Motivation Discounting Discounting Plant-Level Optimization Results

Do Interest Rates Smooth Investment?

Russell Cooper1 Jon Willis2 1Pennsylvania State University 2Federal Reserve Bank of Kansas City

Motivation Discounting Discounting Plant-Level Optimization Results

Question: How do variations in the interest rate influence

plant-level and aggregate investment?

The answer will improve our understanding of:

Motivation Discounting Discounting Plant-Level Optimization Results

Micro evidence

Investment at the plant level is characterized by infrequent adjustment.

Motivation Discounting Discounting Plant-Level Optimization Results

Micro evidence

Investment at the plant level is characterized by infrequent adjustment.

Motivation Discounting Discounting Plant-Level Optimization Results

Previous research

Research of Thomas (2002), Khan and Thomas (2003), and Khan and Thomas (2008) concludes that non-convexities at the plant level are not important for aggregate investment.

State dependent interest rates in these models are determined in equilibrium.

The striking result is the absence of aggregate effects of lumpy investment.

Motivation Discounting Discounting Plant-Level Optimization Results

Previous research

Research of Thomas (2002), Khan and Thomas (2003), and Khan and Thomas (2008) concludes that non-convexities at the plant level are not important for aggregate investment. State dependent interest rates in these models are determined in equilibrium.

The striking result is the absence of aggregate effects of lumpy investment.

Motivation Discounting Discounting Plant-Level Optimization Results

Previous research

Research of Thomas (2002), Khan and Thomas (2003), and Khan and Thomas (2008) concludes that non-convexities at the plant level are not important for aggregate investment. State dependent interest rates in these models are determined in equilibrium.

The striking result is the absence of aggregate effects of lumpy investment.

Motivation Discounting Discounting Plant-Level Optimization Results

Previous research

Research of Thomas (2002), Khan and Thomas (2003), and Khan and Thomas (2008) concludes that non-convexities at the plant level are not important for aggregate investment. State dependent interest rates in these models are determined in equilibrium.

The striking result is the absence of aggregate effects of lumpy investment.

Motivation Discounting Discounting Plant-Level Optimization Results

Our focus

In studying the investment decisions of establishments, what interest rate process are they responding to?

Our focus is studying the effects of interest rate movements found in the data.

Motivation Discounting Discounting Plant-Level Optimization Results

Our focus

In studying the investment decisions of establishments, what interest rate process are they responding to?

Our focus is studying the effects of interest rate movements found in the data.

Motivation Discounting Discounting Plant-Level Optimization Results

Our focus

In studying the investment decisions of establishments, what interest rate process are they responding to?

Our focus is studying the effects of interest rate movements found in the data.

Motivation Discounting Discounting Plant-Level Optimization Results

Key theme: Specifying an interest rate process

Why distinguish data-based interest rate process from model-based interest rate process?

Table: Interest rate properties

Std. dev. relative Correlation to output with output

Data .444 -.385

Benchmark (RBC) .096 .889

State-dependent adjustment .095 .892

Motivation Discounting Discounting Plant-Level Optimization Results

Roadmap for presentation

1 Model with non-convex adjustment costs for investment 2 Specify interest rate process (state dependent discount factor) 3 Specify aggregate process: detrending specification has strong

Motivation Discounting Discounting Plant-Level Optimization Results

Results

Plant-level moments used to estimate parameters in PE studies are insensitive to interest rate process

Specification of interest rate process strongly influences plant-level and aggregate investment response to shocks Specification of aggregate shock process strongly influences the responsiveness of investment to aggregate shock Observed extensive margin of investment behavior supports data-based interest rate process

Motivation Discounting Discounting Plant-Level Optimization Results

Results

Plant-level moments used to estimate parameters in PE studies are insensitive to interest rate process

Specification of interest rate process strongly influences plant-level and aggregate investment response to shocks

Specification of aggregate shock process strongly influences the responsiveness of investment to aggregate shock Observed extensive margin of investment behavior supports data-based interest rate process

Motivation Discounting Discounting Plant-Level Optimization Results

Results

Plant-level moments used to estimate parameters in PE studies are insensitive to interest rate process

Specification of interest rate process strongly influences plant-level and aggregate investment response to shocks Specification of aggregate shock process strongly influences the responsiveness of investment to aggregate shock

Observed extensive margin of investment behavior supports data-based interest rate process

Motivation Discounting Discounting Plant-Level Optimization Results

Results

Plant-level moments used to estimate parameters in PE studies are insensitive to interest rate process

Specification of interest rate process strongly influences plant-level and aggregate investment response to shocks Specification of aggregate shock process strongly influences the responsiveness of investment to aggregate shock Observed extensive margin of investment behavior supports data-based interest rate process

Motivation Discounting Discounting Plant-Level Optimization Results

Results

Plant-level moments used to estimate parameters in PE studies are insensitive to interest rate process

Specification of interest rate process strongly influences plant-level and aggregate investment response to shocks Specification of aggregate shock process strongly influences the responsiveness of investment to aggregate shock Observed extensive margin of investment behavior supports data-based interest rate process

Motivation Discounting Discounting Plant-Level Optimization Results

Results

Plant-level moments used to estimate parameters in PE studies are insensitive to interest rate process

Specification of interest rate process strongly influences plant-level and aggregate investment response to shocks Specification of aggregate shock process strongly influences the responsiveness of investment to aggregate shock Observed extensive margin of investment behavior supports data-based interest rate process

