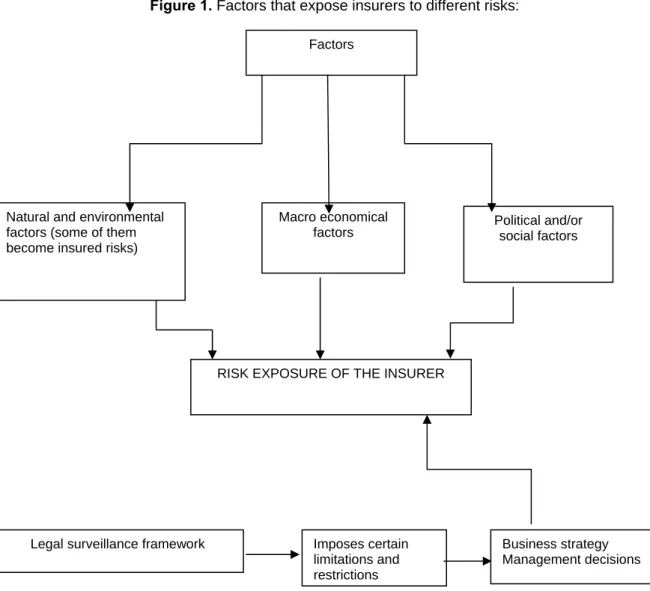

Influence of adjacent insured risks upon the management of insurance companies

Full text

Figure

Related documents

The current study contributes to the understanding of light users by focusing on the cognitive and motivational structure of sustainability for consumers that

The Government agrees not to seek any pricing reduction in future contracts resulting from this VECP until the contractor recovers its nonrecurring implementation investment

commuter trains) CAPITOL SOUTH METRO STATION FEDERAL CENTER SW METRO STATION L’ENFANT PLAZA METRO STATION JUDICIARY SQ METRO STATION GALLERY PL- CHINATOWN METRO STATION METRO

In the proposed fault isolation scheme, a multi-layer perceptron neural network (MLPNN) is employed in each of the AUVs after the neural observer to categorize the type of the

Lane and Walti (2007) show that, after controlling for common factors, the correlations in the idiosyncratic component of national stock market returns have increased among members

The SBA and its resource partners, including Small Business Development Centers, Women’s Business Centers, Veterans Business Outreach Centers, and SCORE, have the expertise to

; ; TAHAP EKSPLORASI TAHAP EKSPLORASI DAERAH DAERAH EKSPLORASI EKSPLORASI PEMBORAN SMR PEMBORAN SMR PENGEMBANGAN, PENGEMBANGAN, Luas st%uktu% 1isa l!1i0 Luas st%uktu% 1isa