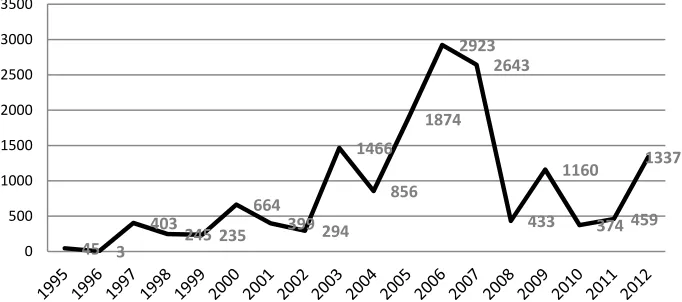

Outward FDI from Hungary: the Emergence of Hungarian Multinationals

Full text

Figure

Related documents

Wh haatt ccllu ue e w wo orrd d iiss u usse ed d iin n tth hiiss p prro ob blle em m?.. Wh haatt o op pe erraattiio on n ssh ho ou ulld d yyo ou u u

Compensation Regulations at Annual and Supplemental Assessment Stages Students must pass modules totaling at least 50 ECTS credits and have an overall average mark of 40%. If

High estimates of heritability coupled with genetic advance as per cent of mean were exhibited for early seedling vigor, plant height, panicle exertion, 100 seed weight, number

For each case study, nonlinear incremental dynamic analyses have been performed adopting successively the seven artificially generated accelerograms. All selected collapse

His passion for wildlife led him to include in the stewardship plan management practices that would expand wildlife habitat opportunities. Part of this was accomplished by

The apparent effect of this proposed rule is to allow Eligible Professionals (EPs), Eligible Hospitals (including Critical Access Hospitals) (EHs) to continue to use the 2011

If the vehicle is not in use (ignition off) while a traffic information station is received and the traffic information function is switched on, incoming traffic reports from