NOT FOR PROFIT

FINANCIAL REPORTING GUIDE

© New Zealand Institute of Chartered Accountants

This document is copyright. Apart from any fair dealing for the purpose of private study, research, criticism, or review, as permitted under the Copyright Act, no part may be reproduced by any process without written permission. Inquiries should be addressed to the publisher.

Published August 2007 by:

New Zealand Institute of Chartered Accountants 40 Mercer Street

PO Box 11 342 Wellington New Zealand

The New Zealand Institute of Chartered Accountants

The New Zealand Institute of Chartered Accountants represents the interests of nearly 29,000 members of the accounting profession working in New Zealand and around the world. It upholds the highest levels of responsibility and trust vested in the profession, by providing appropriate standards, policies and services to support members in their work.

Those intending to become Chartered Accountants, Associate Chartered Accountants or Accounting Technicians are required to achieve prescribed academic and professional standards before being admitted to the Institute. All members must comply with a rigorously enforced Code of Ethics and undertake continuing education to ensure they are up to date with best business practices and information.

Financial reporting, professional and auditing standards are prepared by the Institute of Chartered Accountants and followed by its members to ensure the credibility of information used by decision-makers in business and the capital markets. The Institute of Chartered Accountants also takes a leading role in working with government and policy-makers to advocate for more efficient taxation and commercial laws that promote the interests of New Zealand.

For further information about the Institute, visit www.nzica.com

About this report

This Guide has been prepared by the Public Benefit Entity working group, a sub-committee of the Financial Reporting Standards Board of the Institute. It is intended to be used in conjunction with the model financial statements and disclosure checklist for not-for-profit entities that are reporting in accordance with New Zealand equivalents to International Financial Reporting Standards.

Disclaimer

This publication has been prepared for the New Zealand Institute of Chartered Accountants by the Public Benefit Entity working group. It is intended to assist members of the Institute involved in preparing or auditing general purpose financial statements for not-for-profit entities that are reporting in accordance with New Zealand equivalents to International Financial Reporting Standards. Whilst every effort has been made to ensure that it reflects current legislation and financial reporting standards relevant to not-for-profit entities, neither the Institute nor any members of the working group shall be liable on any ground whatsoever to any party in respect of decisions or actions they may take as a result of using this publication nor in respect of any errors in, or omissions from it. The information contained in this publication is a general commentary only and should not be used, relied upon or treated as a substitute for specific professional advice. Whilst the Institute encourages members to use this Guide in working for or with not-for-profit entities, it will be the sole obligation of the member concerned to ensure that the member complies with the member’s wider professional and legal obligations.

FOREWORD

The New Zealand Institute of Chartered Accountants (the Institute) has published this Guide to assist members of the Institute who prepare financial statements for not-for profit entities, advise not-for-profit entities on financial reporting issues or audit the financial statements of not-for profit entities. Its focus is on small to medium not-for-profit entities with relatively simple operations, but it may be a useful starting point for larger not-for-profit entities or those with more complex transactions.

Financial statements are frequently the main source of financial information for members and others interested in the financial performance of a not-for-profit entity. The Institute believes that the users of the financial statements of a not-for-profit entity are entitled to high quality financial reporting and acknowledges that not-for-profit entities can experience significant challenges in providing these. The Institute has prepared this Guide to help members improve the quality and consistency of information in not-for-profit financial statements.

Financial statements play an important role in demonstrating accountability for the use of resources. The Institute considers that financial accountability is best demonstrated by general purpose financial statements prepared in accordance with generally accepted accounting practice in New Zealand.

The Institute’ Code of Ethics requires that members of the Institute who are involved in, or have responsibility for, the preparation and presentation of general purpose financial statements and non-financial statements (for example, as an employee, an external advisor or a volunteer) should take all reasonable steps within their power to ensure that generally accepted accounting practice is complied with.

This Guide is intended to make it easier for members to identify and understand the requirements of New Zealand equivalents to International Financial Reporting Standards in respect of small or medium not-for-profit entities. It outlines the key requirements of standards that are relevant to the majority of small to medium not-for-profit entities with relatively simple operations, and discusses other financial reporting issues that are particularly relevant to such entities. It does not cover all financial reporting standards. For example, it does not explain the detailed financial reporting requirements for foreign currency transactions, financial instruments or the acquisition or disposal of other entities. This Guide does not establish new or additional authoritative requirements and is not a substitute for reference to the standards themselves.

The Institute intends to update the Guide from time to time.

I am confident the Guide will be a valuable tool for members involved in the preparation, presentation, or audit of the financial statements of not-for-profit entities.

Denise Bovaird President August 2007

Contents

Chapter 1 – Introduction 1

Chapter 2 – Reporting Entity 11

Chapter 3 – Financial Reports 17

Chapter 4 – Assets and Liabilities: Statement of Financial Position 21

Chapter 5 – Income and Expenses: Statement of Financial Performance 46

Chapter 6 – Statement of Changes in Equity 61

Chapter 7 – Cash Flow Statement 63

Chapter 8 – Notes 66

Chapter 9 – Statement of Service Performance 74

Glossary 78

Appendix 1: List of Pronouncements 87

Appendix 2: Framework for Differential Reporting 90

Appendix 3: Review Engagements 93

Appendix 4: New Zealand Application Guidance: When is an Entity a Public Benefit Entity? 97

Appendix 5: Accounting Policies 104

Chapter 1 – Introduction

Key points

• This Guide is intended to help members of the Institute who are involved in, or have responsibility for, the preparation and

presentation of general purpose financial statements of small to medium not-for-profit entities with relatively simple operations. It is also intended to help members auditing such statements.

• This Guide assumes that entities are reporting in accordance with New Zealand equivalents to International Financial Reporting

Standards (NZ IFRSs). At the time of writing, entities are required to adopt NZ IFRSs for annual periods beginning on or after 1 January 2007. Early adoption is permitted. However, the timing of adoption is under review. Entities are advised to check current requirements.

• The Institute’s Code of Ethics requires that members of the Institute who are involved in, or have responsibility for, the

preparation and presentation of general purpose financial statements and non-financial statements should take all reasonable steps within their power to ensure that generally accepted accounting practice (GAAP) is complied with.

• The Guide focuses on financial reporting by small to medium not-for-profit entities such as clubs and societies, sports groups,

churches, and charities. It is not intended for large entities or those with complex operations. A small to medium entity meets two or more of the following criteria:

− total income under $20 million; − total assets of less than $10 million; and − fewer than 50 full-time equivalent employees.

An entity may exceed one of these criteria and still be classed as small or medium.

• Although the Guide has been written primarily for members of the Institute, it may also be useful to others with an interest in

financial reporting issues relevant to small to medium not-for-profit entities.

• This chapter explains how to identify an entity’s reporting requirements. An entity’s reporting requirements may be set out in

legislation, regulations, common law, the entity’s constitution or contractual arrangements.

• Financial reporting standards are the main element of GAAP. They state what information must be shown in general purpose

financial statements, the general requirements for the presentation of financial information and the treatment of specific items.

• The Guide assumes that the small to medium not-for-profit entities on which it focuses qualify for differential reporting

concessions (exemptions to the full requirements of financial reporting standards). This chapter explains how an entity qualifies for differential reporting concessions.

