This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

TRANSNATIONAL MS&E

VALUE AND SUPPLY CHAIN

OPTIMISATION

FINAL REPORTAuthors:

doc dr. Gašper Gantar, Envita Alenka Zelenič

Contributing and editing (Spirit Slovenia): Alenka Mubi Zalaznik

Mitja Škrbec Tilen Globokar

2 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

CONTENT

1. INTRODUCTION ... 4

2. TERMINOLOGY ... 5

3. KNOWLEDGE SUPPLY CHAIN AND KNOWLEDGE VALUE CHAIN... 7

3.1 Knowledge supply chain ... 7

3.1.1 Innovation funnel ... 8

3.1.2 Domains and role-players of the knowledge supply chain ... 13

3.2 Knowledge value chain ... 14

3.2.1 Knowledge value chain model ... 15

3.2.2 Relationship between business value chain and KVC ... 15

4. KNOWLEDGE NETWORK (KN) – A STEP TOWARD IMPROVED MANAGEMENT OF THE KNOWLEDGE SUPPLY CHAIN ... 18

4.1. What is a knowledge network? ... 18

4.2. Role – players in KNs ... 18

4.3 Knowledge network characteristics ... 19

4.4 Aligning the knowledge network to support hierarchical deployment of innovation projects .. 21

4.4.1 Resolution of integrated planning ... 21

5. EUROPEAN INNOVATION POLICY - LEVERAGING ITS POLICIES EXTERNALLY ... 24

5.1 FL and regional knowledge supply chain ... 25

6. CONCLUSIONS ... 27

3 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

LIST OF FIGURES

Figure 1 The material and knowledge supply chains that support sustainable innovation

Figure 2 Innovation Funnel

Figure 3 Model 1 - Innovation funnel model common in larger, technology intensive companies

Figure 4 Model 2 - Innovation funnel model common in small, entrepreneurial start-ups

Figure 5 The extended innovation funnel

Figure 6 The Left Side – The Exploring Side of the Funnel

Figure 7 The Right Side – The Exploiting Side of the Funnel

Figure 8 The Stage Gate Model

Figure 9 The components of the knowledge supply chain

Figure 10 Different reasons for collaboration with different partners

Figure 11 Knowledge value chain model

Figure 12 Relationship between business value chain and KVC

Figure 13 The knowledge value chain

Figure 14 integrated knowledge network components

Figure 15 Examples of knowledge network characteristics with indicators (on the right side)

Figure 16 Framework Knowledge Networks - a micro perspective

Figure 17 Aggregating levels of different role-players and roadmaps

Figure 18 The position and function of FL in the knowledge supply chain as specify in the FLAME project

4 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

1.

INTRODUCTION

In the present competitive climate1 where the only certainty is uncertainty, knowledge is considered the main distinguishing factor of business success and is seen as the foundation of competitive advantage. Knowledge is seen to be the most important strategic resource, and many organisations realise that the value incorporated in their products and services is mainly due to the development of organisational knowledge resources. In the current competitive context, many organisations have realised that the only source of sustainable competitive advantage they can leverage is the effective use of their existing knowledge as well as the fast acquisition and utilisation of new knowledge.In his writings Drucker supports the proposition that knowledge is the single most important element fuelling the competitiveness of an enterprise, an industry, or even an entire country. He was among the first to realize that knowledge is neither a theory, nor a luxury — it’s a mission-critical resource you need to manage effectively in order to compete optimally in a persistently challenging global economy. The only competitive advantage that approaches true sustainability is, according to Drucker, produced by (1) acquiring organizational knowledge better and faster, and (2) converting that knowledge into results better and faster, than your rivals. This knowledge is also called superiority, a term borrowed from modern military strategy.

The purpose of this report is to present more in detail the role of knowledge supply- and knowledge- value chains in the process of enabling actors primarily from the MS&E sector, but other sectors as well, to internationalise their services.

The report puts special attention to knowledge networks (KN) - organizational environment within which knowledge processes take place in order to achieve innovation. KNs have been identified as a possible step toward improved management of the knowledge supply chain. The identified core characteristics impacting the performance of such a knowledge network are: reach, relationships, resources, roles, technology, flows, performance, and openness.

A special attention has been given to the convergence of many disciplines and to a particular kind of the interaction among individuals (in our case organisations – members of the knowledge supply chain). Innovation is namely “a team sport” that succeeds only through constant communication, iteration, and improvement.

European innovation policy framework has been taken into account when addressing the issue of creating FLs in Europe. Developing a common set of tools in MS&E technology transfer is considered an interesting opportunity not only for the MS&E sector within the project partner countries’ region but also for other sectors and other EU regions as well as beyond EU borders.

1

Daniela Carlucci, Bernard Marr, Gianni Schiuma: The knowledge value chain: how intellectual capital impacts on business performance, Int. J. Technology Management, Vol. 27, Nos. 6/7, 2004

5 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

2.

TERMINOLOGY

The following terminology and acronyms are used throughout this document. We are indicating them here to enable clear communication and reduce the possibility of misunderstandings.

