Buying price (at the time the option is negotiated) Contango money

50s. I½d.

is. (say) 51sr. I½d. Thus the investor pays 4s. 7½d. in any event and 55s. 9d. (being 45. 7½d. plus 5IS. I½d.) if he exercises his right to buy the shares. The contango money is approximately the dealer's cost of contanging the stock during the term of the option, i.e. interest for 3 months on 5os. I½d. at 7½% p.a.; the reasons for this charge will be explained in greater detail on p. 44 below.

The last Thursday in each Stock Exchange Account is a ' declara-tion day', so that an investor is free to exercise his opdeclara-tion in any account during the term of an option. Most options are nominally for 3 months, but the actual full term is determined by the

4I

STOCK EXCHANGE OPTIONS

ment day which is quoted. For example, option rates are currently* being quoted for mid-May settlement which means that the Settlement day would be Tuesday 17 May for the last declaration day which would be 12 days previous, Thursday 5 May. Depending on when it is taken out the term of a 3-month option normally varies from 13 weeks 3 days to 15 weeks 2 days. The amount of the contango money charged is fixed at outset and is, consequently, the same whenever, during the term, the option is exercised.

Options may also be taken out for 1 month or 2 months and for these the rates are somewhat lower and the contango money is less.

PROSPECT OF PROFIT OR LOSS ON A 'CALL' OPTION

In our example the investor paid 4?. 7½d. in any event and 555. 9d. if he exercised his right to buy the shares. There are three possibilities:

(a) If the shares stand at 51s. 1½d. or less, the option is not worth exercising and the loss is 4s. 7½d.

(b) If the shares rise to 51s. I½d.-55s 9d. the option is worth exercising and the loss is less than 4s. 7½d.

(c) If the shares rise over 55s. 9d. the investor makes a profit. At 55s. 9d. the investor breaks even and this requires a rise of over 11 % in the share price; the investor pays out 4s. 7½d. in any event and to achieve a profit of 4s. 7½d. the share price must rise by over 20%.

The figures are on middle prices. Usually the investor wishes to sell so that the price has to be slightly higher, e.g. at 55s. 10½d. to sell at 55s. 9d. and break even. There is no commission on the sale, provided the investor sells in the same account as the declaration day. If the shares are taken up 2 % stamp duty is payable, but this is so for any purchase.

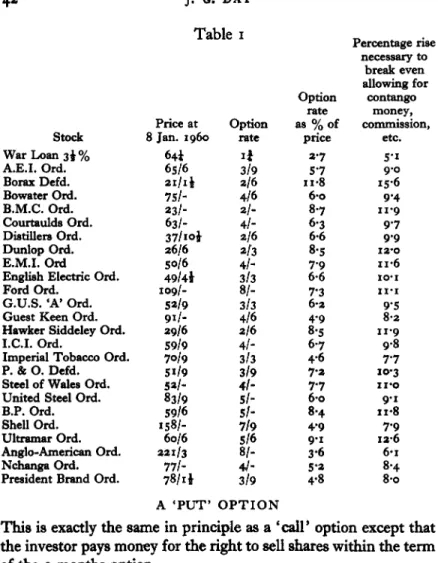

Table 1 shows that for most shares a rise of 10% is needed to break even on an option, and that for a share such as Borax the rise has to be as great as 15 %. In most normal conditions, therefore, options do not pay because the cost is prohibitive.

42

Table I Percentage rise

necessary to break even allowing for contango money, commission, etc. Option rate as % of price Option rate Price at 8 Jan. I960 Stock War Loan 3½% A.E.I. Ord. Borax Defd. Bowater Ord. B.M.C. Ord. Courtaulds Ord. Distillers Ord. Dunlop Ord. E.M.I. Ord

English Electric Ord. Ford Ord.

G.U.S. 'A' Ord. Guest Keen Ord. Hawker Siddeley Ord. I.C.I. Ord.

Imperial Tobacco Ord. P. & O. Defd. Steel of Wales Ord. United Steel Ord. B.P. Ord. Shell Ord. Ultramar Ord. Anglo-American Ord. Nchanga Ord. President Brand Ord.

