2013 Trends to Watch: Cloud

Services

The debate on cloud services’ place in enterprise IT is over

Reference Code: IT019003114 Publication Date: 25 Oct 2012 Author: John MaddenSUMMARY

Catalyst

The debate over whether cloud services will play a role in corporate IT is settled. Cloud is now largely viewed by enterprise customers as an additional path to outsourcing and service delivery. However, customers have many lingering questions on just how extensively and for what functions cloud services should be deployed. Moving into 2013, such decisions will be influenced by trends such as those we detail in this report, including the growing connection between cloud, mobility, and data; cloud services governance and integration; and continuing development of cloud ecosystems among vendors.Ovum view

Whether they like it or not, enterprise customers must consider cloud as part of the future state of their corporate IT. For many customers, the drumbeat around cloud’s promise of morepredictable IT operating costs, decreased capital spending, and increased flexibility is simply too loud to ignore. Going into 2013, our survey data (as detailed in our Ovum Cloud Services Business Trends Survey) indicates that overall cloud services investment will accelerate, with softwareasaservice (SaaS) deployments slightly outpacing investment in infrastructure and platformasaservice (IaaS and PaaS) deployments. In addition, private cloud will remain the preferred cloud services deployment model over public and hybrid deployments, although customers’ attitudes toward the latter continue to evolve. While cost remains a driving factor for many cloud services investments, some customers are beginning to consider cloud more strategically, in terms of what it could mean for improving business processes, entering new markets and geographies, and increasing overall business efficiency. A small but measurable shift is occurring in viewing cloud services as less tactical and more strategic, and we expect the strategic potential of cloud to take on even greater importance throughout 2013. Discussions around cloud services will move beyond simply whether to adopt a point IaaS, SaaS, or PaaS service. Instead, cloud will envelop other emerging trends to the point where any consideration ofcloud services will include a “nexus” of cloud, mobility, and data (business intelligence, data management, and analytics). Indeed, many IT services and outsourcing vendors are already connecting these trends in their cloud services gotomarket efforts, although when you dive into each provider’s individual portfolios, few have a full set of capabilities in each area. In addition, vendors are wrapping this nexus in a casing of security services in order to meet various compliance requirements within vertical industries. Using cloud services more strategically has implications for how they are managed, governed, and ultimately integrated with existing IT assets and other cloud services. These issues are increasingly important if customers want to move beyond private cloud and embrace a hybrid model where they can access an orchestrated set of services in traditional, private, and public cloud environments. Our survey data indicates that customers that have invested or are considering investing in cloud services need guidance on cloud management and governance models, which in theory should be tied to a broader cloud strategy within an IT organization. Vendors, in turn, have invested in a host of cloud services assessments and consulting offerings that are meant to map out cloud investments. We expect vendors to continue to develop and market such services throughout 2013. As the strategic importance of cloud services grows, vendors will want to be viewed as cloud services innovators in 2013, able to deliver the latest technology and services in customer cloud engagements. Innovation is certainly in the eye of the beholder, but vendors view innovation as one method of achieving differentiation among competitors. Customers, meanwhile, want assurances that they’re working with am IT services and outsourcing vendor that is a “switchedon” cuttingedge provider. One way larger IT services vendors create this innovation profile is through cloud ecosystems, either by acting as an ecosystem leader themselves – often through acquiring smaller cloudbased companies – and/or by ensuring they have an extensive network of alliances and partnerships. These ecosystems can include technology development, gotomarket, and joint sales components, and in some cases vendors are using these ecosystems for access to an array of cloud services from a variety of providers – services that those providers can then offer to their customers in a hybrid deployment model.

Key messages

• The deployment of cloud services will be tied to an emerging nexus of cloud–mobility–data, with a heavy emphasis on security and compliance. • Private cloud services will continue to outpace public or hybrid cloud services deployments. • Cloud governance, management, and integration will be solidified as key corporate priorities. • Vendors will search for innovation and a competitive edge through cloud services ecosystems, by either acting as an ecosystem leader or engaging in alliances and partnerships.BUSINESS TRENDS AND TECHNOLOGY ENABLERS

