Produced by: RBS Morgans Limited

Equity | Australia | Metal

s

& Mining

10

Diggers & Dealers 2011

Our Top 5 Diggers

Key Themes from Diggers: Everyone loves small-mid caps. Overwhelming attention was focussed on the producers who are either a) about to produce such as BDR, YTC, SFR, b) increasing production: RRL, IGO, SAR or c) Corporate targets for raisings which was almost everyone in the room.

Our Top 5 from Diggers (in no particular order)

Beadell Resources (BDR) – Upside in the iron ore potential?

Peter Bowler (the crafty veteran) alluded to BDR currently having a chat with Anglo in regards to the iron ore. He believes they have the potential to delineate “significant” resources of iron ore at Amapa and could perhaps go it alone. According to Peter this could be bigger than the gold project. It’s not a done deal, but when have you known Mr Bowler to not deliver on something.

Saracen Minerals (SAR) – 160koz in the wings if they can pull it together – BEST PICK SAR has 17 different resources, 2 main projects, underground and open pit development and is throwing out 111kozpa at ~$680/oz production cost. SAR intends spending $25m on exploration in the next 12 months to develop Red October. Aiming for production of 160kozpa by 2015. Potential takeover target as well as an acquisitor in the short term. Alacer Gold (AQG) – 800kozpa by 2015!

Q2 highlights – 101,000 oz production - Cash operating cost - $542/oz. Commercial production achieved at Copler In turkey in April 2011. Huge exploration potential upside at Copler with 800,000ozpa production anticipated from the group by 2015. Highly attractive growth profile.

YTC Resources (YTC) – Nymagee copper looks good and getting better

YTC has two projects – Hera their advanced pre-production gold project with a DFS due in 4 weeks, and Nymagee and advanced copper exploration project with some cracker-jack copper grades at depth and a maiden resource due in a month or two.

Sandfire Resources (SFR) – All is tickety-boo at DeGrussa - BUY PT $8.28

Mining and earthworks are progressing on time and budget at DeGrussa. Open pit mining has commenced with Mill parts due in November & February. Construction is on time (if not a little bit ahead of schedule). Exploration is complicated but there’s lots of smoke out there for the brains at SFR to figure out. Any discovery will mean a significant re-rating. We maintain our BUY recommendation on the stock and price target of $8.28/share.

4th August 2011 Analysts James Wilson Australia +61 8 6462 1974 [email protected] RBS Morgans Limited (A.B.N. 49 010 669 726) AFSL235410

Best Picks

Producers:■ Saracen Minerals (SAR)

■ Alacer Gold (AQG)

Emerging producers

■ Beadell Resources (BDR)

■ Sandfire Resources (SFR)

The Keynote Speech Day 1 – Todd Buchholz

Former Reagan administration Whitehouse advisor. Director of the Tiger Hedge Fund. Todd’s talk was interesting but was more a comedy show rather than a serious economic discussion along the lines of Niall Ferguson. It was a good keynote, but it didn’t tell us anything that we didn’t already know.

China’s ageing population – the one Child policy means that China has a very old population going forward. Where’s the growth going to be in 15-20 years when a large proportion of the population is elderly?. China is in a golden era of massive economic growth – but it’s likely to hit the wall in 10-15 years because of the population issue.

China has tapped the brakes on growth – will it be gentle or perhaps something stronger. Todd feels that China will be the locomotive for growth for the next 10-15 years.

Deployment of the rescue packages – The US $800bn rescue package on infrastructure has so far resulted in only 6% being spent roads/rail etc…mainly because of political posturing and red tape. China however punted $600bn into infrastructure and almost all of it was committed immediately.

The US Job machine is broken – extended jobless benefits and the healthcare tripwire aren’t helping growth. Example of Obama’s healthcare tripwire: If you have 49 employees you don’t have to supply them with health benefits…..employee 50 and you do for every employee – so why would you think about growing your business and employing an extra person when it will trigger Obama-care!.

China.com – China.communism? Will China allow free flows or will they keep trying to contain intellectual ferment. We think that even China doesn’t know the answer to this one.

Will copper lose its pHD. Copper is often referred to as the metal with a pHD, mainly because it tracks economic growth.

Best Comment: “If you think the world’s going to end tomorrow, it’s already tomorrow in Australia”

Closing Comments: In the maelstrom or perfect storm of meltdowns and looming threats of terror – Now is the time for innovation for the future and the community. And usually innovation is borne in the darkest hour.

