i

A DYNAMIC ANALYSIS OF THE INFLUENCE OF MONETARY POLICY ON THE GENERAL PRICE LEVEL IN ZIMBABWE UNDER PERIODS OF

HYPERINFLATION AND DOLLARISATION BY

WILLIAM KAVILA

THESIS SUBMITTED IN FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE OF

PHILOSOPHIAE DOCTOR COMMERCII (ECONOMICS) in the

FACULTY OF BUSINESS AND ECONOMIC SCIENCES DEPARTMENT OF ECONOMICS

of the

NELSON MANDELA METROPOLITAN UNIVERSITY

PROMOTER: PROFESSOR PIERRE LE ROUX

ii DEPARTMENTOFACADEMIC

ADMINISTRATION

EXAMINATIONSECTION

SUMMERSTRANDNORTHCAMPUS PO Box 77000

Nelson Mandela Metropolitan University Port Elizabeth

6031

Enquiries: Postgraduate Examination Officer

DECLARATION BY CANDIDATE

NAME WILLIAM KAVILA

STUDENT NUMBER 213457342

QUALIFICATION PhD (ECONOMICS)

TITLE OF THESIS A DYNAMIC ANALYSIS OF THE INFLUENCE OF MONETARY POLICY ON THE GENERAL PRICE LEVEL IN ZIMBABWE UNDER PERIODS OF HYPERINFLATION AND DOLLARISATION DECLARATION

In accordance with Rule G4.6.3, I hereby declare that the above mentioned thesis is my own work and has not previously been submitted for assessment to another university or for another qualification.

SIGNATURE:

iii ABSTRACT

This thesis analyses the influence of monetary policy on the general price level in Zimbabwe during periods of hyperinflation and dollarisation. The first part of the analysis covers the period January 2006 to July 2008 when the country experienced high inflation and ultimately hyperinflation. The second part covers the period 2009 to 2012, when the country adopted the multi-currency system and became fully dollarised. In terms of motivation, the study firstly sought to empirically examine the factors that led to hyperinflation in Zimbabwe, paying particular attention to the influence of monetary policy. Secondly, the thesis sought to determine the major factors that influenced price formation in a dollarised Zimbabwean economy; a completely new macro-economic environment. A significant development in this new macro-economic environment was the loss of monetary policy autonomy of the central bank, which also contributed to the relevance of the study.

This thesis makes two contributions. The first contribution is the finding that hyperinflation in Zimbabwe was caused by expansionary monetary policy as a result of the activities of an unrestrained and unaccountable central bank. The second contribution was the empirical finding that in the fully dollarised economy inflation is largely determined by external factors. This implies that the domestic economy has no control over domestic inflation developments and as such, Zimbabwean authorities should formulate appropriate economic policies to respond to the impact of external shocks on domestic price formation when the need arises. The role of monetary policy in Zimbabwe’s hyperinflation episode is assessed using the Autoregressive Distributed Lag (ARDL) and the Error Correction Model (ECM) approaches with monthly data from January 2006 to July 2008. The impact of monetary policy on hyperinflation is captured by the coefficient of broad money supply and the interest rate. Results indicate that hyperinflation was caused by expansionary monetary policy, the exchange rate premium and inflation expectations for both the short and long term. Zimbabwe’s hyperinflation episode which peaked during the period 2007 to 2008 brings to the fore the importance of ensuring that the central bank is independent in executing its mandate of influencing the monetary policy process in a manner that ensures price stability.

iv

The ARDL and ECM approaches are also used to explore the dynamics of inflation in the dollarised Zimbabwean economy, with monthly data from January 2009 to December 2012. The main drivers of inflation under the multi-currency system were found to be the United States of America dollar/South African rand exchange rate, international oil prices, inflation expectations and the South African inflation rate. The findings contrast with the hyperinflationary era, where empirical studies have cited excessive money supply growth as the major driver of inflation dynamics in Zimbabwe. The results also suggest a higher exchange rate pass-through to domestic prices, consistent with empirical literature which postulates that inflation in dollarised economies is largely explained by movements in the exchange rate of major trading partners and international prices. The policy implication from the analysis is the need for policy makers to aggressively promote policies that ensure increased productivity of the economy. An improvement in productivity would influence the relative prices of tradable and non-tradable goods and ultimately the general price level in the economy.

The study also quantified the independence of the Reserve Bank of Zimbabwe (RBZ) using the Mathew (2006), “new index for institutional quality” and the results showed that the RBZ is not an independent central bank. The central bank is found to have a low index of central bank independence (CBI), against a high level of inflation. While this relationship does not imply causality it can be inferred that the lack of independence of the RBZ could have influenced inflation dynamics in Zimbabwe. Only a subordinated central bank can be compelled to engage in inflationary deficit financing and also fund quasi-fiscal activities. The provisions of the RBZ Act [Chapter 22:15] in their current form make the central bank an appendage of the Ministry of Finance and Economic Development and this has, to a large extent, resulted in conflict between the political goals of government and the central bank’s primary objective of achieving price stability. In the event that Zimbabwe reintroduces its own currency in future, the achievement of the primary goal of price stability by the central bank will only be realised if the apex bank is given more autonomy.

v

DEDICATION

I humbly dedicate this thesis first to God, the Almighty, for giving me the strength and good health to be able to complete it. I also dedicate the thesis to my wife Martha and my sons, Tiyisani, Kombo and Engisani.

vi

ACKNOWLEDGEMENTS

First and foremost, I would like to thank God, the Almighty for giving me good health, peace of mind and endurance that enabled me to complete this piece of work. I wish to sincerely thank the United States Agency for Aid and Development-Strategic Economic Research and Analysis (USAID-SERA) Programme for providing me the financial assistance to do the programme. I sincerely acknowledge the guidance and kind encouragement of my supervisor, Professor Pierre Le Roux through-out the writing of this thesis. The assistance rendered by all staff at USAID-SERA including Dr Daniel Ndlela, Ms Emmanuella Matorofa, Ms Evidence Ndari, Ms Angeline Zengeni, Ms Monalisa Jenje and Ms Patience Shuva is kindly acknowledged. I also acknowledge the guidance given by Dr Bruce Bolnick in the writing of the research proposal for this thesis.

I would also like to thank my personal assistant, Ms Emma Chakavarika for the various forms of assistance she provided in the production of this thesis. My colleague Dr Nebson Mupunga is kindly thanked for the distinct technical support and encouragement he gave me as I worked on my thesis. I also express my appreciation for the technical support from my other colleagues namely; Mr Tawedzerwa Ngundu, Mr Pardon Chitsuro, Mr Simelizwe Ncube and Mr Prudence Moyo. I would also like to express my sincere appreciation to the Reserve Bank of Zimbabwe (RBZ) library staff, Mr Benard Marara, Mr Newman Mapfumo and Mr Nelson Mutimodyo for assisting me with reading materials.

I am very grateful to the Department of Economics at Nelson Mandela Metropolitan University for their excellent PhD programme and very conducive learning environment. My special gratitude goes to Mr Fred Geel, for language and technical editing of my thesis and research papers.

I would also like to thank the Governor of the RBZ Dr J.P. Mangudya and the Director of Research, Mr S. Nyarota for allowing me to embark on this programme as well as giving me the necessary support.

vii

The support and encouragement of my wife Martha and my sons, Tiyisani, Kombo and Engisani is also greatly acknowledged. There were many times when they did not enjoy my company as I worked long hours into the night. My sincere thanks to you all for the valuable support you gave me in producing this work.