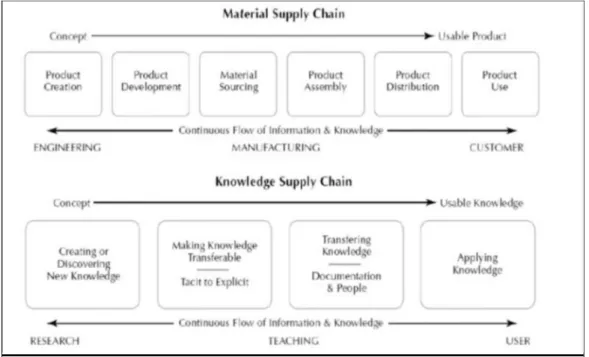

Material Supply Chain

Is applicable to the product development innovation process and shows how engineering, manufacturing and customer value are linked in the process of creating a product from concept through to customer utilisation

Knowledge Supply Chain

Is equivalent to a knowledge generation value chain. It indicates how discovering new knowledge, making the knowledge transferable (from tacit to explicit), transferring that knowledge through documentation and from person to person, and finally applying that knowledge, all support the material supply chain

Knowledge Value Chain

It is a sequence of intellectual tasks by which knowledge workers build their employer's unique competitive advantage and/or social and environmental benefit.

Knowledge Network

Organizational environment within which knowledge processes take place in order to achieve innovation

Community of practice

A group of individuals engaged on a recognised subset of applied research questions, with accepted attitudes, behaviours relating to the communication of research findings

Innovation Funnel

The overall development process starting with a broad range of inputs and gradually refining and selecting from among them, creating a handful of formal development projects that can be pushed to rapid completion and introduction.

TT, Technology Transfer

The process of converting scientific and technological advances into marketable goods or services. Also, terms TTO (Technology Transfer Offices/Organisations) and TTP (Technology Transfer Professionals) are used to describe the organisations/entities established to support this process and individual with specialist knowledge and expertise to do so, respectively.

MS&E, Material Sciences & Engineering

These are the main (or at least initial) areas of research that the Future Labs are supposed to focus on.

ROs, Research Organisations

Research Organisations are any research organisations, public or private, involved in the fields of material sciences and engineering (MS&E).

6 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

FL, Future Lab

Future Labs are the end result of the FLAME project. This document outlines the form which these Future Labs should take to have the most positive impact on the desired target partners and within the existing environment.

SMEs, Small and Mid-sized Enterprises

Future Labs will be focusing mainly on small and mid-sized companies as their initial target industrial partners.

7 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

3.

KNOWLEDGE SUPPLY CHAIN AND KNOWLEDGE VALUE CHAIN

3.1 Knowledge supply chain

Innovation2 is the successful implementation of a new product, process, service or technology in such a way that sustainable execution of the enterprise mission, either to make money, to provide a service or to give sustainability, is fulfilled. Figure 1 below, from the NGM report, indicates the basic components of two supply chains: a material supply chain and a knowledge supply chain. Understanding the knowledge supply chain will facilitate rapid innovation in the material supply chain, and the two supply chains are thus also interrelated.

- The material supply chain is applicable to the product development innovation process and shows how engineering, manufacturing and customer value are linked in the process of creating a product from concept through to customer utilisation. Engineering, manufacturing and the customer are involved in the continuous flow of related information and knowledge about the product, its manufacturing and its utilisation. A similar supply chain could be depicted for services and logistics.

- The knowledge supply chain is equivalent to a knowledge generation value chain. It indicates how discovering new knowledge, making the knowledge transferable (from tacit to explicit), transferring that knowledge through documentation and from person to person, and finally applying that knowledge, all support the material supply chain.

Figure 1: The material and knowledge supply chains that support sustainable innovation

2

N. D. Du Preez, L. Louw: Managing the Knowledge Supply Chain to Support Innovation, Laboratory for Enterprise Engineering, Department of Industrial Engineering, Stellenbosch University, South Africa, COMA 07 International Conference on Competitive Manufacturing

8 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

3.1.1 Innovation funnel

All enterprises3 require a unique kind of environment to thrive that free markets alone do not provide. The success of innovation requires the convergence of many disciplines and a particular kind of the interaction among individuals. Innovation is a team sport that succeeds only through constant communication, iteration, and improvement.

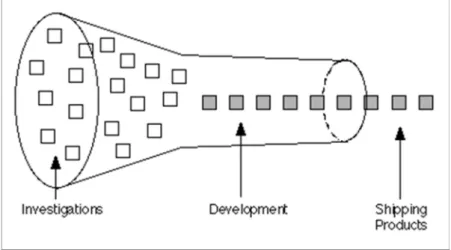

The aim of any product4 or process development project is to take an idea from concept to reality by converging to a specific product that can meet a market need in an economical, manufacturable form.

The overall development process starts with a broad range of inputs and gradually refines and selects from among them, creating a handful of formal development projects that can be pushed to rapid completion and introduction. This notion can be illustrated as a converging funnel (bellow).

Figure 2: Innovation Funnel

In its simplest form, the development funnel provides a graphic structure for thinking about the generation and screening of alternative development options, and combining a subset of these into a product concept. A variety of different product and process ideas enter the funnel for investigation, but only a fraction become part of a full-fledged development project.

Managing the development funnel involves three very different tasks or challenges. The first is to widen the mouth of the funnel - the organisation must expand its knowledge base and access to information in order to increase the number of new product and new process ideas. The second challenge is to narrow the funnel neck - ideas generated must be screened and resources focused on the most attractive opportunities.

