YTC Resources Limited

Gold

& C

op

pe

r: Deve

lo

per

Price Target $0.72Brief Business Description

Hartleys Brief Investment Conclusion

Issued Capital - fully diluted Market Cap - fully diluted Cash (est) EV Main Projects

Hera (NSW) Au, Base Metals

Nymagee (NSW) Cu

Resources

2.2Mt @ 4g/t Au, 15.6 g/t Ag, 2.8% Pb & 3.9% Zn

Board

Top Shareholders

Yunnan Tin Aust TDK Resources

14.8%

Wonderful Investments Limited9.0%

Company Address Author Mike Millikan Resources Analyst Ph +61 8 9268 2805 E [email protected]YTC.asx

Speculative Buy

Nymagee to give Hera project scale for 2012 production

248.2m 253.6m $146.4m 1 Jun 2011

Share Price (last) $0.590

Gold and Base Metals Explorer/Developer

$149.6m $33.0m $113.4m

Hartleys has provided corporate advice w ithin the past 12 months and continues to provide corporate advice to YTC Resources Limited. See back page for full disclosure.

Mr Richard Hill (Non-Exec. Dir.) Quoqing Zhang (Non-Exec. Dir.) Ms Christine Ng (Non-Exec. Dir.)

2 Corporation Place Orange, NSW, 2800

Mr Wenxiang Gao (Chairman) Mr Anthony Wehby (Vice Chairman) Mr Rimas Kairaitis (Dir. and CEO) Mr Stephen Woodham (Non-Exec. Dir.) Mr Robin Chambers (Non-Exec. Dir.)

YTC RESOURCES LIMITED

Nymagee a Significant Copper Discovery

On-going drilling by YTC Resources Limited (“YTC”, “Company”) at its

Nymagee project (YTC 90%), located ~100km southeast of Cobar, NSW

continues to intersect high-grade copper with silver credit. Recent results

have identified shallow copper mineralisation over broad intervals at the

southern and northern end of the historic mine and with more high-grade

copper lodes confirmed through deeper drilling. Nymagee is evolving into a

significant copper discovery for the Company, with the mineralised system

containing at least three high-grade copper lodes which should result in a

longer mine life and potentially enable increased production rates (once

developed). YTC believes that the Nymagee system may be similar to the

nearby world-class CSA deposit which has yielded over 1.5Mt of copper and

extends to depths over 1.5km with multiple high-grade copper lodes.

Strong lead-zinc-silver lenses are also developing within the Nymagee

system which has the potential to provide further credits and improve project

economics once in production. Recent drilling of the western lead-zinc-silver

lens has delivered some of the widest intercepts at the highest grades to

date, and is located only 15m west of the Main Lens at Nymagee.

Far West Lens provides more upside at Hera

The Hera deposit consists of a number of sub-vertical, high grade

gold-lead-zinc-silver-copper lenses with zones of coarse gold. Some of the lenses are

gold-rich, whereas others are more base metal rich. The deposit is still open

at depth and along strike. The project has an indicated and inferred

resource of 2.18Mt @ 4.0g/t Au, 15.6g/t Ag, 2.8% Pb and 3.9% Zn for

~560.7koz Au Eq. However, this is likely to be updated in both size and

confidence level with the current ongoing drilling as part of the DFS.

The Main lens contains the bulk of the resource and has a ~600m strike.

Other significant lenses include the 1530, the Far West and the Western

Lead lens. Further strong gold and base metal results have been received

from recently completed infill-drilling of the Far West Lens, with visible gold

identified in some intervals

Expanded DFS on track for mid year

YTC is currently completing a DFS into the development of Hera and

Nymagee. The DFS originally proposed a 350ktpa plant, producing

~50kozAuEq per annum, from the Hera project alone. However, following

the exploration success at Nymagee, as well as the Far West Lens at Hera,

the Company is now looking at expanded production scenarios. Drilling is

continuing at Hera and Nymagee with a maiden resource due for Nymagee

soon. In addition, the completion of the DFS and key project approvals for

Hera are expected in mid 2011 with a decision to mine in the September

quarter 2011.