Motivation Discounting Discounting Plant-Level Optimization Results

Our Approach

1 Decentralized solution for establishment’s problem with empirically consistent

State dependent discounting

Adjustment costs for investment

Heterogeneity in productivity

Monopolistic competition

Use equilibrium prices instead of planner’s problem

2 To study:

Smoothing effects of state-dependent discounting

Effects of variation in the interest rate on plant-level and

Motivation Discounting Discounting Plant-Level Optimization Results

Our Approach

1 Decentralized solution for establishment’s problem with empirically consistent

State dependent discounting

Adjustment costs for investment

Heterogeneity in productivity

Monopolistic competition

Use equilibrium prices instead of planner’s problem

2 To study:

Smoothing effects of state-dependent discounting

Effects of variation in the interest rate on plant-level and

Motivation Discounting Discounting Plant-Level Optimization Results

State-Dependent Discount Factor (SDDF)

Household optimization for any asset j: Et h

˜

βt+1Rtj+1

i

= 1

Asset pricing kernel: ˜βt+1= βU

0(C t+1)

U0(C t)

Establishment-level problem (stationary):

V(A, ε,k,Z) = max

k0

π(A, ε,k)−C(A, ε,k,k0) +

EA0,Z0,ε0|A,Z,ε[ ˜β(·)V(A0, ε0,k0,Z0)] o

Monetary Policy targets RtM+1 conditional onZt andZt+1

Impacts Euler Equation

Motivation Discounting Discounting Plant-Level Optimization Results

State-Dependent Discount Factor (SDDF)

Household optimization for any asset j: Et h

˜

βt+1Rtj+1

i

= 1 Asset pricing kernel: ˜βt+1= βU

0(C t+1)

U0(C t)

Establishment-level problem (stationary):

V(A, ε,k,Z) = max

k0

π(A, ε,k)−C(A, ε,k,k0) +

EA0,Z0,ε0|A,Z,ε[ ˜β(·)V(A0, ε0,k0,Z0)] o

Monetary Policy targets RtM+1 conditional onZt andZt+1

Impacts Euler Equation

Motivation Discounting Discounting Plant-Level Optimization Results

State-Dependent Discount Factor (SDDF)

Household optimization for any asset j: Et h

˜

βt+1Rtj+1

i

= 1 Asset pricing kernel: ˜βt+1= βU

0(C t+1)

U0(C t)

Establishment-level problem (stationary):

V(A, ε,k,Z) = max

k0

π(A, ε,k)−C(A, ε,k,k0) +

EA0,Z0,ε0|A,Z,ε[ ˜β(·)V(A0, ε0,k0,Z0)] o

Monetary Policy targets RtM+1 conditional onZt andZt+1

Impacts Euler Equation

Motivation Discounting Discounting Plant-Level Optimization Results

State-Dependent Discount Factor (SDDF)

Household optimization for any asset j: Et h

˜

βt+1Rtj+1

i

= 1 Asset pricing kernel: ˜βt+1= βU

0(C t+1)

U0(C t)

Establishment-level problem (stationary):

V(A, ε,k,Z) = max

k0

π(A, ε,k)−C(A, ε,k,k0) +

EA0,Z0,ε0|A,Z,ε[ ˜β(·)V(A0, ε0,k0,Z0)] o

Monetary Policy targets RtM+1 conditional onZt andZt+1

Impacts Euler Equation

Motivation Discounting Discounting Plant-Level Optimization Results

Issues

Asset Pricing

Can we rely on the HH Euler equation to price assets, including investment and the federal funds market?

Canzoneri et al. (2007) find huge differences between money market rates and (parameterized) HH Euler equations. Is this the right channel for monetary policy?

What are the adjustment costs at the plant-level?

Cooper and Haltiwanger (2006)

Includes market power and heterogeneity

Check moment implications with state dependent discounting

Motivation Discounting Discounting Plant-Level Optimization Results

Issues

Asset Pricing

Can we rely on the HH Euler equation to price assets, including investment and the federal funds market?

Canzoneri et al. (2007) find huge differences between money market rates and (parameterized) HH Euler equations.

Is this the right channel for monetary policy?

What are the adjustment costs at the plant-level?

Cooper and Haltiwanger (2006)

Includes market power and heterogeneity

Check moment implications with state dependent discounting

Motivation Discounting Discounting Plant-Level Optimization Results

Issues

Asset Pricing

Can we rely on the HH Euler equation to price assets, including investment and the federal funds market?

Canzoneri et al. (2007) find huge differences between money market rates and (parameterized) HH Euler equations. Is this the right channel for monetary policy?

What are the adjustment costs at the plant-level?

Cooper and Haltiwanger (2006)

Includes market power and heterogeneity

Check moment implications with state dependent discounting

Motivation Discounting Discounting Plant-Level Optimization Results

Issues

Asset Pricing

Can we rely on the HH Euler equation to price assets, including investment and the federal funds market?

Canzoneri et al. (2007) find huge differences between money market rates and (parameterized) HH Euler equations. Is this the right channel for monetary policy?

What are the adjustment costs at the plant-level?

Cooper and Haltiwanger (2006)

Includes market power and heterogeneity

Check moment implications with state dependent discounting

Motivation Discounting Discounting Plant-Level Optimization Results

Issues

Asset Pricing

Can we rely on the HH Euler equation to price assets, including investment and the federal funds market?

Canzoneri et al. (2007) find huge differences between money market rates and (parameterized) HH Euler equations. Is this the right channel for monetary policy?

What are the adjustment costs at the plant-level?

Cooper and Haltiwanger (2006)

Includes market power and heterogeneity

Check moment implications with state dependent discounting

Motivation Discounting Discounting Plant-Level Optimization Results

What interest rate should be used to discount plant level profits?

1 Model Based:

Interest rate derived from general equilibrium model (Thomas

(2002), Khan and Thomas (2003), and others)

Mapping from states to interest rates determined within model

2 Data Based:

Estimate functional relationship between Euler-equation-based

discount rate and aggregate state variables

Coefficients from data not model

3 Estimate state-dependent market rates directly

Motivation Discounting Discounting Plant-Level Optimization Results

What interest rate should be used to discount plant level profits?