The goal is not just to apply limited resources to selected projects with the highest expected payoff, but to create a portfolio of projects that will meet the business objectives of the firm while enhancing the firm's strategic ability to carry out future projects. The third challenge is to ensure that the selected projects deliver on the objectives anticipated when the project was approved.

3

Victor W. Huang, Greg Horowitt, The Rainforest, The Secret to Building the next Silicon Waley, Regenwald; 1.02 edition (February 21, 2012)

9 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. There are two dominant models of development funnel, which are broad patterns showing the kinds of choices companies (SMEs and large companies) have to make.

- Model 1 (see Figure 3) is common in larger, technology intensive companies, relying primarily on their R&D group to generate ideas for technologies, products and processes. Encouragement is given to generate many more ideas than will be applied, and these are then screened in various ways and at various stages.

Figure 3: Model 1 - Innovation funnel model common in larger, technology intensive companies

- Model 2 (below) is a top down model common in small enterprises, in which they sometimes bet on a single project.

Figure 4: Model 2 - Innovation funnel model common in small, entrepreneurial start-ups

In both illustrations the circles represent new products; shading indicates the extent of development, and size the scale of the project.

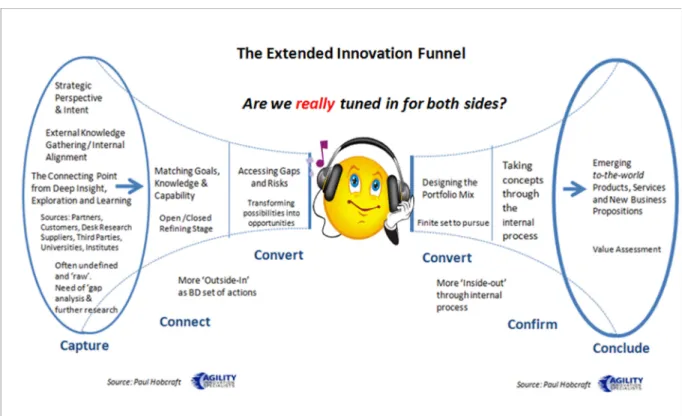

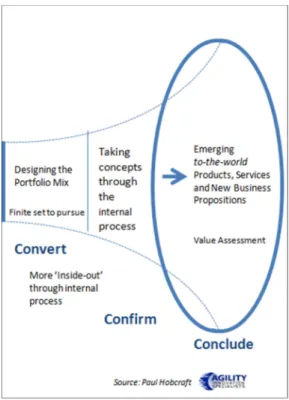

But according to Paul Hobcraft5 there are two distinctive parts to any innovation funnel – the left side (the exploring side) and the right side (the exploiting side).

5

10 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 5: The extended innovation funnel

- The Left Side – The Exploring Side

Figure 6: The Left Side – The Exploring Side of the Funnel

The Left Side is often not deeply appreciated and it is the side the less time is spent upon. “Before anything else, preparation is the key to success”. Really mastering this side of the funnel allows for the potential for better ideas/concepts to move through the complete funnel. This is the raw end, the side that really is the hardest part, the often really, really, fuzzy part. This is the place mostly lying

11 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. outside the organization’s domain of knowledge where the ‘real world’ functions and where constantly search and scan the horizon for possible ‘breaking opportunity or possibility is needed, not just ideas that might fit from within the organisation’s own world but ones that alter that world. What is needed to capture within the left side of the funnel?

1. Firstly, this is where innovation and the organisation’s strategy need to get good alignment. Having a clear perspective of what the organisation needs to focus upon is going to get it far quicker to spotting possible opportunities. It helps to have a ‘reasonable’ understanding of intent, of capabilities, of potential to take this ‘raw material’ and convert it into a tangible set of ideas or concepts.

2. The External Knowledge gathering and Internal Alignment need to keep working these ‘nuggets’ of raw opportunities, relating them, exploring them, turning them over in organisation’s mind, in its thinking about possibilities and seeking different points of alignment.

3. The connecting points come from the deeper set of insights the organisation has about its markets, customers and their unmet needs and organisation’s capacities to translate these through exploring any potential from the ‘raw material’ and the degrees of learning that comes with this, to convert it into something value and eventually commercial.

4. Knowing where to go as sources of knowledge is becoming more critical. These can be through existing partners, through university connections, collaborations with competitors, institutes or by completing organisation’s own desk research offers the organisation a wealth of places to explore. The key is being alert to ‘seeing possibility’ but at the same time ‘being aware’.

5. Once the organisation has some raw concepts or ideas they will need some testing against. Not just can this be translated into a finished product that gives us value but does it map back to organisation’s research, its internal understanding of market/ customer and their needs. To sell any raw thinking back into a company the organisation needs to make it relevant, it needs to connect, and it needs context.

The organisation really does need to make the necessary connections

1) Going back to matching goals, the knowledge gained and needed and the internal capabilities to translate this really needs working through before it enters the actual internal process.

2) Also a preliminary assessment if this can be managed and where it is going to be developed; purely internally (closed innovation) or do you need to have a collaboration with external partners (open innovation) or equally, the raw thinking was already found through a collaboration and you need to build the justification to take this further, in agreements, resourcing etc.

3) Many organizations are looking beyond raw thinking and deliberately searching for concepts already part-baked or proven concepts that can be ramped up or scaled quickly or just needing the additional expertise their organization can bring into the mix.