64¼ 65/6 21/I½ 75/- 23/- 63/-37/10½ 26/6 So/6 49/4½ 109/-53/9 91/-29/6 59/9 70/9 5i/9 52/-83/9 S9/6 158/-60/6 221/3 77/-78/I½ 1¾ 3/9 2/6 4/6 3 / - 4/-2/6 2/3 4/-3/3 87-3/3 4/6 2/6 4/-3/3 3/9 4l- 5l-7/9 S/6 8/- 4/-3/9 2.7 5.7 II.8 6 0 8.7 6.3 6.6 805 7.9 6.6 7.3 6 2 4.9 8.5 6.7 4.6 7.3 7.7 6 0 8.4 4.9 9 . i 3.6 5.2 4.8 5.I 9.0 15.6 9.4 11.9 9.7 9.9 I2.O II.6 IO.I I I - I 9.5 8.2 II.9 9.8 7.7 10.3 II.O 9.I 11.8 7.9 12.6 6.I 8.4 8.o A 'PUT' OPTION

This is exactly the same in principle as a 'call' option except that the investor pays money for the right to sell shares within the term of the 3 months option.

As before the investor pays option money plus commission, but, as it is a sale, the striking price is the selling price at the time the option is negotiated and no contango money is required.

The option rate for a 'put' is normally the same as for a 'call', but they are not so common, partly because human nature is optimistic and partly because of technical difficulties (see p. 45 below).

43

STOCK EXCHANGE OPTIONS

A 'PUT AND CALL' OPTION

This is a double option, whereby the investor pays money (usually double the option rate) for the right to buy or sell at the ' striking price' during the period of the 3 months option. No contango money is payable and, as he will not want to both buy and sell, only one commission is payable. The striking price is normally the middle price or any suitable price within reason.

In the example on p. 40 the investor would pay 8s. y^d. (twice 4s. plus 7½d. commission) and he would have the option to buy or sell at 50s. The possibilities of profit or loss are as follows. (a) If the shares stand between 41s. 4½d. and 58s. 7½d., one of the

two alternative options is worth exercising and the loss is less than 8s. 7½d.

(b) If the shares fall below 4IS. 4½d. or rise above 58s. 7½d., then either a 'put' or 'call' option is worth exercising and there is a

profit.

These prices should be adjusted for the jobber's turn if the investor decides to buy/sell against exercising his put/call option. The break-even points are 4Is. 4½. and 58s. 7½d. and this spread of 17s. 3d. represents almost 35% or a movement of 17½% either side. The cost of a 'put and call' option is, therefore, normally prohibitive.

•GIVING' OR 'TAKING' MONEY

An investor who pays to take out an option, 'gives' money for the 'put' or 'call' as it may be.

The other side of the coin is the dealer who 'takes' this money for the' put' or' call'. It is possible for investors to take the dealer's role and 'take' money for options. The reasons for this and its effect on institutions are discussed below.

THE OPTION DEALER'S TECHNIQUE

One might have thought that 1959, a year of rapidly rising shares prices, an election result which was at least surprising in some of its implications for investors, and a year which included a rash of take-over bids and struggles, would have been disastrous to option

44

J-dealers. But surprisingly perhaps, it was an extremely prosperous year for them; they are by nature suspicious of innocent inquiries and quick to cover an exposed position, and above all they thrive on market activity.

Traditionally an option dealer, when he has taken money for a call option, buys hah0 the stock so that he is partly covered. If he can also persuade the jobber to take money for a ' put and call' option for the other half then he is completely covered, e.g. if the option is called he has half the stock and himself calls half from the jobber; if the option is not called, he has the option to 'put', i.e.

sell, the shares he has bought at the striking price.

Obtaining a put and call option for half the stock is rare however and the dealer may be forced to run half the option, buying a further half or selling the half already bought if he judges it necessary.

The contango money in the cost of the option is to cover the cost of buying and carrying the stock. If the option dealer buys stock, he does not wish to pay for the stock (and pay stamp duty); he, therefore, buys, but contangos his purchase from account to account, i.e. he postpones settlement and payment, paying interest on the money. These contango facilities are usually provided by the jobbers or financial institutions. For example a large investor may wish to sell a line of stock at the current price, but does not necessarily need or want the cash; it will, therefore, be prepared to forego payment for some weeks receiving contango money (a reasonable rate of interest on its money). In these circumstances the taking of options causes purchases of stock which are financed by jobbers (and they probably in turn by the banks) or by large financial institutions.