William Kavila November 2015

viii TABLE OF CONTENTS Page DECLARATION ii ABSTRACT iii DEDICATION v ACKNOWLEDGEMENTS vi

TABLE OF CONTENTS viii

LIST OF FIGURES xiv

LIST OF TABLES xv

LIST OF ABBREVIATIONS xvii

CHAPTER ONE

BACKGROUND, PROBLEM STATEMENT AND OBJECTIVES OF THE STUDY

1.1 Introduction 1

1.2 Background to the study 2

1.3 Statement of the problem 4

1.4 Objectives of the study 7

1.5 Research question 7

1.6 Significance of the study 8

1.7 Summary 10

1.8 Overview of the Thesis 12

CHAPTER TWO

OVERVIEW OF ECONOMIC DEVELOPMENTS IN ZIMBABWE SINCE INDEPENDENCE

2.1 Introduction 13

2.2 The decade of controls (1980-1990) 14

2.3 The first phase of the Economic Structural Adjustment Programme (1991-1995)

ix

2.3.1 Outcome of the first phase of reform programme 18

2.3.2 Analysis of specific outcomes 20

2.3.2.1 Fiscal sector 20

2.3.2.2 Public enterprises reform 21

2.3.2.3 Monetary policy and financial sector reform 21

2.3.2.4 Trade and exchange liberalisation 22

2.3.2.5 Domestic deregulation and investment promotion 22

2.3.2.6 Social Sector 23

2.3.3 Overall assessment of economic reform programme 23

2.4 Zimbabwe Programme for Economic and Social Transformation (ZIMPREST)

23

2.5 The economic crisis (1997 – 2008) 24

2.5.1 Economic developments 25

2.5.2 Economic reforms during the economic crisis 28

2.5.2.1 The 1998 Reform Programme 28

2.5.2.2 The 1999 Reform Programme 30

2.5.2.3 Zimbabwe Millennium Recovery Programme (MERP) 32

2.5.2.4 National Economic Recovery Programme (NERP) 33

2.5.2.5 Macro-Economic Policy Framework (MEPF) 34

2.5.3.6 National Economic Development Priority Programme (NEDPP) 35 2.5.3 Quasi-fiscal activities of the Reserve Bank of Zimbabwe 35

2.4 Exchange rate management during the economic crisis 43

2.6 Return to macro-economic stability (2009 – 2012) 47

2.7 Summary 51

CHAPTER THREE

THEORETICAL AND EMPIRICAL LITERATURE REVIEW

3.1 Introduction 54

3.2 The theoretical literature review of inflation 54

3.2.1 Monetary theory of inflation 55

3.2.2 Demand pull inflation 60

3.2.3 Cost push inflation 60

3.2.4 Expectations theory of inflation 61

3.2.5 Structuralist theory of inflation 64

3.3 Empirical literature review of inflation 65

x

3.4.1 Theoretical issues 71

3.4.2 Empirical literature review on monetary policy and inflation 73 3.5 Literature review on inflation and dollarisation 77

3.5.1 Theoretical aspects of dollarisation 77

3.5.1.1 Unofficial dollarization 78

3.5.1.2 Official dollarization 79

3.5.1.3 Preconditions for dollarization 79

3.5.2 Empirical literature review on inflation and dollarisation 80 3.5.2.1 Inflation dynamics in partially dollarised economies 81 3.5.2.2 Exchange rate pass-through and inflation in dollarised economies 83 3.5.2.3 Inflation dynamics in fully dollarised economies 84

3.5 Summary 85

CHAPTER FOUR

RESEARCH DESIGN AND METHODOLOGY

4.1 Introduction 88

4.2 Model selection 89

4.3 Model derivation 90

4.4 Estimation methodology 93

4.5 The error correction representation of an ARDL model 93

4.5.1 The Wald F test 94

4.5.2 Long-run model 94

4.5.3 Long-run elasticities 94

4.6 The role of monetary policy under periods of hyperinflation 94 4.7 Central bank independence and the dynamics of hyperinflation 96 4.8 Dynamics of inflation in a dollarised economy 96 4.9 Response of inflation process to macro-economic shocks 98

4.10 Granger Causality 101

4.11 Diagnostic tests 102

4.11.1 Unit root tests 102

4.11.2 Serial correlation test 102

4.11.3 Heteroskedasticity test 102

4.11.4 Model specification test 102

xi

4.12 Stability tests 103

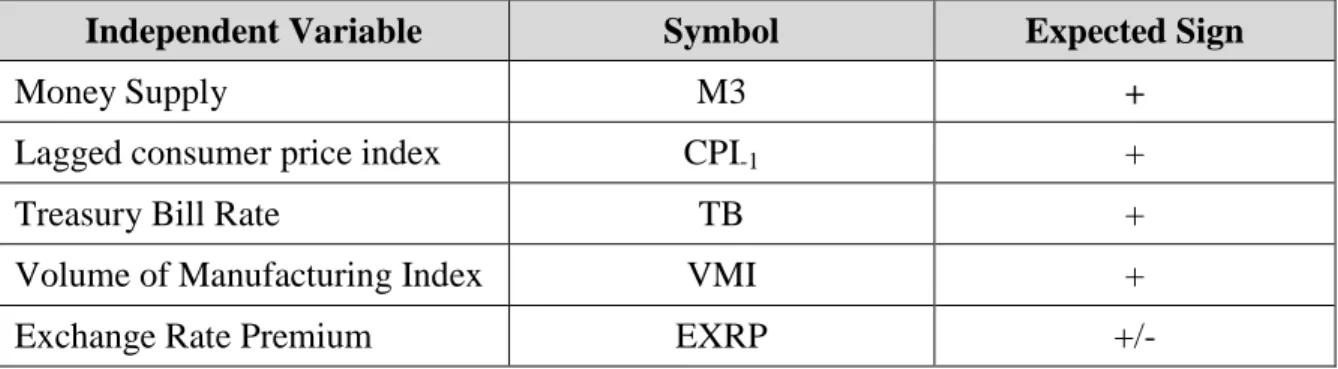

4.13 Definition and justification of variables 103

4.13.1 The dependent variable 104

4.13.2 Independent variables - hyperinflation period 104

4.13.2.1 Broad money supply (M3) 104

4.13.2.2 Exchange rate premium (EXRP) 105

4.13.2.3 Treasury bill rate (TB) 105

4.13.2.4 Volume of manufacturing index (VMI) 105

4.13.2.5 Lagged consumer price index (CPI-1) 106

4.13.3 Explanatory variables - dollarisation period 106

4.13.3.1 Broad money supply (M3) 106

4.13.3.2 US$/South African rand exchange rate (SEXC) 106

4.13.3.3 International food prices (FOOD) 106

4.13.3.4 International oil prices (OIL) 107

4.13.3.5 South African inflation (SCPI) 107

4.13.3.6 Lagged consumer price index (CPI -1) 107

4.14 A priori expectations: a summary 107

4.15 Data sources and characteristics 108

4.16 Summary 108

CHAPTER FIVE

THE INFLUENCE OF MONETARY POLICY ON THE GENERAL PRICE LEVEL IN ZIMBABWE DURING HYPERINFLATION

5.1 Introduction 110

5.2 A historical perspective of world hyperinflations 111 5.3 The road to Zimbabwe’s hyperinflation episode of 2006-2008: A 114 5.4 The conduct of monetary policy in Zimbabwe (1980-2012) 128

5.5 Diagnostic tests 133

5.5.1 Unit root test 133

5.5.2 Serial correlation, heteroskedasticity and model specification test 134

5.6 Empirical results and analysis 135

5.6.1 Estimated coefficients using ARDL model 135

5.6.2 Error correction model results 136

5.6.3 Pairwise Granger causality test results 137

xii

5.8 Summary 139

CHAPTER SIX

CENTRAL BANK INDEPENDENCE AND THE DYNAMICS OF HYPERINFLATION IN ZIMBABWE

6.1 Introduction 142

6.2 The Reserve Bank of Zimbabwe: A historical perspective and brief analysis of its operations

143 6.3 An overview of central bank independence and inflation 146

6.3.1 Measures of central bank independence 147

6.3.2 A review of studies on central bank independence 148 6.4 Summary of results of earlier studies on CBI and inflation 153 6.5 Measuring the independence of the RBZ using the Mathew (2006)