Then the final part of the left side of the innovation funnel are:

1) Doing the assessment of risks and returns. Assessing the potential value to the organization to turn its full resources on and take the idea/ concept through the idea to

12 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

commercialisation funnel. Addressing the gaps, the risks, the impact becomes the beginning of refining the business case.

2) It is at this point you transform possibility into business opportunity. The seeds of an idea have already been through a fairly vigorous evaluation, it is at this point you make the ‘case’ for this to enter the classic’ innovation funnel.

- The Right Side – The Exploiting Side

Figure 7: The Right Side – The Exploiting Side of the Funnel

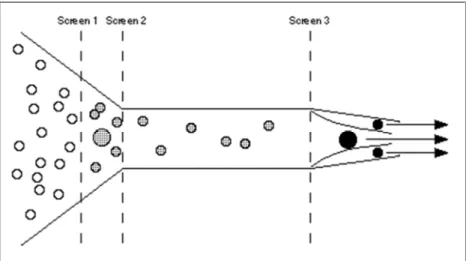

This is the better known and discussed part of the funnel. By working through the left side of the funnel the organisation has refined much more. What is entering the funnel is arguable not needing the traditional wide-neck funnel; it actually becomes the narrow part. It is then a real need to widen out these as the concept takes hold and has resource taking these up and exploring the idea and working through the concept to turn it into final offerings or multiple ones for release into the world. Ideas were evaluated well before they entered the commercialisation process (the right side of the funnel). The critical thing here is they need to meet the organisation’s portfolio aspirations and goals, any concepts need to ‘fit’. Fit not just a portfolio but the strategic goals, the product intent, the market and customer needs. This is the point the organisation starts really testing and refining inside itself. Stop just ideas simply entering the organisation’s commercialization part of the funnel, it wastes precious resource and dilutes energy, better spent on focusing on the real few valuable potentials moving across into the right side of the funnel. Taking concepts through the internal process, we come back to the stages the organisation takes a concept through – this could look like this, based on the stage-gate approach (Figure 8).

13 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 8: The Stage Gate Model

To summarise, the present thinking of the innovation funnel needs to be extended backwards, even back before the classic ‘ideas’ of people gathered in brainstorming sessions or simply using idea management software to explore mostly random thoughts that often do not translate. You need to start with a strategic perspective and define your intent, your intent to look for ‘targeted’ ideas and raw opportunities not the ones randomly offered in idea generation sessions. Start at the beginning and not as we seem to do, in the middle. Let’s listen to both sides of the innovation funnel; it can produce a better (re)sounding results. The more and earlier you know what kind of value your business is aiming to create, the better the eventual concepts entering the commercial end of the funnel will be. Then managing these in the most appropriate way given the context in which your business operates makes both ends of the funnel mutually important.

3.1.2 Domains and role-players of the knowledge supply chain

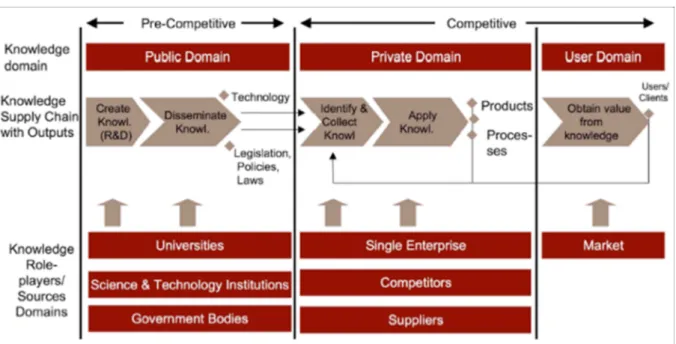

As seen from Figure 10 (below), the knowledge supply chain is dissected into different knowledge domains, different corresponding supply chain outputs as well as different role-players. In many cases the different role-players are also organised in more or less formal Integrated Knowledge Networks. Some aspects are clear when analysing this diagram:

- Public and private domain information result in an abundance of knowledge. This implies an extensive risk of information overload

- The innovation process that must support the material supply chain is much too complex to be addressed by a single team in a single project thus dividing to conquer is an imperative. Thus a multiple team approach with proactive knowledge creation, evaluation, filtering and a deployment is advised.

- The extensive interaction between public domain activities and private domain development work is an imperative.

- Such a hierarchy of interrelated teamwork can be devised, and can facilitate the rate at which innovation is deployed

The knowledge supply chain covers different knowledge domains: public, private and user domains.

A public domain, which is part of the pre-competitive phase, includes knowledge creation (R&D) and dissemination resulted in technology, legislation, policies, laws, etc. Key role – players or domain sources are universities, Science and Technology Institutions (S&T), Government bodies. The second, the so called private domain, part of the so called competitive phase. It includes identification and collection of knowledge as well as its application, resulting in the form of outputs such as products, processes, etc. The most important role-players are single enterprises, competitors, suppliers, etc. The last domain is the so called user domain, which is also part of the competitive phase. It focuses on obtaining value from knowledge, resulting in the number of users, clients, etc. Key role-player in the user domain is the market.

14 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 9: The components of the knowledge supply chain.

It is clear that significant benefits are to be gained for those companies that successfully formalise knowledge networks, which will be described in detail further on in this document.

The different reasons for collaborating with different partners are tabulated in Figure 11, from which it is clear that a wide range of stakeholders and benefits are realised through collaboration.

