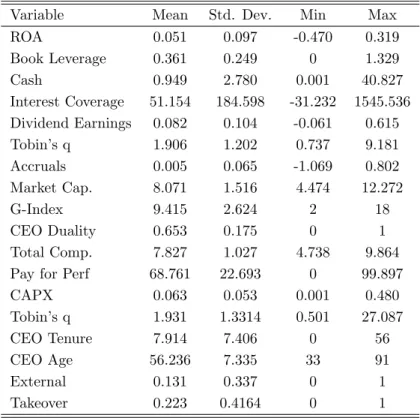

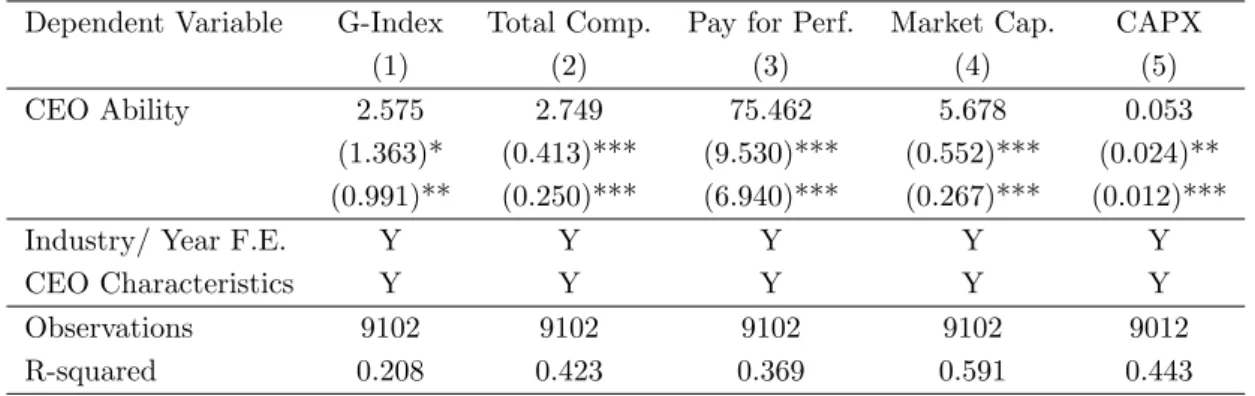

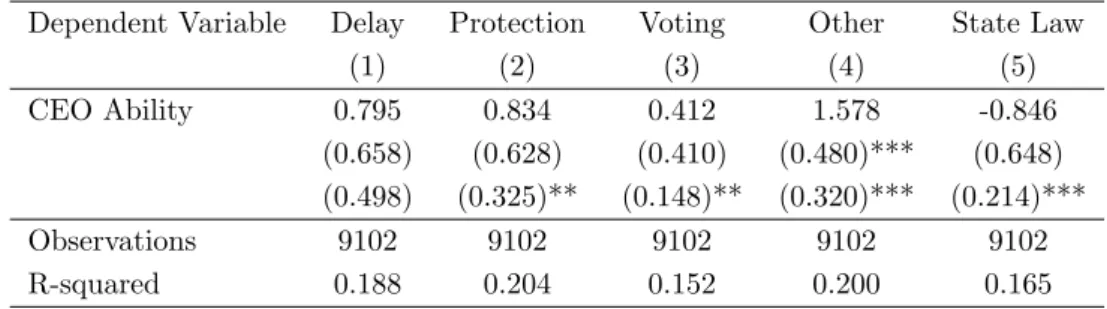

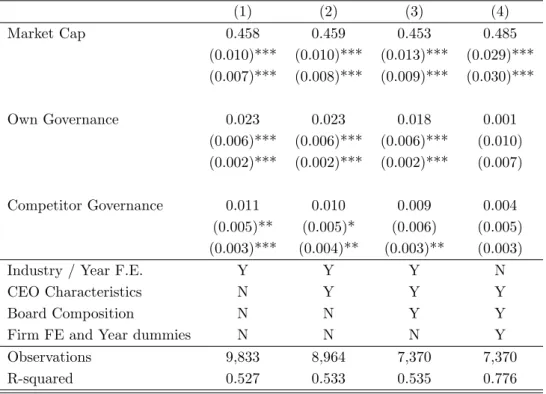

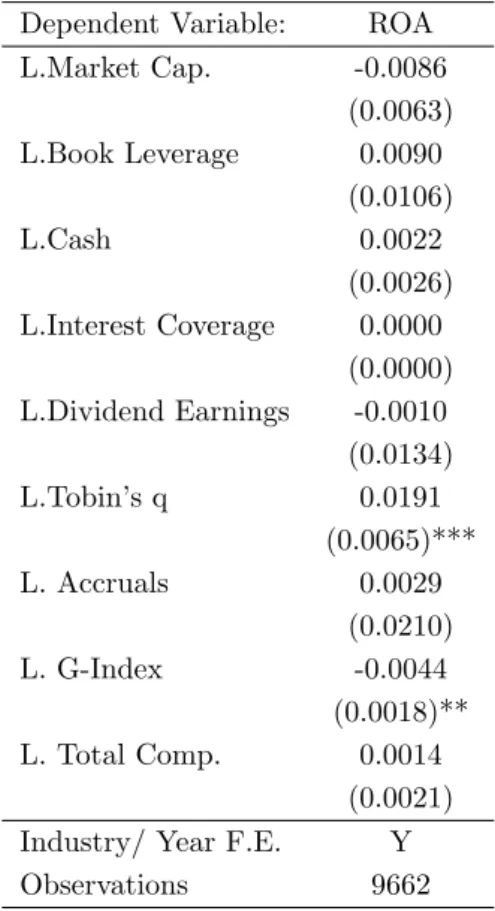

Competition for Managers, Corporate Governance and Incentive Compensation

Full text

Figure

Related documents

These samples can then be plugged into functionals of interest for systemic risk assessment, e.g., to work out the distribution of the number of banks defaulting or the probability

To explore how network externalities vary at the individual level, I use video-messaging data that tracks the adoption of 2,118 employees in a large bank and their 2.4

In particular, a declining trend in the ratio in the case of the PRC is noticeable, and this is likely to reflect a shift in the money held by the general public from cash to

Overall, it seems that some relative prices of intermediate goods may react to the accumulation of foreign exchange reserves (build up of reserves – devaluation – increase in

With this in mind, the fi eld of o ff shore wind farm layout optimization has grown to include sophisticated methodologies for the evaluation of the levelized cost of energy (LCOE) of o

comprehension (Lawrence & Snow, 2011; Nystrand, 2006) which can include the potential for follow-up questions to challenge and/or support students in the learning process

Interval comparison Interval identification Chord identification Chord inversions Chord progressions Scale identification Rhythm reading Rhythm imitation Rhythm correction

This also marked a significant development in the expansion of the family, with Sir Richard Musgrave and his three brothers John, Nicholas and William becoming