New Index of Institutional Quality

156

6.6 Summary 160

CHAPTER SEVEN

INFLATION DYNAMICS IN THE DOLLARISED ECONOMY

7.1 Introduction 164

7.2 Diagnostic tests results 165

7.2.1 Unit root tests 165

7.2.2 Serial correlation, heteroskedasticity and model specification test 166

7.2.3 Lag length selection 167

7.3 Empirical results and analysis 167

7.3.1 ARDL model results 167

7.3.2 The error correction model (ECM) 169

7.4 Stability tests 170

7.5 Summary 171

xiii

CHAPTER EIGHT

THE REACTION OF INFLATION TO MACRO-ECONOMIC SHOCKS

8.1 Introduction 173

8.2 A brief overview of the reaction of inflation to macro-economic shocks

174

8.3 Empirical results and analysis 176

8.3.1 Determination of lag length 176

8.3.2 Granger causality tests 177

8.3.3 Bayesian VAR estimates 178

8.3.4 Impulse responses 179

8.3.5 Variance decomposition 181

8.4 Stability tests 182

8.5 Summary 182

CHAPTER NINE

SUMMARY, CONCLUSION AND POLICY RECOMMENDATIONS

9.1 Introduction 185

9.2 Summary of issues 185

9.2 Conclusions 191

9.3 Policy implications 193

9.4 Areas for future study 198

REFERENCES 199

ANNEXURES 223

Annexure 1: Time series data – hyperinflation period (2006:2008) 223 Annexure 2: Time series data – dollarisation period (2009-2012) 224 Annexure 3: Quasi-fiscal activities of central banks of selected

countries 225

Annexure 4: Main QFAS of the RBZ (2004-2008) 229 Annexure 5: World hyperinflations by country 230 Annexure 6: Some of the denominations introduced by the RBZ at

the peak of hyperinflation 232

Annexure 7: Components of the J.T Mathew New Index for Central

xiv

LIST OF FIGURES

Figure 2.1: Real GDP growth rates (%) 26

Figure 2.2: Gross domestic product and quasi fiscal activities (2004- 2008) 40

Figure 2.3: Reserve money and inflation 41

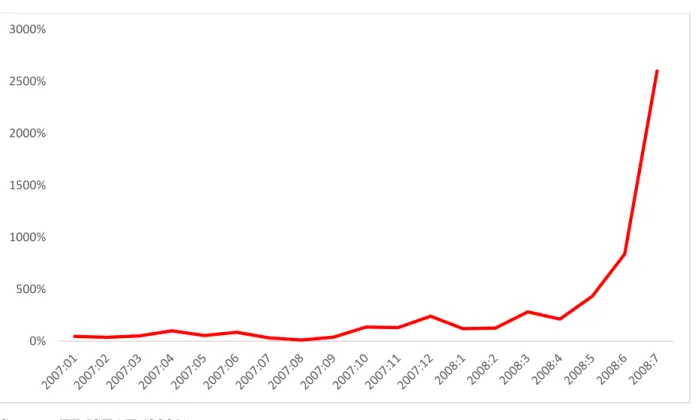

Figure 2.4: Month-on month inflation (2007:01 to 2008:07) 42

Figure 2.5: Real GDP growth (2000-2012) 49

Figure 2.6: Annual inflation (2009-2012 50

Figure 5.1: Exchange rate developments (Jan 2000 to Dec 2003) 117 Figure 5.2: US$/Z$ exchange rate developments (January 2004-Dec 2005) 118

Figure 5.3: Current account balance 120

Figure 5.4: Inflation and 91 day treasury bill rate (1997-2002) 130 Figure 5.5: Inflation and M3 growth (1997-2002) 131 Figure 5.6: Money supply growth and inflation (2003-2006) 132 Figure 5.7: Plot of cumulative sum of recursive residuals 138 Figure 5.8: Plot of cumulative sum of squares of recursive residuals 138 Figure 6.1: Relationship between inflation and central bank independence 160

Figure 7.1: Plot of cusum test statistic 170

Figure 7.2: Plot of cusum of squares test statistic 171

Figure 8.1: Impulse responses of ZCPI 180

xv

LIST OF TABLES

Table 2.1: Zimbabwe: Selected economic indicators (1980-1990) 15 Table 2.2: Zimbabwe: Selected economic indicators (1991-1996) 18 Table 2.3: Balance of payments summary (US$ millions) 27

Table 2.4: Balance of payments indicators 28

Table 2.5: Quasi-fiscal expenditure growth rates (per cent) 38 Table 2.6: Selected RBZ assets and liabilities (per cent of total) 39

Table 2.7: Currency rebasing 43

Table 4.1: Hyperinflation model - a priori expectation 107 Table 4.2: Dollarisation inflation model - a priori expectation 108

Table 5.1: World hyperinflation (1900-2008) 112

Table 5.2: Stationarity test results 133

Table 5.3: Wald coefficient test results 134

Table 5.4: Diagnostic test results of residuals of hyperinflation equation 134

Table 5.5: ARDL model results 135

Table 5.6: Long run elasticities 136

Table 5.7: Error correction model results 136

Table 5.8: Pairwise Granger causality test results 137 Table 6.1: Survey of studies on CBI and inflation 153 Table 6.2: Zimbabwe: Measured monetary policy independence (MPI) 157 Table 6.3: Zimbabwe: Measured personnel/political independence (PI) 157 Table 6.4: Zimbabwe: Measured fiscal independence (FI) 158 Table 6.5: Zimbabwe: Measured CBI and Inflation 158 Table 6.6: Measured CBI and inflation rates for selected developed and

developing countries 159

Table 7.1: Stationarity tests results 165

Table 7.2: Wald coefficient test results 166

Table 7.3: Diagnostic test results of residuals of dollarized economy equation 166

Table 7.4: VAR lag order selection criteria 167

Table 7.5: Estimated coefficients using the ARDL approach 168

xvi

Table 7.7: Short run error correction model (ECM) 169

Table 8.1: Lag length 177

Table 8.2: Granger causality tests 177

Table 8.3: Bayesian VAR estimates with ZCPI as dependent variable 178

xvii

ABBREVIATIONS AND ACRONYMS

AfDB African Development Bank

ARDL Autoregressive Distributed Lag

ASPEF Agriculture Sector Productivity Enhancement Faculty BACOSSI Basic Commodities Supply Side Interventions

BAZ Bankers Association of Zimbabwe

BRN Bank of Rhodesia and Nyasaland

BVAR Bayesian Vector Auto-regression

CBI Central Bank Independence

CPI Consumer Price Index

CMB Cotton Marketing Board

CSC Cold Storage Commission

CZI Confederation of Zimbabwe Industries

DMB Dairy Marketing Board

ECB European Central Bank

ECM Error Correction Model

ESAF Enhanced Structural Adjustment Faculty

ESAP Economic and Structural Adjustment Programme

EXRP Exchange Rate Premium

Fed Res Federal Reserve Bank

FI Financial/Fiscal Independence

FOLIWARS Foreign Currency Licensed Warehouses and Retail Shops

FRN Federation of Rhodesia and Nyasaland

GDP Gross Domestic Product

GMB Grain Marketing Board

GOZ Government of Zimbabwe

GNU Government of National Unity

GPA Global Political Agreement

IBRD International Bank for Reconstruction and Development

xviii

LARP Local Authorities Reorientation Programme

MEPF Macro-economic Policy Framework

MERP Millennium Economic Recovery Programme

MPI Monetary Policy Independence

M3 Broad Money

NEDPP National Economic Development Priority Programme

NERP National Economic Recovery Programme

OECD Organisation for Economic Cooperation and Development PARP Parastatals Reorientation Programme