Economic and business pressures will impact the cloud services market

Table 1: Cloud services trends to watch Monitor the business environment Global economic factors continue to put pressure on enterprise customers and how they manage and deliver IT services to their organizations. This will compel customers to consider how cloud services could alleviate these cost pressures. Create the technology portfolio IT services providers and outsourcers are connecting trends around cloud, mobility, and data (business intelligence, information management, and analytics) in their marketing efforts to enterprise customers. As customers start to think about cloud services more strategically, this “nexus” of trends will come into play. Select solutions and services Many enterprise customers will consider cloud services because of their potential to deliver nearterm cost savings, but others will start to consider cloud as a more strategic move, integrating cloud services into their futurestate IT plans. Manage deployment outcomes Flexibility, automation, and transparency are necessary for successful cloud services deployments, but cloud services and integration will emerge as critical success factors going forward. Source: OvumCLOUD SERVICES TIED TO NEXUS OF CLOUD–MOBILITY–DATA

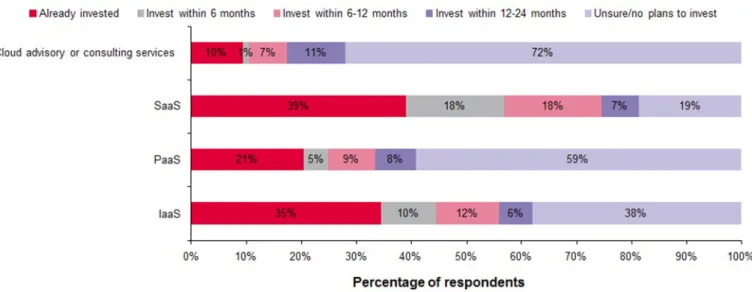

Accelerated adoption of cloud services expected, especially SaaS

Despite, or perhaps due to, the level of hype that preceded it, cloud services will never achieve a “hockey stick” growth trajectory as we saw with other IT technology and services trends (such as mobility or social media). Growth and adoption have remained more measured, with many customers approaching cloud services with an open mind but a cautious heart. Nevertheless, based on our Cloud Services Business Trends Survey and interactions with enterprise customers, we expect stronger adoption of cloud services in 2013 and beyond, with SaaS deployments slightly outperforming IaaS. As seen in Figure 1, 81% of respondents (which included large enterprise clients with 1,000 or more employees in the US, UK, Germany, and France) expected to deploy SaaS within two years, while almost twothirds expected IaaS investments in the same time period.Figure 1: Current and planned cloud services investments Source: Ovum Cloud Services Business Trends Survey, n=200 These results mirror the findings from Ovum’s Technology Trends survey, which is a broader survey on a variety of IT technologies and services across a variety of geographies and vertical industries. Among respondents with more than 1,000 employees, current and planned SaaS adoption is slightly ahead of IaaS, 34% to 32%; 68% percent indicated that they would deploy SaaS within 24 months. Reducing shortterm IT costs and ensuring longerterm savings continues to drive a majority of cloud services investments, and these issues will continue to play an important role in any cloud deployments in 2013. CIOs (depending on the region and geography) are dealing with either flat or reduced IT budgets and are under pressure from executive leaders and CFOs to deliver services more efficiently and thereby reduce the organization’s overall cost of doing business. As seen in Figure 2, respondents in our Cloud Services Business Trends Survey indicated that cutting IT or business costs remain the most important factors for cloud services investments.

Figure 2: Factors influencing cloud investment decisions Source: Ovum Cloud Services Business Trends Survey

Moving from tactical to strategic cloud services

Although cost remains a dominant motivator for cloud services investment, recently there has been a noticeable shift in how some customers are approaching the implementation of cloud – from a tactical, shortterm investment profile to one that’s more strategic, longer term, and transformational. Part of this is due to vendors’ efforts to position cloud as a catalyst for transformational change within an organization. But part is also due to customers wanting to take advantage of other market trends, most notably the explosive growth of mobility and emerging trends around data. The latter includes business intelligence, data management, and in particular analytics to mine customer data for usage and buying patterns and to predict and improve business performance. Some customers don’t want to limit transformation to cloud services, but they want to use cloud as one lever toward their transformative goals. As a result, customers and vendors are increasingly linking cloud, mobility, and data as part of transformational roadmaps, and we expect the connections of this cloud–mobility–data “nexus” to solidify in 2013. Customers, for example, will have more discussions about how they want or need cloudbased applications delivered to any device in use throughout their organization (mobile phones, iPads, other tablets) or how cloud services create new opportunities and challenges in terms of securely managing data and analyzing that data for business benefits. IT services vendors this year have already stepped up their marketing efforts that link these parts of their portfolios, and we expect that activity will increase throughout 2013. No matter how strong theirmarketing, some vendors are stronger than others when it comes to the actual offerings in their portfolios, and in some cases vendors are still trying to integrate these offerings into something more cohesive. To that end, we expect providers to make investments and acquisitions that will beef up one or all of these areas and to concentrate on the integration between them. Although cloud, mobility, and data are horizontal trends, some of these investments and acquisitions could be aimed at building up expertise and credibility in specific vertical industries, such as public sector, manufacturing, retail, and healthcare. In fact, health care will be a particular focus for IT services and outsourcing vendors in the US as requirements from nationwide health care reform – which mandates the use of IT for things such as health information exchanges and electronic health records – start to materialize. To be clear, this shift to making cloud services more strategic and transformational encompassing the nexus of cloud–mobility–data – is currently more the exception than the rule. But a combination of market trends and customer needs will make this shift more pronounced throughout next year.

