The Finnish Maritime Cluster

Mikko Viitanen, Tapio Karvonen, Johanna Vaiste and Hannu Hernesniemi

Technology Review 145/2003

The Finnish Maritime Cluster

Mikko Viitanen Tapio Karvonen

Johanna Vaiste Hannu Hernesniemi

National Technology Agency Technology Review 145/2003

Tekes – your contact for Finnish technology

Tekes, the National Technology Agency, is the main financing organisation for applied and industrial R&D in Finland. Funding is granted from the state budget.

Tekes’ primary objective is to promote the competitiveness of Finnish indus-try and the service sector by technological means. Activities are aimed at di-versifying production structures, increasing productivity and exports and creating a foundation for employment and social well-being. Tekes finances applied and industrial R&D in Finland to the extent of nearly 400 million euros annually. The Tekes network in Finland and overseas offers excellent chan-nels for cooperation with Finnish companies, universities and research insti-tutes.

Technology programmes – part of the innovation chain

The technology programmes are an essential part of the Finnish innovation system. These programmes have proved to be an effective form of coopera-tion and networking for companies and the research sector for developing innovative products and processes. Technology programmes promote de-velopment in specific sectors of technology or industry, and the results of the research work are passed on to business systematically. The pro-grammes also serve as excellent frameworks for international R&D coopera-tion. Currently, 35 extensive technology programmes are under way.

Copyright Tekes 2003. All rights reserved.

This publication includes materials protected under copyright law, the copyright for which is held by Tekes or a third party. The materials appearing in publications may not be used for commercial purposes. The contents of publications are the opinion of the writers and do not represent the official position of Tekes. Tekes bears no responsibility for any possible damages arising from their use. The original source must be mentioned when quoting from the materials.

ISSN 1239-758X ISBN 952-457-135-8

Translation from Finnish: Susanna Saarikivi Cover: LM&CO

Page layot: DTPage Oy Printers: Paino-Center Oy, 2003

Foreword

For some time now, there has been a need for an objective study of the importance of the maritime sector in the Finnish National Economy. The lack of such a study has specifically come up in dis-cussions on the Finnish maritime policy and the contents and scope of subsidies to shipyards. The primary purpose of this study, The Finnish Maritime Cluster, is to define the importance of the maritime cluster in Finland, to determine the patterns of networking within this cluster and to de-scribe its economic and social impacts. The study was launched after the completion of various pre-studies on the subject. Formally commissioned by the Association of Finnish Maritime Indus-tries, this project t was carried out in co-operation by several fields.

The study was conducted by the Turku University Centre for Maritime Studies and by Etlatieto Oy. The project leaders were Senior Researcher Mikko Viitanen from the Centre for Maritime Studies and Research Director Hannu Hernesniemi from Etlatieto. In addition to the leaders, Researchers Tapio Karvonen and Johanna Vaiste from the Centre for Maritime Studies were involved in the work. Scholarship researchers Marika Mäkinen and Anne Sassi also took part in the study and wrote their master’s theses on the subject. The work of the scholarship researchers was funded by the Finnish Navigation Fund (Merenkulun Säätiö).

The study was directed by a steering group. The Chairman of this group was Mikko Niini from Kvaerner Masa-Yards. The members of the steering group were Rauli Hulkkonen from Tekes, Manu Harmo and Risto Paaermaa from the Ministry of Trade and Industry, Raimo Kurki and Harry Favorin from the Ministry of Transport and Communications, Henrik Nordell from the Association of Finnish Marine Industries, Hans Ahlström from Ålands Redarförening, Pertti E. Aalto from Fortum Shipping, Tuomas Nylund from Silja Line, Cristian Ramberg from the Port of Turku, Matti Sommarberg from Kalmar Industries, Eve Tuomola-Oinonen from the Port of Helsinki and Juhani Vainio from the Centre for Maritime Studies. This study was funded by Tekes and the above-men-tioned Ministries, Associations, Companies and Ports.