Figure 10: Different reasons for collaboration with different partners

3.2 Knowledge value chain

The Knowledge Value Chain (KVC)6 is an Intelligence Management methodology focused on knowledge processes — business strategy, market research, corporate intelligence, knowledge management, special libraries, and even R&D and legal research. It is a sequence of intellectual tasks by which knowledge workers build their employer's unique competitive advantage and/or social and environmental benefit. Improvements also flow from the knowledge integration that occurs when

6

15 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. knowledge management techniques are applied to the continuous improvement of a business process or processes. The term first started coming into common use around 1999, appearing in management-related talks and papers. It was registered as a trademark in 2004 by TW Powell Co., a Manhattan company.

3.2.1 Knowledge value chain model

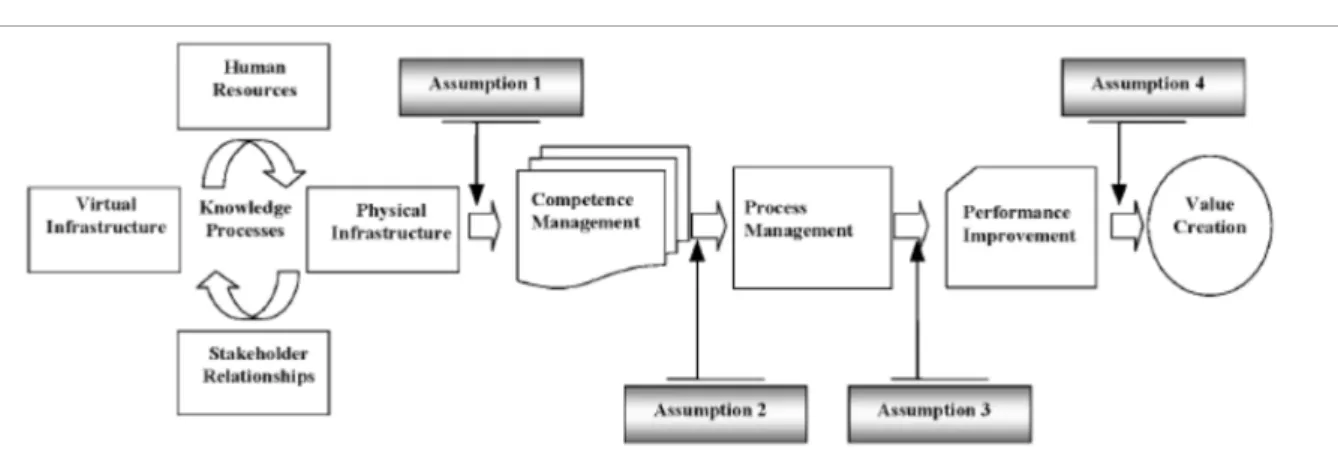

The knowledge value chain model7 (see figure 11 below) consists of knowledge management (KM) infrastructure (knowledge worker recruitment, knowledge storage capacity, customer / supplier relationship, chief knowledge officer (CKO) and management), the process of KM (knowledge acquisition – scanning, focused search and performance monitoring, knowledge innovation – the process organizationally amplifying the knowledge created by individuals and crystallizing it as part of the knowledge network of the organisation, knowledge protection – protection of intellectual property rights (IPR), knowledge integration – translation of raw knowledge into actionable knowledge by means of an acute understanding of business context and knowledge dissemination – creation of knowledge – shearing environment) and the interaction among those components resulting in knowledge performance.

Figure 11: Knowledge value chain model

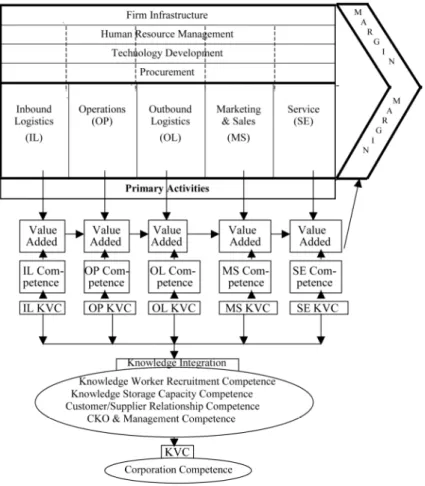

3.2.2 Relationship between business value chain and KVC

As the value chain itself implies, each element of activity can create value and then all the value flows to the endpoint of the business value chain and joins together forming the overall value of business, which is usually expressed as a margin (see Figure 12).

7

Ching Chyi Lee and jie Yang »Knowledge value chain«, University of Hong Kong, Hong Kong - www.emerald– library.com

16 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 12: Relationship between business value chain and KVC

The added value comes from the competence of element activity itself, which in turn comes from specific sub-KVC of itself. Finally, all the sub-KVC are integrated together into the whole KVC. In the process of knowledge integration, the competence of knowledge infrastructure is gradually forming. In the end, corporation competence follows KVC.

Improvements in business performance equal an increase in value generated for the key stakeholders of an organisation. The generated value is the result of an organisation’s ability to manage its business processes. The effectiveness and efficiency of performing organisational processes are based on organisational competencies. KM enables an organisation to grow and develop organisational competencies. Therefore, the cognitive nature of organisational competencies allows us to state that their improvement takes place through KM and that KM is at the heart of business performance improvement and value creation.

