393

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

Volume-5, Issue-3, June-2015

International Journal of Engineering and Management Research

Page Number: 393-400

Dematerialization of Shares & Retail Investors in India - A Study

Dr. Surendar G

Assistant Professor, Department of Business Management, SR Engineering College (Autonomous), Waranagal, Telangana, INDIA

ABSTRACT

This paper is attempted to know the level of understanding on dematerialization of shares among the retail investors in India. In the process, the theoretical aspects of dematerialization like need and importance, benefits, and procedure for it are presented as a prelude to the empirical analysis. It is found from the study that all the sample investors had a demat account except very little amount. Majority of the investors had all their shares in demat form. Still there is a need to create awareness among retail investors and encourage them to dematerialize their shares that have not done. ‘Not understanding the dematerialization system and account maintenance charges’ are the major reasons cited for partial dematerialization of shares.

Keywords--- Retail Investors, Equity Shares,

Dematerialization

I.

INTRODUCTION

Dematerialization or ‘Demat’ is a process whereby securities such as shares, debentures, are converted into electronic data and stored in computers by a Depository. Physical form securities registered an investor’s name are surrendered to depository participant (DP)and these are sent to the respective companies who will cancel the physical paper after “Dematerialization” and credit investor’s depository account with the DP. The securities on Dematerialization appear as balances in investor’s depository account. These balances are transferable like physical shares. Later, if an investor wishes to have these ‘demat” securities converted back into paper certificates, the same can be done with the help of the Depository. At present, there are two depositories in India; they are National Securities Depository Limited (NSDL) and Central Depository Services Limited (CDSL). These depositories have appointed different Depository Participants (DP) for them. An investor can open an account with any of the depositories’ DP. However, transfers arising out of

trades on the stock exchanges can take place only amongst account-holders with NSDL’s DPs

II.

NEED FOR

DEMATERIALIZATION

Dematerialization was introduced to overcome the problems associated with physical form of securities. Most of these problems arose due to the intrinsic nature of paper based trading and settlement, like theft or loss of share certificates, delay in transfer of shares, possibility of forgery on various documents leading to bad deliveries and legal disputes, prevalence of fake certificates in the market, mutilation or loss of share certificates in transit, etc. The physical form of holding and trading in securities also acts as a bottleneck for broker community in capital market operations.

In this scenario dematerialization was introduced. The Depositories Act, 1996 enacted by the Indian Parliament has facilitated paperless trading by way of dematerialization of shares. Securities and Exchange Board of India (SEBI) and the Government of India together have endeavored from time to time to ensure that the concept of paperless trading is effectively implemented for the benefit of the investors at large.

III.

OBJECTIVE OF THE STUDY

• To study the need and procedure of dematerialization of shares in general

• To study the level of understanding on dematerialization of shares among retail investors.

IV.

METHODOLOGY

394

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

native place; hence I have selected Warangal as one of the cities to study. Admittedly, the sample does not represent the country’s entire population but only “the universe of potential investors”. Secondary data is also used to supplement the findings drawn from the primary data. The secondary data is collected from the various sources available like websites mainly SEBI, RBI, BSE and NSE, Magazines, Journals etc. wherever necessary.

Sample Design:Retail investors from five cities namely

Bangalore, Chennai, Hyderabad, Mumbai and Warangal, who have been operating for a period of two years or more are still performing during the period of the study are selected on the basis of convenient sample method. For an in depth study 100 literate retail investors have been selected from each city. And these retail investors are identified from the selected cities with the help of stock broking houses like Kotak Securities Ltd., ICICI Securities Pvt. Ltd., India Bulls Securities Ltd and Share Khan, etc

Data Analysis: The data is analyzed by employing

simple statistical tools like averages, mean standard deviation. Pie-charts and bar charts are also used to present the data wherever required. Further standard deviation is also used to judge the homogeneity of the mean.

V.