PRIVATE CLOUD SERVICES OUTPACE PUBLIC OR HYBRID

Customer concerns about security still dominant

Even as customers start viewing cloud services as more strategic and transformational in 2013, cloud services security will remain a dominant concern among enterprise customers. In our Cloud Services survey, when asked about challenges to cloud services adoption, respondents cited data security concerns and regulatory/compliance issues as their biggest obstacles. Figure 3 below displays results from the entire survey base of 200 respondents. However, the results were virtually the same for each of the four main geographies as well as the major vertical industries, such as manufacturing as shown in Figure 4.Figure 3: Challenges or impediments to cloud services adoption Source: Ovum Cloud Services Business Trends Survey Figure 4: Barriers to cloud services adoption in manufacturing Source: Ovum Cloud Services Business Trends Survey

Private cloud remains the gateway to cloud services for many customers

Security concerns have prompted many enterprise customers to invest initially in private cloud services rather than public or hybrid models, and we expect that trend to continue into 2013. Private clouds, whether deployed onsite or offsite or managed internally or by a third party, provide a dedicated infrastructure and virtualized environment solely for use by a single organization. For some customers, that’s a much more attractive proposition than deploying resources into a public cloud with a shared and potentially less secure environment; indeed in some vertical industries a private cloud is necessary for legal, regulatory, and/or compliance reasons. Our survey data shows that a majority of customers intend to spend more of their cloud services budget on private versus public cloud in 2013 and beyond, and for many customers private cloud will continue to be the gateway to broader adoption of cloud services. This is not to say that customers are not warming to the use of public or hybrid environments. While our survey data does show greater spending on private cloud, respondents stated spending on public cloud would tick up in 2013 and in subsequent years. Use of public clouds among customers will ultimately depend on the type of cloud service and the applications and workloads involved. Some customers may opt for virtual private clouds, where a logical private cloud is established within a shared or public cloud environment. Recently, IT services and outsourcing vendors have been aggressive in emphasizing hybrid environments, where customers can deploy services in whatever model they see fit – traditional, private, virtual private, or public – and easily and seamlessly move applications and workloads from one model to another, with the provider handling the integration and orchestration of cloud services. While few customers have actually adopted hybrid models, some customers going forward may at least consider public and hybrid clouds, especially as vendors promote the concept of hybrid clouds as being the better way to ensure customer choice for cloud services.CLOUD GOVERNANCE AND INTEGRATION WILL BE KEY

Customers lacking on cloud strategy and governance

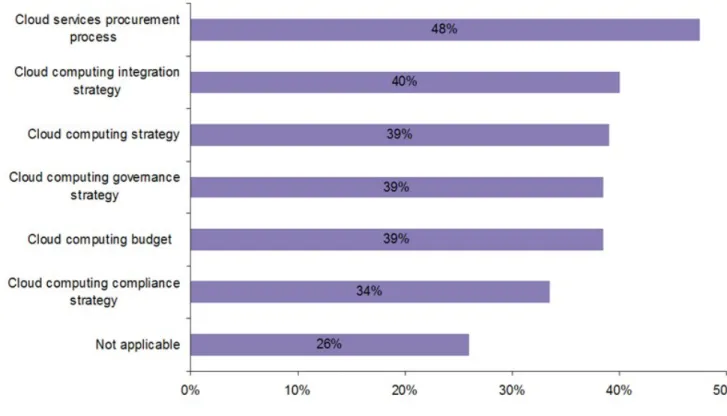

If, as we expect, customers start looking at cloud services more strategically rather than as simply a tactical point solution, there are implications as to how these services are managed, governed, and ultimately integrated with existing IT assets and other cloud services. These issues are increasingly important if customers want to move beyond private cloud and embrace a hybrid model where they can access an orchestrated set of services in traditional, private, and public cloud models. A proper place to start when tackling these issues is a broad cloud services strategy, which would influence issues related to governance, compliance, and integration. We expect cloud governance and integration will emerge as a top priority in 2013 among customers looking to implement cloud services. For instance, our survey data indicates that customers that have invested or are considering investing in cloud services need guidance on how to develop an effective cloud strategy and on issues related tocloud management, governance, and integration models, as seen in Figure 5. Only 39% of respondents stated they had a cloud strategy or cloud governance strategy, and only 34% stated they had a cloud compliance strategy.