New Resource Estimate Soon; YTC rated a Speculative Buy

The drilling at Nymagee and Hera continue to both de-risk and extend the

ore bodies. The deposits have not been closed off by drilling implying further

resource growth to come. We have a price target for YTC of 72cps based on

our weighted valuation development scenario for Hera and Nymagee. We

continue to recommendation YTC Resources Limited as a Speculative Buy.

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 Jun-11 Feb-11 Oct-10 Jun-10 Volume - RHS YTC Shareprice - LHS

Sector (S&P/ASX SMALL RESOURCES) - LHS

A$ M

YTC Resources

Hartleys Limited

YTC Resources Limited

1 June 2011

SUMMARY MODEL

YTC Resources Limited Share Price

YTC $0.590 Speculative Buy

Key Market Inform ation Directors Com pany Inform ation

Share Price $0.590 Mr Wenxiang Gao (Chairman) 2 Corporation Place

Market Capitalisation $146m Mr Anthony Wehby (Vice Chairman) Orange, NSW, 2800

52 Week High-Low $0.82-$0.17 Mr Rimas Kairaitis (Dir. and CEO) Tel: (02) 6361 4700

Issued Capital 248.2m Mr Stephen Woodham (Non-Exec. Dir.) Fax: (02) 6361 4711

Issued Capital (fully diluted inc. ITM options) 253.6m Mr Robin Chambers (Non-Exec. Dir.) Web: w w w .ytcresources.com

Options 5.425m @ 0.29c Mr Richard Hill (Non-Exec. Dir.)

Hedging

-Yearly Turnover/Volume $95.5m/202.8m shares

Liquidity Measure (Yearly Turnover/Issued Capital) 82% 1Top 10 Shareholders m shares %

Valuation $0.72 2

3Yunnan Tin Aust TDK Resources 24.24 14.76%

Financial Perform ance Unit FY2010A FY2011F FY2012F FY2013F 4Wonderful Investments Limited 14.77 8.99%

5Yunnan Tin YTC Holdings Pty Ltd 9.76 5.95%

Net Revenue A$m 1.4 0.1 2.9 53.7 6HSBC Custody Nom Aust Ltd 8.18 4.98%

Total Costs A$m (2.8) (2.1) (5.1) (45.3) 7ANZ Nominees Limited 5.98 3.64%

EBITDA A$m (1.4) (1.9) (2.2) 8.5 8Locksley Holdings Pty Ltd 3.34 2.04%

Depreciation/Amort A$m (0.1) (0.1) (2.3) (11.7) 9Smiff Pty Ltd 3.17 1.93%

EBIT A$m (1.5) (2.0) (4.5) (3.2) #UBS Wealth Management Aust Nom 3.07 1.87%

Net Interest A$m 0.4 0.2 (1.1) (6.2) B & M Jackson Pty Ltd 2.50 1.52%

Pre-Tax Profit A$m (1.1) (1.8) (5.6) (9.4) Mr Ian Bruce Cooper 1.65 1.01%

Tax Expense A$m - - -

-NPAT A$m (1.1) (1.8) (5.6) (9.4) Resources

Abnormal Items A$m - - -

-Reported Profit A$m (1.1) (1.8) (5.6) (9.4) Hera (I + I)

Tonnes Au g/t Ag g/t Pb % Zn % Cu %

2,180,000 4.0 15.6 2.8 3.9 0.2

Financial Position Unit FY2010A FY2011F FY2012F FY2013F

Production Sum m ary Unit FY2010A FY2011F FY2012F FY2013F

Cash A$m 8.4 29.6 19.4 21.7 *Attributable

Other Current Assets A$m 0.2 0.4 1.1 6.3 Payable Zinc Metal 000t - - 0.2 4.4

Total Current Assets A$m 8.6 30.1 20.4 27.9 Payable Copper Metal 000t - - 0.0 0.3