1 Model Based:

Interest rate derived from general equilibrium model (Thomas

(2002), Khan and Thomas (2003), and others)

Mapping from states to interest rates determined within model

2 Data Based:

Estimate functional relationship between Euler-equation-based

discount rate and aggregate state variables

Coefficients from data not model

3 Estimate state-dependent market rates directly

Motivation Discounting Discounting Plant-Level Optimization Results

What interest rate should be used to discount plant level profits?

1 Model Based:

Interest rate derived from general equilibrium model (Thomas

(2002), Khan and Thomas (2003), and others)

Mapping from states to interest rates determined within model

2 Data Based:

Estimate functional relationship between Euler-equation-based

discount rate and aggregate state variables

Coefficients from data not model

3 Estimate state-dependent market rates directly

Motivation Discounting Discounting Plant-Level Optimization Results

What interest rate should be used to discount plant level profits?

1 Model Based:

Interest rate derived from general equilibrium model (Thomas

(2002), Khan and Thomas (2003), and others)

Mapping from states to interest rates determined within model

2 Data Based:

Estimate functional relationship between Euler-equation-based

discount rate and aggregate state variables

Coefficients from data not model

3 Estimate state-dependent market rates directly

Motivation Discounting Discounting Plant-Level Optimization Results

Finding the pricing kernel: ˜

β

=

B

(

·

)

Use the Data

1 Calculate ˜βt+1=βU

0(C t+1) U0(C

t) from data

2 SpecifyB(·)

3 Estimate it from aggregate data

Use a Model

1 Stochastic Growth Model with Monopolistic Competition (eg.

Chatterjee and Cooper (1993))

2 Ct=C(At,Kt),Kt+1=K(At,Kt) , ˜βt+1= βU

0(C t+1) U0(Ct)

3 (A,K) are aggregate state variables

4 Solve model and obtain evolution of states and controls to

Motivation Discounting Discounting Plant-Level Optimization Results

Finding the pricing kernel: ˜

β

=

B

(

·

)

Use the Data

1 Calculate ˜βt+1=βU

0(C t+1) U0(C

t) from data

2 SpecifyB(·)

3 Estimate it from aggregate data

Use a Model

1 Stochastic Growth Model with Monopolistic Competition (eg.

Chatterjee and Cooper (1993))

2 Ct=C(At,Kt),Kt+1=K(At,Kt) , ˜βt+1= βU

0(C t+1) U0(Ct)

3 (A,K) are aggregate state variables

4 Solve model and obtain evolution of states and controls to

Motivation Discounting Discounting Plant-Level Optimization Results

Estimating

B

(

A

t,

A

t+1,

K

t)

Data: follow Stock and Watson (1999)

Consumption = Nondurables + Services (BEA)

Output = Real Business Nonfarm GDP (BEA)

Labor = Private nonfarm payroll employment (BLS)

Capital = Real private nonresidential fixed capital stock (BEA)

log(A) = log(Output) - 0.65*log(Labor) - 0.35*log(Capital)

Details:

Annual data from 1948 - 2008

Motivation Discounting Discounting Plant-Level Optimization Results

Estimating

B

(

A

t,

A

t+1,

K

t)

Data: follow Stock and Watson (1999)

Consumption = Nondurables + Services (BEA)

Output = Real Business Nonfarm GDP (BEA)

Labor = Private nonfarm payroll employment (BLS)

Capital = Real private nonresidential fixed capital stock (BEA)

log(A) = log(Output) - 0.65*log(Labor) - 0.35*log(Capital)

Details:

Annual data from 1948 - 2008

Motivation Discounting Discounting Plant-Level Optimization Results

Estimating

B

(

A

t,

A

t+1,

K

t)

1 Construct ˜βt+1= βU

0(C t+1)

U0(C

t) using U(C) =log(C) and β = 0.96

2 Regress ˜βt+1 on{At,At+1,Kt}

Motivation Discounting Discounting Plant-Level Optimization Results

Side Note: Filtering the data

1940 1950 1960 1970 1980 1990 2000 2010

−1 −0.9 −0.8 −0.7 −0.6 −0.5 −0.4 −0.3 −0.2 −0.1 0 Solow residual log level

1940 1950 1960 1970 1980 1990 2000 2010

−0.1 −0.08 −0.06 −0.04 −0.02 0 0.02 0.04 0.06 0.08 0.1

Filtered Solow residual

log deviation from trend

! = 0.84

Motivation Discounting Discounting Plant-Level Optimization Results

Side Note: Filtering the data

−11940 1950 1960 1970 1980 1990 2000 2010−0.9 −0.8 −0.7 −0.6 −0.5 −0.4 −0.3 −0.2 −0.1 0 Solow residual log level

1940 1950 1960 1970 1980 1990 2000 2010

−0.1 −0.08 −0.06 −0.04 −0.02 0 0.02 0.04 0.06 0.08 0.1

Filtered Solow residual

log deviation from trend

! = 0.84

Motivation Discounting Discounting Plant-Level Optimization Results

Side Note: Filtering the data

1940 1950 1960 1970 1980 1990 2000 2010

−0.1 −0.08 −0.06 −0.04 −0.02 0 0.02 0.04 0.06 0.08 0.1

Filtered Solow residuals

log deviation from trend

! = 0.84

! = 0.14

Linear filter ("=100000) Band Pass filter (" = 7)

1940 1950 1960 1970 1980 1990 2000 2010

−0.15 −0.1 −0.05 0 0.05 0.1 0.15

Filtered Solow residual

log deviation from trend

Motivation Discounting Discounting Plant-Level Optimization Results

Pricing kernel (SDDF): ˜

β

=

B

(

A

t,

A

t+1,

K

t)

Source At At+1 Kt R2 dEtdA[ ˜βt(·)]

