D EPAR T MENT O F BU SIN ESS AD MIN ISTR AT IO N BU SIN ESS AN D SO C IAL SC IEN C ES

AAR H U S U N IVER SIT Y

Analysing Public-Private Partnership

Master thesis

MSc in Finance and International Business

Author: Jurgita Jakutyte Student ID: JJ91185 Academic supervisor: Jingkun Li

Page | 2

TABL E OF C

ONT E NT S Introduction ... 5 Problem statement ... 6 Structure ... 7 Delimitations ... 9 1. Literature review ... 11 1.1. Definition ... 11 1.2. Types of PPPs ... 161.3. Reasons for implementing PPPs ... 19

1.4. value for money ... 21

1.5. Advantages and disadvantages of PPP ... 26

1.6. Criticism of PPPs ... 29

2. Analysis ... 32

2.1. The project ... 32

2.2. Alternatives for project implementation ... 32

2.3. Identifying an appropriate PPP scheme ... 34

2.3.1. Overview of Lithuania’s legal PPP environment ... 34

2.3.2. Choosing a PPP scheme ... 38

2.4. Cost and benefit analysis ... 39

2.4.1. Assumptions overview ... 40

2.4.2. Data overview ... 46

2.4.3. Financial analysis ... 48

2.4.4. Socio-economic analysis ... 49

2.4.5. Sensitivity analysis ... 52

2.4.6. Overview and the discussion of the CBA results... 56

2.5. Factors not covered by CBA ... 58

3. Conclusions ... 63

4. Bibliography ... 66

Page | 3

CONT E NT OF F

IGURESFigure 1. European PPP trend, 1990-2009 ... 6

Figure 2. Cash flows in PPP and traditional procurement mode ... 16

Figure 3. Structure of Public Sector Comparator ... 22

Figure 4. Optimal risk allocation point ... 23

Figure 5. Model for risk allocation ... 24

Figure 6. Identifying Value for Money ... 26

Figure 7. PPP scheme under economic activity... 37

Figure 8. PPP scheme under social activities ... 38

Figure 9. Sensitivity analysis – FNPV on investment... 53

Figure 10. Sensitivity analysis – FNPV on capital ... 54

Figure 11. Sensitivity analysis - Socio-economic results ... 55

CONT E NT OF

TABL E S

Table 1. Distribution of investment costs, % ... 46Table 2. Financial return on the investment costs –PPP and traditional procurement approach ... 48

Table 3. The structure of financing in PPP and traditional procurement approach 48 Table 4. Financial return on capital – PPP and traditional procurement approach 49 Table 5. Assumptions for the socio-economic analysis ... 51

Table 6. Net benefits of non-market impact ... 51

Table 7. Socio-economic analysis results ... 52

Page | 4

LIST OF

ABBRE V IAT IONS

BBO Buy-Build-Operate

BOOT Build-Own-Operate-Transfer BOT Build-Operate-Transfer CBA Cost-Benefit Analysis CO2 Carbon dioxide

CPVA Central Project Management Agency DBFO Design-Build-Finance-Operate

DBOM Design-Build-Operate-Maintain

EPEC European Public-Private Partnership Expertise Centre EIB European Investment Bank

ENPV Economic net present value of investment EU15 European Union of 15 member states

FNPV/C Financial Net Present Value of the Investment FNPV/K Financial Net Present Value of Capital

FRR/C Financial Rate of Return of the Investment FRR/K Financial Rate of Return of Capital

IMF International Monetary Fund

Kg Kilogram

Km Kilometre

OECD Organization for Economic Co-operation and Development PPP (3P) Public-Private Partnership

PSC Public Sector Comparator PwC PricewaterhouseCoopers SPV Special Purpose Vehicle STPR Social Time Preference Rate

t

tonnetkm tonne-kilometre VAT Value Added Tax VFM Value for Money

Page | 5

INT RODUCT ION

PPP (3P) – public-private partnership – a concept used widely in the public procurement that lacks both clarity and united definition (Meidute & Paliulis, 2011). The concept has no clear boundaries for distinguishing what kind of private and public partnership is assumed to be a form of PPP or a form of a traditional procurement. This results in some confusion, both in the academic literature, as well as within the international experiences. Nevertheless, PPP, in general terms, could be defined as a long term contractual relationship between a public and private sectors, which is usually characterised by having features such as bundling of functions, exchange of resources, shared responsibility, risks and rewards, and is arranged with the aim to provide a public service/asset.

PPP is not a new phenomenon even though it is perceived as such due to its recent popularity. Growing interest is a result of changing attitudes as well as expectations of the society towards the government and public services (Grimsey & Lewis, 2004). Today society expects to see the government more as a governor and regulator rather than the direct provider of public services. In addition, it requires infrastructure of better quality, more efficient provision of public services, as well as better use of public money. Considering all this, PPPs are seen as a procurement mode that may satisfy these changing needs. Nevertheless, PPPs are not a ‘miracle’ solution (European Commission, 2003; Harris, 2004; Meidute & Paliulis, 2011) to the problems of the conventional procurement; they are complex and expensive and, as a result, only certain projects qualify for the use of public-private partnerships.

The figure below shows the trend of growing interest in the use of PPP within Europe for the period of 1990 – 2009. It is important to note that between 1990 and 2004 from all PPP projects more than half were arranged in the United Kingdom. Only recently the trend has changed and other European countries have experienced increased use of PPPs (EIB, 2010).

Page | 6 Figure 1. European PPP trend, 1990-2009

Source: Adopted from EIB (2010, p. 7)

Even though, the numbers are increasing, the portion of PPP projects in the overall public procurement is still not that significant (Appendix 1). For example, in the United Kingdom, the biggest producer of PPP projects, public private partnerships represent only 10-13% of all public infrastructure projects (Deloitte Research, 2006).

Having this in mind, the question rises, why PPPs represent such a small fraction of all public projects if they deliver benefits such as greater efficiency, timely delivery of public projects, better quality of service provision, etc.? In order to try to answer this, the paper examines the concept of public-private partnership and reviews the advantages, disadvantages, and the reasons why PPPs are implemented. In addition, the case study is perf ormed where the conventional procurement approach is compared to public-private partnership. The paper investigates what PPPs are, what they deliver and when they prevail over the conventional procurement approach.

PROBL E M ST AT E ME NT

The aim of the paper is to analyse the concept of public private partnership and its suitability for a procurement of a public project. The objectives of the thesis are achieved by reviewing the relevant literature and performing an analysis on the

0 20 40 60 80 100 120 140 160 0 5.000 10.000 15.000 20.000 25.000 30.000 35.000 Nu m b e r o f p ro je c ts V a lu e o f p ro je c ts , m ln . € Years

Page | 7 case study by examining the different procurement approaches available for the project: PPP and conventional procurement. The analysis will answer which procurement approach should be the appropriate one for the case study concerned.