BENEFITS OF

DEMATERIALIZATION

Transacting through the depository way has several advantages over the traditional system of transacting using share certificates. Some of the benefits are: (a) Trading in Demat completely eliminates the risk of bad deliveries, which in turn eliminates all cost and wastage of time associated with follow up for rectification. (b) In case of transfer of electronic shares, investors save 0.5% in stamp duty. (c) The investors also avoid the cost of courier/notarization/ the need for further follow-up with his broker for shares returned due to company objection. (d) In case the certificates are lost in transit or when the share certificates become mutilated or misplaced, to obtain duplicate certificates, the investor has to spend at least Rs.500 for indemnity bond, newspaper advertisement etc, which can be completely eliminated in the demat form (g) He can also expect a lower interest charge for loans taken against demat shares as compared to the interest for loan against physical shares. This could result in a saving of about 0.25%to 1.5%. Many banks have implemented this.

George Mathew (1999) mentioned in their study titled “Small investors opting out of demat shares” that small investors are flocking to the odd-lot counters of brokers to sell off their small holdings and avoid going to the depository for mandatory scrip less trading which improves efficiency and allow quick electronic transfers. Government and SEBI should create awareness on dematerialization of their shares among retail investors;

otherwise the intention of this program may not fulfill its purpose.

VI.

PROCESS OF

DEMATERIALIZATION

Whenever an investor wishes to dematerialize the securities, he or she has to fill a Demat request from (DRF) provided by the depository Participant (DP) for dematerialization of share. The form is submitted along with the physical certificates. Each security comes with a unique international securities number (ISIN) and each different ISIN requires a different request form to be furnished. The process of Dematerialization involves the following steps:

1) Investor submits Physical Share Certificates with the DRF to the DP

2) The depository is intimated of the request by the DP

3) The certificates are submitted to the issuer company’s registrar

4) The Dematerialization request is confirmed by the registrar

5) Registrar than updates accounts after Dematerialization and informs the depository of the completion of the process

6) Depository updates accounts and information is passed on the DP

7) Investor’s Demat account is updated by the DP

VII.

DEMATERIALIZATION

CURRENT SCENARIO

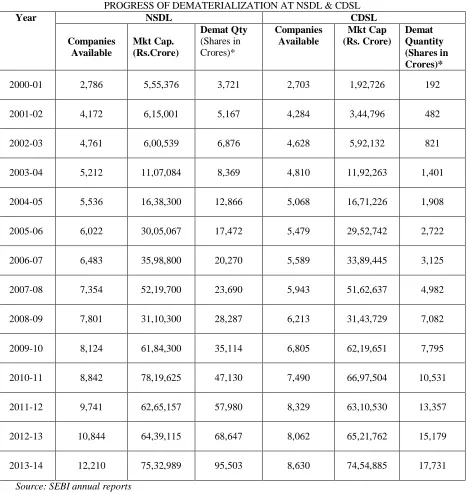

At the end of March 2014, there are 130.6 lakh demat accounts at NSDL and 87.8 lakh demat accounts at CDSL. As on March 31, 2014, 12,210 companies have signed up for dematerialisation at NSDL and 8,630 at CDSL The quantity of dematerialised securities increased by 15.9 percent to 79,550 Crores in 2013-14 from 68,647,58 crores in 2012-13 at NSDL. At CDSL too, the quantity of dematerialised securities increased by 16.8 percent from 15,179 crores in 2012-13 to 17,731crores in 2013-14. The quantity of dematerialised shares increased at the CDSL but both the quantity and value of shares settled in demat declined. On the other hand at NSDL, the value of shares settled in demats increased but the quantity of shares settled in demats decreased. The total value of demat settled shares increased by 6.2 percent from 12,72,531 crore in 2012-13 to 2012-13,51,886 crore in 202012-13-14 at NSDL. However, at CDSL the value of shares settled in demat decreased by 2.8 percent from 3,18,559 crore in 2012-13 to 3,09,767 crore in 2013-14. The ratio of dematerialised equity shares to total outstanding shares of listed companies was 83.8 percent at NSDL and 13.8 percent at CDSL at the end of 2013-14.