• Information provided in the Guide is not, and should not be treated as, financial reporting advice on the interpretation of

particular financial reporting standards, or their application to particular transactions, balances, circumstances or entities.

Some important terms

Here are some definitions or explanations which may be helpful to keep in mind as you read this Guide. Please note that some of these definitions or explanations have been simplified for the purposes of this Guide. There is a full Glossary at the back of the Guide, which contains definitions of these and many other terms.

Financial reporting standards are documents that state what must be shown in general purpose financial statements, the general requirements governing the presentation of financial information and the treatment of specific items for accounting purposes. Financial reporting standards are approved by an independent body, the Accounting Standards Review Board.

Generally accepted accounting practice (GAAP) is the term used to describe the basis for preparing general purpose financial statements. The term includes both the broad concepts and principles to be used in preparing general purpose financial statements and the specific practices and procedures to be used when reporting on particular transactions and events. The key aspect of GAAP is compliance with appropriate financial reporting standards. A more detailed explanation of GAAP is included in this chapter.

General purpose financial statements are statements provided to meet the information needs of external users who are unable to require or contract for, the preparation of special reports to meet their specific information needs. The general purpose financial statements of a not-for-profit entity are prepared for members, supporters, contributors and anyone else who is not able to obtain special purpose financial statements for their own specific needs.

General purpose financial reports are financial reports that may include general purpose financial statements, non-financial statements and supplementary information.

For the purposes of this Guide, a not-for-profit entity1 is a public benefit entity that is:

• organised, to the extent that it can be separately identified;

• not-for-profit2 and does not distribute any surplus that may be generated to those who own or control it;

• institutionally separate from the Government (that is, private); • self-governing, that is in control of its own destiny; and

• non-compulsory, that is membership and participation are voluntary.

A public benefit entity is a reporting entity whose primary objective is to provide goods or services for community or social benefit and where any equity has been provided with a view to supporting that primary objective rather than for a financial return to equity holders. Guidance on assessing when an entity is a public benefit entity is set out in an Appendix to NZ IAS 1 Preparation and Presentation of Financial Statements. This Appendix is reproduced as Appendix 4 to this Guide.

A small to medium entity meets two or more of the following criteria:

• total income under $20 million; • total assets of less than $10 million; and • fewer than 50 full-time equivalent employees.

These criteria are used in NZ IFRSs to distinguish between large and other entities. Other criteria may be used by bodies such as the Charities Commission.

Special purpose financial reports are financial reports tailored to meet the specific information needs of a particular user. Financial statements included in special purpose reports may be prepared using different accounting policies than would be used for general purpose financial statements, or the statements themselves may differ from those in general purpose financial statements.

Who should read this Guide?

1.1 The Guide is intended to help members of the Institute who are involved in, or have responsibility for, the preparation and presentation of general purpose financial statements of small to medium not-for-profit entities with relatively simple operations. It is intended to help members meet their professional obligation to take all reasonable steps within their power to ensure that generally accepted accounting practice (GAAP) is complied with. This obligation is set out in the Institute’s Code of Ethics. It is also intended to help members auditing such statements. Members may assist not-for-profit entities as employees, board members, external advisers or in a voluntary capacity. The Guide is intended to help members by identifying the most common aspects of GAAP in relation to small to medium-sized not-for-profit entities reporting in accordance with NZ IFRSs.

1.2 Although this Guide has been written mainly for members of the Institute, it may also be useful to others with an interest in financial reporting issues relevant to small to medium not-for-profit entities.

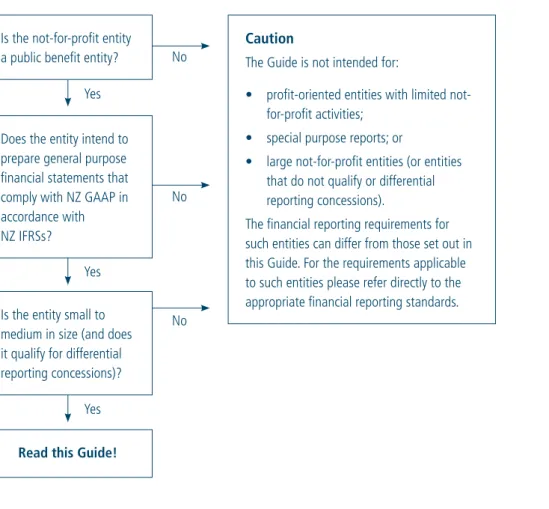

1.3 The following flow chart indicates when this Guide is likely to be useful.

1These characteristics of not-for-profit entities are taken from Counting Non-profit Institutions in New Zealand, Statistics New Zealand, 2005.

2Statistics New Zealand classifies organisations as not-for-profit if they make profits but any surplus is ploughed back into the basic mission of the organisation and not distributed

to the owners, members, founders or governing board. An entity distributing a surplus to another not-for-profit institution is still a not-for-profit institution under the Statistics New Zealand not-for-profit criterion because the surplus remains within the not-for-profit sector to be used for charitable and other not-for-profit purposes (refer to Identifying Non-Profit Institutions in New Zealand, Statistics New Zealand, April 2006).

FIGURE 1: WHEN TO USE THIS GUIDE

What this Guide covers

1.4 This Guide outlines the key requirements of GAAP under NZ IFRSs in relation to the general purpose financial

statements3 of small to medium not-for-profit entities. The Guide assumes that entities are reporting in accordance with

NZ IFRSs. At the time of writing, entities are required to adopt NZ IFRSs for annual periods beginning on or after 1 January 2007. Early adoption is permitted. However, the timing of adoption is under review. Entities are advised to check current requirements. The Guide also discusses what to do when there is no financial reporting standard that covers a particular type of transaction.

1.5 The Guide explains the most common transactions and events and the resulting assets, liabilities, income and expenses of small to medium not-for-profit entities. It provides only a brief overview of the treatment of financial instruments and does not deal with a number of more specialised topics such as foreign currency transactions or the acquisition or disposal of other entities. Appendix 1 to this Guide lists the standards current at the time of writing and explains the extent to which they are covered by the Guide. Individual chapters also indicate which issues are not covered by the Guide. Where entities have transactions and events not covered by this Guide, members will need to refer directly to the relevant financial reporting standards.

1.6 Information provided in the Guide is not, and should not be treated as, financial reporting advice on the interpretation of particular financial reporting standards, or their application to particular transactions, balances, circumstances or entities. Is the not-for-profit entity

a public benefit entity?

Does the entity intend to prepare general purpose financial statements that comply with NZ GAAP in accordance with NZ IFRSs?

Is the entity small to medium in size (and does it qualify for differential reporting concessions)?

Read this Guide!

Caution

The Guide is not intended for:

• profit-oriented entities with limited

not-for-profit activities;

• special purpose reports; or

• large not-for-profit entities (or entities

that do not qualify or differential reporting concessions).