ST RUCT URE

The paper is divided into two main parts. The thesis is structured in the way that from the very beginning an understanding of the concept of PPP could be developed, which is used for the second part of the thesis, where the analysis is performed.

The first part of the thesis provides an extensive discussion on the theoretical foundations of public private partnerships. It focuses on the discussion of the relevant concepts, characteristics, types, advantages and disadvantages of the PPP. The first part of the paper answers questions, such as: what PPPs are, why such a procurement mode is practiced and how it differs from other procurement approaches, such as conventional procurement and privatisation.

The second part of the thesis is the analysis of the case study. It is divided into two main sections. The first section includes an overview of the project’s background and its adequacy for a PPP. It further includes a review of the Lithuanian environment regarding PPP law and provides a discussion on the suitable PPP form for the infrastructure project concerned. The second section of part two consists of the cost and benefit analysis, which involves the following steps:

Data overview (identification of costs and benefits, assumptions);

Financial analysis;

Socio-economic analysis;

Sensitivity analysis;

Page | 8 In addition, the second part of the thesis is expanded with a discussion on other factors that are not covered by CBA, however, factors that are relevant when a PPP approach is considered.

The last part of the paper concludes the discussion on public-private partnerships and the analysis performed.

MET HODOL OGY

The paper is written by following the deductive, in other words, a “top-down” approach. The paper begins with the general overview of the theory and then narrows down to the analysis of a specific case study. In addition, the paper is based on the secondary sources.

The first part of the paper emphasises on the literature review. The literature review is based on the European Commission, EPEC, Hong Kong Efficient unit, Victoria Partnership guidance on PPPs, reports of OECD, IMF, PwC, Deloitte, and views provided by a variety of PPP researchers – such as Grimsey and Lewis, Akintoye, Hodge, etc. The articles, books and reports used in the paper were accessed through a variety of research databases, such as OECD iLibrary, Science Direct, Business Source Complete, etc.

The second part of the paper emphasises on analysing a particular public-private partnership project. The analysis is carried out by performing a cost-benefits analysis (CBA) while employing guidance of the European Commission: “Guide to Cost Benefit Analysis of Investment projects: Structural Funds, Cohesion Fund and Instrument for Pre-Accession” (2008) and “Guide to cost benefit analysis of investment projects” (2002). Some additional insights for the application of CBA have been adopted from OECD (2006), Boardman, Greenberg, and Vining (2011) and Campbell and Brown (2003).

Cost and benefit analysis is a technique used to identify, measure and compare benefits and costs of an investment project and it is used to assist the decision maker in choosing the most beneficial project from the alternatives available

Page | 9 (Campbell & Brown, 2003). In this paper cost and benefit analysis is used as a tool to determine the main differences between procuring a project through a traditional procurement mode and a PPP. It should be noted that the CBA used in this paper does not try to compare different project implementation alternatives1. The idea of the analysis is to compare the same project financed by public and private funds. Therefore, it could be said that the aim the cost and benefit analysis performed in this paper is to understand whether the inclusion of the private partner in the public procurement influences the investment decision rule – whether to proceed with the project or abandon it instead.

The addition to CBA is an overview of other factors that are not incorporated in the aforementioned analysis, which, however, are influential when the choice of procurement approach is considered. The discussion on these factors is performed in accordance to the theory overview of the first part of the thesis.

DEL IMIT AT IONS

The concept of public-private partnership encompasses a variety of different partnerships and relationships, which are not covered fully in the thesis. The paper focuses on one particular PPP infrastructure approach, within which the topic is analysed.

What concerns the second part of the paper, due to time constraints and size limitations, the CBA is performed only to the level that is enough to identify the most important points regarding the differences between procuring a project through PPP and conventional procurement approach. In addition, due to the complexity and extent of the project, the analysis has been simplified and only most important impacts taken into account. As a result, there is possibility for some divergence between results presented in the paper and the reality. Further development on the CBA could be made if more specific studies were conducted: for example, a detailed market demand analysis or more specific environmental

1

The paper does not intend to compare the usual cost and benefit analysis’ alternatives: “Business as usual”, “Do minimum”, “Do something”, “Do something else” (European Commission, 2008).

Page | 10 studies examining the CO2 emission, air pollution, etc. Moreover, due to the lack of relevant information, which is a consequence of the absence of the analogues projects in Lithuania, most of the assumptions are based on the foreign countries’ experience, especially of the more developed Western economies, which might be highly inaccurate when situation in Lithuania is considered. With addition to this, it is a nature of CBA to use a variety of assumptions, which might sometimes appear to be imprecise, in particularly, when a long term project is analysed.

Page | 11

1. L

IT E RAT URE REV IE W1.1. D

EF I N I T I ONPublic private partnership (PPP), in simple terms, is a form of private-sector involvement (PSI)2 in which a private partner brings its skills, capital, commercial innovation into the provision of the services the government is responsible for. It should be noted, however, that such an explanation covers only a part of this broad concept. It is widely acknowledged within the relevant literature that there is no clear definition for PPP which would cover all aspects of different relationships that these partnerships encompass (Daube, Vollrath, & Alfen, 2007; Hodge & Greve, 2007; OECD, 2008) and at the same time restricting it to a more narrow description. As Weihe (2006) argues, the concept of PPP is nebulous – it “allows for great variance across parameters such as time, closeness of cooperation, types of products/services, costs, complexity, level of institutionalization as well as number of actors involved”, as a result, nearly any type of the relationships that include both the private and the public sector (whether it is a service contract or a joint venture) may be called a public-private partnership (PwC, 2005). In order to make some distinction between the variety of definitions present, Weihe (2006) attempted to classify them into 5 categories: local regeneration, policy, infrastructure3, development and governance approaches. The local regeneration and the policy approaches are similar due to perceiving PPP concept as a very wide definition that covers changes in policies of environment, economic renewal, development, and institutional set up. The difference between the two is that the local regeneration approach focuses on the local level while policy approach – on the national. The third approach – the infrastructure approach – covers the cooperation of private and public sector in order to create and maintain

2 Private-sector involvement is a new focus of EU which has been created in order to “assist the government in

meeting its priorities, building on the clear recognition that public funds are limited” (Tanga, Shena, & Chengb, 2010, p. 684).

3

In order to define infrastructure, we use the definition provided by Grimsey and Lewis (2004, p. 20): “investment in infrastructure on some definitions is said to provide ’basic services to industry and households ’, ‘key inputs into the economy and ‘a crucial input to economic activity and growth’”. Infrastructure approach in PPP does not cover such infrastructure as “coal or steel or motor vehicles”, it concerns infrastructure like roads, motorways, ports, airports, telecommunication, prisons, schools, etc.