In other European countries, cluster studies have proved an important tool for the objective consid-eration of questions concerning industrial, regional and educational policies. It is my hope that this study will also help the Finnish decision-makers arrive at the right conclusions and that it can be used as a guideline for constructive national-level decision-making.

As the Chairman of the steering group, I wish to thank the researchers, the steering group, the par-ties providing the financing and the supporters of this study, as well as the companies who made this study possible by taking part in and being interviewed for it.

Helsinki, May 2003 Mikko Niini

Abstract

The maritime cluster in Finland consists of several sectors, such as those associated with shipping, marine industries and port operations in the private and public sectors. The main objective of the Finnish Maritime Cluster study was to assess the significance and map the networks of this cluster in Finland as well as to describe its economical and social importance.

The study involved a comprehensive enquiry carried out amongst the most important companies of the various sec-tors in the maritime cluster to establish its economical and employment-related impacts. This enquiry covered some 260 companies by means of interviews and other methods. In addition to private sector companies, this figure also in-cludes ports operating in the public sector. Additionally, the conductors of the study had access to data collected by the Tax Administration and Statistics Finland on some 2,400 companies associated with the maritime cluster, whose names came up in connection with the study. The to-tal turnover of all companies directly associated with the maritime cluster is some 11.4 milliard Euro. The maritime cluster directly employs approximately 47,000 people in the private sector and in ports. Its indirect impacts seen through consumption are manifold.

The maritime cluster is a functional entity in which the var-ious industries, such as shipping, marine industries and port operations, are in close interaction with one another not only directly but also through their company networks. Through these networks, the large companies in the mari-time cluster extend their influence to the whole country, excluding the northernmost parts of Lapland. The econom-ical impact of the maritime cluster is the most significant in the Åland Islands, as well as in the regions of Helsinki, Turku and Rauma. The majority of the companies associ-ated with this cluster are naturally locassoci-ated on the coastline, but there also is a large number of maritime cluster compa-nies inland.

In the enquiry carried out in companies for this study, it came up that co-operation and networking between compa-nies is regarded as very important in the increasingly tough competitive situation. The inquiry also raised the question of government aids offered by different countries. These aids distort the competitive situation in ship-building and maritime transports. The companies in the Finnish mari-time cluster want to see themselves in an operating climate corresponding to that of the companies in competitor coun-tries. The companies also emphasise the importance of im-proving the image of the marine industries and ensuring the availability of a labour force in the future.

Because of the country’s geographical location, maritime transport is essential for the Finnish economy. Further de-velopment and efficiency of maritime transport and ports are vital for the competitiveness of our export industry. Ports and the companies operating in them are crucial links in the foreign trade logistics chain.

The large companies in the maritime cluster are highly in-ternational and play an important part in the export indus-try. These companies attract notable cash flows to the Finn-ish national economy, which in turn contributes greatly to the welfare of the Finnish society. Typical features of large maritime cluster companies are the application of ad-vanced technology and a high level of innovation, which have resulted in a significant growth potential in their com-pany networks in particular. The maritime cluster has de-veloped to include important activities in associated fields, such as insurance, financial services and maritime classifi-cation.

The public sector plays an important role in the maritime cluster. As the economy develops, the scope of co-opera-tion between the private maritime sector and public admin-istration has become increasingly wide.

Key words: maritime cluster, shipping, marine industry, port operations, sub-contractor network, national econ-omy, competitiveness