395

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

TABLE 1

PROGRESS OF DEMATERIALIZATION AT NSDL & CDSL

Year NSDL CDSL

Companies Available

Mkt Cap. (Rs.Crore)

Demat Qty (Shares in Crores)*

Companies Available

Mkt Cap (Rs. Crore)

Demat Quantity (Shares in Crores)* 2000-01 2,786 5,55,376 3,721 2,703 1,92,726 192

2001-02 4,172 6,15,001 5,167 4,284 3,44,796 482

2002-03 4,761 6,00,539 6,876 4,628 5,92,132 821

2003-04 5,212 11,07,084 8,369 4,810 11,92,263 1,401

2004-05 5,536 16,38,300 12,866 5,068 16,71,226 1,908

2005-06 6,022 30,05,067 17,472 5,479 29,52,742 2,722

2006-07 6,483 35,98,800 20,270 5,589 33,89,445 3,125

2007-08 7,354 52,19,700 23,690 5,943 51,62,637 4,982

2008-09 7,801 31,10,300 28,287 6,213 31,43,729 7,082

2009-10 8,124 61,84,300 35,114 6,805 62,19,651 7,795

2010-11 8,842 78,19,625 47,130 7,490 66,97,504 10,531

2011-12 9,741 62,65,157 57,980 8,329 63,10,530 13,357

2012-13 10,844 64,39,115 68,647 8,062 65,21,762 15,179

2013-14 12,210 75,32,989 95,503 8,630 74,54,885 17,731

Source: SEBI annual reports

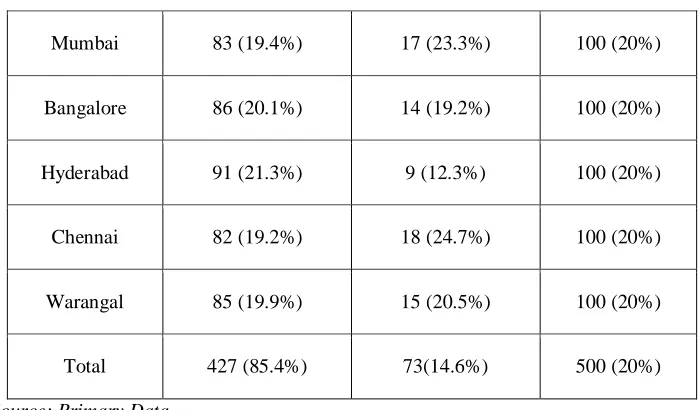

In the above background investors were enquired whether they know what the dematerialization is? The response of the investors is mentioned in the following table 2.

TABLE 2

CITY WISE INVESTORS’ OPINION ON UNDERSTANDING DEMATERIALIZATION

City of Respondent

Did you understood the concept of dematerialization of shares

Total

396

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

Mumbai 83 (19.4%) 17 (23.3%) 100 (20%)

Bangalore 86 (20.1%) 14 (19.2%) 100 (20%)

Hyderabad 91 (21.3%) 9 (12.3%) 100 (20%)

Chennai 82 (19.2%) 18 (24.7%) 100 (20%)

Warangal 85 (19.9%) 15 (20.5%) 100 (20%)

Total 427 (85.4%) 73(14.6%) 500 (20%)

Source: Primary Data

The table reveals that 85.4% (427) of the total responded retail investors were able to understand the dematerialization of shares where as only about 14.6% of the respondents i.e., 73 out of the total respondents (500) have said that they did not understood the dematerialization of shares. It means majority of the respondents knows the dematerialization of shares.

Further, an attempt is also made to test whether there is any significant difference among the sample respondents belongs to selected cities with regard to their understanding the dematerialization concept.

Null Hypothesis (Ho): There is no significant difference among respondents belongs to selected cities with regard to their perception on dematerialization of shares.

Since the calculated value (3.946) is less than the table value (9.488) at 5% significance level, hence the null hypotheses is not rejected or the null hypothesis is accepted. Therefore it may be concluded that there is no significant difference among respondents belongs to

selected cities with regard to their perception on dematerialization of shares.

Further the investors were enquired whether they have a demat account? Table 3 presents the response of the investors.

TABLE 3

INVESTORS HAVING DEMATERIALIZATION ACCOUNT

Do You have a Demat

Account? No. of Investors % of Investors

Yes 483 96.6

No 17 3.4

Total 500 100.0

Source: Primary Data

Chi-Square Test

Value df

Asymp. Sig. (2-sided) Pearson Chi-Square 3.946a 4 .413

397

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

The table reveals that 96.6 percent of the investors have a demat account and 3.4 percent of the investors did not have a demat account. This means almost all investors (around 97%) had demat accounts, very little amount of

investors i.e., 3.4% of the investors did not have demat account.