Page | 12 infrastructure, as well as deal with the financial and legal aspects of such projects. The fourth approach – the development approach – concentrates on the development of infrastructure in developing countries where corruption, social deprivation, global disasters are present. This approach includes many forms of cooperation between the public and private sectors such as strategic or entrepreneurial partnerships. The last approach is the governance approach which does not specify any context or policy as it emphasizes on organizational and management side, as well as new ways of cooperation and governing. For the purpose of this thesis, the concept of PPP will be limited to the infrastructure approach.

Even thought the concept has been narrowed down, there are still many definitions explaining what a PPP is under the approach chosen. For example, the European Commission (2004, p. 3) defines PPPs as “forms of cooperation between public authorities and the world of business which aim to ensure the funding, construction, renovation, management or maintenance of an infrastructure or the provision of a service”; whereas OECD (2008, p. 12) defines it as “an arrangement between the government and one or more private partners (which may include the operators and the financers) according to which the private partners deliver the service in such a manner that the service delivery objectives of the government are aligned with the profit objectives of the private partners and where the effectiveness of the alignment depends on a sufficient transfer of risk to the private partners”. Further examples of definition include the one proposed by IMF (2006, p. 1) that explains the concept as the “arrangements where the private sector supplies infrastructure assets and infrastructure-based services that traditionally have been provided by the government”, and EIB (2004, p. 2) that views PPP as a relationship of the two sectors which has an aim “of introducing private sector resources and/or expertise in order to help provide and deliver public sector assets and services…<it is> used to describe a wide variety of working arrangements from loose, informal and strategic partnerships, to design build finance and operate (DBFO) type service contracts and formal joint venture companies”. An overview of the PPP definitions under the variety of international organizations draws some

Page | 13 conclusions on the basic set of features that characterise PPP under the infrastructure approach:

long term contractual arrangement between the public and private sector;

functions are bundled;

responsibility for the provision of the services is shared;

resources are shared:

o the private sector brings in capital, skills, experience, commercial innovation, etc.;

o the public sector delivers skills, political authority, access to publicly run services, assets, etc.;

risks and rewards are shared.

In order to understand the PPP concept fully, it is also useful to distinguish it from the traditional procurement mode. The reason for this is that the boundaries between the two modes are ambiguous. In order to remove this ambiguity the main differences between the two modes are identified and explained.

First of all, the main differentiating point between PPP and traditional procurement is that in PPPs risks are shared between the private and public partners whereas in a conventional procurement most of the risks are retained by the government4 (European Commission, 2005; OECD, 2008) . This is in line with the functions included in the contracts. In a PPP different tasks are bundled together and, as a result, private partner takes responsibility for the whole package of the associated risks. In the conventional procurement, on the other hand, the government usually purchases a single function from a private partner and, as a result, the private partner is responsible only for the risks associated with this function. Consequently, in the traditional procurement the private partner has no incentives to incorporate decisions that may favour future operations as after completion of the task, the private partner is no longer involved in the operations of the asset/service. For

4

Because there is no single clear definition for PPP, the most important factor that distinguishes the procurement mode and the type of PPP used is the amount of risk and responsibility transferred to the private partner (European Commission, 2005, p. 1).

Page | 14 instance, if the government proposed a tender to deliver a package of services, such as design, build and maintain a facility, the private partner involved would be incentivized from the very beginning to make decision that could minimize the future risks associated with cost overruns. Such an example has been identified in the international experience by Grimsey and Lewis (2004, p. 135), where an innovative decision to construct 45-degrees windowsills in UK hospital was proposed with an intention to save future cleaning costs. It is hardly likely that such a decision would have been made in the conventional procurement case. A government would propose a tender to design a facility with input requirements already specified. The specific requirements can be seen as a frame from the private partner’s point of view as these requirements restrict private partner to innovate and come up with more efficient solutions. The aim of the private partner responsible for a design function is to design a facility while incorporating all the details required and within the budget stated. The review of function bundling and risk allocation in both procurement cases help to determine what defines a PPP and a traditional procurement approach.

Secondly, the two modes differ between each other when the function specification is considered. What this means is that, in a PPP, government states what it expects from the private partner in output terms, whereas in the conventional procurement it does that through input specification. Considering the aforementioned example, in a PPP case, government might require a hospital to be big enough to accommodate 300 people and to be kept in a good condition by clarifying what good condition means, whereas in the conventional procurement option, a government would request a certain size, with a certain number of rooms, with specific materials used, etc. In the PPP case, private partner is free to use its skills and innovation in order to provide the outputs required in a most efficient way, whereas the latter case does not allow such a freedom as a private sector is restricted to the requirements specified.

Thirdly, in a PPP approach, returns to the private partner are linked to the performance of their functions, i.e. the provision of outputs specified by the

Page | 15 government, whereas in a conventional procurement approach, private partner is remunerated for the completion of a specific function. This contributes to the level of incentives attached to the private partner: in a PPP case, if a private partner does not operate as expected, it might incur some sort of penalties (Harris, 2004), if it operates better than expected, it may be awarded by, for example, receiving higher portion of additional profits. In a traditional procurement case, on the other hand, private partner is not awarded for an extra value added to the task it was responsible for, however, it might be penalized f or the uncompleted function. Considering all this, the private partner in a traditional procurement is not encouraged to provide more than the government requested for, which means some possible gains might be overlooked.

Fourthly, the relationships involved in both of the procurement modes differ (OECD, 2008). In the traditional procurement, in order to deliver the services and infrastructure required, the government acts as an intermediary – on the one side it deals with direct users of the services, taxpayers, and financial markets, and on the other side – with other private companies. The idea behind such a relationship structure is that the government gathers financing directly from the users of the service, taxpayers and financial markets, and uses it to remunerate the other side – the private companies for the capital goods provided to deliver the public service and develope the infrastructure. If the project is handled through a public-private partnership, the intermediary role of the government is decreased – public authority deals with the taxpayers and the single private operator only. The role of the private operator, on the other hand, is enhanced: private operator becomes responsible for the intermediary role – it collects financing from the direct users of the service and financial markets and remunerates the other side – other private companies for the capital goods provided. If the private operator acts in accordance to the performance standard specified, in some of the cases5, it receives additional payment from the government (Maski & Tirole, 2008). The relationship structures of the two schemes are represented in the Appendix 2.

5

The private operator may be remunerated through: the collection of direct user charges only, through the government payment only, or through a combination of both (Grimsey & Lewis, 2004).

