GE-International Journal of Management Research

Vol. 5, Issue 2, February 2017 Impact Factor- 5.779 ISSN(O): 2321-1709, ISSN(P): 2394-4226© Associated Asia Research Foundation (AARF)

Website: www.aarf.asia Email : [email protected] , [email protected]DATA CALLING OR VOICE CALLING: AN EXPLORATION OF

CHANGING ORIENTATIONS

Harun Marwaha1, Prof. Kingshuk Bhadury2 1

MBA Student, Symbiosis Institute of Management Studies, India. 2

Professor, Symbiosis Institute of Management Studies, India.

ABSTRACT

The Telecom industry globally has always been the one that had to deal with an everchanging business and technology environments more than any other industry over the years. Traditionally, the revenue for telecom has always been voice and messaging(SMS) services with data services emerging in the 1990s. Indian telecom industry is one of the youngest industries but has grown tremendously over the past few years, becoming second largest telecom market in 2016. Recently the telecom industry in India lost to Over-The-Top (OTT) messaging services like Whatsapp, Facebook Messenger, Hike etc. and were once again caught off guard by the Over-The-Top (OTT) voice services. The impact of OTT services telecom company’s voice and messaging services has been a fact from fiction. OTT services have caused a disruption in the mobile internet traffic over past year. With no restrictions on data calling, and piggybacking on telco’s infrastructure while eating their revenue, this study attempts to explore the change in orientation from traditional voice calling to data calling.

KEYWORDS: CHANGE, DATA CALLING, OTT, OVER-THE-TOP(OTT), VOICE

CALLING.

INTRODUCTION

Indian telecom industry, with a subscriber base of 1058.86 million till March 2016 is

currently the second largest telecom market and has been growing tremendously in the past

decade and a half. The wireless segment (97.62 per cent of total telephone subscriptions)

share of 2.4 percent. The government of India has been instrumental with their liberal and

reformist policies along with strong consumer demand has helped India become the third

highest number of Internet users in the world.

The telecom operators today strive to provide seamless and high quality voice, data and

multimedia services in a multi-device, mobile environment. Traditionally the principal

revenue streams for telecom operators have been voice and messaging (SMS) with data

coming in at a far third till recently. But while telcos had been quick to react to previous

game changing developments such as the internet explosion and the emergence of cellular

mobile communications in the 1990s, they seem to have been caught napping in the face of

the newest challenge to their revenues, Over The Top (OTT) service providers. The OTT

service providers deliver audio, video and other media over the internet and bypass the traditional operator‟s network. Since, the OTT players do not require any business or

technology affiliations with network operators for providing such services, they are often

known by the term "Over-The-Top" (OTT) applications. OTT players like Google, Facebook,

Viber Media are enabled by technology advances such as open source platforms,

smartphones, innovative services, cutting edge functionalities, super-fast IP networks and shift in consumer preferences towards their “freemium” based business models are seeing an increasing adoption rate. They do not contribute directly to telco‟s revenue but utilize the telecom operators‟ network and infrastructure. Internet is the heart and soul of these OTT

applications, they cannot survive even a second with internet service providers and telecom

operators. But the most worrying fact for the telcos is that these OTT players offer services

that are close and almost free substitutes to their own offerings and a credible and measurable

threat to their revenues. Thanks to the “freemium” based business models of these OTT players, consumer preferences have already moved from telcos‟ messaging(SMS) service to OTT players free messaging applications which again free surf on telecom operator‟s

infrastructure. Now, the impact of OTT services on telcos‟ voice revenue is a recognized

reality. Their impact on mobile data traffic and telcos data revenue are areas of key

importance as this will tell whether impact on their voice revenue can be compensated by

data revenue.

The main purpose of this project is to make people aware of the shifting trend from

traditional voice calling to data calling which is subsequently causing loss to the telecom

companies. It is due to such research work that telecom companies are now demanding

LITERATURE REVIEW

Many organizations have studied the impact of Over-The-Top(OTT) services on telecom and

internet service providers but very few have shown the shift in orientation from voice calling

to data calling. A lot of organizations have studied the impact on SMS service, due to

increasing adoption and use of OTT messaging services.

For example, according to Informa Telecoms & Media in 2013, the global annual SMS

revenues will fall by US$23 Billion by 2018, from US$ 120 Billion in 2013 to US$ 96.7

Billion by 2018. As per their forecasts, Asia Pacific is forecasted to get hit the most by the

new and innovative messaging applications in both emerging and developed markets.

Another report by Cellular Operators Association of India, the Indian telecom industry grew

only 6.5% last year, which is the lowest since 2010 even when the industry saw a growth in

active subscribers during this period. Idea Cellular Managing Director said that the industry

has seen a decline in revenue from voice calls, although the overall active subscribers

increased by 79 million but the report does not talk about the reasons due to which there is a

loss in revenue.