The financial reporting requirements for such entities can differ from those set out in this Guide. For the requirements applicable to such entities please refer directly to the appropriate financial reporting standards. Yes

Yes

Yes

No

No

No

What this chapter covers

1.7 In order to help members determine whether the material in this Guide is likely to be of use to them in preparing or auditing the financial statements of not-for-profit entities that are reporting in accordance with NZ IFRSs, this chapter provides an overview of the following topics:

• members’ professional obligations under the Code of Ethics; • general purpose financial statements;

• special purpose financial statements;

• GAAP (including variations in GAAP for different types of entities); and

• identifying the financial reporting and auditing requirements applicable to not-for-profit entities.

Ethical obligations of NZICA members

1.8 The Institute’s Code of Ethics applies to all members of the Institute. Members must be able to demonstrate at all times that their actions, behaviour and conduct comply with the Code of Ethics. Non-compliance with the Code of Ethics may lead to disciplinary action against the member.

1.9 The Code of Ethics includes rules on compliance with professional and technical standards. Two key requirements of the Code of Ethics (paragraphs 103 and 104) are set out below. The Code of Ethics (paragraph 105 and Appendix 2) also contains guidelines for members in employment who are involved in disputes with their employer regarding compliance with their professional obligations.

103 Members who are involved in, or have responsibility for, the preparation or presentation of general purpose financial reports should take all reasonable steps within their power to ensure that generally accepted accounting practice is complied with.

104 All material departures from generally accepted accounting practice should be disclosed and explained in the general purpose financial report. The explanation should include the reasons for the departure and its financial and non-financial effects.

General purpose financial statements

1.10 General purpose financial statements are financial statements provided to meet the information needs of external users who are unable to require, or contract for, the preparation of special reports to meet their specific information needs. In the context of a not-for-profit entity, external users would include members, supporters, contributors and anyone else who is not able to obtain special purpose financial statements for their own specific needs. A number of not-for-profit entities are required to prepare general purpose financial reports that include general purpose financial statements. 1.11 The New Zealand Equivalent to the IASB Framework for the Preparation and Presentation of Financial Statements is based on the presumption that general purpose financial statements are prepared and presented in accordance with GAAP.

Special purpose financial statements

1.12 Not all not-for-profit entities prepare general purpose financial statements. Some may prepare only special purpose financial statements. Special purpose financial statements are tailored to meet the specific information needs of a particular person, group of people or organisation. They include financial statements prepared for internal users such as officers of the organisation and for external parties who have the power to demand particular information to meet their information needs, such as lenders, bankers and government departments. Such users can specify the accounting policies to be applied, the format of the financial statements and other material to be included in a special purpose financial report. If an entity has no obligation to present general purpose financial statements in accordance with GAAP (for example, under legislation or its own constitution), and all the members of the entity are in agreement, it may be appropriate to prepare special purpose financial statements. There is no requirement for special purpose financial statements to comply with GAAP. Rather, any special purpose financial statements should specify the basis on which they have been prepared. Although this Guide does not cover special purpose reporting, it may also be useful for those purposes.

More about GAAP

1.13 The Institute’s Code of Ethics imposes an obligation on members who are involved in, or have responsibility for, the preparation or presentation of general purpose financial statements to take all reasonable steps within their power to ensure that GAAP is complied with. The Institute considers that financial statements prepared in accordance with GAAP are necessary for a not-for-profit entity to demonstrate its financial accountability to members and other stakeholders. The financial reporting standards that constitute GAAP are approved by an independent body. The use of independent standards gives users more confidence in the reliability of the financial statements. In addition, users can more easily compare the financial statements of different entities when those financial statements are prepared in accordance with a common set of standards.

1.14 When an entity is required to prepare general purpose financial statements in accordance with GAAP, the law or document establishing that requirement may not specify what it means by GAAP. For most not-for-profit entities the following definition of GAAP will apply.

GAAP means:

• compliance with all New Zealand equivalents to International Financial Reporting Standards (IFRSs), and Financial Reporting Standards (FRSs) applicable to the entity; and

• in relation to matters for which no provision is made in New Zealand equivalents to IFRSs, or FRSs and that are not subject to any applicable rule of law, adopting accounting policies that:

o are appropriate to the circumstances of the entity; and

o have authoritative support within the accounting profession in New Zealand.

New Zealand Preface, paragraph 11 1.15 In some cases (for example, where a not-for-profit entity issues debt securities to the public or operates as a company

under the Companies Act) a not-for-profit entity may be required to report in accordance with the Financial Reporting Act 1993 and apply the definition of GAAP in that Act4.

1.16 The standards referred to in the definition of GAAP are generally developed by the New Zealand Institute of Chartered Accountants and approved by the Accounting Standards Review Board, an independent body. Copies of the standards are available on the Institute’s website5. Collated copies of the standards are published regularly.

1.17 Several years ago the Accounting Standards Review Board decided to replace the financial reporting standards that had been developed by New Zealand with International Financial Reporting Standards (IFRSs) developed by the International Accounting Standards Board. These standards, adapted as necessary for the New Zealand environment, are referred to as New Zealand equivalents to IFRSs (or NZ IFRSs). The changeover from the previous set of standards to NZ IFRSs is scheduled to occur for annual periods beginning on or after 1 January 2007. Early adoption is permitted. However, the timing of adoption is under review. Entities are advised to check current requirements. This Guide assumes that entities are reporting in accordance with NZ IFRSs.

1.18 NZ IFRSs are developed for application by a wide range of entities. Some requirements in NZ IFRSs apply only to profit-oriented entities or public benefit entities (the definition of public benefit entities includes most public sector entities and not-for-profit entities). This Guide focuses on the requirements of NZ IFRSs in respect of not-for-profit public benefit entities only. The Appendix to NZ IAS 1 Presentation of Financial Statements – New Zealand Application Guidance: When is an Entity a Public Benefit Entity? gives guidance on the definition of public benefit entities. It discusses indicators that can be used in determining the primary objective of a public benefit entity.6 These indicators include the entity’s founding

documents, the nature of the benefits, the amount of the expected financial surplus, the nature of the equity interest and the nature of the entity’s funding. The Appendix to NZ IAS 1 should be used to decide whether the public benefit entity reporting requirements in NZ IFRSs are appropriate for an entity.

4Section 3 of the Financial Reporting Act states:

For the purposes of this Act, financial statements and group financial statements comply with generally accepted accounting practice only if those statements comply with— (a) Applicable financial reporting standards; and

(b) In relation to matters for which no provision is made in applicable financial reporting standards and that are not subject to any applicable rule of law, accounting policies that—

(i) Are appropriate to the circumstances of the reporting entity; and (ii) Have authoritative support within the accounting profession in New Zealand.

5Copies of the standards are available at http://www.nzica.com 6The Appendix to NZ IAS 1 is reproduced as Appendix 4 to this Guide.

Differential reporting concessions for small to medium NFPs

1.19 Many small to medium not-for-profit entities will qualify for exemptions, called “differential reporting concessions”, from some of the specific requirements of financial reporting standards (for example, entities that qualify for differential reporting concessions are not required to prepare a cash flow statement). These concessions mainly exempt an entity from making the disclosures required by standards, but they also allow some simplified methods for recognition and measurement. Recognition is the process of incorporating an item in the financial statements and it is subject to an item meeting relevant definitions and criteria. Measurement is the process of determining the monetary amounts at which items such as assets and liabilities are to be recognised and carried in the financial statements.