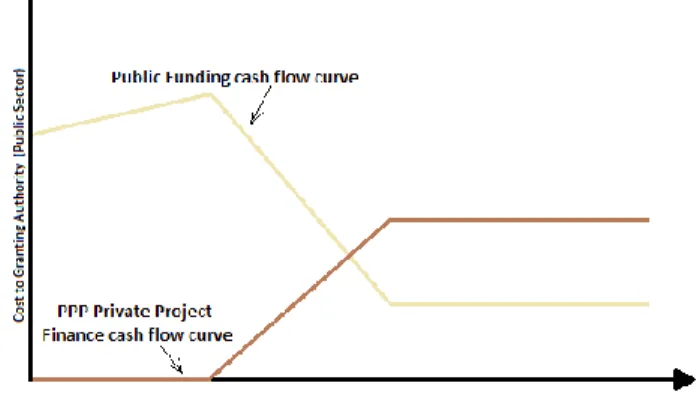

Page | 16 Finally, a crucial advantage of PPP from a government’s point of view is the financing. In a PPP case capital is provided by the private partner. This means that the government does not incur immediate cash outflow due to the project, which might be an impossible task when restricted public funds are considered. In a traditional procurement mode, on the other hand, the government finances the project from its own funds, that is it incurs large investment costs instantly. Figure 2 represents the comparison between the two financing options in the public procurement.

Figure 2. Cash flows in PPP and traditional procurement mode

Source: Akbiyikli, Eaton, and Turner (2006, p. 71)

All in all, the two modes differ between each other when the following factors are considered: amount of risks transferred and tasks bundled, the way requirements for the service delivery are specified, characteristics of private partners returns, relationship between the parties involved and the financing flows. Nevertheless, it is clear that sometimes these differences may be too ambiguous or too subjecitve to state clearly which procurement approach is adopted.

1.2. T

Y PES OFPPP

SThe spectrum of different PPPs range from the short term service contracts to concessions. Nevertheless, as the focus of this thesis is the concept of PPP under an infrastructure approach, the overview of different PPP modes will be limited to the ones that are covered by the PPP approach chosen. These modes have

Page | 17 common characteristics, such as: being long term, involving risk transfer, shared responsibility, resources and rewards.

In general, private partner involvement arrangements in PPPs differ between each other depending on the level of responsibilities and risks transferred to the private partner (Amekudzi & Morallos, 2008). The responsibilities concerned include activities such as: designing, building, financing, maintaining, operating, and owning the facilities. The allocation of risks will be discussed in more detail later in the paper; however, what matters at this point is the amount of risks transferred and retained by the government.

Most common forms in the infrastructure approaches are:

Turnkey procurement, which includes: BOT (build-operate-transfer), BBO (buy-build-operate), etc. (European Commission, 2003, 2005);

DBFO (Design-Build-Finance-Operate), which includes: DBOM (design-build-operate-maintain), BOOT (build-own-operate-transfer), concessions, etc. (Deloitte Research, 2006; European Commission, 2005; IMF, 2004). Turnkey procurement6 is described as the scheme where the private partner takes on the responsibility to design, construct and operate the asset, whereas the public sector retains the responsibility for the financial risks involved. Using this procurement mode, public sector sets the quality outputs required and by doing so it ensures that the private sector brings the necessary efficiency gains as well as the asset is maintained to the standards expected. This mode of procurement is used in water and waste projects as it ensures incentivized management and maintenance of the asset through the bundling of functions passed on to the private partner (European Commission, 2005).

DBFO scheme7 is characterized by involving a private partner with responsibilities (financing, designing, building, constructing, and operating the asset/service) attached to it. Public sector’s role is to set the specific output requirements for the

6

See Appendix 3 for illustration of the turnkey procurement’s scheme.

7

Page | 18 private partner, whereas private partner’s role is to fulfil those requirements. The DBFO schemes are usually long term and involve bundling of functions in order to provide private partners with the necessary incentives for it to operate in the most efficient and innovative way. These schemes involve performance linked payment mechanisms with an aim to ensure the presence of motivation for the private partner to operate on its full capacity. The idea behind such schemes is that the private partner designs, builds, operates and maintains the asset for the agreed term. At the end of this term, the asset is either transferred back to the government or is left under the ownership of the private partner – depending on the specific structure of the scheme chosen. For example, one of the most common schemes under DBFO is concession. Concession is described as a PPP scheme, where exclusive rights to operate an asset or provide certain services are granted to a private company (usually a SPV8), which in return has to design, build, finance and operate the asset/service for the time agreed upon. These exclusive rights usually permit the private partners to collect the revenues from the direct users of the asset/service. Concessionaires typically own the rights to the asset/service during the time of concession, however, at the end of this period the ownership of the asset/service is usually transferred back to the public sector (Deloitte Research, 2006; European Commission, 2005; IMF, 2006). Literature overview shows that concession is usually assumed to be a form of PPP (Deloitte Research, 2006; European Commission, 2004; IMF, 2006; Ng, Xie, Cheung, & Jefferies, 2007; PwC, 2005), however, OECD (2008) argues the opposite. First of all, it states, that the amount of risk transferred differs in PPPs and concessions: concessions involve higher level of risks allocated to the private partner, compared to other forms of PPPs. Secondly, it is usual for concessionaires to collect revenues from the direct users of the asset/service and, according to OECD, this feature differentiates concession from other PPP forms. As a result, OECD concludes that concessions should not be treated as a PPP. Nevertheless, in this paper concession is considered as a form of PPP.

8

SPV (special purpose vehicle) – “an organization that can be established as a distinct legal entity to bring together the companies involved in a PPP in order to manage the project and share the risks and rewards”

Page | 19 The international experience shows that most of the time DBFO schemes are used in transport sector for building highways, bridges, railways, whereas concessions are chosen for mobile phone services, toll roads or provision of municipal water. The similarities between the turnkey procurement and DBFO schemes are that the activities involved are same in both of the schemes, differing only in the amount of functions involved in the arrangements. What differentiates the two schemes is that in the first one the majority of risks remains within the public sector, whereas in the latter – risks are shared between the partners, allowing for the possibility to transfer the optimal amount of risks to the private partner.