Case 1 Data 0.34 -0.46 0.01 0.56 -0.04

λ= 100000 (0.05) (0.06) (0.03)

(ρA = 0.84) Chat-Coop 0.43 -0.64 0.09 NA -0.11

KPR 0.37 -0.59 0.09 NA -0.12

Motivation Discounting Discounting Plant-Level Optimization Results

Pricing kernel (SDDF): ˜

β

=

B

(

A

t,

A

t+1,

K

t)

Source At At+1 Kt R2 dEtdA[ ˜βt(·)]

Case 1 Data 0.34 -0.46 0.01 0.56 -0.04

λ= 100000 (0.05) (0.06) (0.03)

(ρA = 0.84) Chat-Coop 0.43 -0.64 0.09 NA -0.11

KPR 0.37 -0.59 0.09 NA -0.12

Motivation Discounting Discounting Plant-Level Optimization Results

Pricing kernel (SDDF): ˜

β

=

B

(

A

t,

A

t+1,

K

t)

Source At At+1 Kt R2 dEtdA[ ˜βt(·)]

Case 1 Data 0.34 -0.46 0.01 0.56 -0.04

λ= 100000 (0.05) (0.06) (0.03)

(ρA = 0.84) Chat-Coop 0.43 -0.64 0.09 NA -0.11

KPR 0.37 -0.59 0.09 NA -0.12

Motivation Discounting Discounting Plant-Level Optimization Results

Pricing kernel (SDDF): ˜

β

=

B

(

A

t,

A

t+1,

K

t)

Source At At+1 Kt R2 dEtdA[ ˜βt(·)]

Case 1 Data 0.34 -0.46 0.01 0.56 -0.04

λ= 100000 (0.05) (0.06) (0.03)

(ρA = 0.84) Chat-Coop 0.43 -0.64 0.09 NA -0.11

KPR 0.37 -0.59 0.09 NA -0.12

Motivation Discounting Discounting Plant-Level Optimization Results

Pricing kernel (SDDF): ˜

β

=

B

(

A

t,

A

t+1,

K

t)

Source At At+1 Kt R2 dEtdA[ ˜βt(·)]

Case 3 Data 0.20 -0.59 0.06 0.46 0.12

λ= 7 (0.09) (0.10) (0.15)

(ρA = 0.14) Chat-Coop 0.09 -0.41 0.09 NA 0.03

KPR 0.08 -0.39 0.09 NA 0.03

Motivation Discounting Discounting Plant-Level Optimization Results

Pricing kernel (SDDF): ˜

β

=

B

(

A

t,

A

t+1,

K

t)

Source At At+1 Kt R2 dEtdA[ ˜βt(·)]

Case 3 Data 0.20 -0.59 0.06 0.46 0.12

λ= 7 (0.09) (0.10) (0.15)

(ρA = 0.14) Chat-Coop 0.09 -0.41 0.09 NA 0.03

KPR 0.08 -0.39 0.09 NA 0.03

Motivation Discounting Discounting Plant-Level Optimization Results

State-Dependent Discount Factor (SDDF)

−40 5 10 15 20 25 30 35 40 45 50 −20 2 4

Aggregate shock and expected discount factor (E[!]) when "A = 0.14

periods (years)

percentage log deviation from steady state

0 5 10 15 20 25 30 35 40 45 50−0.4

−0.2 0 0.2 0.4

percentage log deviation from steady state

Aggregate profitability shock (left axis) Empirical discount factor (right axis) Chat−Coop discount factor (right axis)

0 5 10 15 20 25 30 35 40 45 50

−6 −4 −2 0 2 4 6

Aggregate shock and expected discount factor (E[!]) when "A = 0.84

periods (years)

percentage log deviation from steady state

0 5 10 15 20 25 30 35 40 45 50−0.6

−0.4 −0.2 0 0.2 0.4 0.6

percentage log deviation from steady state

Motivation Discounting Discounting Plant-Level Optimization Results

Stochastic Discount Factor

0 5 10 15 20 25 30 35 40 45 50

−4

−2 0 2 4

Aggregate shock and expected discount factor (E[!]) when "A = 0.14

periods (years)

percentage log deviation from steady state

0 5 10 15 20 25 30 35 40 45 50−0.4

−0.2 0 0.2 0.4

percentage log deviation from steady state

Aggregate profitability shock (left axis) Empirical discount factor (right axis) Chat−Coop discount factor (right axis)

0 5 10 15 20 25 30 35 40 45 50

−6 −4 −2 0 2 4 6

Aggregate shock and expected discount factor (E[!]) when "A = 0.84

periods (years)

percentage log deviation from steady state

0 5 10 15 20 25 30 35 40 45 50−0.6

−0.4 −0.2 0 0.2 0.4 0.6

percentage log deviation from steady state

Motivation Discounting Discounting Plant-Level Optimization Results

Experiments

Questions

1 What are the effects of interest rates on aggregate and plant-level investment?

2 Is there smoothing of nonconvexities through state-dependent discounting?

Study by comparing outcomes

Motivation Discounting Discounting Plant-Level Optimization Results

Experiments

Questions

1 What are the effects of interest rates on aggregate and plant-level investment?

2 Is there smoothing of nonconvexities through state-dependent discounting?

Study by comparing outcomes

Motivation Discounting Discounting Plant-Level Optimization Results

Plant-Level Optimization Problem

V(A, ,k) = max{Vi(A, ε,k),Va(A, ε,k)}, ∀(A, ε,k),

where

Vi(A, ε,k) = Π(A, ε,k) +EA0,ε0|A,ε

h

˜

βV(A0, ε0,k(1−δ))i

Va(A, ε,k) = max

k0 Π(A, ε

0,k)−C(A, ε,k,k0) +

EA0,ε0|A,ε

h

˜

βV(A0, ε0,k0)i

where

C(A, ε,k,k0) =

disruption cost

z }| {

(1−λ) Π(A, ε0,k) +pb(I>0)(k0−(1−δ)k)