1.20 The criteria for qualifying for differential reporting concessions are set out in the Framework for Differential Reporting for Entities Applying the New Zealand Equivalents to International Financial Reporting Standards Reporting Regime 2005 (Framework for Differential Reporting)7. An entity qualifies for differential reporting exemptions when the entity does not

have public accountability (as defined in the Framework for Differential Reporting) and:

• at balance date, all of its owners are members of the entity’s governing body; or • the entity is not large (as defined in the Framework for Differential Reporting).

1.21 Appendix 2 of this Guide explains the criteria and what they mean for not-for-profit entities. In the vast majority of cases not-for-profit entities that qualify for differential reporting concessions will do so because:

• they are not publicly accountable for the purposes of the Framework for Differential Reporting (the definition of public accountability in the Framework for Differential Reporting focuses on issuers and entities with the ability to tax or rate); and

• they are not large (as defined in the Framework for Differential Reporting).

1.22 This Guide focuses on the financial reporting requirements applicable to not-for-profit entities that qualify for differential reporting concessions. The differential reporting concessions available in individual standards are described in an Appendix to the Framework for Differential Reporting and are identified within individual standards8. Any readers

seeking information on the financial reporting requirements for other entities should refer to the requirements of each applicable standard.

1.23 Differential reporting concessions are not compulsory – a qualifying entity can choose to take advantage of some concessions but not others. However any concessions used must be applied consistently. If a qualifying entity chooses to make any disclosure from which it is exempt, the entity must do so in accordance with the relevant standard. Entities that qualify to use differential reporting concessions and that elect to do so will not be able to assert compliance with IFRSs.

Identifying financial reporting and auditing requirements for not-for-profit entities

Types of not-for-profit entities

1.24 Not-for-profit entities have a wide variety of purposes and forms. Some not-for-profit entities achieve their objectives through their own activities, while others do so by making grants to individuals or other organisations. Some operate as a single entity while others operate in combination with other entities or organisations such as branches or supporters’ groups. Some are financed from permanent endowments or public appeals, others from regular subscriptions, and others from the proceeds of trading profits. Not-for-profit entities include incorporated societies, unincorporated societies, trusts and companies.

1.25 This section explains how to identify the financial reporting and audit requirements applicable to not-for-profit entities and illustrates this by application to some common types of not-for-profit entities.

Identifying financial reporting requirements

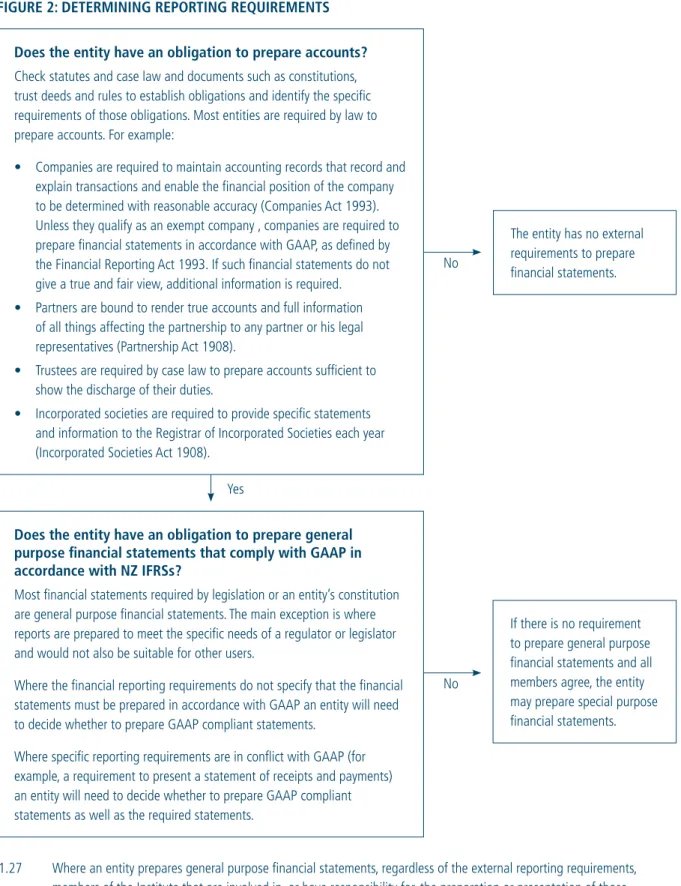

1.26 Figure 2 identifies key questions in identifying the financial reporting requirements applicable to not-for-profit entities.

7The Framework for Differential Reporting is included in Applicable Financial Reporting Standards (published by the Institute on a regular basis) and is available on the Institute’s

website at http://www.nzica.com

8Disclosure concessions are identified by way of an asterisk beside the relevant requirement in the standard. Other concessions are described in the scope section of each

FIGURE 2: DETERMINING REPORTING REQUIREMENTS Does the entity have an obligation to prepare accounts?

Check statutes and case law and documents such as constitutions, trust deeds and rules to establish obligations and identify the specific requirements of those obligations. Most entities are required by law to prepare accounts. For example:

• Companies are required to maintain accounting records that record and

explain transactions and enable the financial position of the company to be determined with reasonable accuracy (Companies Act 1993). Unless they qualify as an exempt company , companies are required to prepare financial statements in accordance with GAAP, as defined by the Financial Reporting Act 1993. If such financial statements do not give a true and fair view, additional information is required.

• Partners are bound to render true accounts and full information

of all things affecting the partnership to any partner or his legal representatives (Partnership Act 1908).

• Trustees are required by case law to prepare accounts sufficient to

show the discharge of their duties.

• Incorporated societies are required to provide specific statements

and information to the Registrar of Incorporated Societies each year (Incorporated Societies Act 1908).

Does the entity have an obligation to prepare general purpose financial statements that comply with GAAP in accordance with NZ IFRSs?

Most financial statements required by legislation or an entity’s constitution are general purpose financial statements. The main exception is where reports are prepared to meet the specific needs of a regulator or legislator and would not also be suitable for other users.

Where the financial reporting requirements do not specify that the financial statements must be prepared in accordance with GAAP an entity will need to decide whether to prepare GAAP compliant statements.

Where specific reporting requirements are in conflict with GAAP (for example, a requirement to present a statement of receipts and payments) an entity will need to decide whether to prepare GAAP compliant statements as well as the required statements.

The entity has no external requirements to prepare financial statements.

If there is no requirement to prepare general purpose financial statements and all members agree, the entity may prepare special purpose financial statements. Yes

No

No

1.27 Where an entity prepares general purpose financial statements, regardless of the external reporting requirements, members of the Institute that are involved in, or have responsibility for, the preparation or presentation of those statements have an obligation under the Institute’s Code of Ethics (as discussed in paragraph 1.9) to take all reasonable steps within their power to ensure that generally accepted accounting practice is complied with. Where an entity prepares special purpose financial statements members should ensure that these statements are clearly labelled as special purpose and that the basis of preparation is clearly explained.