PI Personnel/Political Independence

QFAs Quasi-Fiscal Activities

RBZ Reserve Bank of Zimbabwe

SDR Special Drawing Rights

SCPI South African Inflation

SEXC US$/South African rand exchange rate

STERP Short Term Emergency Recovery Programme

TB Treasury Bill rate

TBF Troubled Bank Facility

TFCBS Tradable Foreign Currency Balances

USA United States of America

US$ United States of America dollar

VBERS Volume Based Exchange Rate System

VECM Vector Error Correction Model

VMI Volume of Manufacturing Index

Z$ Zimbabwe dollar

ZIMPREST Zimbabwe Programme for Economic and Social Transformation

ZISCO Zimbabwe Steel Company

ZIC Zimbabwe Investment Centre

ZIMSTAT Zimbabwe National Statistical Agency

ZIMRA Zimbabwe Revenue Authority

1

CHAPTER ONE

BACKGROUND, PROBLEM STATEMENT, OBJECTIVES AND SIGNIFICANCE OF THE STUDY 1.1 Introduction

This chapter comprises the background, problem statement, objectives and significance of the study. It also outlines the research questions that guided the empirical analysis in this study. Price instability arguably stifles economic growth and development (Nguyen et al. 2012) and the case for Zimbabwe provides a good example of how a sustained increase in prices can result in the near collapse of an economy. High and increasing inflation resulted in an unprecedented loss in value of the local currency (IMF 2009; Fed Res Bank of Dallas 2011; Coomer and Gastraunthaler 2011; Kairiza 2012), culminating in its rejection as a medium of exchange and store of value in 2008. The economy’s monetary transmission mechanism was virtually destroyed as interest rates became redundant. In addition, rising inflation created an environment of negative real interest rates which discouraged savings. The negative real interest rates benefitted debtors at the expense of creditors, an unfair form of income redistribution. Relatedly, high inflation created a wage – inflation spiral as workers demanded higher compensation against the background of the relentless increase in prices. The higher wage demands were passed on to the same workers in the form of higher prices, leading to other rounds of wage demands.

High inflation also eroded the value of fiscal revenue inflows, resulting in fiscal deficits as revenues fell short of budgeted expenditures. Consequently, the RBZ was forced to assist in covering the government revenue shortfalls through printing money. RBZ funding was also extended to all other sectors of the economy as they were equally in distress because of escalating inflation. The support to other sectors of the economy by the RBZ was in the form of subsidies such as free foreign exchange transfers to public enterprises, liquidity support to banking institutions and public enterprises, and liquidity support to the private sector through the Productive Sector Facility (PSF) and the Agricultural Sector Productivity Enhancement Facility (ASPEF) (Munoz 2007). The source of funds for all these quasi-fiscal activities of the RBZ was money creation which resulted in excessive monetary expansion (Munoz 2007;

2

Coorey et al. 2007; Kramarenko et al. 2010). It was not clear how the central bank hoped to address this plethora of challenges by providing inflationary concessional funding to all sectors of the economy and, thereby, worsening the situation by creating an unstable economic environment.

The high inflation environment created a high level of uncertainty for business and also rendered Zimbabwean products uncompetitive on the international market. The Zimbabwean population experienced unprecedented levels of poverty as living standards plummeted (Fed Res Bank of Dallas 2011) with the last blow coming in the form of loss of all savings and pensions as well as funeral and life assurance benefits accumulated over a very long period of time, for some sections of the population. It is important that Zimbabwe’s policy makers fully understand the determinants of inflation dynamics so that the country does not go through the same harrowing experience of hyperinflation again.

The high inflation and ultimately hyperinflation led to the abandonment of the local currency as a medium of exchange by the transacting public during the last quarter of 2008, leading to the formal adoption of dollarization by the Government of Zimbabwe (GOZ) in January 2009. It is equally important for policy makers to understand that while the adoption of the multi-currency system brought stability in the economy it has its own challenges pertaining to the impact of external shocks on domestic price formation. In this regard, an analysis of the dynamics of inflation in a dollarised economy is also important and this study seeks to do such an analysis.

1.2 Background to the study

Zimbabwe experienced relatively stable prices during the first ten years of independence on account of an extensive system of administrative controls on prices in all markets. The country, however, started experiencing high rates of inflation beginning 1999, following the onset of the economic crisis during the last quarter of 1997. The economic crisis was triggered by weak macro-economic policies, low export earnings, governance problems and the involvement of the country in the Democratic Republic of Congo conflict which led to the suspension of balance of payments support by the IMF (IMF 2001; Kairiza 2012). Although political factors

3

could have partly accounted for Zimbabwe’s economic meltdown, other factors such as the monetisation of fiscal deficits, quasi-fiscal operations of the RBZ, exchange rate depreciation and a decline in the gross domestic product could also have contributed to escalating inflation levels (Coorey et al. 2007; Kairiza 2012).

In a bid to deal with high inflation that was prevailing in the economy, Dr Gedion Gono who took over as governor of the RBZ in December 2003 announced a raft of monetary policy tightening measures. The access to RBZ liquidity support by commercial and merchant banks was tightened. Some banking institutions, however, ended up abusing the liquidity support from the central bank by using the funds to finance non-core banking activities. The liquidity support had been ear-marked specifically to assist banks fund their end of day short positions. As part of the stringent monetary policy instituted by the RBZ statutory reserve requirements were increased from 20 to 30 per cent for deposit money banks and from 5 to 15 per cent for finance houses, effective January 2004 (RBZ 2003). The new measures resulted in an increase in interbank interest rates and the collapse of the Zimbabwe Stock Exchange market. Inflation declined from 598.7 per cent in December 2003 to 132.8 per cent in December 2004, as a result of the tight monetary policy measures implemented by the central bank during 2004. The downward trend in inflation was, however, short-lived because the RBZ started engaging in quasi-fiscal activities in the form of direct financing to firms, the purchase of farm equipment and acquisition and distribution of farming inputs. This policy action was hailed as a heterodox approach to economics that was more practical, compared to the traditional classical economic theory. The central bank increased currency in circulation at escalating rates, particularly during the period January 2005 to May 2007, when the rate of increase in currency circulation exceeded the January 1921 to May 1923 peak of printing by the German central bank (Hanke 2008). Propping up the productive sectors of the economy through the central bank’s quasi-fiscal activities played a major role in firmly setting the stage for hyperinflation (Coorey et al. 2007).

The hyperinflationary environment that was created consequently resulted in the abandonment of the local currency in favour of foreign currencies (IMF 2009; Fed Res Bank of Dallas 2011;

4

Coomer and Gastraunthaler 2011; Kairiza 2012). This move was then formalised by the introduction of the multi-currency system, wherein the South African rand, United States of America dollar (US$), British pound and the Botswana pula were accorded legal tender status. The introduction of the multi-currency regime, however, implied that the central bank could no longer exercise an independent monetary policy stance. In essence, the monetary policy of the main-currency country, the United States of America (USA), would more or less become the monetary policy of Zimbabwe. On a positive note, the introduction of the multi-currency system put an abrupt end to hyperinflation and the country started experiencing single digit inflation levels (IMF 2009; RBZ 2009; Fed Res of Dallas 2011). Under the multi-currency system, the current account was largely liberalised and economic agents were authorised to transact in hard currencies as well as making tax payments to the Zimbabwe Revenue Authority (ZIMRA) in foreign exchange (Kramarenko et al. 2010).

Against this background, this thesis examines the dynamics of inflation and monetary policy in Zimbabwe over the periods 2006-2008 and 2009-2012, in order to infer the influence of monetary policy and institutional factors in explaining inflation dynamics. Zimbabwe moved from three digit to four digit levels of 12 month inflation in 2006, clearly passing the psychological barrier. A widely held view was that a central bank that is independent from political influence is conducive to low inflation (Loungani and Sheets 1997; de Haan and Kooi 2000; Walsh 2008; Ito 2010; Kasseeah, Weng and Moheeput 2011). In this regard, the study will also include a qualitative analysis of the role of central bank independence (CBI) in explaining inflation persistence and dynamics in Zimbabwe. The major factors behind Zimbabwe’s hyperinflation, its effects and consequent abrupt end are particularly instructive. It, therefore, remains to be established to what extent monetary policy and institutional factors have influenced inflation persistence and dynamics in the economy.