Global revenue survey conducted by Ernst & Young in 2013 suggested that data would eat

into higher voice and SMS margins. As per the survey, significant increase in data traffic has

been projected and rise in contribution of data to telco revenue mix will result in lower

overall margins for telcos and potential revenue cannibalization would occur due to the free

data-centric Over The Top (OTT) applications.

Shanthi (2005)[1] throws light on the telecommunications market of India – post privatization.

In the scenario of falling prices, hyper-competition and increasing attrition rates and the

author says that identifying possible churn before it actuallyhappens, enables telcos detect

and control churn. The author provides a predictive churn model for telecom segment, to

allow a qualitative insight for understanding the structure and methodology of churn

management in the Indian telecom sector, and discusses the level of applicability of such

models in the Indian context.

Bepko[2] (2000) says that among the areas which need to be addressed in service quality

research is the nature of consumer expectations across the range of intangibility. Previous research had compared consumers‟ service quality expectations across services, but different

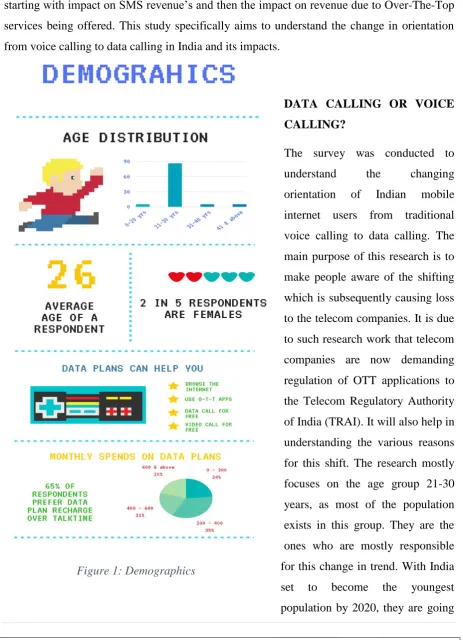

Figure 1: Demographics

for the significant differences in expectations of quality. The paper used a controlled,

repeated measures design where subjects were each asked to evaluate three services, varying

in their degree of intangibility, over a ten-week period.

The literature reviewed above indicates impacts on revenue of telecom industry globally, starting with impact on SMS revenue‟s and then the impact on revenue due to Over-The-Top

services being offered. This study specifically aims to understand the change in orientation

from voice calling to data calling in India and its impacts.

DATA CALLING OR VOICE

CALLING?

The survey was conducted to

understand the changing

orientation of Indian mobile

internet users from traditional

voice calling to data calling. The

main purpose of this research is to

make people aware of the shifting

which is subsequently causing loss

to the telecom companies. It is due

to such research work that telecom

companies are now demanding

regulation of OTT applications to

the Telecom Regulatory Authority

of India (TRAI). It will also help in

understanding the various reasons

for this shift. The research mostly

focuses on the age group 21-30

years, as most of the population

exists in this group. They are the

ones who are mostly responsible

for this change in trend. With India

set to become the youngest

to be the driving force for changing trends.

1. Easy adaptability to technology:

From the survey that was conducted, most of the respondents are comfortable with adapting

to new technology which is major drive of changing orientation from data calling to voice calling. With more new and innovative “freemium” applications coming in the market, data

calling can be the new trend in the

Indian telecom market.

2. Age vs Data Calling usage:

As per the survey, almost 70% people

use data calling, irrespective of the

age. Though most of the distribution

is between the age 20-30 years, but as

shown in the previous point it can

already be seen that adaptability to

technology is irrespective of the age.

This survey shows the change in trend

from voice calling to data calling.