−ps(I<0)((1−δ)k−k0)

| {z }

irreversibility

+ν 2

k0−(1−δ)k k

2 k

| {z }

Motivation Discounting Discounting Plant-Level Optimization Results

Cooper and Haltiwanger (2006)

Three forms of investment adjustment costs:

disruption cost (λ)

quadratic adjustment cost (ν)

irreversibility (ps)

Estimate {λ, ν,ps} via SMM

Motivation Discounting Discounting Plant-Level Optimization Results

Parameters:

From CH (2006)

λ= 0.8

ν = 0.15

ps =0.98 ρε = 0.88

σε = 0.1

Constant returns to scale

θ = 5

Motivation Discounting Discounting Plant-Level Optimization Results

State Dependent Discounting and Plant-Level Investment

Plant-level moments used in CH (2006) estimation are insensitive to ˜β

Table: Plant-level moments

Model Corr(i,i−1) Corr(i, ε) Spike + Spike

-β -0.13 0.19 0.13 0

˜

Motivation Discounting Discounting Plant-Level Optimization Results

Plant-level investment regression on simulated data:

I

i(

A

, ε

i,

K

i)

Model ρA A εi Ki R2

β 0.14 -12.78 28.47 -0.46 0.36

(3.22) (0.26) (0.00)

0.84 23.59 29.82 -0.43 0.36

(1.37) (0.27) (0.00)

˜

β(At,At+1) 0.14 24.58 28.40 -0.46 0.36

(Empirical) (3.22) (0.26) (0.00)

0.84 13.76 29.74 -0.43 0.36

(1.37) (0.27) (0.00)

˜

β(At,At+1) 0.14 -1.97 28.63 -0.46 0.36

(Chat-Coop) (3.21) (0.26) (0.00)

0.84 -6.48 30.20 -0.44 0.36

Motivation Discounting Discounting Plant-Level Optimization Results

Intensive margin

Table:Plant-level investment regression (Adjusters only):Ii(A, εi,Ki)

Model ρA A εi Ki R2

β 0.14 4.54 25.54 0.02 0.90

(2.57) (0.45) (0.01)

0.84 26.11 29.58 0.02 0.98

(0.56) (0.23) (0.01) ˜

β(At,At+1) 0.14 17.11 24.60 0.04 0.90

(Empirical) (2.59) (0.45) (0.01)

0.84 18.42 29.61 0.03 0.98

(0.50) (0.21) (0.00) ˜

β(At,At+1) 0.14 5.28 25.25 0.03 0.90

(Chat-Coop) (2.51) (0.44) (0.01)

0.84 2.80 29.67 0.03 0.99

Motivation Discounting Discounting Plant-Level Optimization Results

Extensive margin

Table:Linear probability regression using plant-level simulated data (extensive

margin)

Model ρA A εi Ki R2

β 0.14 -0.67 1.25 -0.84 0.37

(0.15) (0.01) (0.01)

0.84 1.00 1.26 -0.81 0.37

(0.06) (0.01) (0.01) ˜

β(At,At+1) 0.14 1.17 1.25 -0.84 0.37

(Empirical) (0.15) (0.01) (0.01)

0.84 0.58 1.24 -0.79 0.37

(0.06) (0.01) (0.01) ˜

β(At,At+1) 0.14 -0.11 1.26 -0.85 0.37

(Chat-Coop) (0.15) (0.01) (0.01)

0.84 -0.33 1.27 -0.81 0.37

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate Investment

0 5 10 15 20 25 30

−0.03 −0.02 −0.01 0 0.01 0.02 0.03 0.04 periods (years)

deviation from mean

Aggregate shock and aggregate investment rate (I/K) when !A = 0.14

0 5 10 15 20 25 30−0.03

−0.02 −0.01 0 0.01 0.02 0.03 0.04

deviation from mean

Aggregate profitability shock (left axis) Investment rate (fixed ") (right axis)

0 5 10 15 20 25 30

−0.06 −0.03 0 0.03 0.06 0.09

Aggregate shock and aggregate investment rate (I/K) when !A = 0.84

periods (years)

deviation from mean

0 5 10 15 20 25 30−0.04

−0.02 0 0.02 0.04 0.06

deviation from mean

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate Investment

0 5 10 15 20 25 30

−0.03 −0.02 −0.01 0 0.01 0.02 0.03 0.04 periods (years)

deviation from mean

Aggregate shock and aggregate investment rate (I/K) when !A = 0.14

0 5 10 15 20 25 30−0.03

−0.02 −0.01 0 0.01 0.02 0.03 0.04

deviation from mean

Aggregate profitability shock (left axis)

Investment rate (fixed ") (right axis)

Investment (empirical) (right axis)

0 5 10 15 20 25 30

−0.06 −0.03 0 0.03 0.06 0.09

Aggregate shock and aggregate investment rate (I/K) when !A = 0.84

periods (years)

deviation from mean

0 5 10 15 20 25 30−0.04

−0.02 0 0.02 0.04 0.06

deviation from mean

Aggregate profitability shock (left axis)

Investment rate (fixed ") (right axis)

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate Investment

0 5 10 15 20 25 30

−0.03 −0.02 −0.01 0 0.01 0.02 0.03 0.04 periods (years)

deviation from mean

Aggregate shock and aggregate investment rate (I/K) when !A = 0.14

0 5 10 15 20 25 30−0.03

−0.02 −0.01 0 0.01 0.02 0.03 0.04

deviation from mean

Aggregate profitability shock (left axis)

Investment rate (fixed ") (right axis)

Investment (empirical) (right axis)

Investment (Chat−Coop) (right axis)