1.3 Statement of the problem

Zimbabwe experienced relatively low inflation levels between 1980 and 1990, partly explained by a system of administrative controls on the product, foreign exchange and labour markets (Chibber et al. 1989). Inflation averaged 13 per cent between 1980 and 1990, before rising to around 20 per cent during the first phase (1991-1995) of the International Monetary Fund (IMF) supported Economic and Structural Adjustment Programme (ESAP).

5

A combination of factors could have explained inflation during the first phase of ESAP and these were, among others, the removal of price controls; and monetisation of fiscal deficits. In addition, there were supply constraints caused by intermittent droughts (IMF 1993; Morande and Schmidt-Hebbel 1991; RBZ 1996). Periodic devaluations, necessitated by the need to maintain export competitiveness and foreign prices, may also have caused inflation during the economic reform period (Durevall and Kadenge 2002). Furthermore, low export earnings, coupled with the suspension of balance of payments support by the IMF subjected the Zimbabwe dollar (Z$) to severe pressure, leading to its substantial depreciation (RBZ 2000). The local currency had lost half of its value to the US$ by the end of 1997, leading to a critical shortage of foreign currency in the official foreign exchange market. The acute shortage of foreign currency triggered the emergence of a parallel market for foreign exchange. Consequently, most firms sourced foreign exchange for importing essential inputs from the parallel market and passed on the increased costs of production to consumers in the form of higher prices. Inflation increased from 20.1 per cent in 1997 to 589.7 per cent by the end of 2003. Concomitantly, the country’s economy declined, mirrored in reduced output across most key sectors of the economy, notably agriculture, manufacturing, mining, construction and tourism. This is likely to have increased inflationary pressures in the economy.

As standards of living declined due to the continued erosion of incomes by high inflation, veterans of the war of liberation invaded commercial farms during the year 2000, leading to acute farming activity disruptions (IMF 2001; Moss 2007; Besada and Moyo 2008; Kairiza 2012). The Government of Zimbabwe (GOZ) responded by officially embarking on the land reform programme in 2002, leading to some disturbances on commercial farms. The disruption of commercial farming activities resulted in a 30 per cent fall in agricultural output, with knock-on effects on overall output of the economy. In consequence, overall output declined by 14 per cent and 9 per cent in 2002 and 2003, respectively. Output declines in key sub-sectors cascaded into production declines in downstream industries, which fed through to other sectors of the economy. The resultant supply side bottlenecks, against the background of excessive growth in money supply could have fuelled inflation.

6

In addition, persistent shortages in foreign currency fuelled the parallel market, with the Z$ to US$ exchange rate depreciating to as high as Z$6 000 per US$1, compared to the official exchange rate of Z$824 per US$1 by mid-2003. Economic agents lost confidence in the economy and this is likely to have led to the heightening of inflationary expectations. Firms on their part adjusted prices upwards almost on a daily basis and later on an hourly basis, as the parallel market premium continued to rise, further compounding the problem.

Speculative behaviour emerged as economic agents continued to lose confidence in the economy, especially during the period 2002 to 2003. Commercial banks, for example, diverted depositors’ funds to non-core business areas such as investing in real estate and the purchase of motor vehicles to hedge themselves against inflation (RBZ 2003). This created liquidity problems for the banks and they ended up failing to settle their positions, turning to the central bank for accommodation (RBZ 2003). The rather unlimited access to central bank credit by commercial banks continued to fuel economy-wide speculative activities. The central bank simply printed money to accommodate the banks’ short positions and this led to excessive monetary expansion, which might have fuelled inflation.

As the economic crisis deepened, the central bank responded by printing money to bail out both the private and public sectors. Quasi-fiscal operations intensified between 2005 and 2008, leading to excessive monetary expansion and steep exchange rate depreciation. Broad money supply growth increased from 520 per cent by end December 2005 to 1 416.6 per cent by end December 2006; 64 113 per cent by end December 2007 and 344 quintillion per cent by end December 2008. Inflation also surged and stood at 585.4 per cent; 1 281.1 per cent; and 66 212.3 per cent by end December 2005; end December 2006; and end December 2007, respectively. The inflation spiral continued, with the annual price increase reaching 231 million per cent by end July 2008. The surge in inflation could also have been a reflection of underlying imbalances in the economy that were worsened by a booming parallel market for foreign exchange and declining economic activity. Unofficial estimates put the annual inflation rate at 100 billion per cent by the end of December 2008.

7

The uniqueness of Zimbabwe’s hyperinflation episode and the country’s abrupt return to macro-economic stability underscores the need for a comprehensive analysis of the factors underlying the causes and effects. Although inflation stabilised at below 5 per cent, following the adoption of the multi-currency system in February 2009, it is likely to become a recurring problem if the economic and institutional factors that brought it in the first place are not correctly identified. This study is, therefore, motivated by the need to comprehensively understand the role of monetary policy in the dynamics of inflation in Zimbabwe.

1.4 Objectives of the Study

The primary objective of this study is to empirically analyse the dynamics of inflation during periods of hyperinflation and dollarization. It is noteworthy that a new macro-economic environment was ushered in by the adoption of a multi-currency system. Specifically the study aims to:

(i) Assess the determinants of hyperinflation in Zimbabwe.

(ii) Empirically determine the role of monetary and institutional factors in the incidence of hyperinflation in Zimbabwe.

(iii) Analyse the implications of the identified factors for the future conduct of monetary policy in Zimbabwe.

(iv) Examine the factors explaining inflation dynamics in the dollarised Zimbabwean economy.

(v) Establish whether there has there been a shift in inflation dynamics in Zimbabwe in the advent of dollarisation.

(vi) Determine the reaction of inflation to macro-economic shocks in a dollarised economy. (vii) Proffer policies that can be put in place to minimise the adverse impact of external

shocks on price formation in the dollarised Zimbabwean economy. 1.5 Research questions

The thesis seeks to answer the following research questions: (i) What were the determinants of hyperinflation in Zimbabwe?

8

(ii) Did monetary and institutional factors play any role in the incidence of hyperinflation in Zimbabwe?

(iii) What are the implications of the identified factors for the future conduct of monetary policy in Zimbabwe?

(iv) What are the factors that determined inflation in the dollarised Zimbabwean economy? (v) Has there been a shift in inflation dynamics in Zimbabwe through the advent of

dollarisation?

(vi) What is the reaction of inflation to macro-economic shocks in a dollarised economy? (vii) What policies should be put in place to minimise the adverse impact of external shocks

on price formation in the dollarised Zimbabwean economy? 1.6 Significance of the study

The achievement, maintenance and promotion of price stability is a mandate most governments delegate to their central banks. In this regard, central banks the world over have a keen interest in understanding the inflation process in their economies (Mishkin 2007). This interest pertains to both past and future inflation trends and the policy measures that could be put in place to respond to domestic and external shocks that influence price formation. The need to understand the inflation dynamics of a country stems from the social welfare costs of uncontrolled inflation and its adverse impact on the allocative and distributive efficiencies of the economy. High inflation often leads to social unrest as living standards are eroded, leading to political instability, detrimental to economic growth and development. The food riots that occurred in Zimbabwe in 1999 are an example of the adverse repercussions of falling living standards caused by high inflation persistence.

The evolution of Zimbabwe’s inflation dynamics over the years, therefore, needs to be explored. What is of particular interest is the recent high inflation which culminated in hyperinflation, leading to the abandonment of the use of the Zimbabwe dollar (Z$) to perform the standard functions of money and the adoption of the multi-currency system in 2009. Dollarisation of the economy itself brought a new dimension to inflation dynamics given that the country lost its monetary policy autonomy. The analysis of the factors which influenced the behaviour of price formation under these two distinct scenarios is particularly instructive for

9

future policy direction. Understanding the role of monetary policy and institutional factors during the hyperinflation period, in particular, would assist policy makers to institute the necessary reforms in order to avoid a similar occurrence in future should the country decide to re-introduce its own currency. Particularly instructive is the role played by the RBZ an institution which was mandated to maintain the internal and external value of the Z$ but instead, abrogated its primary duty by propagating the inflation scourge through its engagement in unconventional activities.