1.28 Financial reporting requirements in relation to some types of entities are outlined below. Please note that there may be some overlap in the categories – for example, some incorporated societies may also be charities registered with the Charities Commission and subject to any reporting requirements established by the Commission.

Incorporated societies

1.29 An entity that is incorporated under the Incorporated Societies Act 1908 is required by that Act to file a certified copy of its annual financial statements with the Registrar of Incorporated Societies each year9. The annual financial statements

must include the following information:

• the income and expenditure of the society for the latest financial year; • the assets and liabilities, as at the close of the financial year;

• all mortgages and secured loans of any description, affecting any of the property of the society, as at the close of the

financial year;

• the society’s full name; and

• the financial year that the financial statements have been prepared for.

1.30 There is a suggested format for the financial statements, but the format is not mandatory10.

1.31 Because the relevant legislative requirements do not specify that the financial statements must be prepared in accordance with GAAP, an incorporated society will also need to consider whether there are any relevant requirements in its constitution. If the constitution is silent, the incorporated society will need to decide whether to prepare GAAP compliant financial statements.

Trusts

1.32 The Charitable Trusts Act 1957 does not impose any specific financial reporting obligations on trusts incorporated under that Act. However, trustees have a legal obligation, owed to the beneficiaries of the trust, under the Trustees Act 1956 to keep adequate accounting records. The statutory obligation arises by virtue of the duty of trustees to properly carry out the general powers and duties conferred on them by the Trustee Act 1956. The courts have confirmed in many cases that there is a common law obligation on trustees, as part of their general fiduciary obligations to the beneficiaries, to keep and to prepare accounts. The general standard for trusts is the preparation of “proper accounts”, or “full and clear accounts” or “appropriate financial records”. Whether this requires the preparation of general purpose financial reports and adherence to GAAP is a question to be answered on a case by case basis.

1.33 Whatever standard is applied, the accounts must clearly present the state of affairs of the trust. What seems essential is that the accounts are appropriate for the potential users of that information, primarily being the beneficiaries and the trustees. In the case of trusts carrying debt, the creditors might also have a legitimate expectation as to the preparation of proper accounts.

1.34 Because beneficiaries can request full information about the trust from the trustees, does this provide them with the right to require the preparation of a special purpose report? Possibly, depending on the rights of the particular beneficiary and the nature of the request, but it does not necessarily preclude the need for general purpose financial reports – particularly where there is more than one beneficiary and/or different classes of beneficiaries.

1.35 Does the beneficiaries’ ability to inspect financial records through their access to full information about the trust mean that the trustees can opt out of producing general purpose financial reports? If this were so, there would be no need for the courts to determine that “full and clear” accounts were required. There is clearly a requirement to produce financial statements (referred to as accounts in the case law), distinct from the requirement to allow access to, or to supply full information.

Companies

1.36 All companies must complete financial statements that meet the requirements of the Financial Reporting Act 1993. Unless they qualify as an exempt company11, companies are required to prepare financial statements in accordance

with GAAP, as defined by the Act. Generally compliance with generally accepted accounting practice will result in

9Incorporated Societies that register under the Charities Act do not have to file annual financial statements with the Registrar of Incorporated Societies. The Companies Office

retrieves this information directly from the Charities Register.

10For more information refer to www.societies.govt.nz

11Exempt companies are small companies which are permitted to prepare very simple accrual-based financial statements. An exempt company as defined by the Financial

Reporting Act means a company, other than an overseas company or an issuer, if,— (a) at least two of the following subparagraphs apply:

(i) as at the balance date of the accounting period for which financial statements are required, the value of the total assets of the company (including intangible assets) reported in the statement of financial position did not exceed $1,000,000;

(ii) in the accounting period for which financial statements are required, the turnover of the company did not exceed $2,000,000;

(iii) as at the balance date of the accounting period for which financial statements are required, the company has 5 or fewer full-time equivalent employees; and (b) as at the balance date of the accounting period for which financial statements are required, the company—

(i) was not a subsidiary of another body corporate or association of persons; and (ii) did not have any subsidiaries.

financial statements that give a true and fair view of the matters to which they relate – if it does not, the Act requires additional information. The reporting requirements for companies are currently under review by the Ministry of Economic Development.

Unincorporated entities

1.37 Unincorporated entities are clubs, societies and other groups that are formally organised but are not incorporated and hence not registered under any act of parliament. They are the largest group of not-for-profit entities in New Zealand. There are no statutory financial reporting requirements applying to such entities. However, in the case of disputes regarding financial reporting the courts will imply an obligation to prepare accounts.

Identifying audit requirements

1.38 Entities may be required by law, their constitution, or as a condition of receiving a grant, to have their financial statements audited. For example, the Lotteries Grants Board requires audited financial statements for grants over a certain amount. An audit of financial statements is designed to provide independent professional assurance that the financial statements reflect the underlying transactions and events. The cost of an audit of financial statements reflects the amount of work required to obtain the evidence to support this opinion. The audit opinion does not:

• provide a guarantee of absolute accuracy in the financial statements;

• express a view on the adequacy of the entity’s accounting and internal control systems or the effectiveness and

efficiency with which the entity has conducted its affairs; or

• guarantee the entity’s future viability.

1.39 In some cases a review of the financial statements may be a more cost-effective option than an audit. A review is designed to provide a “negative assurance report” giving only a moderate level of assurance to readers on the reliability of the financial information. This means the reviewer states that nothing has come to the reviewer’s attention to indicate that the financial information is not presented fairly in accordance with GAAP. For example, if only members of the entity, or a third party such as a funding body, need to know that the financial statements comply with GAAP, an audit of the financial statements may not be needed to provide the level of assurance these users require. Review engagements are designed as a limited review of financial statements; therefore the risk of mistakes, omissions or incorrect disclosures is considerably greater than with an audit of the financial statements. However, because the level of assurance provided by a review is lower, less work is required and the cost is often significantly less. Entities considering a review rather than an audit of financial statements need to decide whether a review will provide the level of assurance required. They must also have authorisation from members or the third party for a review rather than an audit of the financial statements. An entity may be able to change its constitution to specify that a review of the financial statements is permitted. Appendix 3 to this Guide contains more information on the nature of review engagements.

Financial reporting requirements under review

1.40 At the time of writing the reporting requirements for a number of entities are under review. The Ministry of Economic Development will be consulting on proposed reporting requirements for charities. The Ministry has stated that the earliest possible date for any change to charity financial reporting requirements would be for financial years beginning on or after 1 January 2010.

1.41 Charities that are registered with the newly established Charities Commission will need to ensure that they comply with any requirements established by the Commission (refer www.charities.govt.nz). Registered charities are required to submit an “Annual Return” that is accompanied by a copy of the charity’s financial statements. The information provided in these Annual Returns will be publicly available on the Charities Register – unless the Charities Commission decides it is in the public interest to withhold it. Currently there is no requirement in the Charities Act for an Annual Return to include audited financial statements or to comply with any standards set by external groups. However, if an entity has audited financial statements, then the Charities Commission requests that the audited financial statements be provided as part of the annual return. The financial reporting requirements for charities continue to be found in:

• the document, deed, rules, or constitution of the charity itself; or • any legislation the charity is subject to.