1.3. R

E AS ON S F OR I M PL EM EN T I NGPPP

SThe main objective of procuring a public project through a PPP mechanism is to achieve value for money (VFM) (Grimsey & Lewis, 2004; Harris, 2004; New South Wales Government; Quiggin, 2004; Shaoul, 2005) which as Grimsey and Lewis (2005, p. 347) argue is “the optimum combination of whole life cycle costs, risks, completion time and quality in order to meet public requirements”. This definition assents to the one implied by the European Commission (2003, p. 55) which identifies a set of factors that determine value for money: life cycle costs, allocation of risks, time required to implement a project, quality of a service, and ability to generate additional revenues. Following this, a general principal used to determine whether a project should be implemented through a PPP or a traditional procurement is to evaluate which procurement mode ensures lower life cycle costs, better allocation of risks, quicker implementation, higher quality and additional profits. In other words, additional value for money represents additional efficiency gains – delivering or maintaining the same service or asset in a more cost efficient or a more qualitative way than it would have been if the government retained the full responsibility for delivering/maintaining service/asset concerned (EIB, 2004, p. 4; Meidute & Paliulis, 2011; Nisar, 2006). EIB (2004) argues that the critical aspect in order to reach value for money is the ability to share risks and rewards appropriately. OECD (2008) confirms this view recognizing that main reasons for

Page | 20 PPP establishment are the appropriate risk allocation and value for money gains9. Grimsey and Lewis (2005, p. 347), however, imply that the value for money gains can only be achieved if the following conditions are present: a competitive environment, optimal risk allocation and if the comparison between the financing options is handled in a “fair, realistic and comprehensive” way. Furthermore, when questioning PPP’s ability to deliver additional gains, one should consider the qualitative benefits of PPPs – whether they are achievable and whether they really provide the benefits expected. It is essential therefore to check whether the private partner is capable of bringing in skills that the government lacks and whether it has the expertise and know-how necessary to operate more efficiently compared to the government (PwC, 2005).

According to the literature review, further reasons that lie behind the use of PPP as a procurement mode differ between countries depending on the environment present. For example, the main aim of a PPP at the early stage of its development in the United Kingdom was to finance the public infrastructure projects (Grimsey & Lewis, 2004; IMF, 2006; Meidute & Paliulis, 2011). The issue at that time consisted of a growing need for public infrastructure development (as it also is the case in Hong Kong (Cheung, Chan, & Kajewski, 2009)) and a lack of available public funds to finance this need. As a result, a new initiative took place – Private Finance Initiative (PFI) – with the purpose to provide additional funds for public infrastructure projects. On the other hand, countries like Australia do not have such an issue. They are capable of financing projects by themselves, however, they still choose to involve the private sector for the possibility of achieving additional value (Cheung et al., 2009). Moreover, Hong Kong and Australia involve a private partner into the procurement of public services with the aim to ensure a better quality of services. This, on the other hand, does not seem to be the prioritized reason for the PPP development in the United Kingdom, which

9

The gains associated with the inclusion of the private partner are based on the assumptio n that the private partner has more to offer than the public entity could realize by itself - it is assumed that the private partner will bring more innovative and cost efficient solutions in addition to a better management. Nevertheless, caution should be taken here that the mere inclusion of the private partner will not be sufficient to generate value for money required (OECD, 2008, p. 18).

Page | 21 emphasizes the point that reasons to implement PPP depend on the circumstances surrounding countries’ economic and political environment.

In many of the countries the choice for PPPs, however, is due to financial reasons (such as lack of public funds and restricted public investment). This reason is amplified when “a tight fiscal environment following the development of European Monetary Union” (EIB, 2004, p. 4) is considered as due to this European countries experience difficulties in organizing large investment sums to finance public infrastructure projects from the public funds only.

All in all, in theory, the main reason to develop PPPs lies behind the concept of value for money, creating additional benefits due to private partner’s expertise, know-how, ability to operate efficiently and generate additional revenues. Despite the theoretical foundations, it is evident that PPPs are also often used in cases when there is a lack of public funds for the growing need for public infrastructure.

1.4.

V AL U E F OR M ON EYThe concept of value for money is ambiguous and in order to understand it better, it is worth analysing the estimation procedure for it. When estimating the value for money that a partnership creates, governments have to choose between four methodologies: CBA of public and private partner proposals, PSC-PPP comparison before the tender, PSC-PPP comparison after the bidding process, and identification of value for money through the competitive bidding process (Grimsey & Lewis, 2005; Sarmento, 2010). The literature review shows that the calculation of PSC (public sector comparator) and comparison of it with the PPP option before the tender is the most commonly used method. The purpose of public sector comparator is to verify that value for money is generated (Harris, 2004; Quiggin, 2004) and in order to do this “the hypothetical risk-adjusted cost if a project were to be financed, owned and implemented by the government” (Partnerships Victoria, 2001, p. 6) should be calculated. The calculation of such costs is done by estimating four elements: raw PSC, competitive neutrality, transferable and retained risks, all of which are represented in the figure below:

Page | 22 Figure 3. Structure of Public Sector Comparator

Source: Partnerships Victoria (2001, p. 6)

To begin with, the first component – raw PSC – includes the calculation of project’s base costs as if the government would procure the project through the conventional method. It includes identifying and calculating project’s direct (capital, maintenance, operating costs) and indirect costs (overheads, administrative costs) as well as any revenues incurred (Amekudzi & Morallos, 2008). The next component – competitive neutrality – involves adjusting the cash flows in order to remove any competitive advantages or disadvantages that the government may have over the private sector (Amekudzi & Morallos, 2008; Partnerships Victoria, 2001). The advantages and disadvantages concerned may be due to differ ent aspects of the taxing system applicable to the public and private sectors. For example, land and income tax rates may differ as government authority may receive exemption whereas bidder may not. In addition, competitive neutrality adjustments may rise due to differing regulatory requirements for the partners concerned. The third and fourth elements of PSC calculation concern the estimation of transferrable and retainable risks, where risks are identified, allocated and priced. The price of risks transferred to the private partner should be included in PSC value. Transferrable risk element together with retained risk element ideally should ensure the optimal allocation of risks between the partners involved in the project.

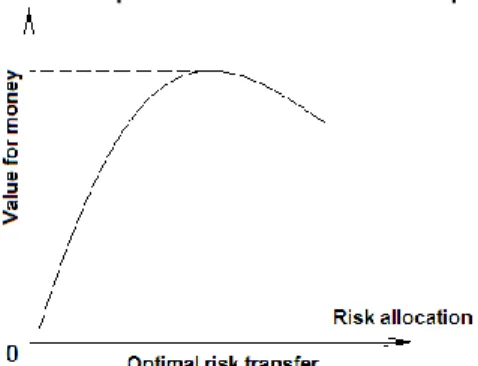

The allocation and valuation of project’s risks is inherent in the value for money concept (European Commission, 2003; Grimsey & Lewis, 2004; Nisar, 2006;

Page | 23 Sarmento, 2010). The aim of the risk transfer is to transfer only those risks that the private partner could offset in a most efficient and least costly way(Grimsey & Lewis, 2004; Harris, 2004; Nisar, 2006). Risk allocation produces highest value for money once the optimal risk transfer point is identified (Figure 4): transferring too much or too little risks results in either procuring an inefficient project or procuring a project with excess costs incurred by the government (for example, if risks are transferred to the private partner that it does not have control over or cannot control it at least-cost, then the private partner will require higher premium for these additional risks assumed (Hodge, 2004)), consequently, producing lower value for money (Amekudzi & Morallos, 2008).