Zimbabwe’s hyperinflation episode ranks as the second highest in history, surpassed only by the 1946 hyperinflation in Hungary (Hanke and Krus 2012). Nevertheless, there is a general paucity of empirical literature on the causes of inflation in Zimbabwe for both the hyperinflation and dollarisation eras. To the knowledge of this researcher, the only published empirical study on the factors that influenced hyperinflation in Zimbabwe is attributed to Makochekanwa (2007). Makochekanwa (2007) modelled an inflation function for Zimbabwe using an error correction model (ECM), covering the period February 1996 to December 2006. The study concluded that money supply, parallel market exchange rate premium and lagged inflation significantly explained the country’s hyperinflation. Other research works on Zimbabwe’s hyperinflation, for example, Coorey (2007); Munoz (2007), Hanke (2008) and Noko (2011) are largely qualitative.

While these earlier studies are quite insightful in respect of inflation dynamics in Zimbabwe, they did not empirically analyse the role of monetary policy and institutional factors in explaining inflation dynamics in Zimbabwe. This study attempts to bridge that gap by answering two specific questions; firstly what role did monetary policy and institutional factors play in Zimbabwe’s hyperinflation episode, and in this way going beyond the attribution of high inflation to excess money growth. Secondly, what were the major inflation drivers in the dollarised economy after the country adopted the multi-currency system in 2009? The study also extends earlier empirical work by Pindiriri (2012) on inflation dynamics in the dollarised Zimbabwean economy by analysing the reaction of inflation in the dollarised environment to externally generated macro-economic shocks. The policy implications of the results are also analysed, with a view to proffering advice on how the country can minimise the impact of the

10

shocks on price formation given that the country lost monetary policy autonomy upon the adoption of the multi-currency system. Responding to the impact of external shocks on inflation dynamics in a dollarised economy also requires a shift in the mind-set of policy makers as this is tantamount to dealing with a completely different macro-economic situation. This study also demonstrates how an unbridled and uncontrolled central bank can single-handedly destabilise the economy, leading to the debasement of a national currency. Two issues emerge under this scenario, firstly, the importance of appointing professional people to administer the affairs of the central bank and secondly, the need to have an independent and accountable central bank. The significance of inflation expectations in influencing inflation dynamics under periods of hyperinflation, as found by this study, points to the importance of starting the process of confidence building in the economy. In addition, there will also be need for institutions mandated to achieve and maintain price stability to be credible in discharging this mandate in future.

1.7 Summary

This chapter provides a brief account of the background to inflation dynamics in Zimbabwe and the factors that might have contributed to inflation during the period under review. It highlights the fact that Zimbabwe enjoyed relative price stability over the period 1980 to 1990, before experiencing increasing inflation levels during the first and second phases of the IMF supported Economic and Structural Adjustment Programme. During these two distinct periods the RBZ used indirect instruments of monetary policy to control the money supply.

An economic crisis triggered by both internal and external disequilibria led to the implementation of unorthodox policies by the central bank in a bid to reduce spiralling inflation, particularly during the period 2006 to 2008. It was the belief of the RBZ that by printing money and lending to productive sectors of the economy at concessionary rates, output would increase, leading to the dampening of inflationary pressures. The level of money creation by the central bank was, however, unrelated to economic activity and it intensified during the period 2006 to 2008, resulting in excessive monetary expansion. The excess money

11

balances held by the public were used to buy foreign exchange on the parallel market, leading to exchange rate depreciation.

During the same period, the country experienced unprecedented levels of inflation which rendered the local currency worthless as it continued to be subjected to speculative attacks. In response, the central bank adopted a monetary targeting framework as a monetary policy strategy but this did not yield positive results as the level of money creation far outweighed the mopping up levels. The local currency depreciated sharply against major international currencies, losing its function as a medium of exchange. Consequently, economic agents rejected the local currency and started transacting in foreign currencies. The GOZ soon realised that it was a futile exercise to try to force economic agents to transact using a worthless currency and thus formalised dollarisation by introducing the multi-currency system in 2009. Under the multicurrency system, the country uses the US$, pound Sterling, euro, South African rand, Botswana pula, Australian dollar, Japanese yen, Chinese yuan and the Indian rupee for transactions. The US$ and South African rand are the most widely used currencies in the country, with the former being the reference currency.

The chapter also highlights that while there have been insightful studies on hyperinflation in Zimbabwe, for example, Coorey et al. (2007), Makochekanwa (2007) and Hanke and Crus (2012), these studies did not empirically determine the role of monetary policy, institutional and governance factors in influencing inflation dynamics in Zimbabwe. This presents a gap which this study attempts to bridge. In addition, the chapter alludes to the instructiveness of the major factors behind Zimbabwe’s historical hyperinflation, its impact on the economy and its abrupt end; bringing to the fore, the importance of investigating the role of institutional factors in explaining inflation dynamics.

The following chapter provides an overview of economic developments, encompassing the evolution of inflation and monetary dynamics in Zimbabwe over the period 1980 to 2012, to put the influence of monetary policy on hyperinflation and during dollarisation into context. It also provides a detailed analysis of the various policies implemented during the four distinct periods up to 2012 and the related developments on price formation.

12 1.8 Overview of the Thesis

This thesis is organised into nine chapters as follows: Chapter one covers the background to the study, problem statement, objectives and significance of the study. Chapter two gives an overview of economic developments with special emphasis on the evolution of prices over the study period. It highlights the macro-economic developments that are likely to have influenced inflationary dynamics during the study period. Chapter three reviews the theoretical and empirical literature on inflation in general and monetary policy and inflation in particular. The chapter also surveys two different views regarding the formations of inflation expectations, namely the rational expectations hypothesis and adaptive expectations approach. Theoretical and empirical literature on dollarisation and inflation is also reviewed in Chapter three.

Chapter four outlines the research design and methodology used in the study. Chapter five analyses the role of monetary policy and institutional factors during Zimbabwe’s hyperinflation episode. The chapter also discusses the monetary policy actions taken by the central bank in order to ascertain whether they were influential in explaining inflation dynamics in the country. Interestingly, among the fundamental elements of inflation dynamics in Zimbabwe, the central bank has been cited as the major contributor to the hyperinflationary environment experienced by the country (Hanke and Krus 2012; Coorey et al. 2007; Munoz 2007).

Chapter six provides a qualitative analysis of the relationship between central bank independence and inflation in Zimbabwe during the high inflation period. It explores the correlation between the degree of independence of the central bank and inflation in the country. An attempt is made to quantify the independence of the RBZ by applying the Mathew (2006) “new index of institutional quality”. Chapter seven provides an analysis of the factors underlying inflation dynamics in a dollarised economy. The analysis revolves around explaining the significant and abrupt change from hyperinflation to single digit inflation levels. Chapter eight consists of an analysis of the reaction of Zimbabwe’s inflation to macro-economic shocks during the period 2009-2012, building on the results obtained in chapter seven. The summary and conclusion of the study, as well as major policy implications of the findings of the study are covered in Chapter nine.

13

CHAPTER TWO

OVERVIEW OF ECONOMIC DEVELOPMENTS IN ZIMBABWE SINCE INDEPENDENCE 2.1 Introduction

This chapter provides an overview of the macro-economic developments in Zimbabwe, in four distinct phases, namely, the decade of controls (1980-1990), the first and part of the second phase of economic reforms (1991-1996), the economic crisis (1997-2008) and the return to macro-economic stability or the multi-currency era (2009-2012). The chapter places emphasis on inflation dynamics and monetary policy in context of the various policy initiatives undertaken by the Zimbabwean Authorities and overall economic developments.