Property, Plant & Equip. A$m 0.5 0.6 70.4 77.1 Payable Lead Metal 000t - - -

-Exploration A$m 20.9 30.4 37.4 39.3 Payable Silver Metal 000oz - - 1.3 24.5

Investments/other A$m - - - - Payable Gold Metal 000oz - - 1.0 18.6

Tot Non-Curr. Assets A$m 21.4 31.0 107.8 116.4 Gold Equivalent 000oz - - 1.6 30.0

Total Assets A$m 30.0 61.1 128.3 144.3 Cash Cost (AuEq) $A/oz - - 1,706 1,006

Short Term Borrow ings A$m - - (40.0) (40.0)

Other A$m (0.6) (0.8) (5.6) (6.4) Price Assum ptions Unit FY2010A FY2011F FY2012F FY2013F

Total Curr. Liabilities A$m (0.6) (0.8) (45.6) (46.4)

Long Term Borrow ings A$m - - - - Gold US$/oz 1092 1383 1458.7 1393.7

Other A$m (1.4) (1.6) (1.6) (1.6) Exchange Rate A$/US$ 0.9 1.0 1.0 1.0

Total Non-Curr. Liabil. A$m (1.4) (1.6) (1.6) (1.6) $A Gold A$/oz 1237 1402 1423.1 1429.4

Total Liabilities A$m (2.0) (2.4) (47.2) (48.0)

Hedging Unit FY2010A FY2011F FY2012F FY2013F

Net Assets A$m 28.0 58.7 81.1 96.3

Total Forw ard Sales - Gold 000oz - - -

-Cashflow Unit FY2010A FY2011F FY2012F FY2013F Forw ard Gold Price $A/oz - - -

-Operating Cashflow A$m (0.6) (0.2) 3.3 5.3 Sensitivity Analysis Valuation ($/s) NPAT EPS (¢) CFPS (¢)

Income Tax Paid A$m - - -

-Interest & Other A$m 0.3 0.2 (1.1) (6.2) Base Case 0.702 -1.8 -1.3 -1.3

Operating Activities A$m (0.3) 0.0 2.3 (0.9) Exchange Rate +10% 0.575 -2.6 -1.3 -1.3

Exchange Rate -10% 0.855 -2.6 -1.3 -1.3

Property, Plant & Equip. A$m (0.3) (0.2) (71.2) (14.2) Gold Price +10% 0.743 -2.6 -1.3 -1.3

Exploration and Devel. A$m (5.0) (9.7) (8.0) (6.0) Gold Price -10% 0.661 -2.6 -1.3 -1.3

Investments A$m (10.9) - - - Copper Price +10% 0.786 -2.6 -1.3 -1.3

Investm ent Activities A$m (16.2) (9.9) (79.2) (20.2) Copper Price -10% 0.617 -2.6 -1.3 -1.3

Operating Co sts +10% 0.61 -2.6 -1.3 -1.3

Repayment of Borrow ings A$m - - - - Operating Costs -10% 0.790 -2.6 -1.3 -1.3

Equity A$m 25.3 33.0 68.0 24.6 *N.B. NPAT, EPS, CFPS forecasts are for FY2011

Dividends Paid A$m - - -

-Financing Activities A$m 23.6 31.1 66.7 23.4 Share Price Valuation (NAV) Est. $m Est. $/share

Net Cashflow A$m 7.1 21.3 (10.3) 2.3 Hera & Nymagee 104.1 0.411

Exploration 50.0 0.197

Ratio Analysis Unit FY2010A FY2011F FY2012F FY2013F Cash 33.0 0.130

Forw ards 0.0 0.000

Cashflow Per Share A¢ (0.6) (0.8) (1.1) 0.7 Corporate Overheads (9.6) (0.038)

Cashflow Multiple X (92.9) (76.2) (53.5) 81.8 Total Debt 0.0 0.000

Earnings Per Share A¢ (1.4) (0.8) (1.9) (2.9) Tax Losses 3.6 0.014

Price to Earnings Ratio X (43.1) (73.9) (31.1) (20.0) Options & Other Equity 1.4 0.006