Also, the rise in usage of data calling

is mostly due to Over-The-Top

players providing multiple

functionality, international calling

without any extra charges. For

example, Whatsapp, Skype, Hike and

Viber provide messaging and voice

calling along with video calling. All

three of them have easy to use

interface, free of charge and provide

multiple functions. With deep

penetration of Whatsapp in India

(96% of smartphone owners use it), it

is surely leading the way in changing

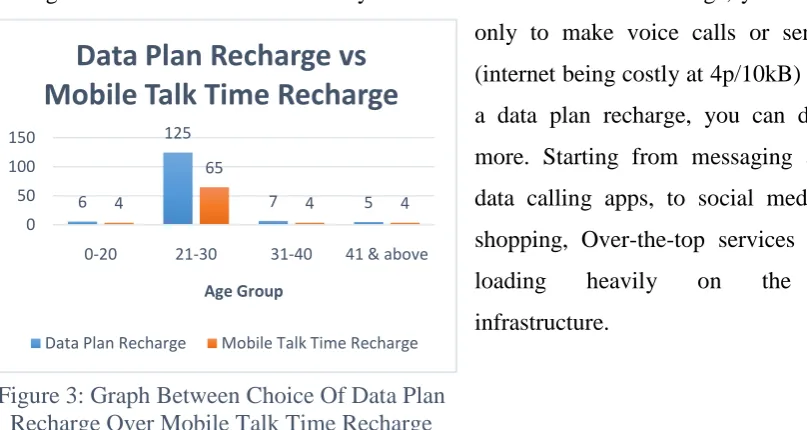

[image:5.595.266.525.203.703.2]Indians from using traditional voice

6 125 7 5 4 65 4 4 0 50 100 150

0-20 21-30 31-40 41 & above

Age Group

Data Plan Recharge vs

Mobile Talk Time Recharge

Data Plan Recharge Mobile Talk Time Recharge

calling to data calling.

Siddhartha‟s father, Mr. Kumar, wanted to learn how to use WhatsApp. He reached out to his

son Siddhartha who readily agreed to help his father. Siddhartha took out his fancy

smartphone and taught his father how to use WhatsApp and how to call using WhatsApp.

Such ease and flexibility left his father surprised and that is how Mr. Kumar was introduced

to the world of OTTs and since then Mr.Kumar, how so ever aged he may be, has never

looked back or turned to that traditional voice calling and switched to data calling.

3. Data Plan Recharge vs Mobile Talk Time Recharge

Out of 220 respondents, 65% said that they prefer data plan recharge over a mobile talk time

recharge. The reason for this is mostly that with mobile talk time recharge, you can utilize

only to make voice calls or send SMS

(internet being costly at 4p/10kB) but with

a data plan recharge, you can do much

more. Starting from messaging apps, to

data calling apps, to social media apps,

shopping, Over-the-top services are free

loading heavily on the telcos

infrastructure.

Siddhartha usually reached out to his father, Mr. Kumar for his monthly recharge of Rs. 400

for talk time recharge and Rs. 295 for data plan recharge to purchase for his monthly mobile

spends. But this month, he asked for a change in the monthly spend, he only asked for Rs.

400 for internet pack as he can now call using his mobile internet data plan. Siddhartha

figured out that with more internet data, he can do a lot more like use his data for calling,

messaging, games, videos etc. but with the mobile talk time recharge he can only use it for

calling and messaging. By recharging only his internet pack, he saved more and could use his

smartphone to larger extent.

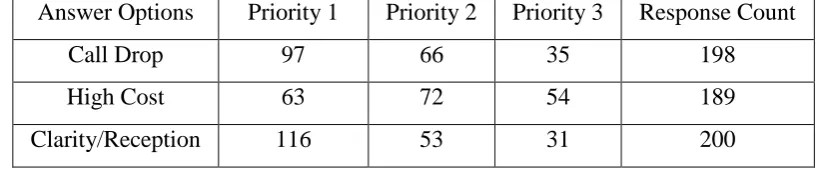

4. Issues with voice calling leading to this change:

TRAI‟s benchmark for call drops is <= 2% i.e., in 100 calls only two calls or lesser can drop.

Unfortunately, this is not the case and lot of calls are dropped every day. VoLTE or data

[image:6.595.79.483.250.465.2]calling is a viable solution to the call drop issue. So, if you have a stable wireless connection

or a good internet connection on your mobile phone, data calling is the best possible way to

connect over voice. With LTE offering more benefits in terms of spectral efficiency (VoLTE

has up to three times more voice and data capacity than 3G UMTS and up to six times more

than 2G GSM), telcos can opt for faster migration. This would also mean larger Capex but in

the longer run, with unprecedented levels of data usage growth in India, the bets can pay off.

Additionally, VoLTE deployment would mean no need to maintain legacy voice networks.

Affordability and call charges on voice calling is another issue. OTT apps like Whatsapp,

Skype and Hike pose a great threat to the revenue and there has been no change in the

charges of either mobile talk plans or data plans. But on further analysis, charges for using a

data plan for a minute of call (Consumes 0.5 MB of data) is about 10p but a standard call

[image:7.595.86.495.304.389.2]charge is 50p per minute.

Table 1 : Problems Faced During Voice Calling

Answer Options Priority 1 Priority 2 Priority 3 Response Count

Call Drop 97 66 35 198

High Cost 63 72 54 189

Clarity/Reception 116 53 31 200

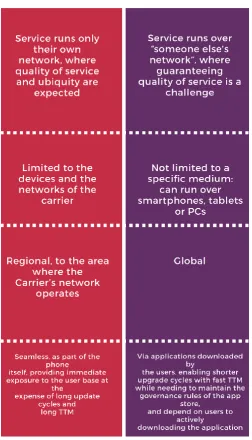

5. OTT Services vs Telecom Services:

The ability to do more with OTT services, the adaptability to new and changing technology

has been the driving force for changing trends in India. India has the third largest scientific

and technical work force in the world. This demographic bonus should continue for several

decades before India starts aging and it can make the real difference in changing orientations