Further the investors were enquired whether they have all their shares in the demat form? Their responses are given in Table 4.

TABLE 4

PERCENTAGE OF SHARES IN DEMAT FORM

Shares Dematerialized

No. of Investors

% of Investors

Fully 444 88.8

Partly 39 7.8

Not 17 3.4

Total 500 100.0

Source: Primary Data

The above table reveals that 88.8 percent of the sample investors had all their shares in demat form, whereas 7.8 percent of the investors had at least some shares in the physical form and remaining 3.4 percent share holders having no demat account, it means that these investors are still having their shares in physical form only.

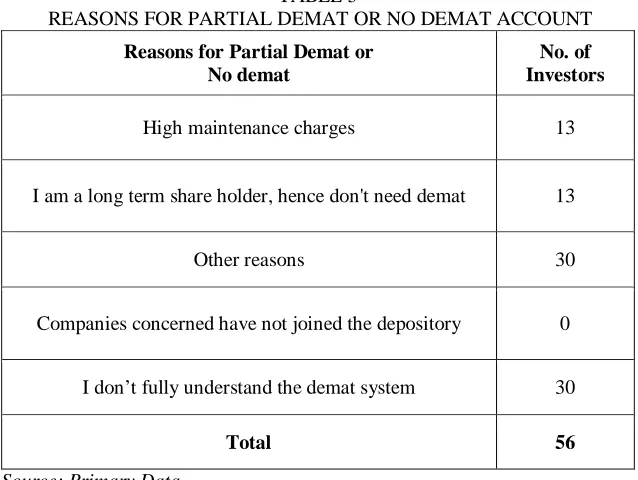

Investors were also enquired the reasons for partial dematerialization of shares. Reasons vary from the investor to investor. The responses of the investors for this

are given in table 5.7.

TABLE 5

REASONS FOR PARTIAL DEMAT OR NO DEMAT ACCOUNT

Reasons for Partial Demat or No demat

No. of Investors

High maintenance charges 13

I am a long term share holder, hence don't need demat 13

Other reasons 30

Companies concerned have not joined the depository 0

I don’t fully understand the demat system 30

Total 56

Source: Primary Data

It reveals that the ‘Other reasons’ and ‘I don’t need a demat account’ are the major reasons to not to join

398

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

demat’ are the next leading reasons for not joining or partial demat of shares. Hence, they are compelled to retain those companies’ shares in the physical form.

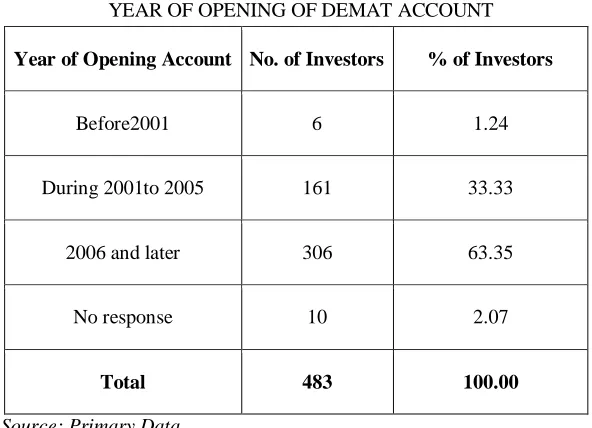

Further, the investors were enquired about the year of opening of their demat account. The responses are tabulated in Table 6.

TABLE 6

YEAR OF OPENING OF DEMAT ACCOUNT

Source: Primary Data

Table brings out that one third of the sample investors have opened their account during 2001 to 2005, 63% of the sample investors have opened during 2006 and later. Before 2001 there was a too little respondents having demat accounts i.e., 1.24 percent of the total respondents.

Further the investors who are dematerialized their shares fully or partly were enquired about the problems faced while dematerialization, the response provided in the

following table 7.