Dividends Per Share A¢ - - - - Total 182.5 0.72

Dividend Yield % - - -

-Net Debt / Equity % (0.3) na 0.3 0.2 Valuation at Spot 215.3 0.85

Interest Cover X 9.4 na na

-Return on Equity % na na na na (A UDUSD: 1.071 A u:US$ 1,531/o z A g: US$ 38.30/o z Zn: US$ 1.02/lb Cu: US$ 4.17/lb)

Analyst: Mike Millikan Phone: +61 8 9268 2805

Sources: IRESS, Company Information, Hartleys Research

June 2011

Hartleys Limited

YTC Resources Limited

1 June 2011

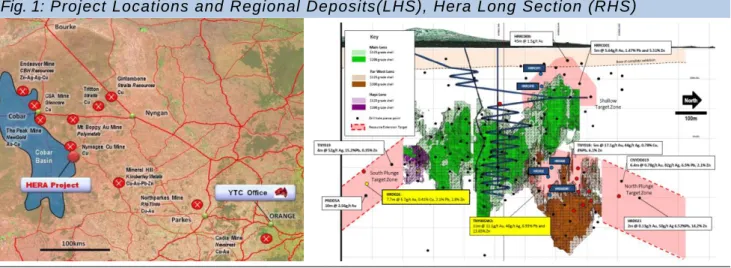

Fig. 1: Project Locations and Regional Deposits(LHS), Hera Long Section (RHS)

Source: YTC Resources Limited

The Hera and Nymagee projects are located ~100km southeast of Cobar in NSW. The Nymagee copper mine

was mined between 1880 and 1917 down to a depth of 250m, producing 422kt of ore at a grade of 5.8% Cu.

The mine is only 5km from Hera. Since the mine closed, the deposit has only seen limited modern exploration.

Fig. 2: Nymagee Long Section (LHS), Cross Section (RHS )

Source: YTC Resources Limited

YTC is drilling out the deposit underneath the previous workings with a view to generating a sufficient size

resource to enable the recommencement of mining at Nymagee to supplement the ore from Hera. As part of

the DFS, the Company is designing the treatment circuit so as to be able to treat the Nymagee high grade

copper ore with the Hera gold and base metals ore. With the two separate mines, the Company should be

able to utilise a larger plant enabling higher copper output, as well as lower treatment costs. Drilling to date

has identified excellent grades and widths of copper, with the high grade (+3% Cu) mineralisation appearing

to be contained within sub-vertical pipes within the overall ore body. The drilling has confirmed that the

mineralisation in the Nymagee Main lode has a consistent strike of at least 300m and remains open at depth.

Hartleys Limited

YTC Resources Limited

1 June 2011

Fig. 3: CSA Cross Section (LHS), Nymagee Cross Section (RHS)

Source: YTC Resources Limited

The Company believes that Nymagee has a number of similarities to the CSA deposit such as the lower grade

halo around and above the massive sulphide mineralisation, the sub-vertical orientation of the lodes, the large

and small scale zoning of the lodes, as well as the mineral assemblages of the lodes.

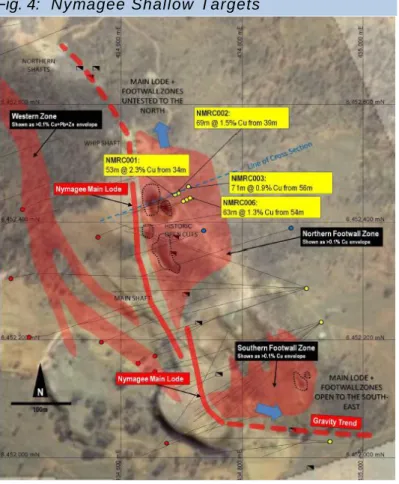

Fig. 4: Nymagee Shallow Targets

Source: YTC Resources Limited

Two new copper lodes

discovered:

12m @ 3.7% Cu from

324m

6m @ 3.75% Cu from

471m

High-grade lodes in

the footwall is

consistent with the

world-class CSA Mine

The CSA mine has

yielded over 1.5Mt of

copper, and has a

vertical extent of over

1.8km.

Drilling (<250m) in the upper parts of

the historic mine continues to intersect

strong Pb-Zn-Ag mineralisation with the

potential to form a substantial target

outside the main copper resource.