Figure 4. Optimal risk allocation point

Source: Partnerships Victoria (2001, p. 52)

Unfortunately, there is no universal solution regarding risks allocation for every single project, however, there is a general agreement on how different risks should be allocated. To begin with, risks in general are allocated to different categories, such as, for example, proposed by OECD (2008): legal and political risks in addition to the commercial ones. Categories are differentiated on the basis of who takes the responsibility for the risks concerned – private partner or the government authority. For example, construction, supply and demand side risks lie under the commercial risk category (market risk, project risk and internal risk) as they are handled better by the private partner, whereas legal and political risks are assumed to be handled better by the government. Other categorization is proposed by Li, Akintoye, and Hardcastle (2001), who distribute risks into three levels: macro, meso and micro. Macro level covers risks outside the project – environmental, political, legal risks that are concerned with national or industry level. Meso level

Page | 24 risks emerge within the project’s implementation phase – design, construction, operation. Finally, the micro level risks concern risks that appear between the partners involved, they rest on the idea that both of the parties have different incentives and objectives, and therefore, risks due to power struggle, differences in working methods and environment between the partners may emerge. Furthermore, Grimsey and Lewis (2004) argue for more detailed risk categorisation – they divide risks into nine categories that are suitable for the infrastructure approach: technical, construction, operating, revenue, financial, force majeure, regulatory/political, environmental and project default risks. This distribution is similar to the one proposed by Gray (2004), IMF (2004) and the European Commission (2005).

Finding the most optimal risk allocation point requires identifying what risk is handled best by which party. As mentioned above, there is no one optimal risk allocation solution that fits every specific project, however, some general guidance is present in the literature on PPPs (Bing, Akintoye, Edwards, & Hardcastle, 2005; European Commission, 2003; Grimsey & Lewis, 2004; OECD, 2008; Quiggin, 2004). For example, if Harris (2004) risk allocation model was considered, the risks would be assigned accordingly:

Figure 5. Model for risk allocation

Source: Harris (2004)

The proposed model identifies risks that should be passed on to the supplier (transferable risks), that should be retained by the government and the ones that do not belong to neither of the parties. As the figure shows, risks such as design, construction, operating performance, technology obsolescence, etc. are usually

Page | 25 assigned to the private partner. The reason for that is that the private partner receives most of these risks implicitly with the responsibilities passed on to the private partner (Harris, 2004). When, for example, DBFO is concerned, the responsibilities of the private partner include designing, building, financing and operating the asset, all of these tasks include associated risks, and by contractually agreeing to handle these tasks, the private partner, consequently, agrees to handle the risks concerned (Akintoye, Beck, & Hardcastle, 2003). The risks that are retained by the government authority are risks that the private partner has no influence over while the government does (Nisar, 2006). For example, the discriminatory regulatory risk – government might decide to change certain regulations that may influence the success of the private partner. In order to keep private partner safe from such possible modifications, the government has to take responsibility for the consequences of such certain change. Risks under the shared risk group are those that cannot be controlled at least cost or in the best way by neither of the party, for example, inflation, exchange and interest rate risks (Akintoye et al., 2003). An example of a more detailed risk allocation matrix, proposed by Chan, Yeung, Yu, Wang, and Ke (2011), is presented in the Appendix 4.

After identifying and allocating the risks, the next step is to place a value on them. There are three factors determining the price of the risk – probability of the risk occurring, consequence of the risk and the contingent factor10. The value of the transferable risk equals the contingent amount that the government would pay to the private partner if a risk occurred under the conventional procurement approach (Amekudzi & Morallos, 2008; Hodge, 2004).

Four elements: raw PSC, competitive neutrality, transferable risks as well as retained risks, produces the value of PSC, which is then compared to the value proposed by the private partner – estimate of PPP value. The value for money is represented in net present value terms as a difference between the expected costs of PSC and PPP (Amekudzi & Morallos, 2008), as shown in the figure below:

10

Page | 26 Figure 6. Identifying Value for Money

Source: Amekudzi and Morallos (2008, p. 121)

1.5. A

D V AN T AG ES AN D D I S AD V AN T AG ES OFPPP

As it has already been reviewed, the appropriately constructed PPPs entail the advantage of delivering better value for money compared to the traditional procurement approach. Delivering projects on time and on budget set (Meidute & Paliulis, 2011) are two of the most important advantages that are hidden under the concept of value for money. As study conducted by UK’s National Audit Office (2003) showed, from all conventionally procured projects, 70% were delivered late and 73% with costs exceeding the initial budget (data of 1999), whereas only 22% of PFI projects were late and only 24% delivered project in excess of the budget (data of 2002). The reason for such a difference lies behind the risks transferred in line with additional responsibility and accountability attached to the private partner in the case of PPP, what incentivizes the private partner to operate in the most efficient way. In addition, due to the long term characteristics of the partnerships, partners involved tend to act in a more cooperative way to each other in this case creating additional synergy benefits. Private partner manages complex financial arrangements as well as highly technical tasks more efficiently by using its innovative skills, on the other hand – the public sector preferably controls the legal

system, regulation and policies. As a result, a combination of the leading features of both of the partners produces a higher value (Harris, 2004).

Page | 27

The other advantage of PPPs lies behind the construction of the proposal to procure a public project. Government constructs PPP proposals that focus more on outputs rather than inputs. As a result, such mindset encourages government to perform a thorough discussion on which services should be provided, what standards should be expected, and what is the aim of the service provided/asset developed. Such a detailed discussion on service provision or asset development requires a detailed analysis of the project which in some of the cases may hinder the government from moving ahead if the project becomes inadequate. In addition, such kind of initial discussions encourage the government to think about the project with long term strategic goals in mind rather than focus on short term objectives. Furthermore, PPP’s ability to spread the costs of large investments over the lifetime of the asset is seen as an attractive advantage for the public sector. This eases the current debt of the government sector as it does not have to incur large cash outflows immediately. It follows, that the government can get projects financed even though in reality there are no public funds available. This advantage could be considered from two points of view: first – large investment costs are spread out, and second – private funds are considered as the new financing opportunities for the government (Meidute & Paliulis, 2011). On the other hand, this advantage should be considered with caution as sometimes the government might be incentivized to prove better value for money for a PPP project than it actually is just to guarantee the financing of the project.