17 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. Assumption 1: Knowledge management is at the basis of developing organisational competencies.

Assumption 2: The effectiveness and efficiency of organisational processes depend on organisational competencies.

Assumption 3: Improvements in business performance depend on effective and efficient processes.

Assumption 4: Improvements in business performance equates with an increase in value generated for organisational stakeholders.

18 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

4. KNOWLEDGE NETWORK (KN) – A STEP TOWARD IMPROVED

MANAGEMENT OF THE KNOWLEDGE SUPPLY CHAIN

4.1. What is a knowledge network?

The most valuable8 and most up-to-date knowledge in an organisation is the collective knowledge that is contained in the heads of the individuals (tacit knowledge) combined with captured (explicit) knowledge. Due to new personal learning, experiences, insights and ideas, this tacit knowledge is continually being updated. By enabling individuals to better communicate and collaborate within a team, across teams and across entire organisations and inter-organisations, even more significant new knowledge, insights and ideas will be created, transferred, shared, absorbed and leveraged at a much faster rate, thus promoting innovation rates.

Knowledge Network could be understood as “a number of people, resources and relationships among them, who are assembled in order to accumulate and use knowledge primarily by means of knowledge creation and transfer processes, for the purpose of creating value”. Concerning the development of knowledge networks, we could distinguish between emergent and intentional ones. Intentional knowledge networks are networks that are built up from scratch, whereas emergent knowledge networks already exist but have to be cultivated in order to perform well. A related concept to that of a knowledge network is the concept of a community of practice (COP). COP could be defined as “a group of individuals engaged on a recognised subset of applied research questions, with accepted attitudes, behaviours relating to the communication of research findings.”

Knowledge Networks can therefore be seen as the organizational environment within which knowledge processes take place in order to achieve innovation.

4.2. Role – players in KNs

The following are relevant components ofknowledge networks according to Vassiliadis etal.9:

- A Project Team/Task Force represents a group of people having a specific issue or a problem to solve in order to achieve a desired goal.’

- A community of interest is for example a platform on the internet, where a group of people in a loose confederation share common interest in, and information about their interest.

- A community of practice is a group of people who are to a large extent involved in similar work in a common craft.’

- Members. Actors or members in a social network can be persons, groups, but also collectives of organizations, communities or even societies. Members of knowledge network take different roles. From an organizational perspective, customers, suppliers, competitors or government organizations as well as employees have distinct functions within a network.

- Relationships. In order to create connectivity of the members through interactivity in a network we have to examine closely the relationships.

- Knowledge. As stated earlier knowledge can be of different kinds: it can be tacit or explicit, social or individual.

8

N. D. Du Preez, L. Louw: Managing the Knowledge Supply Chain to Support Innovation, Laboratory for Enterprise Engineering, Department of Industrial Engineering, Stellenbosch University, South Africa, COMA 07 International Conference on Competitive Manufacturing

9Vassiliadis, S., Wicki, Y., Seufert, A., Back, A., von Krogh, G., Knowledge Networks: Linking Knowledge Management to Business Strategy,

19 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. The main role-players as defined by the authors are universities, S&T Institutions, government bodies, single enterprises, competitors, suppliers and the market as is depicted in Figure 15. These are organised in different communities, that when integrated, constitutes a knowledge network. This diagram implies some high-level integration realities.

Figure 14: integrated knowledge network components

4.3 Knowledge network characteristics

The characteristics impacting the performance of such a knowledge network are: reach, relationships, resources, roles, technology, flows, performance, and openness. Figure 15 provides an insight into characteristics of members, relationships and knowledge.

20 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 15: Examples of knowledge network characteristics with indicators (on the right side)

Seufert et al.10 define the framework of knowledge networks as comprising actors, individuals, groups, organizations and relationships between actors ‘which can be categorized by form, content and intensity; resources which may be used by actors within their relationships, and institutional properties, including structural and cultural dimensions such as control mechanisms, standard operating-procedures, norms and rules, communication patterns, etc.’. This is depicted in Figure 16.

10

Seufert, A., Von Krogh, G., and Bach, A., 1999, Towards Knowledge Networking, Journal of Knowledge Management, 3:180-190.

21 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 16: Framework Knowledge Networks - a micro perspective

4.4 Aligning the knowledge network to support hierarchical deployment of

innovation projects

It is clear that the challenges of rapidly deploying innovation processes require more than just incidental integration and knowledge alignment. Competitive Industry has responded by formalising knowledge networks that could address specific integration requirements.

Vassiliadis et al.11 state that “knowledge network characteristics differ according to the business goal they are mainly dedicated to’. They continue saying that it is important to stress that ‘a deeper understanding of the business strategy of a knowledge driven company is necessary in order to develop and nurture an appropriate knowledge network”.

It is clear that structure and communication protocol are not the only important aspects for successfully utilising an IKN in enterprise-wide Innovation Management. The ability to proactively manage the knowledge work within all subsets of the network (components) as well as to rapidly integrate it in the bigger whole is one of the main challenges of an IKN. Efficient planning for innovation projects over different levels of knowledge aggregation is therefore essential.