59.9%

41.9%

80.2%

34.2% 38.3%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0%

Response Percent

Data Calling Expectations

[image:9.595.90.513.40.180.2]Affordability Data Consumption Connectivity Privacy Convenient

Figure 5: Operators vs OTT Players

6. Pre-paid plans vs Post-paid plans:

2016 saw India, a developing country, overtake US, a developed country, to become World‟s

2nd largest smartphone market, just behind China. This major milestone was breached in

February this year, when total smartphone user base swelled to 220 million by the end of

2015; and is right now 250 million. According to Nielsen, a global information and

measurement company, 84% of all smartphone owners and 92% of feature phone owners in

India have prepaid connections. Out of the 84% smartphone owners, a majority of them

prefer data plans that have a fixed monthly charge for limited amount of data usage. This is

majorly due to a tight budget and lack of steady income. More number of prepaid subscribers

means that they can easily shift their monthly spends of talk time plans to data plans and vice

versa.

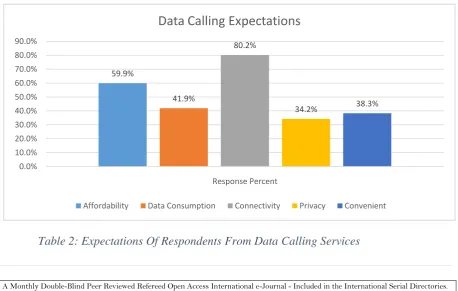

[image:9.595.72.531.487.778.2]7. Data Calling Expectations:

Most of the respondents chose connectivity (80.2%) as the top expectation from data calling

and then came affordability (59.9%). With the current infrastructure of internet services in

India, bridging the gap between expectation and reality can be tough.Fulfilling the

expectations of customers can be tough for OTT players for voice calls as they do not have

anetwork infrastructure of their own and rely totally on the telecom company for the same.

Neither has there been a major change in charges of internet plans in the past 2 years, so the

data calling expectations are still far from being fulfilled. But to compensate for the loss of

voice calls, telecom companies can surely improve their infrastructure of internet services

and increase the internet usage of mobile users.

8. Government rules and regulations (TRAI):

TRAI has been in tandem with the telecom companies as well as the consumers. In order to

favour the telecom companies, they have not asked them to decrease the data plan charges or

push more money towards network development. They also favoured net neutrality so that

OTT services provided by big and small companies remain at the same level. TRAI and

Department of Telecom (DoT) is also helping this change in orientation from voice calling to

data calling, they recently gave clearance to Whatsapp and other data calling applications to let the user‟s call landlines. In a letter from COAI to DoT, Vodafone and Airtel asked to ban

calling apps but as there are no rules and regulations in place for OTT apps, there has been no

violation by calling apps.

CONCLUSION

From the study, we could find out various reasons and choice of data calling apps over

traditional voice calling in India. The orientation change in India is real and it is to an extent

affecting telecom revenues as well. With high penetration of Whatsapp in India, adaptability

of consumers to technology, high spending of consumers on data plans, high prepaid

subscriber base, the change from voice calling to data calling is easier and better for

consumers. The obstacle is the network infrastructure in India. Telecom companies are

already struggling with inadequate coverage, overloaded cell towers, spectrum shortage,

issues with switching between towers, technical failures leading to low call quality, frequent

call drops. These same issues are being faced by data calls as well, but once you have a stable

internet connection via 2G, 3G or Wi-Fi on your smart phone, you can enjoy the benefits of

data calls. Data calls are surely cheaper than voice calls and Over-The-Top applications

rules and regulations as of now globally, whereas network carriers have to follow rules and

regulations setup by TRAI and other regulatory bodies. India is set to become the youngest

country by 2020, this change in demographics makes India more adaptable to everchanging

upgrades and new features that OTT services provide. This change in orientation from voice

calling to data calling can also see the onset of a major war between OTT players (Facebook,

Google, Hike) and Telecom Service Providers (Airtel, Reliance, Vodafone).

REFERENCES

Journal Papers

1.Shanthi N.M. (2005), „Effectiveness of Predictive Churn Models for sustaining market

share in telecom industry – An Appraisal‟, ICFAI Journal of Services Marketing, September 2005.

2. Bebko and Charlene Pleger (2002), „Service Intangibility and Its Impact on Consumer Expectations of ServiceQuality‟, Journal of Service Marketing, Vol. 14, No. 2, pp. 9-26.

Books

Pravin Prashant (2004), ‘10 Years of Change: Dialing in Change’ - Voice and Data. Pratibha B. Munot (2002), ‘Study of Telecommunications Structure in India’ (Oklahoma State University, M.S. inTelecommunication Management Program)