RC drilling has discovered shallow Cu

mineralisation in the northern and

southern ends of the Nymagee

mineralised system.

Approvals have been received for

deeper drill holes beneath the main

Nymagee Cu system and approvals for

the shallow Cu mineralised targets are

pending.

YTC expects to have 3 rigs active in the

coming weeks.

HARTLEYS RESEARCH COVERAGE LIST

Hartleys Research Coverage Hartleys Hartleys

Nam e Ticker Last M. CAP Status Research Nam e Ticker Last M. CAP Status Research Price* (A$m ) Recom m endation Price* (A$m ) Recom m endation

Resources Oil & Gas

Gold Conventional Oil & Gas

1. Intrepid Mines Limited IAU 1.83 783 Explorer Speculative Buy 1. Woodside Petroleum Ltd WPL 45.65 35,613 Major Buy

2. Beadell Resources Limited BDR 0.795 494 Developer Accumulate 2. Nexus Energy Ltd NXS 0.39 369 Developer / Explorer Speculative Buy

3. Gold One International Limited GDO 0.505 407 Producer No Rating 3. Tap Oil Ltd TAP 0.93 223 Producer / Explorer Buy

4. Integra Mining Limited IGR 0.460 348 Producer Speculative Buy 4. Carnarvon Petroleum Ltd CVN 0.25 168 Producer / Explorer Accumulate

5. Silver Lake Resources Limited SLR 1.86 332 Producer Buy 5. FAR Ltd FAR 0.11 131 Explorer / Producer Speculative Buy

6. Catalpa Resources Limited CAH 1.740 283 Producer Buy 6. Otto Energy Ltd OEL 0.11 119 Explorer / Producer Buy

7. Tanami Gold NL TAM 0.855 222 Producer Speculative Buy 7. Cooper Energy Ltd COE 0.39 113 Producer / Explorer Buy

8. Focus Minerals Ltd FML 0.074 212 Producer Buy 8. Amadeus Energy Ltd AMU 0.24 72 Producer / Explorer Speculative Buy

9. PMI Gold Corporation Limited PVM 0.650 125 Developer Speculative Buy 9. Haw kley Oil and Gas Ltd HOG 0.32 44 Producer / Explorer Buy

10. YTC Resources Limited YTC 0.575 113 Developer Speculative Buy 10. WHL Energy Ltd WHN 0.04 30 Explorer / Producer Speculative Buy

11. Papillon Resources Limited PIR 0.520 95 Explorer Speculative Buy 11. Sun Resources NL SUR 0.03 12 Explorer / Producer Hold

12. Ausquest Limited AQD 0.160 36 Explorer Speculative Buy

13. Cortona Resources Limited CRC 0.140 27 Developer Speculative Buy 1. Aurora Oil and Gas Ltd AUT 2.85 1,150 Producer / Developer Reduce

14. Emmerson Resources Limited ERM 0.125 25 Explorer Speculative Buy 2. Samson Oil & Gas Ltd SSN 0.135 233 Developer / Producer Buy

15. Canyon Resources Limited CAY 0.370 11 Explorer Speculative Buy 3. Oilex Ltd OEX 0.40 101 Explorer / Producer Speculative Buy

16. Southern Gold Limited SAU 0.079 11 Explorer Speculative Buy 4. European Gas Ltd EPG 0.45 90 Producer / Explorer Speculative Buy

17. Geopacific Resources NL GPR 0.240 9 Explorer Speculative Buy 5. Strike Energy Ltd STX 0.18 59 Explorer / Producer Buy

Iron Ore 6. Entek Energy Ltd ETE 0.14 39 Producer / Explorer Speculative Buy

18. Atlas Iron Limited AGO 3.62 1,978 Producer Buy Sub-Total 38,565

19. Centaurus Metals Ltd CTM 0.081 70 Explorer Speculative Buy Industrials

Coal Resource Services - Capital Intensive

20. Riversdale Mining Limited RIV 17.000 3,203 Developer No Rating 1. Ausdrill Limited ASL 3.27 996 Contract Drilling Buy