0 5 10 15 20 25 30

−0.06 −0.03 0 0.03 0.06 0.09

Aggregate shock and aggregate investment rate (I/K) when !A = 0.84

periods (years)

deviation from mean

0 5 10 15 20 25 30−0.04

−0.02

0 0.02 0.04 0.06

deviation from mean

Aggregate profitability shock (left axis)

Investment rate (fixed ") (right axis)

Investment (empirical) (right axis)

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate Investment

0 5 10 15 20 25 30

−0.03 −0.02 −0.01 0 0.01 0.02 0.03 0.04 periods (years)

deviation from mean

Aggregate shock and aggregate investment rate (I/K) when !A = 0.14

0 5 10 15 20 25 30−0.03

−0.02 −0.01 0 0.01 0.02 0.03 0.04

deviation from mean

Aggregate profitability shock (left axis) Investment rate (fixed ") (right axis)

0 5 10 15 20 25 30

−0.06 −0.03 0 0.03 0.06 0.09

Aggregate shock and aggregate investment rate (I/K) when !A = 0.84

periods (years)

deviation from mean

0 5 10 15 20 25 30−0.04

−0.02

0 0.02 0.04 0.06

deviation from mean

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate Investment

0 5 10 15 20 25 30

−0.03 −0.02 −0.01 0 0.01 0.02 0.03 0.04 periods (years)

deviation from mean

Aggregate shock and aggregate investment rate (I/K) when !A = 0.14

0 5 10 15 20 25 30−0.03

−0.02 −0.01 0 0.01 0.02 0.03 0.04

deviation from mean

Aggregate profitability shock (left axis) Investment rate (fixed ") (right axis) Investment (empirical) (right axis)

0 5 10 15 20 25 30

−0.06 −0.03 0 0.03 0.06 0.09

Aggregate shock and aggregate investment rate (I/K) when !A = 0.84

periods (years)

deviation from mean

0 5 10 15 20 25 30−0.04

−0.02 0 0.02 0.04 0.06

deviation from mean

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate Investment

0 5 10 15 20 25 30

−0.03 −0.02 −0.01 0 0.01 0.02 0.03 0.04 periods (years)

deviation from mean

Aggregate shock and aggregate investment rate (I/K) when !A = 0.14

0 5 10 15 20 25 30−0.03

−0.02 −0.01 0 0.01 0.02 0.03 0.04

deviation from mean

Aggregate profitability shock (left axis)

Investment rate (fixed ") (right axis)

Investment (empirical) (right axis)

Investment (Chat−Coop) (right axis)

0 5 10 15 20 25 30

−0.06 −0.03 0 0.03 0.06 0.09

Aggregate shock and aggregate investment rate (I/K) when !A = 0.84

periods (years)

deviation from mean

0 5 10 15 20 25 30−0.04

−0.02 0 0.02 0.04 0.06

deviation from mean

Aggregate profitability shock (left axis)

Investment rate (fixed ") (right axis)

Investment (empirical) (right axis)

Motivation Discounting Discounting Plant-Level Optimization Results

Correlation of aggregates with aggregate shock (A)

Extensive Margin Intensive Margin

Model ρA I K KI Fraction of adjusters mean(Ii Ki|

Ii Ki>0.2)

Data 0.14 0.08 -0.02 0.12 0.14 NA

0.84 0.05 -0.36 0.23 0.19 NA

β 0.14 -0.51 0.03 -0.50 -0.55 0.61

0.84 0.55 0.73 0.43 0.46 0.09

˜

β(At,At+1) 0.14 0.61 0.15 0.58 0.62 0.01

(Empirical) 0.84 0.47 0.69 0.36 0.36 0.47

˜

β(At,At+1) 0.14 -0.19 0.10 -0.20 -0.23 0.49

Motivation Discounting Discounting Plant-Level Optimization Results

Extensive margin

0 5 10 15 20 25 30 35 40 45 50

−0.04

−0.02 0 0.02 0.04

Extensive margin when ρA = 0.14

periods (years)

profitability shock

0 5 10 15 20 25 30 35 40 45 500.08

0.1 0.12 0.14 0.16

fraction of establishments with investment spike

Aggregate profitability shock (left axis) Spikes (empirical specification) Spikes (Chat−Coop specification)

0 5 10 15 20 25 30 35 40 45 50

−0.06

−0.03 0 0.03 0.06

Extensive margin when ρA = 0.84

periods (years)

profitability shock

0 5 10 15 20 25 30 35 40 45 500.08

0.1 0.12 0.14 0.16

fraction of establishments with investment spike

Motivation Discounting Discounting Plant-Level Optimization Results

Extensive margin

0 5 10 15 20 25 30 35 40 45 50

−0.04 −0.02 0 0.02 0.04

Extensive margin when ρA = 0.14

periods (years)

profitability shock

0 5 10 15 20 25 30 35 40 45 500.08

0.1 0.12 0.14 0.16

fraction of establishments with investment spike

Aggregate profitability shock (left axis) Spikes (empirical specification) Spikes (Chat−Coop specification)

0 5 10 15 20 25 30 35 40 45 50

−0.06 −0.03 0 0.03 0.06

Extensive margin when ρA = 0.84

periods (years)

profitability shock

0 5 10 15 20 25 30 35 40 45 500.08

0.1 0.12 0.14 0.16

fraction of establishments with investment spike

Motivation Discounting Discounting Plant-Level Optimization Results

Aggregate capital regression:

K

t+1=

K

(

A

t,

K

t)

Model ρA At Kt R2

Data 0.14 0.23 0.23 0.16

(0.08) (0.12)

0.84 0.13 0.98 0.90

(0.06) (0.05)

β 0.14 -0.33 0.71 0.64

(0.02) (0.03)

0.84 0.63 0.50 0.96

(0.02) (0.01) ˜

β(At,At+1) 0.14 0.60 0.58 0.72

(Empirical) (0.03) (0.02)

0.84 0.35 0.59 0.90

(0.02) (0.02) ˜

β(At,At+1) 0.14 -0.10 0.78 0.60

(Chat-Coop) (0.02) (0.03)

0.84 -0.09 0.74 0.66

Motivation Discounting Discounting Plant-Level Optimization Results

Do Adjustment Costs Matter for Aggregate Investment in

Model with State-Dependent Discounting?