Contents

Foreword Abstract

1 Introduction . . . 1

2 Previous Research, Statistics and the Maritime Sector World Market . . . 3

2.1 Preliminary Work on the Maritime Cluster and Cluster Studies in Finland . . . 3

2.2 The Maritime Cluster in Statistics . . . 5

2.3 Maritime Cluster Research Abroad . . . 8

2.3.1 The Swedish Maritime Cluster Study . . . 8

2.3.2 The Dutch Maritime Cluster Study . . . 9

2.3.3 The German Maritime Cluster Study . . . 11

2.3.4 The Norwegian Maritime Cluster Study . . . 11

2.3.5 The Italian Maritime Cluster Study . . . 12

2.3.6 The EU Study of the Economic Impact of Marine Industries in Europe . . . 12

2.4 The Maritime Sector World Market and Finland . . . 13

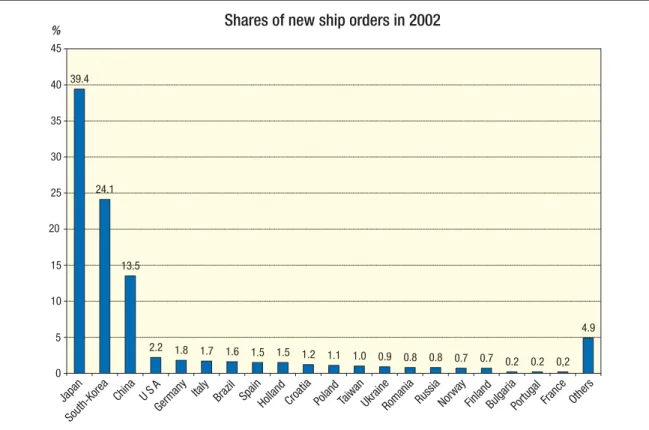

2.4.1 Current Situation in the Shipbuilding Market . . . 13

2.4.2 The World Merchant Fleet and Maritime Transport . . . 15

3 Theoretical Framework of the Study . . . 19

3.1 Cluster Analysis . . . 19

3.1.1 The Cluster . . . 19

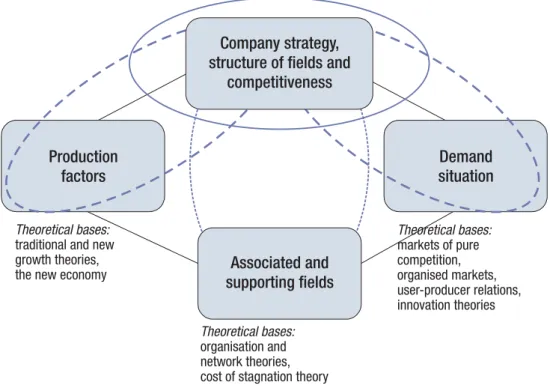

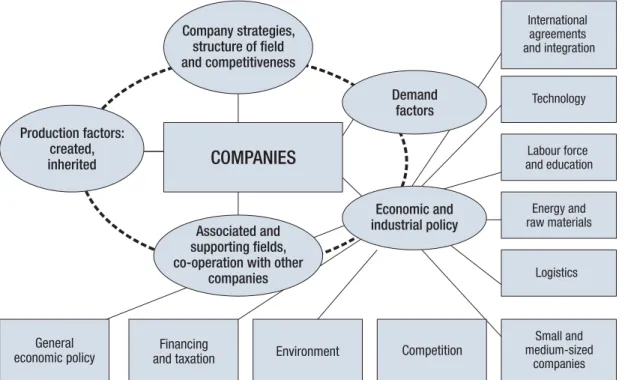

3.1.2 Competitiveness . . . 20

3.1.3 The Competitiveness Model . . . 20

3.1.4 The Impact of Public Authorities of Competitiveness . . . 23

3.2 Economic Impact Study (EIS). . . 24

4 Materials and Methods . . . 27

4.1 Questionnaire Study. . . . 27

4.2 Profit and Loss Statements and Asset and Liability Statements Provided by the Tax Administration . . . 28

4.3 Other Material. . . 28

5 Results of the Questionnaire Study . . . 29

5.1 Company Information. . . 29

5.1.1 Shipbuilding, Ship-Repairing and Subcontracting . . . 29

5.1.2 Maritime Transport – Shipping Companies, Ports and Their Related Companies . . . 31

5.2 Competition Situation. . . . 33

5.2.1 Shipbuilding, Ship-Repairing and Subcontracting . . . 33

5.2.2 Maritime Transport – Shipping Companies, Ports and Their Related Companies . . . 37

5.3 Customer Relations and Demand . . . 43

5.3.1 Shipbuilding, Ship-Repairing and Subcontracting . . . 43

5.3.2 Maritime Transport – Shipping Companies, Ports and Their Related Companies . . . 45

5.4 Co-operation . . . 48

5.4.1 Shipbuilding, Ship-Repairing and Subcontracting . . . 48

5.4.2 Maritime Transport – Shipping Companies, Ports and Their Related Companies . . . 51

5.5 Production Factors. . . 57

5.5.1 Shipbuilding, Ship-Repairing and Subcontracting . . . 57

5.5.2 Maritime Transport – Shipping Companies, Ports and Their Related Companies . . . 57

6 Results of the Strategy Questions . . . 59

6.1 Shipbuilding and Ship-Repairing Companies . . . 59

6.2 Subcontractors of Shipbuilding Companies . . . 61

6.3 Shipping Companies . . . 65

6.4 Ports . . . 68

6.5 Companies Related to Shipping Companies and Ports . . . 70

7 The Maritime Cluster in the Finnish National Economy . . . 75

7.1 Defining the Maritime Cluster and its Sectors . . . 75

7.2 Need for the Maritime Sector in Finland . . . 76

7.2.1 Supply and Demand of Maritime Transport Between Finland and Other Countries . . . 76