Finally, from the private partner’s point of view, PPPs deliver opportunity for the private sector to get involved in the new markets (telecommunication, municipal water systems, energy, etc.) that otherwise would be closed for the private sector’s participation. In addition to this, the private partner involved in the new markets has a support of the government, which may facilitate gathering the funds required. On the other hand, one of the main disadvantages of PPPs is large bidding and contractual costs, which refer both to the government and the private partner. Large bidding costs of the PPP projects act as a rejecting force for the private parties as they are unwilling to invest heavily in the bidding process just to be

Page | 28 rejected later. What concerns government, large preparation costs consist of feasibility studies, lawyers, etc. Moreover, PPP projects are highly complicated. Usually, they involve more than two parties: public, private and banking sectors, and all of these parties have their own contradicting aims. In order to construct a unified agreement, a lot of time and capital needs to be invested on complex negotiations.

Furthermore, PPPs are said to deliver benefits because they transfer a significant amount of risks to the private partner. Nevertheless, it should be kept in mind that even though most of the risks are transferred to the private partner, the final entity that is responsible for providing services to the public is the government. As a matter of fact, if the private partner goes bankrupt, solely the government has to deal with the consequences and try to find other expedients how to keep delivering the service to the public. This implies that even though the risks are contractually transferred to the private partner, in practice, government retains a large portion of them in case of the private partner’s failure.

Moreover, in a PPP agreement, government bounds itself to a single private partner for a long term period and it agrees today for services/assets that will be in use in further future. There is a certain amount of risk concerning the future consumers’ need for the specific service. The idea behind the risks concerned is that the partnership may end up delivering services that are no longer required by the public. As a result, the partnership will appear to be less valuable than initially expected.

Finally, PPPs work well only for specific projects, which are complex and require specific private partner’s know-how, skills, and experience. Therefore, advantages that are attached to PPPs are attained only if certain project characteristics are met, whereas if the project is simple, executing it trough a PPP implies higher preparation costs, and as a result, lower value for money.

Considering all of the above, the main idea behind the PPP option is to have a project intricate enough that its complexity could justify additional preparation and

Page | 29 negotiation costs. Developing a project through a PPP usually ensures additional benefits such as implementing the project on time and on budget. Nevertheless, these benefits should be considered while keeping in mind the risks involved in having the long term agreement between private and public sector s for a certain service provision: who can reassure that there will still be a need for some kind of service in, for example, 30 years?

1.6. C

R I T I C I SM OFPPP

SEven though the majority of the international institutions seem to favour the PPP option (EC, UK Treasury, OECD, IMF), some of the researchers see PPPs as a language game in the politics – PPP is regarded as another way of privatizing a service/asset (Hodge & Greve, 2007). This point of view has been neglected by many other researchers who represent arguments proving that PPPs differ from the privatization (Grimsey & Lewis, 2004; Harris, 2004; Hong Kong Efficiency Unit, 2008; OECD, 2008). One of the first differences identified is the sale/transfer concerned. PPP involves government granting a right to the private party to develop and provide certain services/assets for a period of time, whereas privatization, in general terms, involves the sale of the asset. This assents to the amount of risks transferred. In PPP case, the amount transferred differs on the type of PPP chosen. Concession is the mode of PPP that involves the largest amount of risks transferred to the private partner; however, it still does not encompass the transfer of all risks. On the other hand, privatization includes the sale of the full package, which means the transfer of all associated risks. In this case, government is left with no direct responsibility for the service provided/asset developed, whereas in a PPP case, government is the one that retains the initial control and responsibility for the service/asset (Harris, 2004). If the private partner goes bankrupt, the service/asset is transferred back to the government. If the private partner does not operate to the standard required, the government has a right to intervene and punish the private partner. All in all, it is true that privatization and PPP share some similarities, but the idea of PPP is that it shares some superior features of the privatization as well as of the conventional procurement

Page | 30 mode – as Grimsey and Lewis (2004) argue: PPP fills in the missing gap between privatization and the traditional procurement approach.

Other critiques concentrate on the idea that the government should be fully responsible for the services provided as this is the role of the government and not the private sector. However, as Harris (2004, p. 3) argues, the provision of public services (such as free education, transportation or health) by the government is “comparatively recent development”. So the question rises whether it is the actual provision of the services or is it the regulation and control of the service provision (what kind of services to deliver, what kind of standard should be kept, what policy to follow, etc.) that is the role of the government? As Harris (2004) concludes the role of the government is to ensure that a policy is being adopted. If delivering the policy through the parties that are able to do that in the best possible way while additionally creating value for money to the public means that the private partner should be involved, then the advantages of private partner’s efficiency and innovative skills should be utilized.

Further critique concerns the view that PPPs are a ‘trendy’ politics. This means that countries might favour PPPs over the conventional procurement due to the lack of public funds available. Owing to this, the government is left with a choice not between a PPP and a conventional procurement project but with a choice between a project and no project at all as a government is unable to finance the project from its own funds (Robinson, 2000; Shaoul, 2005). The problem of such a preference for PPPs is that there is a high degree of possibility for approval of projects that do not generate better value for money but are accepted for the financial resources only – getting a project procured while having debt off government’s balance sheet (Maski & Tirole, 2008). In addition to this, as value of PPPs are most of the times assessed by using PSC, problems appear when hypothetical risk-adjusted nature of the model is considered. The PSC depends highly on the assumptions employed (Amekudzi & Morallos, 2008), one of the most important one being the rate used to discount the cash flows of the PSC. Furthermore, when risks allocation is performed, it is criticized that not all of the risks may be identified and

Page | 31 valued (Amekudzi & Morallos, 2008; OECD, 2008; Shaoul, 2005), thus leading to inaccurate PSC estimate. As OECD (2008) argues some of the risks may be left out and neither of the party initially agrees to take responsibility for it, however, once the risk evolves, it is the government and the public that have to bear the consequences and not the private partner, leaving some element of value for money out of the initial estimate. Considering all this, the value for money estimate may be easily adjusted in order to make the PPP proposal more attractive, which is seen as a problem when the only reason for PPP project implementation is the lack of public funds.

Moreover, it has been noted that an advantage of PPP is its ability to spread out the huge initial investment costs throughout the years of the lifetime of the asset. This means that the government avoids large investments today and is able to incur them later on in smaller amounts. However, who may guarantee that the government with increasing number of PPPs will be capable of financing these payments in later years? Will it pass this contingent liability to the future taxpayers (Harris, 2004)? In addition, who can be reassured that the same service/infrastructure will be necessary in, for example, 30 years? In addition, will the taxpayers be happy for paying taxes for the services that are unnecessary anymore? These questions are especially relevant to the cases of PPPs where the government contracts to pay availability payments for the services provided by the private partner.

Overall, PPPs attract some significant critiques, however, it should be noted that PPPs are not a magic solution for the conventional procurement issues. The true experiences of PPPs have not been observed yet as it takes time to acknowledge the full impact of each PPP, however, the initial stages of the PPP and the theoretical foundations allow PPPs to be considered as a possible way to bring on additional efficiency gains to the public sector.