Table:Kt+1=K(At,Kt) from model using data-based SDDF (empirical)

Model ρA At Kt R2

Non-Convex AC 0.14 0.60 0.58 0.72

(0.03) (0.02)

0.84 0.35 0.59 0.90

(0.02) (0.02)

No AC 0.14 0.08 3.11 0.90

(0.01) (0.05)

0.84 0.18 1.20 0.91

Motivation Discounting Discounting Plant-Level Optimization Results

Do Adjustment Costs Matter for Aggregate Investment in

Model with State-Dependent Discounting?

Table:Kt+1=K(At,Kt) from model using data-based SDDF (empirical)

Model ρA At Kt R2

Non-Convex AC 0.14 0.60 0.58 0.72

(0.03) (0.02)

0.84 0.35 0.59 0.90

(0.02) (0.02)

No AC 0.14 0.08 3.11 0.90

(0.01) (0.05)

0.84 0.18 1.20 0.91

Motivation Discounting Discounting Plant-Level Optimization Results

Do Adjustment Costs Matter for Aggregate Investment in

Model with State-Dependent Discounting?

Table:Kt+1=K(At,Kt) from model using data-based SDDF (empirical)

Model ρA At Kt R2

Non-Convex AC 0.14 0.60 0.58 0.72

(0.03) (0.02)

0.84 0.35 0.59 0.90

(0.02) (0.02)

No AC 0.14 0.08 3.11 0.90

(0.01) (0.05)

0.84 0.18 1.20 0.91

Motivation Discounting Discounting Plant-Level Optimization Results

Adjustment Costs Matter for Aggregate Investment in

Model with State-Dependent Discounting

Table:Kt+1=K(At,Kt) from model using model-based SDDF (Chat-Coop)

Model ρA At Kt R2

Non-Convex AC 0.14 -0.10 0.78 0.60

(0.02) (0.03)

0.84 -0.09 0.74 0.66

(0.01) (0.03)

No AC 0.14 0.40 1.03 0.68

(0.03) (0.04)

0.84 0.73 0.03 0.54

Motivation Discounting Discounting Plant-Level Optimization Results

What have we learned?

Estimated ˜β process from data is qualitatively similar to model prediction, but small differences in the ˜β specification have large implications for investment behavior

Model-based SDDF contributes strongly to investment smoothing, data-based SDDF does not

Data on extensive margin of plant-level investment behavior show that model-based results overstate role of investment smoothing

Responsiveness of investment to aggregate shocks is affected by specification of aggregate shock process

Motivation Discounting Discounting Plant-Level Optimization Results

What have we learned?

Estimated ˜β process from data is qualitatively similar to model prediction, but small differences in the ˜β specification have large implications for investment behavior

Model-based SDDF contributes strongly to investment smoothing, data-based SDDF does not

Data on extensive margin of plant-level investment behavior show that model-based results overstate role of investment smoothing

Responsiveness of investment to aggregate shocks is affected by specification of aggregate shock process

Motivation Discounting Discounting Plant-Level Optimization Results

What have we learned?

Estimated ˜β process from data is qualitatively similar to model prediction, but small differences in the ˜β specification have large implications for investment behavior

Model-based SDDF contributes strongly to investment smoothing, data-based SDDF does not

Data on extensive margin of plant-level investment behavior show that model-based results overstate role of investment smoothing

Responsiveness of investment to aggregate shocks is affected by specification of aggregate shock process

Motivation Discounting Discounting Plant-Level Optimization Results

What have we learned?

Estimated ˜β process from data is qualitatively similar to model prediction, but small differences in the ˜β specification have large implications for investment behavior

Model-based SDDF contributes strongly to investment smoothing, data-based SDDF does not

Data on extensive margin of plant-level investment behavior show that model-based results overstate role of investment smoothing

Responsiveness of investment to aggregate shocks is affected by specification of aggregate shock process

Motivation Discounting Discounting Plant-Level Optimization Results

What have we learned?

Estimated ˜β process from data is qualitatively similar to model prediction, but small differences in the ˜β specification have large implications for investment behavior

Model-based SDDF contributes strongly to investment smoothing, data-based SDDF does not

Data on extensive margin of plant-level investment behavior show that model-based results overstate role of investment smoothing

Responsiveness of investment to aggregate shocks is affected by specification of aggregate shock process

Motivation Discounting Discounting Plant-Level Optimization Results

Next steps

Study response of investment to monetary policy

How are changes in monetary policy reflected in changes in the

state-dependent discount factor?

Et h

˜

βt+1R j t+1

i

= 1

Specify a Taylor-type rule for the real interest rate

rtf =α+αAAt+αKKt+ρrtf−1+εft

Motivation Discounting Discounting Plant-Level Optimization Results

Next steps

Study response of investment to monetary policy

How are changes in monetary policy reflected in changes in the

state-dependent discount factor?