TABLE 7

OPINION ON PROBLEMS FACED WHILE DEMATERIALIZING THE SHARES

Response No. of Investors % of Investors

Yes 69 14.29

No 414 85.71

Total 483 100.00

Source: Primary Data

Table 7 reveals that out of the total respondents who have dematerialized their shares, 69 investors have faced the problems. It means less amount of investors have faced problems while dematerializing their shares. Further,

an attempt is made to find the reasons they faced while dematerializing the shares. Reasons are mentioned in the following table 8 Year of Opening Account No. of Investors % of Investors

Before2001 6 1.24

During 2001to 2005 161 33.33

2006 and later 306 63.35

No response 10 2.07

399

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

TABLE 8

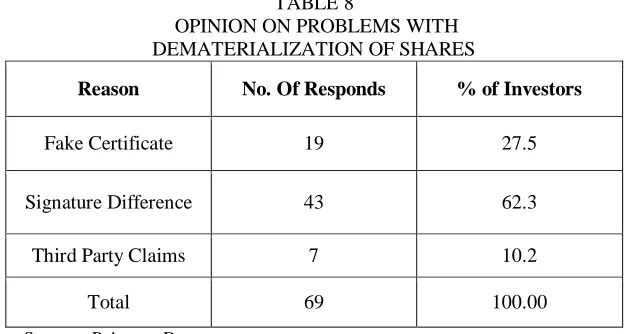

OPINION ON PROBLEMS WITH DEMATERIALIZATION OF SHARES

Reason No. Of Responds % of Investors

Fake Certificate 19 27.5

Signature Difference 43 62.3

Third Party Claims 7 10.2

Total 69 100.00

Source: Primary Data

Most of the investors i.e., 43 out of 69 responses faced a problem ‘Signature Difference’ while dematerialization the shares. The reason might be the time between purchases of shares and dematerialization them and the second reason is ‘fake certificate’. Only 10.2 percent of the investors have faced the problem i.e., third party claims.

Investors further asked opinion on the dematerialization relative statements namely ‘With Demat ownership transfer made fast, Demat has increased volume

of transactions, With Demat fake certificates and forgeries have disappeared, Due to demit transaction costs and charges have been reduced’ and measured using the likert five point scale ranging from strongly agree to strongly disagree. Strongly agree option was assigned a weight of five and strongly disagree option was assigned a weight of one. In between these two extremes other levels such as agree, neither agree nor disagree and disagree were assigned weights of four, three and two respectively.

TABLE 9

MEAN AND STANDARD DEVIATION OF INVESTOR’S OPINION ON DEMATERIALIZATION OF SHARES

Statements N Mean Std. Deviation

With Demat ownership transfer made fast 483 3.27 1.519

Demat has increased volume of transactions 483 3.07 1.187

With Demat fake certificates and forgeries have

disappeared 483 3.06 0.953

Due to demit transaction costs and charges have

been reduced 483 3.05 1.079

Source: Primary Data

The above Table reveals that the investors strongly agree with the statement, ‘With demat ownership transfer is fast’. They also agree to the statements that ‘With demat fake certificates and forgeries have disappeared’. Thus one of the SEBI’s expectations with regarding to dematerialization ‘The reduced risk’

400

Copyright © 2011-15. Vandana Publications. All Rights Reserved.

disagrees to the statement that ‘Demat has reduced the transaction costs and other charges’ and disagreed to the statement ‘Demat has increased volume of transactions’. It can be interpreted that investors’ opinion towards these statements is they expect SEBI to take many more steps to bring down the transaction and other charges associated with dematerialization and simultaneously should increase the volume of transactions.

VIII.

CONCLUSION

From above study it revealed all the sample investors had a demat account except very little amount i.e., 3%. Majority of the investors had all their shares in demat form. Still there is a need to create awareness among retail investors and encourage them to dematerialize their shares that have not done. ‘Not

understanding the dematerialization system and account maintenance charges’ are the major reasons cited for partial dematerialization of shares.

REFERENCES

[1] George Mathew, “Small investors opting out of demat shares”, Indian Express News Paper, May 23, 1999 [2] M.S.Sahoo, “An Overview of the Securities Markets in India”, SEBI Bulletin, March, 2005,

[3] Dr. P Venugopal et al, “Small Investors’ Grievances and Redressal Mechanism in Indian Capital Market” IJMR, Vo. 2,Issue 7, July 2012, ISSN 22315780,