Page | 32

2. AN AL YS IS

2.1. T

H E PR OJ EC TIn the last decades the advantages of having a developed inland waterway in Lithuania were forgotten. The politicians focused more on developing the road and rail rather than the inland waterway network. This is understandable as the potential for Lithuanian biggest river (Nemunas) to become domestically or an internationally important part of the transport network is far more complicated compared to the road or rail network. On the other hand, due to Lithuania’s geographic position and increasing global emphasis on the environmentally friendly modes of transportation, inland waterways are becoming a solution to many of the European environment targets set11. As a result, the interest to encourage the development of Lithuanian waterway is growing and one of the first steps is to develop a wharf in the centre of Lithuania (Appendix 5). The aim of the wharf is to stimulate the freight transportation in Lithuanian inland waterway network by creating opportunity to accommodate barges transporting containers.

2.2. A

L T ER N AT I VES F OR PR OJ EC T I M PL EM ENT AT I ONThe traditional procurement approach for the delivery of public services and facilities has been practised in Lithuania for decades already. The new rising trend, however, is the use of public-private partnerships. Despite the fact that PPPs may bring additional value for money, the PPP option is not always the best solution to the provision of the public service or good. In order to assess whether PPP option should be considered for the wharf’s project, the following circumstances, identified by the Ministry of Municipal Affairs (1999) and adopted to this particular project, should be reviewed:

11 For example, European Commission’s White Paper has noted that the GHGs emission should be decreased

by 80-95% below 1990 levels, from which at least 60% decrease should be achieved in the transport sector by 2050; by 2030 the transport sector’s GHGs emission should be lowered to 20% below the 2008 level. In addition, freight transportation shift to other modes is advocated: the target has been set to transfer the road freight to other transportation modes – rail or waterborne – when the transportation distance exceeds 300km by at least 30% by the year of 2030, and by 50% by the year of 2050 (European Commission, 2011, pp. 3, 9).

Page | 33 1. Does the government have enough know-how or financial resources to

consider the project on its own?

2. Is there a potential for the private partner to provide the public service faster and in a better quality than the government would do on its own?

3. Is there a competitive environment for potential tender of a project?

4. Can the output of the project be identified easily? Can the performance of the private partner be measured easily?

5. Does the project require innovative skills?

The wharf’s project is very specific and the government authority lacks the skills and know-how required to operate the wharf effectively. As a result, due to the expertise and experience of the private sector in the field concerned, the inclusion of the private partner may bring additional value. Furthermore, additional value can be enhanced by delivering the project faster than in the case of the government. The experience of PPP projects around the world prove that PPPs most of the times deliver the projects on time, whereas in the conventional procurement mode, the delivery is often delayed12. Moreover, the output of the wharf can be identified and measured easily, and as a result, monitoring private partner’s performance should not be too problematic. The idea behind PPP is that only the outputs of the project are specified, and the private partner has all the freedom it needs for innovative decision making that could make the project more efficient. Following this, it should be concluded that the PPP option is worth considering and, as a result, the paper analyses the following procurement options:

1. Traditional procurement approach, where government takes a full responsibility for the project and finances, designs, builds, operates and owns it;

12

Study performed by Flyvbjerg, Holm, and Buhl (2002) proved that costs in the conventional procurement approach in 90% of transportation infrastructure projects were underestimated – actual costs exceeded the planned budget on average by 28%. Another study conducted by UK’s National Audit Office (2003) found that from all conventional procurement approach projects arranged, 70% were delivered late and 73% with costs exceeding the initial budget (1999 data), whereas only 22% of PFI projects were late and only 24% delivered project in excess of the budget.

Page | 34 2. PPP approach, where the responsibility of the project delivery is shared

between the private partner and the government, and where it is the private partner that finances, designs, builds and operates the wharf.

Which of the two options delivers better value requires a detailed analysis, which is presented in the following sections.

2.3. I

D EN T I F Y I NG AN APPR OP R I AT EPPP

SC H EM EIn order to determine which PPP scheme should be the appropriate one for the project concerned, first of all, the overview of possible PPP forms in Lithuania is reviewed.

2.3.1. O

VER VI EW OFL

I T H U AN I A’

S L EG ALPPP

EN VI R ON M EN TCurrently Lithuania has no one single legal act determining all existing forms of public-private partnerships, their characteristics, etc. (Meidute & Paliulis, 2011). Nevertheless, some forms of PPPs are covered by Lithuanian laws, such as the Law on Management, Use and Disposal of State and Municipal Authorities’ Property, the Law on Concessions, the Law on Investment. The problem with these laws, however, is that some of them do not fully cover the regulations necessary and therefore, are insufficient (Meidute & Paliulis, 2011).

In Lithuania PPP environment is not yet developed. Some of the interest has been identified, however, it is far away from what, for example, United Kingdom or Australia has already achieved. As Meidute and Paliulis (2011, p. 262) note "there are virtually no PPP projects implemented at a national level that would cover some sector of importance for the society and where the public sector would be represented by central authorities”. Nevertheless, Lithuania is improving its PPP environment and as of today Lithuanian law provides two classifications of public-private partnerships: institutional and contractual partnerships.

Page | 35

IN S T IT U T IO N A L P A R T N E R S H IP

Institutional partnership is a PPP mode when functions of a state or municipal authority are granted to a joint stock company or a limited liability company, which ownership is shared between the state or municipal authority and the private partner. The characteristics describing the nature of this PPP form are determined in the Law on management, use and disposal of state and municipal authorities’ property(Seimas of the Republic of Lithuania, 2012c, article 2, paragraph 12).

The main requirement for establishing an institutional partnership is the exchange of resources between each of the party involved, i.e. the state or municipal government invests its property in exchange for acquiring the authorized capital in either the newly established joint stock or a limited liability company or in a company which is increasing its share capital. The acquired authorized capital should provide the state or municipal government (or both of them together) with more than 50 percent of the vote.

CO N T R A C T U A L P A R T N E R S H I P

In general terms, it could be defined as cooperation between the public and private parties on the basis of the contractual agreement. The contractual partnership can assume the form of a concession or public and private parties’ partnership.

To begin with the concession, the characteristics describing the nature of this PPP form are determined in the Law on Concessions (Seimas of the Republic of Lithuania, 2012a). Concession is an engagement of a concessionaire (private party involved in the concession agreement), in accordance to the concession agreement and the conditions laid down by the awarding authority, in economic-commercial activities related to infrastructure design, construction, extension, renewal, modification, repair, management, use and (or) maintenance, as well as the provision of public service, managemen