7.2.2 Port Operations in Finland . . . 80

7.2.3 Shipbuilding and Ship-Repairing in Finland. . . 81

7.2.4 The Subcontractor Network of the Maritime Sector . . . 82

7.3 Locations of the Maritime Cluster Companies. . . 82

7.4 Influence of the Maritime Cluster on the National Economy in Figures . . . 84

7.4.1 Influence of the Maritime Cluster on the Economy and Employment . . . 84

7.4.2 Impact of the Maritime Cluster on Finland’s Imports and Exports . . . 89

7.5 The Shipbuilding Industry in the Finnish National Economy . . . 90

7.5.1 The Shipbuilding Industry and the Income Circulation Model . . . 90

7.5.2 The Current Situation of the Shipbuilding Industry From the Viewpoint of the National Economy . . . 91

7.5.3 The Cost Structure of Shipbuilding in Finnish Shipyards . . . 92

7.5.4 Impact of the Shipbuilding Industry on Employment in the Finnish National Economy. . . 93

7.5.5 Current Cost Level of Labour. . . 93

7.5.6 Shipbuilding Subcontractors . . . 95

7.6 Merchant Shipping in the Finnish National Economy . . . 96

7.6.1 Production Factors of Shipping . . . 97

7.6.2 Influence of Shipping on the Current Account. . . 99

7.6.3 Government Involvement in the Shipping Market . . . 101

7.6.4 Shipping and the Environment . . . 103

7.7 Ports and Port-Related Companies in the Finnish National Economy . . . 104

7.7.1 Ports in the Finnish National Economy . . . 104

7.7.2 Port-Related Industry in Finland . . . 106

7.8 The Role of the Public Sector and Interest Groups in the Maritime Cluster . . . 106

7.9 Comparison of Economic Policy Choices Using the EIS Analysis Method . . . 108

8 Analysis of the Competitiveness of the Maritime Cluster . . . 117

8.1 The Maritime Cluster Parts and the Cluster as a Whole . . . 117

8.2 Shipbuilding and the Marine Industries . . . 117

8.3 The Partial Clusters of Merchant Shipping . . . 133

8.4 Ports and Their Actor Network. . . 148

8.5 Manufacturing of Port and Cargo Handling Technology . . . 159

8.6 The Mutual Development Dynamics of the Different Parts of the Maritime Cluster and their Effects on Competitiveness . . . 166

8.7 Synergies Between the Maritime Cluster and Other Clusters . . . 170

8.8 Conclusions and Recommendations . . . 174

9 Conclusions . . . 179

Sources . . . 181

Appendix The companies that took part in, that were interviewed for and that were otherwise taken into account in the course of this study . . . 185

1

Introduction

Maritime industries are extremely important for Finland. Because of Finland’s geographical location, maritime transport is essential for the country and without a doubt the most important form of transport in Finnish foreign trade. Port-related industries operate on a highly interna-tional level and attract important cash flows from the inter-national market into the inter-national economy. The function-ing of ports and maritime transport is essential to the Finn-ish export industry.