First-time adoption of NZ IFRSs

1.42 This Guide assumes that entities are reporting in accordance with NZ IFRSs. At the time of writing, entities are required to adopt NZ IFRSs for annual periods beginning on or after 1 January 2007. Early adoption is permitted. However the timing of adoption is under review. Entities are advised to check current requirements. As required by NZ IFRS 1 First-time Adoption of New Zealand Equivalents to International Financial Reporting Standards, the transition occurs at one point in time and is marked by an explicit and unreserved declaration that the financial statements comply with NZ IFRSs. 1.43 When an entity first adopts NZ IFRSs, both the financial statements for the period of adoption and the comparative

financial statements must comply with the new standards. So if an entity adopts NZ IFRSs for the period beginning 1 April 2007, it would prepare financial statements for the year ending 31 March 2008 in accordance with NZ IFRSs. It would also need to prepare opening and closing balances and a statement of financial performance for the year ended 31 March 2007 as the comparative financial statements. A note explaining how the transition from previous GAAP to NZ IFRSs affected the entity’s financial statements is also required at the time of first adoption.

1.44 To establish opening balances an entity will need to:

• recognise all assets and liabilities whose recognition is required by NZ IFRSs;

• no longer recognise items as assets or liabilities if NZ IFRSs do not allow the recognition of such items;

• reclassify items previously recognised as one type of asset, liability or component of equity which are a different type

of asset, liability or component of equity under NZ IFRSs; and

• apply NZ IFRSs in measuring all recognised assets and liabilities.

1.45 The transition process can be viewed as a good opportunity to review all assets and liabilities and ensure they are accounted for in accordance with GAAP.

1.46 Many not-for-profit entities are unlikely to see much change in the types of assets and liabilities included in the statement of financial position. The main differences are likely to relate to classification (for example, investments may need to be reclassified depending upon the purpose for which they are held) and measurement. However, the adoption of NZ IFRSs provides an opportunity to consider appropriate accounting policies for an entity.

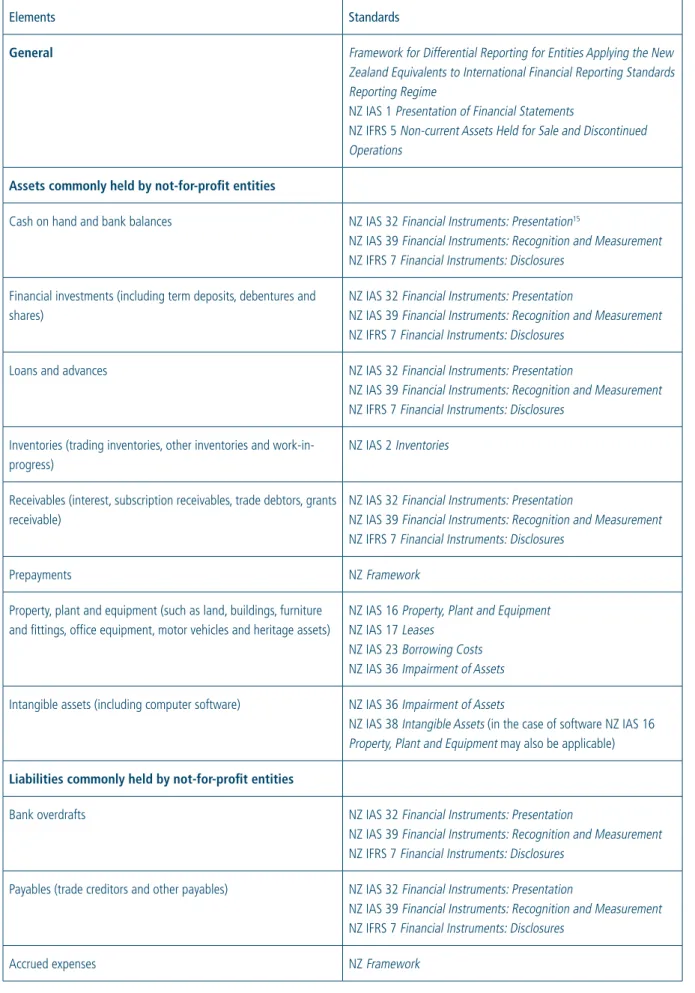

1.47 Chapter 4 discusses the requirements of financial reporting standards in relation to categories of assets and liabilities commonly held by not-for-profit entities.

1.48 When an entity changes its accounting policies (for example, as a result of adopting NZ IFRSs) the general rule is that the new accounting policies have to be applied retrospectively – that is, as if they have always been applied. However, some standards contain transitional provisions and there are some exceptions to this rule. For example, NZ IFRS 1:

• grants exemptions from some requirements of NZ IFRSs (paragraphs 13 to 25F);

• prohibits retrospective application of some aspects of NZ IFRSs (paragraphs 26 to 34B); and • provides some concessions from the requirement to present comparative information.

1.49 The exemption that is most likely to be used by not-for-profit entities is the option to measure an item of property, plant and equipment at the date of transition at its fair value and use that fair value as its deemed cost at that date (paragraphs 16 to 19).

Chapter 2 – Reporting Entity

Key points

• A reporting entity is an entity which provides financial statements to external users as the major source of financial information

about the entity.

• The reporting entity concept determines which activities or operations are covered by the financial statements. The reporting

entity for which financial statements are prepared may be broader or narrower than what is commonly thought of as the not-for-profit entity.

• Where an entity is a separate legal entity the relevant legislation often specifies the reporting entity.

• A not-for-profit entity which does not have any branches, or conducts its activities through other groups or organisations or

affiliated bodies, prepares financial statements for its own assets and liabilities, income and expenses.

• Where a not-for-profit entity has branches, or conducts its activities through other groups or organisations or affiliated bodies

which form part of the same legal entity as the not-for-profit entity the transactions of these branches etc will form part of the not-for-profit entity’s financial statements. Where these activities occur in separate entities, the not-for-profit entity may need to include some or all of the assets and liabilities, income and expenses of those other entities in consolidated financial statements (which are a set of combined financial statements).

• Where a not-for-profit entity has branches, or conducts its activities through other groups or organisations or affiliated bodies

these other entities may be reporting entities in their own right.

• If it is not clear which activities should be included within an entity’s financial statements, specialist advice may be needed.

Introduction

2.1 A reporting entity is “an entity which prepares general purpose financial statements for users who rely on those financial statements as their major source of financial information about the entity” (NZ Framework). In other words it is the entity that is the subject of financial statements in an annual report.

2.2 In some cases it is easy to identify the reporting entity. A separate legal entity that is required (for example, by its constitution, trust deed or legislation) to prepare financial statements is usually also the reporting entity. This will be the case for the majority of not-for-profit entities.

2.3 However, identifying the reporting entity is not so clear cut if the entity:

• is not specifically required to prepare financial statements; and

• is part of a group or operates in conjunction with other linked organisations.

2.4 If an entity has no clear requirement to prepare financial statements it needs to consider whether there are external users which rely upon its financial statements to find out information about the entity. For example, a national group which is a separate legal entity may have five regional branches which are not themselves separate legal entities and which are not required by legislation or their constitution to prepare financial statements. However, the branches may consider that they have a responsibility to provide a public report due to their role in the community. Individual branches can present their own financial statements, and should do so in accordance with generally accepted accounting practice (GAAP). In this situation each branch is a reporting entity.