Vendors continue to push cloud services assessments and roadmaps

IT services vendors, sensing that many customers are interested in cloud services but stymied on how to proceed, have invested heavily in the past year in cloud computing assessments, workshops, and consulting services to help customers develop cloud strategy and implementation plans. Our survey data indicates that uptake of such services so far has been slow, but we’ve heard anecdotal evidence that more customers are signing up for these sessions as they grow more serious about using cloud. We expect vendors to continue to develop and market these consulting services throughout 2013; those with current offerings will add to their portfolios, and other vendors will debut such services for the first time. We also expect these offerings will come to envelop the cloud–mobility–data nexus described earlier, with specialized workshops devoted to mobility, data management, and analytics in the age of cloud (some vendors have already introduced such sessions). Some of these are oneday sessions, usually offered for free as part of business development and as a way to highlight a vendor’s expertise and experience in cloud. Others are multiday or weeklong engagements where a vendor works with a client to map out current IT assets and applications, determine which workloads and functions can be moved to a cloud environment, and consider which cloud services approach – private, public, hybrid – would be ideal as part of a broader cloud strategy. Vendors also use these sessions to tackle issues related to cloud governance and management: who will set up and deploy cloud services, who should have access, who determines when more capacity is needed, and who will manage supplier relationships. Factor in issues such as mobility, where employees may use a range of devices (both corporate and personal) to access services, and governance issues take on even more importance. Vendors, of course, hope these sessions will turn into longer implementation projects, with the vendor providing some degree of management of a client’s cloud services environment. Through 2013, these consulting capabilities will provide an important “tip of the spear” for vendors to initiate customer conversations on cloud strategy and the vendor’s services.Figure 5: Internal cloud procurement and governance strategy Source: Ovum Cloud Services Business Trends Survey

VENDORS SEARCH FOR INNOVATION IN CLOUD ECOSYSTEMS

Trust is a critical factor in selecting cloud services providers

Competition in the cloud services space is already fairly cutthroat, but it will take on new dimensions in 2013 as customers begin to view cloud as more strategic. IT services and outsourcing vendors will want to be viewed as having the broadest cloud services portfolio and providing customers with the widest possible choices on how they plan, implement, and manage cloud. Vendors also want to demonstrate that they can shepherd customers through their cloud services “journey” at every turn. With customers looking to consolidate the number of strategic IT suppliers and outsourcers they deal with, vendors will be under new pressure to sharpen their marketing and their points of differentiation. However, at a more basic level, vendors will need to continue to prove they can be trusted to implement and run cloud services securely and effectively. Customers will naturally turn to their incumbent providers or vendors with whom they’ve worked previously as they explore cloud services, but only if they’ve earned a high level of trust. As seen in Figure 6, respondents rated trust in the provider as thenumber one factor in selecting a cloud services provider, followed closely by security expertise and data/information management expertise. Figure 6: Factors influencing cloud services vendor selection Source: Ovum Cloud Services Business Trends Survey

Ecosystems are an important part of the cloud innovation profile

Trust and security expertise by themselves will not provide strong points of differentiation. As the strategic importance of cloud services grows and market competition intensifies, vendors will want to be viewed as cloud services innovators in 2013, able to deliver the latest technology and services in customer cloud engagements. Innovation is certainly in the eye of the beholder, but vendors view innovation as one method of achieving differentiation, particularly among large outsourcers whose cloud marketing pitches contain many of the same messages. Customers, meanwhile, often tell us that they’re disappointed when providers fail to innovate, or fail to alert customers to innovative technologies and developments. One way larger IT services vendors create this innovation profile is through cloud ecosystems, either by acting as an ecosystem leader themselves – often through acquiring smaller cloudbased companies – and/or by ensuring they have an extensive network of alliances and partnerships. These ecosystems can include technology development, gotomarket, and joint sales components. In some cases vendors are using these ecosystems for access to an array of cloud services from a variety of providers – services that those providers can then offer to their customers in a hybrid deployment model. Some ecosystems center on the establishment of cloud standards, with one of the highestprofile examplesbeing the vendordriven OpenStack standard for IaaS deployments, which has some 150 vendor members. We’ve seen a host of cloudrelated acquisitions during the past year, mostly of smaller cloud management players by larger IT vendors, and we expect such activity to continue into 2013 as vendors attempt to cement their profile as innovators and cloud ecosystem players. We’ve also already seen evidence that many of these acquisitions are being influenced by the cloud–mobility–data nexus, with vendors acquiring various mobility management and mobile application companies, as well as analytics firms, which they then attempt to tie into their cloud marketing and messaging. Vendors in tandem are also starting to open centers of excellence and development sites that are focused on how cloud, mobility, and analytics converge. These centers can provide another showcase for a vendor’s innovation, and we anticipate even more will be launched early in 2013.

