GROWTH FOR GOOD OR GOOD FOR GROWTH?: How Sustainable and Inclusive Activities are Changing Business and Why Companies Aren t Changing Enough

Full text

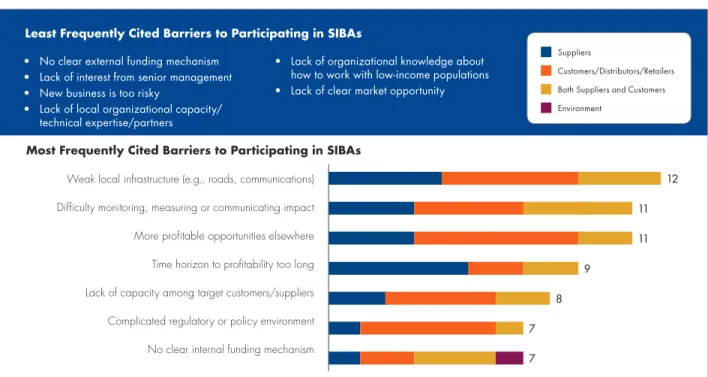

Figure

Related documents

He shows his self-confidence in facing family problem, love and

До складу авторського колективу не слід включати осіб, яких вже раніше було відзначено цією іменною премією, а також які вже були удостоєні Державної премії,

As miRNAs are known to have in the order of hundreds of putative mRNA target genes, which in addition tend to contain binding sites for more than one miRNA species adding to

Ana Motor /Main Motor 4 KW 5.5 HP Sürücü Motor / Driver Motor 0.25 KW Soğutma Suyu Motor / Cooling Water Motor 0.09 KW Hidrolik Pompa / Hydraulic Pump 2.2 LT Lama Kesim Kapasitesi

The documentary proof acceptable to the Commissioner in order to substantiate the application of the zero rate to a supply of movable goods that are consigned or delivered by

MEXT provides support for the creation of innovations in regions through the Comprehensive Support Program for Creation of Regional Innovation of the Japan Science and

Should you wish to partake in optional activities in the city where you tour starts/ends, please check their is sufficient time to do so or alternatively consider booking pre/post

In some groups of female tertiary education graduates, the estimated unemploy- ment rates are exceptionally high, even several years after graduation (university graduates