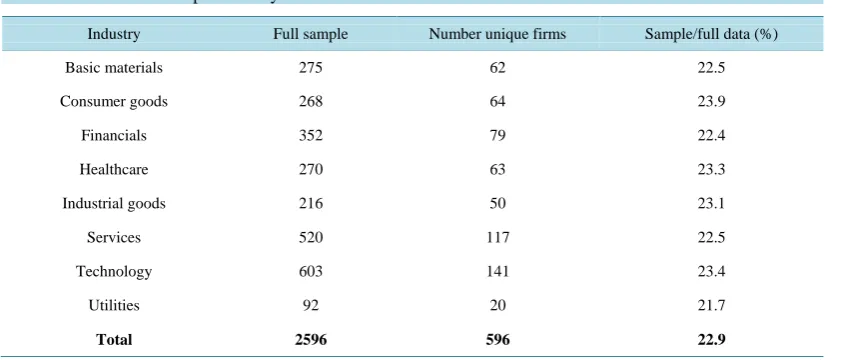

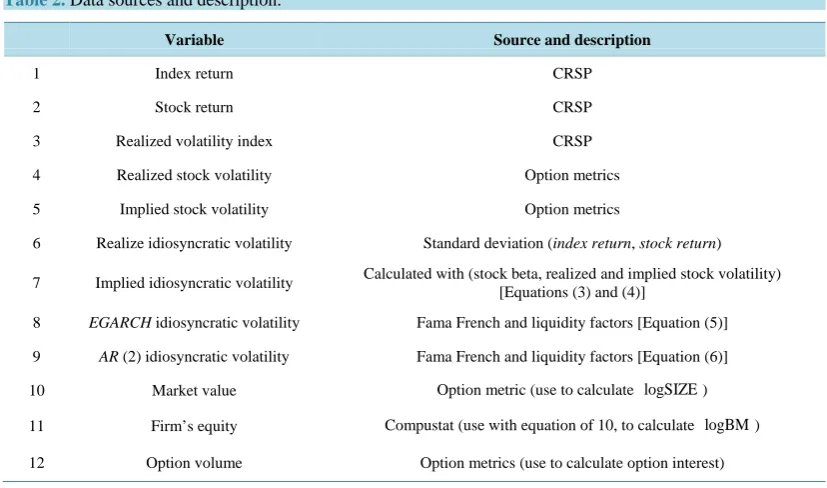

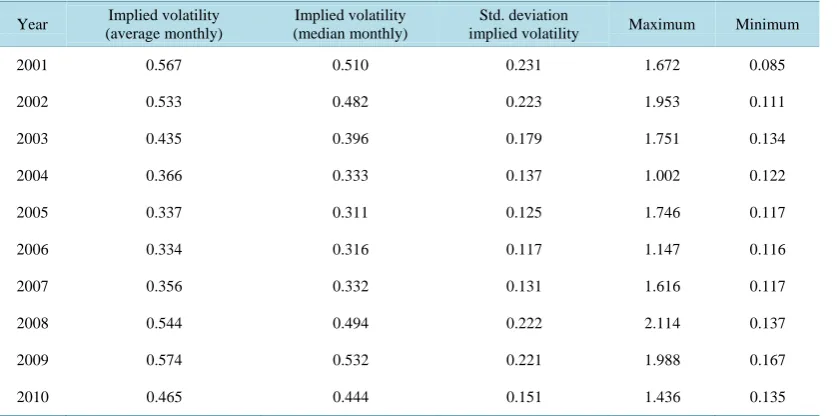

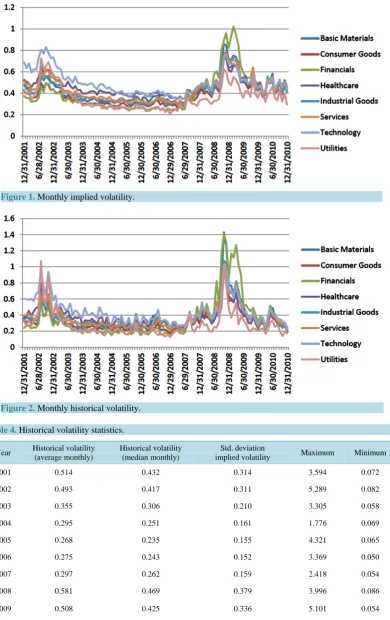

Implied Idiosyncratic Volatility and Stock Return Predictability

Full text

Figure

Related documents

This is shown in the study where key activities of CRM Implementation were grouped into five primary dimensions: acquisition management, contact rate management, regular

The addition of a yellow notch filter in the Christie HD2Kc, HD5Kc and the HD7Kc models allows greater separation between primary colors for richer color depth and a

During an entomological excursion from 14th till 21st July 2012 in Corsica, France, a new locality for the Corsican Blue Polyommatus ( Lysandra ) coridon nufrellensis

Myriad Technologies provided a world class intranet that allows Queensland Treasury to revolutionise the way their staff interact by using the range of tools in available in

thesis entitled “GENETIC DIVERSITY AND STABILITY ANALYSIS OF SWEETPOTATO GERMPLASM FOR LEAFY VEGETABLE” in accordance with Universiti Pertanian Malaysia Higher Degree Act 1980

The simplest conceivable factor model is a one-factor market model, usually labeled the Market Model, which asserts that ex-post returns on individual assets can be entirely

361 § 1 of the Civil Code (A person obliged to pay compensation is liable only for normal consequences of the actions or omissions from which the damage arises.) links the

This Code is based on the 1981 edition of the Public Utilities Board Code of Practice on Water Services and is intended to provide guidance to Professional