Zimbabwe emerged from fourteen years of international sanctions which included seven years of a protracted war of liberation when it attained independence in 1980. This, notwithstanding, the new government inherited a sophisticated and well diversified economy (Lyolds Bank 1986) which grew significantly during the first two years of independence. The country experienced substantial social progress during the first ten years of independence but growth in the economy was erratic (GOZ 2000). A combination of structural bottlenecks, poor weather conditions, low investment levels and low international commodity prices militated against the attainment of sustained economic growth (GOZ 2000). In addition, fiscal imbalances which reflected Government’s ambition to build up social services and deliver on the general populace’s expectations built during the liberation struggle also constrained economic growth (GOZ 2000).

The Government of Zimbabwe (GOZ) tried to address the poor economic performance by opening up the economy in 1991, through the adoption of an Economic Structural Adjustment Programme (ESAP), with the support of the International Monetary Fund (IMF) and the World Bank. While the economic reform programme succeeded in liberalising the economy it did not result in the attainment of sustained high growth rates, largely due to persistent fiscal imbalances (RBZ 1999; IMF 2000). More reform programmes were adopted after ESAP but they were largely unsuccessful due to partial implementation of the policy packages and in

14

some cases, outright lack of commitment to the implementation of the formulated economic programmes (IMF 2000)

The onset of an economic crisis in 1997 led to an estimated cumulative 45% contraction in the Zimbabwean economy over the period 2000-2008 (RBZ 2010). Decline in economic activity was typified by exponential growth in inflation, endemic rent-seeking and speculative activities

and persistent shortages of fuel, cash, basic commodities and foreign exchange (RBZ 2010). Social and services sectors such as education, health, electricity and water, as

well as public services also suffered major declines over the crisis period.

The deterioration in domestic macro-economic conditions, in turn resulted in increased de-industrialisation, which resulted in greater in-formalisation as employment opportunities dwindled (RBZ 2010). In addition, the value of the Zimbabwean dollar declined precipitously resulting in the loss of its basic functions as an acceptable medium of exchange, standard for deferred payments and a store of value (Tsumba 2009; RBZ 2010). Consequently, the informal use of stable foreign currencies notably the US$, the British pound, the South African rand and the Botswana pula increased significantly. In response to increased informal dollarisation, the GOZ formally adopted a multiple currency system in January 2009. The adoption of multiple currencies reduced speculative activities and ushered in macro-economic stability epitomised by low and stable inflation.

2.2 The decade of controls (1980-1990)

Zimbabwe experienced high real growth rates during the first two years (1980 and 1981) of independence (IMF 1983; Lloyds Bank 1986; GOZ 1986; Kadhani 1987). The increase in real GDP the country experienced followed the improved security situation, the opening up of the economy and the good 1980/81 agricultural season, enhanced by increased agricultural extension services (GOZ 1986). Increased domestic demand and the lifting of international sanctions against the country also enhanced overall output. The economy registered real GDP growth rates of 10.8 per cent and 13.5 per cent in 1980 and 1981, respectively as shown in Table 2.1 below. Inflation as measured by changes in the consumer price index (CPI) rose from 7.3 per cent in 1980 to 13.8 per cent in 1981.

15

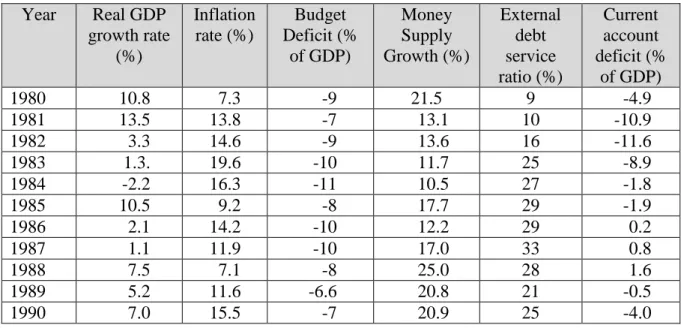

Table 2.1: Zimbabwe: Selected economic indicators (1980-1990) Year Real GDP growth rate (%) Inflation rate (%) Budget Deficit (% of GDP) Money Supply Growth (%) External debt service ratio (%) Current account deficit (% of GDP) 1980 10.8 7.3 -9 21.5 9 -4.9 1981 13.5 13.8 -7 13.1 10 -10.9 1982 3.3 14.6 -9 13.6 16 -11.6 1983 1.3. 19.6 -10 11.7 25 -8.9 1984 -2.2 16.3 -11 10.5 27 -1.8 1985 10.5 9.2 -8 17.7 29 -1.9 1986 2.1 14.2 -10 12.2 29 0.2 1987 1.1 11.9 -10 17.0 33 0.8 1988 7.5 7.1 -8 25.0 28 1.6 1989 5.2 11.6 -6.6 20.8 21 -0.5 1990 7.0 15.5 -7 20.9 25 -4.0

Source: Reserve Bank of Zimbabwe and ZIMSTAT (1991)

A slower growth of 3.3 per cent was registered by the economy in 1982 and this, coupled with the monetisation of fiscal deficits and the devaluation of the Zimbabwean dollar could have, in large part, led to the increase in inflation. The monetisation of budget deficits was necessitated by higher spending against low revenue inflows, as government embarked on a programme of wealth redistribution and infrastructural development. In essence, the GOZ’s main concern was to concentrate on addressing equity considerations through expanded social services, especially in health, education and social development (GOZ 1983; Kadhani 1986). These programmes implied an increase in recurrent expenditure. Recurrent expenditures mainly consisted of wages and salaries, interest on debt and transfer payments and these made up over 90 per cent of total government expenditure.

Zimbabwe’s exchange rate policy during the period 1980 to 1990 was that of ensuring that export competitiveness was at least maintained, if not improved. This objective was achieved by devaluing the exchange rate if the country’s inflation rate was higher than that of its trading partners (RBZ 1982). The local unit declined significantly in both nominal and real terms against all the major currencies between 1982 and December 1990 and this could have influenced inflation. Important to note is that the Z$ was devalued by 20 per cent on

16

December 9, 1982 and was from there-on pegged to a trade-weighted basket of currencies of its major trading partners (RBZ 1982) until 1994 when it was fixed to the US$.

The weights of the currencies in the basket were determined by the total volume of trade (excluding gold and fuel) between Zimbabwe and her major trading partners (RBZ 1982). The weights were constantly reviewed in relation to changes in Zimbabwe’s trade pattern. If the weighted value of the Z$ remained constant against the basket of currencies, then the exchange rate for the local currency in nominal terms on any given day depended on exchange rate movements that took place on the international foreign exchange market; any changes in weights of the currencies in the basket and on any deliberate adjustments by the central bank. In essence, differences in inflation rates and real economic fundamentals between Zimbabwe and her major trading partners in the trade-weighted basket of currencies largely explained the steady decline in the value of the Z$. For example, in 1983 the weighted inflation rate of the countries in the basket of currencies averaged 4.7 per cent, compared to 19.8 per cent for Zimbabwe. Zimbabwe’s annual average rate of inflation stood at 15.5 per cent at the end of December 1990.

A severe drought was experienced by the country in the 1983/84 agricultural season and output in the agriculture sector declined (GOZ 1986). The decline in agricultural output, coupled with depressed demand for the country’s mineral products led to a 2.2 per cent decline in GDP in 1984 (GOZ 1986). The rate of inflation rose from 14.6 per cent in 1982 to 19.6 per cent in 1983; most probably having been influenced by the drought, adjustments in administered prices and an expansionary fiscal policy. This, notwithstanding, as the supply situation improved and some measure of prudence was exercised on the fiscal side, the rate of inflation declined to 16.3 per cent in 1984 and 9.2 per cent in 1985. The trend was, however, reversed when the rate of inflation went up during the first quarter of 1986, ending the year at 14.2 per cent. This could have been partly explained by the increase in administered prices, particularly fuel.

In an effort to arrest the inflation spiral, Government introduced an economy-wide wage and price freeze in June 1987 and managed to contain inflation, which ended the year at 11.9 per

17

cent (RBZ 1991). However, inflation accelerated to 16 per cent in 1990, from 11.6 per cent in 1989, following the June 1989 partial relaxation of the price-wage freeze, the increase in the price of fuel and a significant expansion in money supply (RBZ 1991). In a further attempt to curtail the increase in inflation, the RBZ responded by increasing the rediscount rate, leading to a rise in lending rates.