4.4.1 Resolution of integrated planning

Another challenge is that of resolution management in deployment of the innovation life cycle. Figure 17 depicts examples of different levels of knowledge aggregation together with the various role-players involved. As some of these exist in the public domain, it is possible to proactively

11

Vassiliadis, S., Wicki, Y., Seufert, A., Back, A., von Krogh, G., Knowledge Networks: Linking Knowledge Management to Business Strategy, Research Center, KnowledgeSource, University of St. Gallen

22 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. process some of the knowledge resources into repositories in anticipation of later use in innovation projects. From Figure 17 it is clear that:

- A hierarchy of planning for innovation ranges from a literally global level right down to a single person’s role and mandate for a specific task within a single innovation project.

- Although it is impossible to address all the different layers of planning for each and every innovation project, it is imperative to have readily available as much information as is possible before the start of an innovation project.

23 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 17: Aggregating levels of different role-players and roadmaps

24 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

5. EUROPEAN INNOVATION POLICY - LEVERAGING ITS POLICIES EXTERNALLY

The Europe 2020 strategy and its ʻflagshipʼ iniTaTves focus on investments in educaTon, research and innovation as the key to achieving smart, sustainable and inclusive growth. In this context, the Innovation Union flagship initiative, together with the Digital Agenda, Industrial Policy and Resource Efficient Europe flagships, and the Single Market Act, aim to create the best conditions for Europe's researchers and entrepreneurs to innovate.Figure 18: EU flagship initiatives (source: Sergej Možina, Permanent Representation of the Republic of Slovenia to the EU)

The Innovation Union flagship in particular is about creating a vibrant, innovation-based economy fuelled by ideas and creativity, capable of linking into global value chains, seizing opportunities, capturing new markets and creating high-quality jobs. Overall, progress towards setting up the policy framework for an Innovation Union has been very positive: more than 80% of the initiatives are on track. The call by the Heads of State and Government to deepen the European Research Area is being turned into concrete actions. The Commission's ʻHorizon 2020ʼ proposal for a future European research and innovation programme marks a clear break with the past by covering the entire value creation chain in one single programme. The principle of ʻsmart consolidaTonʼ — i.e. protecting or, if possible, increasing growth-friendly expenditures, such as R&D — is now widely accepted and is embedded in the European Semester. The business environment in Europe will become more innovation-friendly thanks to Single Market measures such as the unitary patent, faster standard setting, modernised EU procurement rules and a European passport for venture capital funds. European Innovation Partnerships are pooling resources and concentrating demand and supply-side

25 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. measures on key societal challenges. While these measures still need to be implemented to start bringing results, they represent a fundamental shift in the right direction.

The global position of Europe is still relatively strong. The EU is one of the world's best performers when it comes to producing high-quality science and innovative products. It still captures the largest and a stable share (28%) of income generated in global manufacturing value chains while the US and Japan saw their shares shrinking. Since 2008, the EU has improved its innovation performance and it closed almost half of the innovation gap with the US and Japan12.

The EU is also keeping its strong innovation lead over Brazil, India, Russia, and China, although the latter is most markedly catching up. In addition, South Korea has almost tripled its innovation lead over the EU since 2008 and joined the US as an innovation leader.

Furthermore, while public R&D spending in the EU grew throughout the crisis as governments strived to keep up their R&D investments and thus incentivise businesses to do likewise, recent data point to a potential reversal of this trend. In 2011, for the very first time since the beginning of the crisis, the total public R&D budget of the 27 EU Member States decreased slightly.

The on-going economic crisis has also exposed structural weaknesses in Europe's innovation performance. The 2013 Innovation Union Scoreboard shows that the process of convergence in the innovation performance of Member States has come to a halt. As convergence was the dominant pattern since the introduction of the Scoreboard in 2001, this signals a clear risk of an increasing innovation divide.

As the crisis gets longer and deeper, growth disparities between some European regions are increasing, there is an even stronger need to implement the Innovation Union swiftly and deepen it in the areas crucial to innovation, such as higher education, innovation-based entrepreneurship and demand-side measures. Momentum in fields like social innovation will also need to be maintained. Europe therefore needs fresh dynamism in its economy. Existing, traditional industries in which Europe excels need to develop new applications and new business models in order to grow and maintain their competitive advantage. Furthermore, in dynamic fields such as ICT-based businesses and in emerging sectors Europe needs more high-growth firms. This calls for an innovation-driven structural change, but Europe is at present missing out on the more radical innovations which drive and lead such structural change.

Consequently, what Europe needs most in the next decade is to attract top talent and reward innovative entrepreneurs, to offer them much better opportunities to start and grow new businesses.

5.1 FL and regional knowledge supply chain

Within the FLAME project the project partners have tried to experiment innovative co-operation modules that facilitate the information flows and interactions among the regions, on an international level. They have tried to provide conditions enabling enterprises to bring MS&E knowledge and technologies to the market, to internationalize their value & supply chains and thereby improve their growth potential.

12

26 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 19: The position and function of FL in the knowledge supply chain as defined within the Flame project

The interest for new materials of many Central European regions’ industrial systems is still high and there are many cases of experimentation of innovative solutions by trial and error, in co-makership with the client. From the point of view of the demand side as new materials applications, the local industrial networks seem interested in investing into nano-technologies, innovative polymers and special metal alloys in many Central European regions, they have very specific applicative requests or a general demand for support to redesign their own business. On the other hand industrial actors engaged in materials research have few common problems and they do not trigger a local demand for systematic research with a critical mass of applications.