Contango facilities, however, are erratic and the volume of options since they were restarted in October 1958 has been much greater than before the war. The dealer may be forced to buy stock and pay for it; this involves paying stamp duty and paying the cost of borrowing the money to pay for the stock (this is usually more expensive than contanging).

At the moment, however, the dealer's main technique for widely dealt in shares is to obtain a financial institution to 'take' money

45

STOCK EXCHANGE OPTIONSfor call. For example he may quote a price of 7s.-7s. 9d. for options in Shell; meaning that investors must pay 7s. 9d. for a 'call' option on Shell, but that he will offer an institution 7s. for the 'call' of Shell. By this means he usually sets off many small 'call' options with one large option on an institution.

The large financial institutions vary their policies with market conditions on the contango facilities they are prepared to grant and the option money they are prepared to take (see page 46) so that dealers are always adjusting their business to the techniques available to them.

Put options are not so easy for a dealer to cover in the market, because if he sells half he may not be able to hold up names indefinitely (i.e. the buying broker may demand delivery of some-thing he has not got). He would, therefore, have to rely on covering with institutions, who often will not accept money for the 'put.'

Perhaps oddly, option dealers are brokers, so that they can deal with jobbers as principals, but they may not deal directly with financial institutions when covering an option. They have to deal through other brokers who charge half commission to the institution.

OPTION RATES

Option dealers often lose money on take-over bids and other sudden unexpected results. This is balanced by their profit on many straight forward options, so that in general it is not worth while to pay money for an option.

If one asks for the option rate on a comparatively rarely dealt in share the option dealer either refuses to quote a rate, if he thinks that he cannot even partly cover himself, or he quotes a high rate bearing in mind 'high' and 'low' prices in recent years and what dividend announcements or other statements may be made during the currency of the option.

In general, however, option rates depend on supply and demand. If more investors want to take out call options than the dealer can get institutions to take money for (or cover in the market) then the option rate rises and vice versa.

46

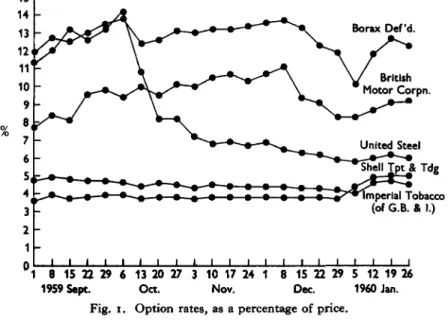

The chart (Fig. I) shows how some option rates varied over the period from just before the 1959 election until 3 months afterwards. It is perhaps surprising that option rates have not fluctuated more (United Steel in this period rose from 38s. 6d. to 86s. 4½d.).

Borax Def'd. British Motor Corpn. United Steel Shell Tpt& Tdg Imperial Tobacco

(of G.B. & I.)

1959 Sept. Oct. Nov. Dec. I960 Jan.

Fig. 1. Option rates, as a percentage of price.

EFFECT ON I N S T I T U T I O N S

If institutions consider a market is too high it may suit their view to take contango money as a short-term investment.

In the same way taking money for the 'call' or 'put' of shares may suit an institution's view of the market. For example, if an institution takes 4s. a share for the 'call' of 10,000 'A' shares and at the same time buys 10,000 'A' shares at 50s. I½d., then if the option is not exercised it has purchased 10,000 'A' shares at the cheap price of 46$. 4½d. and if the option is exercised it hands over the shares it has purchased and has, in fact, received a very high rate of interest (option money, plus contango money less stamp duty and commission) on its money for 3 months. If it considers the market high this may be good policy.

47

STOCK EXCHANGE OPTIONS

Institutions are usually less willing to take money for the 'put' than for the 'call', because there is no contango money and because it is normally, from their point of view, more speculative to take for the 'put'.

EFFECT ON MARKET

Option dealing is of use to jobbers, but during 1959 the main bulk of option dealing was speculative. It has probably helped to improve the market in the widely dealt in shares, but the market in one or two lesser known shares has been overshadowed by option dealing; and it has, on occasions, had a pronounced effect on prices on declaration days, the last Thursdays in the accounts.