2011 Diggers & Dealers awards

Digger of the Year: Independence Group Ltd (IGO) – Chris Bonwick Dealer of the Year: Ivanhoe – Robert Friedland

Best Emerging new company: Gold Road (GOR)

Conference Notes

The conference was another sell-out this year. The involvement of many more big corporates is crowding the forum, as well as the increase in the number of mining services getting booths. The big thing we did notice was the big players presenting – Barrick, Anglogold Ashanti etc…but very few smaller players having presentation slots or even stands within the forum for that matter. We still remain positive on stories such as Regis Resources (RRL), Independence Group (IGO), and Fortescue Metals (FMG) but in reality these great stories really haven’t changed that much (ie they’re still great) so we tried to search out stories that perhaps didn’t get that much attention as other high-calibre picks. We’ve listed a few here in what we consider our best picks of the conference.

Alacer Gold (AQG) – 800kozpa by 2015…..Copler load of that

Q2 highlights – 101,000 oz production - Cash operating cost - $542/oz. Commercial production achieved at Copler In turkey in April 2011. Our original thoughts were Copler has significant exploration potential producing around half of the total production of the company. We feel the deposit is a diamond in the rough. Extensions to the main zone recently showed the potential of the oxide zones to expand as well as the almost untapped sulphide zones. Recent intercepts of 69m@3G/t are impressive and are still open at depth and to the east. Alacer has a very impressive 5.7 million ounces of reserves and 14.8moz of resources under the hood. Highly attractive growth profile and in my opinion are a huge takeover target with Copler as an asset. Expecting production of 800,000oz per annum from 2015. BIG!

Beadell Resources (BDR) – Iron ore might be bigger than ben-hur?

In true diggers style I managed to corner Peter Bowler for an hour as he sat next to me on the plane. He originally sold the iron ore rights for $31.25m to Anglo Pacific Group but now he’s considering an Iron ore offshoot to mine and produce iron ore from the project. Sounds like Beadell is considering going it alone with their iron ore product – recent announcements have shown the potential for iron ore along a 6km long strike at their Amapa project in Brazil. Peter reckons there may be a fairly serious iron ore potential on the project. If so this could be a very serious value-add, but as Peter said, it’s not in the bag yet so we’ll wait and see, discussions are ongoing with Anglo so there’s still risk there. Also there’s infrastructure hurdles to overcome but as I said to Peter “mate you can sell ice to the eskimo’s” and really, when has Peter not delivered on a promise?.

YTC Resources (YTC) – Nymagee looks good and getting better

YTC has two projects in the Cobar region of NSW. Their flagship project “Hera” is located in Cobar, just down the road from the CSA mine run by Glencore. Hera has a resource of ~670,000oz of gold at an 8.6g/t Au gold equivalent grade (Au+Ag+Pb+Zn). YTC should be completing their Definitive Feasibility on Hera by early September – aiming for a small $65m capex and estimated first production by late 2012 assuming they push the button.

Their second project is called “Nymagee” – a copper project around 5km from Hera (both are around 80km from Cobar). Nymagee was originally mined for copper with ~422,000t @ 5.8% Cu mined out from old underground workings. YTC has drilled below the existing workings to find mineralisation extends down nearly 500m still open at depth and along strike. Best grades have included [email protected]% Cu. Management believes that the project could be a analogue of the Glencore owned CSA mine nearby and could extend down as far as 2km like other mines (such as CSA) in the region of similar morphology.

YTC currently has 3 rigs drilling out the 1.2km long gravity anomaly at Nymagee and expects a maiden resource for the Nymagee deposit by late September this year.

Saracen Minerals (SAR) –Potential for upside surprise – site visit was impressive

We visited Saracen’s Red October and Carusoe Dam operations which are located to the NW of Kalgoorlie – and aren’t actually that far from Tropicana. Saracen bought the projects from Sons of Gwalia when they went into administration. Since then and for minimal spend SAR has built up an operation that last year produced 111koz gold at a cash cost of ~$680/oz.

Essentially SAR has around 17 historical and newly found open pits which Saracen is sourcing it’s ore from. Many of the pits are still flooded with active pits at Whirling Dervish, Karari and a few other pits. Saracen’s aim is to dewater the pits, drill for underground resources or establish the potential for cut-backs at existing pits and to increase production to >160,000ozpa by 2015. Their latest development is from Red October (which is a few km south of the massive Sunrise Dam open pit). SAR is developing a small trial underground to conduct exploration and small scale production before they commit to a larger scale operation. This is essentially an analogue for what they want to do with many of their other operations.

Alacer formed from the merger of Avoca Resources and Anatolia Minerals

Market Cap: $3.2bn

Catalysts: Negotiations (positive or negative) with Anglo on the iron ore

Market Cap: $562m

Catalysts: Hera DFS in 3-4 weeks, Nymagee Maiden Resource in 6-8 weeks.

Market Cap: $154m

If SAR can pull it all together (and we believe they can, but this is the risk) then this producer is VERY undervalued given the resources upside in the mineral inventory.