2.5 This chapter explains how to identify the reporting entity for some common structures used by not-for-profit entities:

• a not-for-profit entity with branches which carry out specific activities of the entity, or operate in a particular

geographical area (these branches may or may not be separate legal entities)

• a not-for-profit entity with one or more sub-entities such as trusts or trading companies

• a not-for-profit entity that is the national body of a federation of local organisations and co-ordinates the activities

of those organisations

• a not-for-profit entity which carries out activities in partnership with other bodies but without establishing a separate

legal entity. For example, a church may enter into a joint arrangement with other churches to carry out certain activities.

2.6 Mergers of entities and the acquisition of one entity by another can also occur but are not covered in this Guide. Guidance on accounting for mergers and acquisitions can be found in NZ IFRS 3 Business Combinations.

“Control” and “significant influence”

2.7 Working out how to account for different parts of a not-for-profit entity often depends on whether the overall (parent) not-for-profit entity controls or has significant influence over the other parts (such as branches and sub-entities).

Control

2.8 Control is the power to govern the financial and operating policies of an entity so as to receive benefits from its activities (NZ IAS 27 Consolidated and Separate Financial Statements paragraph 4). Control often exists when one entity has created or acquired another entity.

2.9 NZ IAS 27 provides guidance on determining whether control exists (NZ IAS 27 paragraphs 13 to 21). Power to govern the financial and operating policies of an entity so as to receive benefits from its activities exists when the parent entity:

• owns more than half of the voting power of an entity; • has power over more than half of the voting rights;

• has the power to govern the financial and operating policies of the entity under a statute or agreement;

• has the power to appoint or remove the majority of the members of the board of directors or equivalent governing

body that runs the entity; or

• has the power to cast the majority of votes at meetings of the board of directors or equivalent governing body that

runs the entity.

2.10 This means that a not-for-profit that has branches and, in accordance with NZ IAS 27, is able to govern the financial and operating policies of the branches has control over those branches.

2.11 There is more information on control in FRS-37 Consolidating Investments in Subsidiaries (paragraphs 4.13–4.37 and 5.9–5.11) and International Public Sector Accounting Standard IPSAS 6 Consolidated Financial Statements and Accounting for Investments in Subsidiaries (paragraphs 26–36)12. This additional guidance applies only to public benefit

entities (NZ IAS 27 paragraph NZ 12.1).

Significant influence

2.12 Significant influence is the power to participate in financial and operating policy decisions but not control them (NZ IAS 28 Investments in Associates paragraph 2). A holding of 20% or more of the voting power (directly or through subsidiaries) indicates significant influence unless it can be clearly demonstrated otherwise. If the holding is less than 20%, the entity is presumed not to have significant influence unless influence can be clearly demonstrated by other means (NZ IAS 28 paragraph 6).

2.13 Significant influence is usually shown in one or more of the following ways:

• representation on the board of directors or equivalent governing body; • participation in the policy-making process;

• material transactions between the two entities; • interchange of managerial personnel; or

• provision of essential technical information (NZ IAS 28 paragraph 7).

2.14 This means, for example, if a charity beneficially holds 20% or more of the voting rights in another entity, it would be presumed to have the power to participate in and influence over the other entity’s operating and financial policy, unless this was proven not to be the case. The charity would have significant influence over the other entity.

Branches

2.15 Many not-for-profit entities have branches, which will be either part of the overall legal entity or separate legal entities in their own right.

2.16 If the branches are part of the overall legal entity, they are included in the overall entity’s financial reports. This means that the transactions and balances of the branches (for example, their assets and liabilities) are included in the financial statements of the overall not-for-profit entity. Even where branches form part of the overall legal entity they may be reporting entities in their own right and may have an obligation (explicit or inferred) to provide financial statements to their members on the activities of the branch.

12Although IPSAS 6 is the more recent pronouncement, the guidance in FRS-37 is more relevant for not-for-profit entities because it was developed for application by a wide range

of entities. IPSAS 6 which was developed for application by public sector entities drew heavily on the material in FRS-37. Exposure Draft 112 Proposed Application Guidence for NZ 1AS 27 Consolidated and Separate Financial Statements to Assist in Determining Whether a Public Benefit Entity Controls Another Entity (June 2007) is also relevant.

2.17 If the branches are separate legal entities the overall not-for-profit entity may control the branches or have significant influence over them. If the overall entity has control, the branches are accounted for as subsidiaries; and if the overall entity has significant influence, the branches are accounted for as associates in the financial statements of the overall entity (see below). The constitution or other documents such as trust deeds may help to determine whether a branch is controlled or under significant influence. Some branches may have sub-branches. In such cases it is necessary to consider whether the sub-branches form part of the branch and whether the sub-branches are reporting entities in their own right.

2.18 If a not-for-profit entity has branches the notes to the financial statements should clearly state whether the financial activities of the branches are included in the overall entity’s financial statements and whether the branches produce their own financial statements.

2.19 Branches need to consider whether they should prepare general purpose financial statements. If the only user of a branch’s financial statements is the overall not-for-profit entity it is unlikely that general purpose financial statements are necessary. 2.20 Groups of people who occasionally gather together to raise funds for a charity, and special interest groups that are

affiliated to a particular charity but do not themselves undertake charitable activities, are not branches and their financial activities should not usually be combined with those of the reporting entity.

Sub-entities such as trusts or trading companies

2.21 A not-for-profit entity that has established separate legal entities, such as trusts or trading companies, to carry out specific functions will need to consolidate the financial statements of those entities unless the founding entity does not control those separate entities. The methods of accounting for sub-entities that are controlled (subsidiaries) and those that are subject to significant influence (associates) are discussed below.

Federations

2.22 If a not-for-profit entity is the national body of a federation of local organisations and co-ordinates the activities of those organisations, it will need to determine whether it controls or has significant influence over the local organisations. Control is less likely to exist in a federation structure than in a branch structure. In many cases the national body merely supports, rather than controls, the local organisations. If the not-for-profit entity controls the local organisations it accounts for them as subsidiaries, and if it has significant influence it accounts for them as associates (see below).

Joint arrangements

2.23 Not-for-profit entities may undertake joint arrangements where they operate in partnership with other bodies but without establishing a separate legal entity. Such arrangements may meet the definition of joint ventures (see below) and need to be accounted for as such.

Accounting for controlled entities (subsidiaries)

2.24 If a not-for-profit entity controls another entity (that is, it governs the financial and operating policies of an entity so as to receive benefits from its activities), the not-for-profit entity (the parent) must prepare financial statements that include some or all of the assets and liabilities, income and expenses of the other entity in consolidated financial statements (which are a set of combined financial statements). The controlled entities are referred to as the subsidiaries of the parent entity. A number of adjustments such as the elimination of transactions between the entity and subsidiaries are required when preparing consolidated financial statements.