Et h

˜

βt+1R j t+1

i

= 1

Specify a Taylor-type rule for the real interest rate

rtf =α+αAAt+αKKt+ρrtf−1+εft

Motivation Discounting Discounting Plant-Level Optimization Results

Table: Parameter estimates for Solow-residual technology process

λ ρA σA

7 0.14 0.012

100 0.45 0.015

Motivation Discounting Discounting Plant-Level Optimization Results

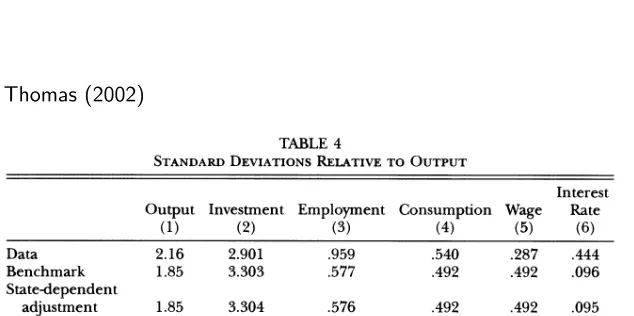

Differences from model-based predictions

Thomas (2002)

JOURNAL OF POLITICAL ECONOMY

TABLE 4

STANDARD DEVIATIONS RELATIVE TO OUTPUT

Output (1)

Investment

(2) Employment (3) Consumption (4) Wage (5) Interest

Rate (6)

Data 2.16 2.901 .959 .540 .287 .444

Benchmark 1.85 3.303 .577 .492 .492 .096

State-dependent

adjustment 1.85 3.304 .576 .492 .492 .095

Constant

adjustment 1.82 3.227 .556 .503 .503 .083

Partial adjustment 1.51 2.223 .305 .708 .708 .019

NOTE.-COI. 1 reports the percentage standard deviations for Hodrick-Prescott-filtered output in the data and the models. (Models are briefly summarized in table 3.) Cols. 2-6 are standard deviations relative to the standard deviation of output. In tables 4-7, the Hansen preference specification implies identical consumption and wage moments within each model economy.

what is perhaps more striking is that the inclusion of state-dependent lumpy investment patterns neither improves nor even affects model performance along any of these dimensions.

Table 4 reveals that the standard deviations for output, investment, employment, and consumption are essentially identical for the bench- mark and state-dependent adjustment economies. The similarities there extend to the constant adjustment model as well, which exhibits only somewhat reduced investment volatility. That closeness is further em- phasized by contrast to the traditional partial adjustment model, which exhibits a substantially weakened cycle because of excessively smooth investment demand. The overall similarity across models is also seen in the first- and second-order autocorrelations of table 6 and in the con- temporaneous and lagged correlations with output reported in tables 5 and 7. Consistent with its slightly reduced relative investment volatility, autocorrelations for the constant adjustment model's output, invest- ment, and employment series are somewhat higher, as are its investment and employment correlations with output.

The discussion above raises two questions. First, given that adjustment

TABLE 5

CONTEMPORANEOUS CORRELATIONS WITH OUTPUT

Investment

(1) Employment (2) Consumption (3) Wage

(4)

Interest Rate

(5)

Data .823 .903 .858 .263 -.385

Benchmark .973 .946 .924 .924 .889

State-dependent

adjustment .973 .946 .925 .925 .892

Constant adjustment .976 .950 .938 .938 .904

Partial adjustment .991 .971 .995 .995 .610

Motivation Discounting Discounting Plant-Level Optimization Results

Differences from model-based predictions

Thomas (2002)

JOURNAL OF POLITICAL ECONOMY

TABLE 4

STANDARD DEVIATIONS RELATIVE TO OUTPUT

Output (1)

Investment

(2) Employment (3) Consumption (4) Wage (5) Interest

Rate (6)

Data 2.16 2.901 .959 .540 .287 .444

Benchmark 1.85 3.303 .577 .492 .492 .096

State-dependent

adjustment 1.85 3.304 .576 .492 .492 .095

Constant

adjustment 1.82 3.227 .556 .503 .503 .083

Partial adjustment 1.51 2.223 .305 .708 .708 .019

NOTE.-COI. 1 reports the percentage standard deviations for Hodrick-Prescott-filtered output in the data and the models. (Models are briefly summarized in table 3.) Cols. 2-6 are standard deviations relative to the standard deviation of output. In tables 4-7, the Hansen preference specification implies identical consumption and wage moments within each model economy.

what is perhaps more striking is that the inclusion of state-dependent lumpy investment patterns neither improves nor even affects model performance along any of these dimensions.

Table 4 reveals that the standard deviations for output, investment, employment, and consumption are essentially identical for the bench- mark and state-dependent adjustment economies. The similarities there extend to the constant adjustment model as well, which exhibits only somewhat reduced investment volatility. That closeness is further em- phasized by contrast to the traditional partial adjustment model, which exhibits a substantially weakened cycle because of excessively smooth investment demand. The overall similarity across models is also seen in the first- and second-order autocorrelations of table 6 and in the con- temporaneous and lagged correlations with output reported in tables 5 and 7. Consistent with its slightly reduced relative investment volatility, autocorrelations for the constant adjustment model's output, invest- ment, and employment series are somewhat higher, as are its investment and employment correlations with output.

The discussion above raises two questions. First, given that adjustment

TABLE 5

CONTEMPORANEOUS CORRELATIONS WITH OUTPUT

Investment

(1) Employment (2) Consumption (3) Wage (4)

Interest Rate

(5)

Data .823 .903 .858 .263 -.385

Benchmark .973 .946 .924 .924 .889

State-dependent

adjustment .973 .946 .925 .925 .892

Constant adjustment .976 .950 .938 .938 .904

Partial adjustment .991 .971 .995 .995 .610

Motivation Discounting Discounting Plant-Level Optimization Results

Parameters:

From aggregate data (1948-2008)

ρA = 0.118 σA = 0.012

State-dependent discounting: ˆ

˜

βt+1 = 0.217ˆAt−0.507ˆAt+1

Motivation Discounting Discounting Plant-Level Optimization Results

Parameters:

From aggregate data (1948-2008)

ρA = 0.118 σA = 0.012

State-dependent discounting: ˆ

˜

βt+1 = 0.217ˆAt−0.507ˆAt+1