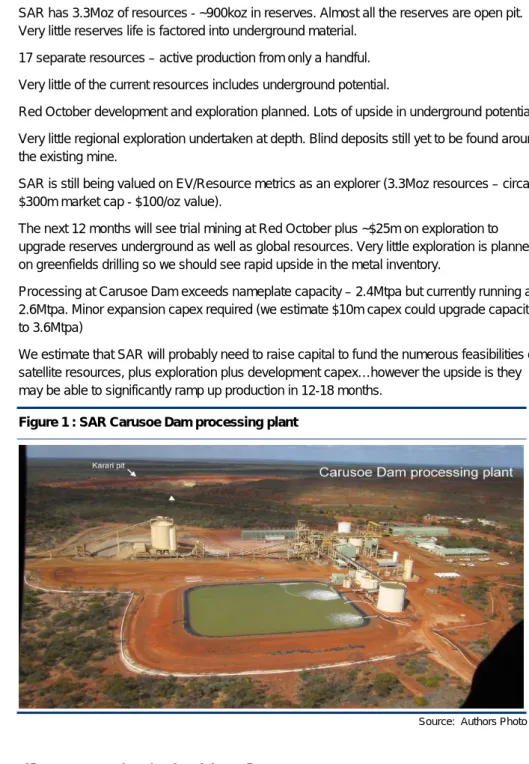

■ SAR has 3.3Moz of resources - ~900koz in reserves. Almost all the reserves are open pit. Very little reserves life is factored into underground material.

■ 17 separate resources – active production from only a handful.

■ Very little of the current resources includes underground potential.

■ Red October development and exploration planned. Lots of upside in underground potential.

■ Very little regional exploration undertaken at depth. Blind deposits still yet to be found around the existing mine.

■ SAR is still being valued on EV/Resource metrics as an explorer (3.3Moz resources – circa $300m market cap - $100/oz value).

■ The next 12 months will see trial mining at Red October plus ~$25m on exploration to upgrade reserves underground as well as global resources. Very little exploration is planned on greenfields drilling so we should see rapid upside in the metal inventory.

■ Processing at Carusoe Dam exceeds nameplate capacity – 2.4Mtpa but currently running at 2.6Mtpa. Minor expansion capex required (we estimate $10m capex could upgrade capacity to 3.6Mtpa)

■ We estimate that SAR will probably need to raise capital to fund the numerous feasibilities on satellite resources, plus exploration plus development capex…however the upside is they may be able to significantly ramp up production in 12-18 months.

Figure 1 : SAR Carusoe Dam processing plant

Source: Authors Photo

Sandfire Resources (SFR) –Site Visit confirms progress Recommendation: Buy PT: $8.28

We visited Sandfire’s DeGrussa project prior to Diggers and Dealers with ~72 visitors Key Points

■ Decline development at the Evans decline is a little ahead of schedule at 150m – a further 950m development Is still to be completed before first ore stopes are intercepted. This is anticipated in 2H CY2012. Ground conditions are still somewhat fractured due to the oxidised nature of the rock but everything is being bolted with no glaring rock stability issues from where we stood.

■ Open pit ore is being mined – current ore zones are low grade gold lodes in the laterite / saprolite which equates to ~30,000t @ 1.2g/t Au.

We are still happy with the SFR story and maintain our $8.28 price target. Significant upside will come from any exploration discovery

per 85t truck).

■ Construction is underway for camp, plant sites. Bulk earthworks for the mill site are underway, the mill is on schedule for a February 2012 delivery (SAG and Ball Mill’s arrive then). Float circuit components arrive in November and so far everything is either slightly ahead or on schedule with no issues that we could see.

■ Gas power – no facility for gas power with the current load on the gas pipeline fully committed – but SFR has the ability to switch power at the on site power station relatively easily if capacity comes on stream. A simple switch out could be a good cost saver for SFR down the track.

■ Exploration: Lots of interesting zones being discovered but a muted response to exploration upside. Recent discoveries of a 300m long zone of malachite a few hundred meters north of the pit are more confusing than exciting – seems structural controls on geology are quite complex. This isn’t a downside but there still remains a lot of work for SFR geologists to do and additional discoveries will come from internal brain-power (which they have in spades) rather than blind scatter-gun drilling.

Figure 2 : DeGrussa Open Pit Mining (ore zones being mined in upper part of photo)

Source: Authors Photo

Figure 3 : DeGrussa Portal and Underground drive development

www.rbsmorgans.com

DISCLAIMER - RBS MORGANS LIMITED

The information contained in this report is general advice only, and is made without consideration of an individual’s relevant personal circumstances. RBS Morgans Limited ABN 49 010 669 726, its related bodies corporate, directors and officers, employees, authorised representatives and agents (“RBS Morgans”) do not accept any liability for the results of any actions taken or not taken on the basis of information contained in this report, or for any errors or omissions contained within. It is recommended that any persons who wish to act upon this report consult with their RBS Morgans investment adviser before doing so. Those acting upon such information without advice do so entirely at their own risk.