The decade of controls was also characterised by low productive investment. As such, gross fixed capital formation declined to 15 per cent of GDP in the mid 1980’s, with private investment falling even more rapidly. Public investment expenditure was on average less than one per cent of GDP between 1980 and 1990. The erratic economic performance underscored the need for the country to adopt corrective measures and re-orientate the economy toward a sustainable growth path (GOZ 1991). The country then embarked on economic reforms supported by the International Monetary Fund (IMF) in 1991 (GOZ 1991).

2.3 The first phase of the Economic Structural Adjustment Programme (1991-1995) In the year 1990 a marked deterioration occurred in the macro-economic situation in Zimbabwe; adverse weather conditions reduced agricultural output and downstream industrial activity (GOZ 1997; IMF 1997 and IBRD 1997). In addition, the recession in the world economy and the crisis in the Middle East compounded the problem.

Real GDP growth averaged 2-3 per cent between 1990 and 1991, with inflation rising from an average of 16 per cent in 1990 to 22 per cent in 1991. The rise in inflation was underpinned by high wage settlements, which were unrelated to productivity, partial reduction of food and other subsidies, price decontrols and high fiscal deficits. Slow export growth, against an unprecedented increase in imports, which followed import liberalisation, weakened the balance of payments position. The current account deficit widened to 4 per cent of GDP in 1990 and further to 12 per cent of GDP in 1991. Inflows of capital were not coming in as much as was expected and this led to a decline in net international reserves to about one week of imports by the end of October 1991.

18

The adverse economic developments prompted Zimbabwean authorities to institute a wide range of economic reforms by adopting an IMF supported Economic and Structural Adjustment Programme (ESAP) in 1991. The main objective of ESAP was to stabilise the economy which faced severe internal and external imbalances (GOZ 1991). The reform programme’s specific objectives included among others: reduction of the fiscal deficit from 10 per cent to 5 per cent of GDP by the fiscal year 1994/95; public enterprise reform to eliminate subsidies; monetary and financial sector reform; trade and exchange liberalisation; domestic deregulation and investment promotion; and the implementation of the social dimensions of adjustment (GOZ 1991).

2.3.1 Outcome of the first phase of reform programme

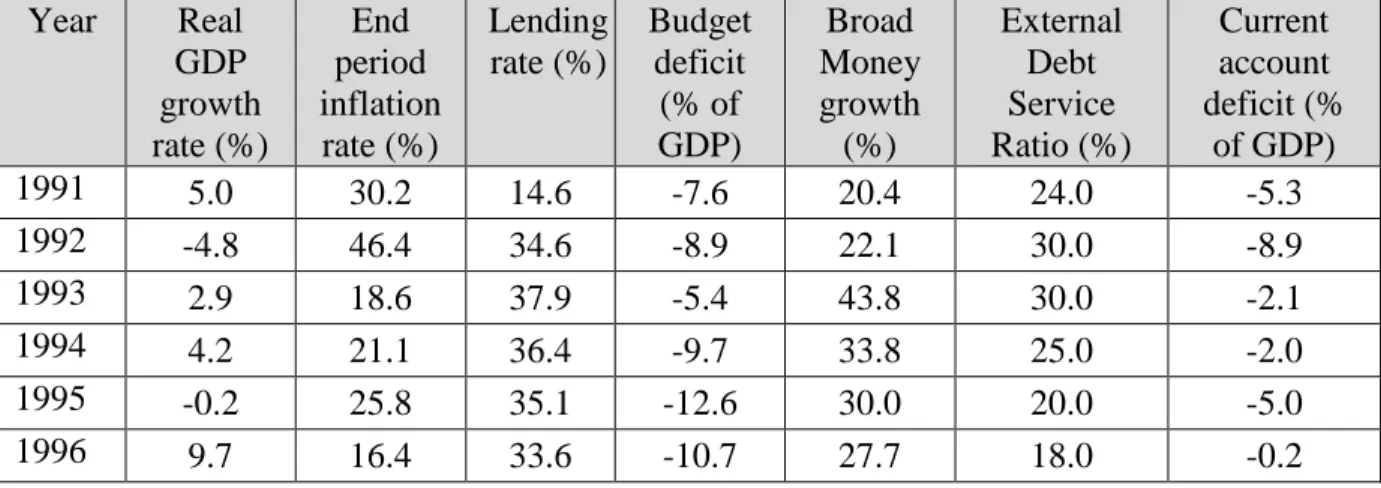

The first phase of the reform programme was generally successful, despite the negative impact of a severe drought the country experienced in the 1991/92 agricultural seasons (IMF 1996; IBRD 1996; GOZ 1996; RBZ 1996). Substantial progress was made in the liberalisation of the foreign exchange, labour and product markets as well as the deregulation of foreign investment (IMF 1996). The economy did not, however, register substantial growth due to macro-economic imbalances as shown in Table 2.2 below.

Table 2.2: Zimbabwe: Selected economic indicators (1991-1996) Year Real GDP growth rate (%) End period inflation rate (%) Lending rate (%) Budget deficit (% of GDP) Broad Money growth (%) External Debt Service Ratio (%) Current account deficit (% of GDP) 1991 5.0 30.2 14.6 -7.6 20.4 24.0 -5.3 1992 -4.8 46.4 34.6 -8.9 22.1 30.0 -8.9 1993 2.9 18.6 37.9 -5.4 43.8 30.0 -2.1 1994 4.2 21.1 36.4 -9.7 33.8 25.0 -2.0 1995 -0.2 25.8 35.1 -12.6 30.0 20.0 -5.0 1996 9.7 16.4 33.6 -10.7 27.7 18.0 -0.2

Source: Reserve Bank of Zimbabwe and ZIMSTAT (1997)

High budget deficits of close to 10 per cent of GDP resulted in monetary policy bearing the burden of managing demand and consequently leading to unsustainably high lending rates.

19

Lending rates rose to levels of above 30 per cent in 1992, constraining the productive sectors of the economy. The economy could not, therefore, generate the necessary supply response, critical for achieving sustainable economic growth. The rate of inflation increased from 30.2 per cent in 1991 to 46.4 per cent in 1992, largely explained by quite a number of factors. First, was the partial reduction of food and other subsidies as well as price decontrols, in line with the economic reforms; and second, high wage settlements. The price decontrols were put in place against the background of a supply constrained economy, which is likely to have put upward pressure on prices.

In addition, rapid monetary expansion, coupled with the rise in the local currency credit requirements of the private sector as foreign exchange became readily available, could also have contributed to the rise in inflation. The distortions built up in the economy between 1980 and 1990 (the pre-reform period) could also not be readily absorbed by the liberalised economy without an increase in prices. The rise in inflation during the period of economic reform could also be attributed to the effects of a devastating drought, which hit the country in the 1991/92 agricultural season. Inflation peaked at 49.1 per cent by August 1992, as Government injected financial resources into the market to finance food imports. The RBZ responded to the rise in inflation by raising the rediscount rate (rate at which commercial banks borrowed from the central bank) from around 21 per cent in January 1992 to 30 per cent by September 1992 and this paid dividends. The rate of inflation declined to 18.6 per cent by the end of 1993, prompting the central bank to lower the rediscount and overnight accommodation rates to 28.5 per cent in September 1993.

Inflation, however, took an upward trend in the first half of 1994, forcing the central bank to raise the rediscount rate to 30 per cent and reserve ratios from 13.5 per cent to 17.5 per cent. There was excessive monetary expansion in the second half of the year 1994, which reflected the improvement in net foreign assets, as the country liberalised its trade and exchange rate systems (RBZ 1995). Inflationary pressures continued to mount as another bad agricultural season was experienced in 1994/95, adversely affecting economic growth. The situation was aggravated by fiscal slippages, drought-induced shortages, increased sales tax and excise duties, as well as the increase in administered prices.