Base Metals 2. NRW Holdings Ltd NWH 2.83 794 Contract mining Accumulate

21. Independence Group NL IGO 5.880 1,191 Gold, Ni, Zn, Cu

Producer/Explorer

Buy 3. Mermaid Marine Ltd MRM 3.10 661 Oil & Gas Services Accumulate

22. Aviva Corporation Limited AVA 0.230 31 Explorer Speculative Buy 4. Fleetw ood Corporation FWD 11.38 652 Accomodation Hold

Other m etals 5. Matrix Composites &

Engineering Limited

MCE 8.31 606 Oil & Gas Services Buy

23. Kasbah Resources Limited KAS 0.255 61 Tin Developer Buy 6. Imdex Ltd IMD 2.09 418 Drilling Supplies Buy

24. Shaw River Resources Limited SRR 0.210 53 Manganese:

Explorer/Developer

Speculative Buy 7. Macmahon Holdings Limited MAH 0.54 393 Contract mining Neutral

25. Hazelw ood Resources Ltd HAZ 0.185 42 Tungsten Developer Speculative Buy 8. MACA Ltd MLD 2.44 366 Contract mining Buy

Uranium 9. Pacific Energy Ltd PEA 0.45 156 Remote Pow er Buy

26. Peninsula Energy Ltd PEN 0.083 173 Developer Buy 10. Sw ick Mining Services Ltd SWK 0.38 90 Contract Drilling Speculative Buy

27. Impact Minerals Limited IPT 0.085 10 Explorer Speculative Buy Resource Services - Labour Intensive

Sub-Total 10,348 11. Monadelphous Group Limited MND 19.54 1,681 Construction Buy

12. Decmil Group Limited DCG 3.22 398 Construction Buy

13. Lycopodium Limited LYL 6.41 248 Engineer. & Constr. Accumulate

14. RCR Tomlinson Ltd RCR 1.60 211 Engineer. & Constr. Buy

15. LogiCamms Limited LCM 1.20 80 Engineer. & Constr. Speculative Buy

16. VDM Group Limited VMG 0.16 34 Engineer. & Constr. Speculative Buy

Other Industrial Com panies

17. Seven West Media Limited SWM 4.45 3,406 Media Accumulate

18. Austal Limited ASB 2.94 553 Civil and Military

Vessels

Buy

19. iiNet Limited IIN 2.84 432 Telecommunications Buy

20. Cash Converters Internat. Limited

CCV 0.77 306 Unsecured Finance Neutral

21. Amcom Telecommunications Limited

AMM 0.35 247 Telecommunications Buy

22. RedHill Education Ltd RDH 0.15 4 'For profit' education Neutral

Sub-Total 12,731

Page 6 of 7

HARTLEYS CORPORATE DIRECTORY

Research

Trent Barnett Head of Research +61 8 9268 3052

Mike Millikan Resources Analyst +61 8 9268 2805

David Wall Energy Analyst +61 8 9268 2826

Peter Gray Analyst +61 8 9268 2837

Janine Bell Research Assistant +61 8 9268 2831

Corporate Finance

Grey Egerton-Warburton

Head of Corporate Finance +61 8 9268 2851 Richard Simpson Director - Corporate Finance +61 8 9268 2824 Paul Fryer Director - Corporate Finance +61 8 9268 2819 Dale Bryan Director - Corporate Finance +61 8 9268 2829

Ben Wale Senior Manager - Corporate

Finance

+61 8 9268 3055

Ben Crossing Senior Manager – Corporate Finance

+61 8 9268 3047

Stephen Kite Senior Manager – Corporate Finance

+61 8 9268 3050

Scott Weir Corporate Finance Exec. +61 8 9268 2821

Registered Office

Level 6, 141 St Georges Tce Perth WA 6000 Australia Postal Address GPO Box 2777 Perth WA 6001 Australia Contact Details Telephone: +61 8 9268 2888 Facsimile: +61 8 9268 2800 Website: www.hartleys.com.au Email: [email protected]

Note: personal email addresses of company employees are structured in the following manner:

[email protected] Hartleys Recommendation Categories

Buy Share price appreciation anticipated. Accumulate Share price appreciation anticipated but the

risk/reward is not as attractive as a “Buy”. Alternatively, for the share price to rise it may be contingent on the outcome of an uncertain or distant event. Analyst will often indicate a price level at which it may become a “Buy”.