This report was prepared as private communication to clients and is not intended for public circulation, publication or for use by any third party. The contents of this report may not be reproduced in whole or in part without the prior written consent of RBS Morgans. While this report is based on information from sources which RBS Morgans believes are reliable, its accuracy and completeness cannot be guaranteed. Any opinions expressed reflect RBS Morgans judgement at this date and are subject to change. RBS Morgans is under no obligation to provide revised assessments in the event of changed circumstances. This report does not constitute an offer or invitation to purchase any securities and should not be relied upon in connection with any contract or commitment whatsoever.

DISCLOSURE OF INTEREST

RBS Morgans may from time to time hold an interest in any security referred to in this report and may, as principal or agent, sell such interests. RBS Morgans may previously have acted as manager or co-manager of a public offering of any such securities. RBS Morgans' affiliates may provide or have provided banking services or corporate finance to the companies referred to in the report. The knowledge of affiliates concerning such services may not be reflected in this report. RBS Morgans advise that it may earn brokerage, commissions, fees or other benefits and advantages, direct or indirect, in connection with the making of a recommendation or a dealing by a client in these securities. Some or all of our Authorised Representatives may be remunerated wholly or partly by way of commission.

RECOMMENDATION STRUCTURE

For a full explanation of the recommendation structure, refer to our website at https://www.rbsmorgans.com/research_disclaimer

If you no longer wish to receive RBS Morgans’ publications please advise your local RBS Morgans office or write to RBS Morgans Limited, Reply Paid 202, Brisbane QLD 4001 and include your account details.

QUEENSLAND NEWCASTLE (02) 4926 4044

BRISBANE – HEAD OFFICE (07) 3334 4888 NEWPORT (02) 9998 4200

BRISBANE – EDWARD STREET (07) 3121 5677 ORANGE (02) 6361 9166

BUNDABERG (07) 4153 1050 PARRAMATTA (02) 9615 4500

BURLEIGH HEADS (07) 5520 8788 PORT MACQUARIE (02) 6583 1735

CAIRNS (07) 4222 0555 SCONE (02) 6544 3144

CALOUNDRA (07) 5491 5422 WOLLONGONG (02) 4227 3022

CAPALABA (07) 3245 5466

CHERMSIDE (07) 3350 9000 VICTORIA

EMERALD (07) 4988 2777 MELBOURNE – HEAD OFFICE (03) 9947 4111

GLADSTONE (07) 4972 8000 MELBOURNE – FARRER HOUSE (03) 8644 5488

GOLD COAST (07) 5592 5777 BERWICK (03) 9796 2676

IPSWICH (07) 3202 3995 BRIGHTON (03) 9519 3555

MACKAY (07) 4957 3033 CAMBERWELL (03) 9813 2945

MILTON (07) 3114 8600 CARLTON (03) 9066 3200

NOOSA (07) 5449 9511 GEELONG (03) 5222 5128

REDCLIFFE (07) 3897 3999 RICHMOND (03) 9916 4000

ROCKHAMPTON (07) 4922 5855 SOUTH YARRA (03) 9098 8511

SPRING HILL (07) 3833 9333 TRARALGON (03) 5176 6055

SUNSHINE COAST (07) 5479 2757 WARRNAMBOOL (03) 5559 1500

TOOWOOMBA (07) 4639 1277

TOWNSVILLE (07) 4725 5787 ACT

YEPPOON (07) 4939 3021 CANBERRA (02) 6232 4999

NEW SOUTH WALES SOUTH AUSTRALIA

SYDNEY – HEAD OFFICE (02) 8215 5000

SYDNEY – MACQUARIE STREET (02) 9125 1788 ADELAIDE (08) 8464 5000

SYDNEY – PHILLIP STREET - LEVEL 33 (02) 8215 5111 NORWOOD (08) 8461 2800

SYDNEY – REYNOLDS EQUITIES (02) 9373 4452

ARMIDALE (02) 6770 3300 WESTERN AUSTRALIA

BALLINA (02) 6686 4144 PERTH (08) 6462 1999

BALMAIN (02) 8755 3333

CHATSWOOD (02) 8116 1700 NORTHERN TERRITORY

COFFS HARBOUR (02) 6651 5700 DARWIN (08) 8981 9555

GOSFORD (02) 4325 0884

HURSTVILLE (02) 9570 5755 TASMANIA

MERIMBULA (02) 6495 2869 HOBART (03) 6236 9000