RECOMMENDATIONS

Recommendations for enterprises

Customers are realizing that cloud is becoming a permanent part of enterprise IT. Many customers will implement cloud at first as a tactical point solution with the goal of achieving immediate cost savings. But customers can attain better value for both IT and business if they realize the longerterm strategic value cloud services can deliver if done right. This is not an either/or proposition: customers can use cloud tactically and strategically if they have proper components in place related to cloud strategy, governance, procurement, and integration. CIOs and IT managers have always walked a thin line between dealing with issues in the hereandnow while thinking the long thought. Maintaining that balance is critical when it comes to realizing the full potential of cloud services. The good news for customers is that there’s no shortage of potential IT services and outsourcing partners with whom to work for cloud services. While it’s not exactly a buyer’s market, vendors are eager to work on cloud engagements and are actively courting existing and new customers. Outsourcing vendors want to establish themselves as dominant cloud players to show that their corporate investments and strategy are paying off, and they want to engage with customers at all points of the cloud “lifecycle.” (Vendors are also mindful about how cloud is disrupting the annuity revenue models of traditional outsourcing, and they need to build up pipelines and customer references as fast as possible.) Customers should keep this in mind and realize, even if they have incumbent outsourcing providers, that they are approaching cloud services from a position of strength. One important consideration, not to be overlooked, is that migrating services to the cloud is as much a cultural change as an operational one. Ultimately, an enterprise’s end users may not (or should not) care from where services are delivered so long as SLAs and key performance metrics are achieved or exceeded. However, cloud services have the potential to change how modern IT shops do their jobs andmay require new skill sets and requirements. This is especially true as other trends such as mobility and analytics are increasingly connected to cloud services strategies.

Recommendations for vendors

Many IT services and outsourcing vendors are connecting their cloud services portfolios with mobility and analytics, and as this trend toward the cloud–mobility–data nexus continues, vendors will need to shore up any perceived weaknesses across those areas. Not only will portfolios potentially need to be enhanced, but sharp and differentiated marketing and messaging has never been more crucial. With this vendor rush toward the nexus, there is a degree of sameness emerging among large providers’ cloud services marketing. While some of that is to be expected, vendors that fail to focus their messaging will find it harder to differentiate. Some differentiation may come from cloud services security, but vendors shouldn’t count on this to be the key decisionmaking factor when competing for customers. Customers have come to expect that vendors as a matter of course will provide the necessary layers of security when planning or deploying cloud services. Security is extremely important and a major influence on what workloads customers put into the cloud, but security alone will not seal the deal for any vendor. Tailoring cloud services marketing to specific verticals may provide a better path to differentiation, as customers in some verticals have specific regulatory and compliance requirements that must be met. As cloud cements itself as part of modernday corporate IT, many vendors are turning to cloud ecosystems, cloud acquisitions, and cloud centers of excellence as ways to demonstrate innovation. All of these can contribute to an innovation profile, but ultimately customers may come to view innovation as whatever affords them the greatest amount of choice in deciding how to leverage cloud services. Some customers are viewing cloud services with a wary eye; they’re concerned that cloud has the potential to lead them down the path of vendor lockin, a hallmark of the early days of outsourcing “megadeals.” Customers will chafe at anything that denies them flexibility, automation, transparency, and choice in cloud services deployments.APPENDIX

Further reading

TSystems and Cloud 7.0: Driving Cloud Services from its Legacy Heartland (August 2012) HP Puts Choice at the Center of Cloud Services Strategy (July 2012) Cloud Services Business Trends Survey: Focus on the UK Market (June 2012) Cloud Services Business Trends Survey: Focus on the French Market (April 2012)Cloud Services Business Trends Survey: Focus on the German Market (April 2012) Drivers and Barriers for Cloud Services in Vertical Markets (April 2012) Cloud Services Business Trends Survey: Focus on the US Market (January 2012) Cloud Services Business Trends Survey: Summary Results (January 2012)