The Flame project has been recognised as the possible solution for the “missing” stage in the MS&E value chain.

The creation of the number of FLs in Europe, developing a common set of tools in MS&E technology transfer, is considered an interesting opportunity. At the same time FLs want to offer something unique to the current environment. The FLs will be facing several issues in their work. It is important to be aware of these and to understand how they will be addressed. Emphasis should be given on services that are not available by other organisations. Different characteristics of partner FLs and the fact that each of them is closely connected to its “mother” institution must be taken into account. But nevertheless, some questions arise, such as:

- What kind of services should the existing Flame network provide to new-born regional FLs, as a scaffolding structure for MS&E businesses?

- What kind of European value is coming out from the regional diverse experiences of FLs and engagement of FCs engagement?

- What kind of recurrent interactions should be designed in order to learn by practical experiences and to provide newcomers in other regions with common tools, but also with a range of practical examples?

FL should focus on providing consultancy services and become a sales channel for all interested research organizations towards potential industrial partners in the entire region and wider. FLs’ key partners could be public and private research institutions (and their technology transfer offices - TTOs) active in the MS&E sector (other sectors as well)13 and industrial partners14.

13

KNOWLEDGE PROVIDERS: The ROs (through their TTOs) are the ones supplying the FLs with the services and products that can be offered to the target customers. FLs will be open for cooperation to all ROs (and their respective TTOs), both public and private, in the target region. All current partner and participating ROs of the FLAME project will be invited to join to begin with. However, due to the focus of FLAME, actively participating entities involved in MS&E will be given preference.

14

KNOWLEDGE ADOPTERS: Target customers are industrial partners which are and/or could be using services, products and inventions in the MS&E and related fields

27 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

Figure 20: Schematic presentation of possible FL’s services

6.

CONCLUSIONS

The current environment for organisations is one that is characterised by uncertainty and continuous change. This rapid and dynamic pace of change is forcing organisations that were accustomed to structure and routine to become ones that must improvise solutions quickly and correctly. To respond to this changed environment, organisations are moving away from the structures of the past that are based on hierarchies, discrete groups and teams and moving towards those based on more fluid and emergent organisational forms such as networks and communities. In addition to the pace of change, globalisation is another pressure that is brought to bear on modern organisations. The growing internationalisation of business means that many organisations now work in a geographically and temporally distributed international environment.

28 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF. Knowledge sharing between communities is likely to be more complex than intra-community knowledge sharing, due to the lack of shared consensual knowledge or shared sense of identity which typically exists in inter-community contexts. To facilitate effective inter-community knowledge sharing requires effort to be invested in developing the social relationship (and hence trust) between members from the communities. Organizations need to balance their efforts at building of practice with supporting inter-community interactions, otherwise they risk developing isolated and inward looking communities.

Within the FLAME project the project partners have tried to experiment innovative co-operation modules that facilitate the information flows and interactions among the regions, on an international level. They have tried to provide conditions enabling enterprises to bring MS&E knowledge and technologies to the market, to internationalize their value & supply chains and thereby improve their growth potential.

The Flame project has been recognised as the possible solution for the “missing” stage in the MS&E value chain. The creation of the number of FLs in Europe, developing a common set of tools in MS&E technology transfer, is considered an interesting opportunity. At the same time FLs want to offer something unique to the current environment. The FLs will be facing several issues in their work. It is important to be aware of these and to understand how they will be addressed. Emphasis will be given on services that are not available by other organisations. Different characteristics of partner FLs and the fact that each of them is closely connected to its “mother” institution must be taken into account.

Knowledge Network could be considered as a step toward improved management of the knowledge supply and also value chain.

29 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.

7.

LITERATURE

1. Daniela Carlucci, Bernard Marr, Gianni Schiuma: The knowledge value chain: how intellectual capital impacts on business performance, Int. J. Technology Management, Vol. 27, Nos. 6/7, 2004 2. N. D. Du Preez, L. Louw: Managing the Knowledge Supply Chain to Support Innovation, Laboratory for Enterprise Engineering, Department of Industrial Engineering, Stellenbosch University, South Africa, COMA 07 International Conference on Competitive Manufacturing 3. Victor W. Huang, Greg Horowitt, The Rainforest, The Secret to Building the next Silicon Waley,

Regenwald; 1.02 edition (February 21, 2012)

4. Wheelwright. S. C. and Clark. K. B., 1992, Revolutionizing Product Development, The Free Press, New York

5. Ching Chyi Lee and jie Yang »Knowledge value chain«, University of Hong Kong, Hong Kong - www.emerald–library.com

6. Vassiliadis, S., Wicki, Y., Seufert, A., Back, A., von Krogh, G., Knowledge Networks: Linking Knowledge Management to Business Strategy, Research Center, KnowledgeSource, University of St. Gallen

7. Seufert, A., Von Krogh, G., and Bach, A., 1999, Towards Knowledge Networking, Journal of Knowledge Management, 3:180-190.

Internet sources:

1. Innovation Union Scoreboard 2013, http://ec.europa.eu/enterprise/policies/innovation/files/ius-2013_en.pdf

2. paul4innovating blog at http://paul4innovating.com/ 3. http://www.knowledgevaluechain.com/home/

30 This project is implemented through the CENTRAL EUROPE programme co-financed by the ERDF.