The Effects of Trading Suspensions in China

Full text

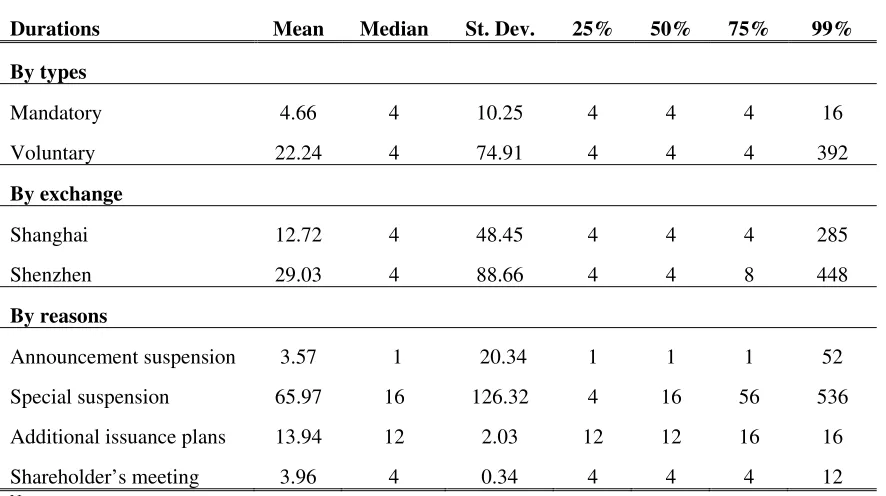

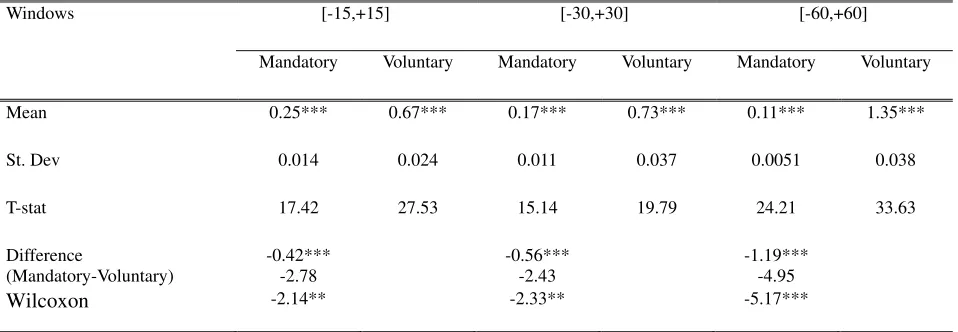

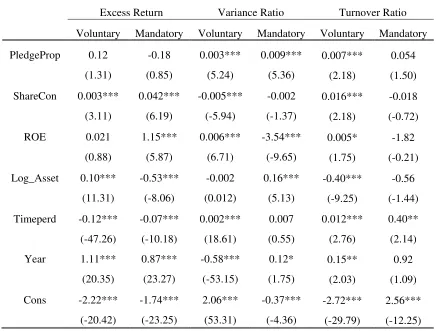

Figure

Related documents

More recent, an analysis on empirical relationship between stock return and trading volume based on stock market cycles by using daily data for Jakarta composite index closing

where L(LIST) is the log-odds ratio that a stock will be selected for option listing, VOLUME is average daily trading volume over the 250 trading days prior to the fifteenth of

In this paper the causality relationship between the trading volume and the stock returns are surveyed using the data related to 220 member companies of Tehran Stock

The dataset used in this study primarily comprises daily closing stock price index and corresponding trading volume series for the stock markets in Nordic

To evaluate dynamic relationships between stock return volatility and trading volume, we substitute the abnormal return level for the squared values of abnormal stock returns,

(2008) The Empirical Relationship between Stock Returns, Return Volatility and Trading Volume in the Brazilian Stock Market, Brazilian Business Review , Vol. (1978),

This implies that non-informational trade has a significant effect on prices and trading activity has explanatory power in addition to present returns, non - linear trading volume

This table presents annual industry-adjusted returns for portfolios based on price momentum and change in trading volume using data on NYSE0AMEX stocks from 1968 to 1995!. The