Neutral Take no action. Upside & downside risk/reward is evenly balanced.

Reduce / Take profits

There is unlikely to be further gains over the investment time horizon but there is a possibility of some price weakness over that period.

Sell Significant price depreciation anticipated.

No Rating No recommendation.

Speculative Buy Share price could be volatile. While it is anticipated that, on a risk/reward basis, an investment is

attractive, there is at least one identifiable risk that has a meaningful possibility of occurring, which, if it did occur, could lead to significant share price reduction. Consequently, the investment is considered high risk.

Institutional Sales

Carrick Ryan +61 8 9268 2864

Justin Stewart +61 8 9268 3062

Simon van den Berg +61 8 9268 2867

Steven Boyce +61 8 9268 2817 Nick Wheeler +61 8 9268 3053

Wealth Management

Nicola Bond +61 8 9268 2840 Bradley Booth +61 8 9268 2873 Adrian Brant +61 8 9268 3065 Nathan Bray +61 8 9268 2874 Sven Burrell +61 8 9268 2847 Simon Casey +61 8 9268 2875 Tony Chien +61 8 9268 2850 Travis Clark +61 8 9268 2876 David Cross +61 8 9268 2860 Nicholas Draper +61 8 9268 2883 John Featherby +61 8 9268 2811 Ben Fleay +61 8 9268 2844 John Georgiades +61 8 9268 2887 John Goodlad +61 8 9268 2890 Andrew Gribble +61 8 9268 2842 David Hainsworth +61 8 9268 3040 Neil Inglis +61 8 9268 2894 Murray Jacob +61 8 9268 2892 Gavin Lehmann +61 8 9268 2895 Shane Lehmann +61 8 9268 2897 Steven Loxley +61 8 9268 2857 Andrew Macnaughtan +61 8 9268 2898 Christian Marriott +61 8 9268 2828 Scott Metcalf +61 8 9268 2807 David Michael +61 8 9268 2835 Damir Mikulic +61 8 9268 3027 Nicole Morcombe +61 8 9268 2896 Jamie Moullin +61 8 9268 2856 Chris Munro +61 8 9268 2858 Michael Munro +61 8 9268 2820 Ian Parker +61 8 9268 2810 Ian Plowman +61 8 9268 3054 Margaret Radici +61 8 9268 3051Charlie Ransom (CEO) +61 8 9268 2868

Elliott Rowton +61 8 9268 3059 Conlie Salvemini +61 8 9268 2833 David Smyth +61 8 9268 2839 Greg Soudure +61 8 9268 2834 Sonya Soudure +61 8 9268 2865 Dirk Vanderstruyf +61 8 9268 2855 Alex Wallis +61 8 9268 3060 Marlene White +61 8 9268 2806 Samuel Williams +61 8 9268 3041

Disclaimer/Disclosure

The author of this publication, Hartleys Limited ABN 33 104 195 057 (“Hartleys”), its Directors and their Associates from time to time may hold shares in the security/securities mentioned in this Research document and therefore may benefit from any increase in the price of those securities. Hartleys and its Advisers may earn brokerage, fees, commissions, other benefits or advantages as a result of a transaction arising from any advice mentioned in publications to clients.

Hartleys has completed a capital raising in the past 12 months for YTC Resources Limited for which it has earned fees. Hartleys has also provided corporate advice within the past 12 months and continues to provide corporate advice to YTC for which it has earned fees and continues to earn fees.

Any financial product advice contained in this document is unsolicited general information only. Do not act on this advice without first consulting your investment adviser to determine whether the advice is appropriate for your investment objectives, financial situation and particular needs. Hartleys believes that any information or advice (including any financial product advice) contained in this document is accurate when issued. Hartleys however, does not warrant its accuracy or reliability. Hartleys, its officers, agents and employees exclude all liability whatsoever, in