2.25 In some instances a not-for-profit entity with subsidiaries will be required to present both consolidated financial statements and financial statements for the parent entity alone. This requirement would be specified in an entity’s founding documents or legislation. Parent entity statements are not required by financial reporting standards. If both sets of statements are required they are usually presented as two columns in a single report.

2.26 There are some exceptions to the requirement to consolidate subsidiaries. For example, if the not-for-profit entity is itself a wholly owned subsidiary, it may not be required to produce consolidated financial statements (NZ IAS 27 paragraph 10). 2.27 Some situations will require careful consideration. For example, a not-for-profit entity may establish another entity for the

purpose of providing independent advice on its activities. Such complex situations are not covered by this document. In such cases you will need to consider the detailed requirements of the relevant reporting standards and seek specialist advice. 2.28 When an entity has a subsidiary in which it controls less than half of the voting power, it has to disclose the nature of

Accounting for significant influence (associates)

2.29 NZ IAS 28 explains how an entity accounts for another entity over which it has significant influence (and that other entity is not a subsidiary or an interest in a joint venture). Such entities are referred to as associates. Associates are relatively uncommon in the not-for-profit sector but can occur.

2.30 The requirements in NZ IAS 28 set out a method of accounting referred to as the equity method. Under this method a not-for-profit entity with an associate recognises its share of the associate’s surplus or deficit (less any unrealised profits on transactions between the entity and the associate).

Accounting for jointly controlled activities (joint ventures)

2.31 In a joint venture situation, an activity is jointly controlled by two or more parties. For example, a number of churches may jointly establish a separate entity to advocate on issues which are of interest to all the churches and to provide aged care services. NZ IAS 31 Interests in Joint Ventures deals with how to identify a joint venture and how to report the activities of a joint venture in the financial statements of the parties that have joint control.

2.32 NZ IAS 31 states that joint control exists when the strategic financial and operating decisions for the activity require the unanimous consent of the parties (NZ IAS 31 paragraph 3). It is possible for a not-for-profit entity to beneficially hold 20% or more of the voting rights in an undertaking but for the management arrangements to be such that control is clearly shared with the other partners. In this case the undertaking is a joint venture rather than an associate. 2.33 The method of combining information on the joint venture’s financial activities in the consolidated financial

statements depends on the type of joint venture. An entity with an interest in a joint venture can recognise its interest in a joint venture in the financial statements by either proportionate consolidation or the equity method. NZ IAS 31 explains these methods.

Maintaining records

2.34 If a not-for-profit entity has subsidiaries, associates or joint ventures it will need to maintain records of transactions between itself and each of these other entities during each period so that the requirements of relevant financial reporting standards can be complied with. When an entity prepares consolidated financial statements NZ IAS 27 requires that it eliminate intragroup balances (for example, loans between the not-for-profit entity and its subsidiary) income and expenses.

Registered charities

2.35 Provision exists within the Charities Act 2005 for a group of charities to be treated as if they were a single entity. The requirements for group registration are met if the Commission is satisfied that:

• each of the organisations within the group qualifies for registration as a charitable entity; and • all of the organisations are sufficiently closely related; and

• it is fit and proper to treat the organisations as forming part of a group.

In addition, the Commission must have regard to the extent to which the entities have similar charitable purposes. 2.36 Charities registered as a group under the Charities Act will be subject to any requirements of the Charities Commission

in respect of such groups. However, it is not a requirement for group registration that the entities registering be part of an accounting group and, accordingly, such groups of charities will not necessarily be the same as the reporting entity under NZ IFRSs.

Examples – identifying the reporting entity

2.37 The following examples identify the reporting entity in various situations.

Please note

The examples here are simplified and do not address the specific circumstances of any particular entity. Each entity will need to consider the facts in its own situation and the application of NZ IAS 27, NZ IAS 28 and NZ IAS 31 to those facts.

Example 1

A sports club is required by its constitution to prepare general purpose financial statements. The club receives some funding from a national body but is independent of that body. The club has not formally established any other clubs or groups.

The reporting entity is the sports club. The financial statements would include the assets and liabilities, and revenue and expenses of the sports club.

Example 2

An incorporated society is a national body with three branches – Auckland, Wellington and Christchurch. The national body receives funding from the Government and co-ordinates fundraising activities by all branches. The national body decides which services will be provided to clients and approves the budgets of each region. The branches are not separate legal entities.

The reporting entity is the national body, including the three branches. The financial statements are not consolidated financial statements because legally the branches are part of the national body. As noted in paragraph 2.4 of this Chapter, the branches may also have an obligation to produce general purpose financial statements and be reporting entities in their own right.

Example 3

An incorporated society is a national body with ten branches throughout New Zealand. The branches are separate incorporated societies. The governing bodies of the branches are appointed by local members and the branches are free to establish their own rules. Each area conducts its own fundraising activities and decides how to spend money raised in its region. The branches pay a fee to the national body, which provides advocacy and other support services. The national body does not fund the activities of the branches. In the event of dissolution, the constitution of each local branch states that any residual assets are to be distributed to entities with related not-for-profit objectives.

The national body and the branches are all separate reporting entities. As the national body has no control over the branches it would not consolidate them in its financial statements.

Example 4

A not-for-profit entity (A) that provides services to low-income families establishes another entity (B) to manage the houses that it owns and which are available for rent by its clients. The board of entity B is appointed by the board of entity A. Entity B operates as a property management agency deciding which applicants can rent houses and the amount of the rental, and has considerable autonomy in doing this. If entity B makes a profit it distributes some of that profit to entity A. If entity B makes a loss it can seek additional funding from entity A. The documents that establish entity B require it to prepare separate financial statements. Entity B is controlled by entity A. Entity A would prepare consolidated financial statements that include entity B’s transactions and balances.

Entity B would also prepare separate financial statements because it is required to do so by its founding documents. If this specific requirement did not exist, entity B would need to consider whether there were any external users who relied upon financial statements to find out information about entity B.

Example 5

A charitable trust provides food and accommodation to homeless people. It regularly liaises with other community groups and works with those groups to ensure its services are provided in the areas where they are most needed. It has a group of supporters that help raise money for its activities.

The reporting entity is the charitable trust. It does not control (or jointly control) the activities of the other groups. Nor does it control the supporters.

Example 6

National Body A is an umbrella body with a number of affiliated associations which operate in various regions around the country. National Body A imposes certain rules and standards on the associations. It does not have the power to wind up its affiliated

associations, but it is able to prevent them from using the name of the National Body. National Body A levies its associations at a fixed fee per member.

The governing bodies of the affiliated associations are appointed by the members of those associations. The governing bodies have financial and operating policy-making powers, subject to the rules and standards of the National Body.

The reporting entity is National Body A. It does not control the affiliated associations.

Each affiliated association may also be a reporting entity. For example, they would be reporting entities if they have obligations to prepare financial statements or if there are external users who rely upon financial statements to find out information about them.

![FIGURE 6: SAMPLE STATEMENT OF TRUST MONEY FORMAT STATEMENT OF TRUST MONIES HELD FOR THE YEAR ENDING [DATE]](https://thumb-us.123doks.com/thumbv2/123dok_us/8554898.2310598/47.892.109.788.191.334/figure-sample-statement-trust-format-statement-monies-ending.webp)