For many years, several different organisations have been hoping for a Finnish maritime cluster study. In the spring of 2002, the maritime cluster research project began. The for-mal commissioner of the study was the Association of Finnish Marine Industries (AFMI), and it was financed by the National Technology Agency Tekes, the Ministry of Transport and Communications, the Ministry of Trade and Industry and the most significant companies and associa-tions of the field. A steering group made up of experts rep-resenting the most important maritime cluster companies, ministries and associations led the research work.

The aims of the study were to define the maritime cluster networks and to describe the economic and social impact of the maritime cluster in Finland. The maritime cluster in-cludes, for example, businesses related to shipping, the ma-rine industries and port operations in the public and private sectors. This study describes the whole Finnish maritime cluster. International studies have shown that maritime clus-ter fields inclus-teract closely with one another. However, it has never been understood in Finland that the different maritime industries have the potential to form a functioning whole.

A broad company inquiry covering different maritime in-dustries was conducted as part of the study. The question-naires used in the study were formulated according to clus-ter theories and studies conducted in other countries. It was important to establish the way in which Finnish maritime companies formed buying, selling and co-operation net-works. The questionnaires provided the researchers with information directly from company management concern-ing such issues as the operations, competitiveness factors and future prospects of the companies. About 210 compa-nies took part in the inquiry. Company management was interviewed on site, over the telephone and/or by a ques-tionnaire sent by post. In addition, the inquiry material was supplemented with additional information covering 50 of the most important cluster companies. The information concerning these companies mainly came from the Tax Administration and from the companies’ annual reports.

The information obtained by means of the questionnaires can be used to improve the operating conditions and com-petitiveness of the maritime cluster companies.

The study was carried out by the Turku University Centre for Maritime Studies and Etlatieto Oy. The Centre for Mar-itime studies was responsible for about two thirds of the study. The researchers in charge of the study were Senior Researcher Mikko Viitanen from the Centre for Maritime Studies and Research Director Hannu Hernesniemi from Etlatieto Oy. Research work was also carried out by Re-searchers Tapio Karvonen and Johanna Vaiste from the Centre for Maritime Studies and scholarship researchers Marika Mäkinen and Anne Sassi. The scholarship re-searchers also wrote their master’s theses based on the study. Their work was financed by the foundation Meren-kulun säätiö. This report was translated by Susanna Saari-kivi from the Centre for Maritime Studies.

The first part of the study is a broad overview of the time cluster studies conducted in other countries, the mari-time cluster world market and the role of Finland in this world market. The theoretical framework of the study is presented inChapter 3. The materials and methods of the study are discussed inChapter 4.The results of the com-pany inquiry are detailed inChapters 5 and 6.The inquiry included questions concerning the maritime sector compe-tition situation, client relations, demand, co-operation and production factors. In addition, the company manage-ment’s views on company strategy were covered.

The results of the study, the theoretical framework, the for-mer studies, expert opinions and studies from other coun-tries were used in the analysis of the results inChapters 7 and 8. The work of analysing the results was divided be-tween the Centre for Maritime Studies and Etaltieto Oy. The section on the economic impact of the maritime cluster (Chapter 7) was written by CMS researchers Mikko Viitanen, Tapio Karvonen and Johanna Vaiste. The influ-ence of the maritime sector for the whole of Finland and from the viewpoint of different industries is discussed in Chapter 7. In this Chapter, the study also provides more de-tail by means of an EIS-analysis based calculations on the current and future operative levels and cost structures of different maritime industries. The competitiveness analy-sis inChapter 8was written by Hannu Hernesniemi from Etlatieto Oy. Marika Mäkinen and Anne Sassi also contrib-uted to this Chapter.Chapter 9is a brief overview of the re-search results.

2

Previous Research, Statistics and

the Maritime Sector World Market

2.1 Preliminary Work on

the Maritime Cluster and

Cluster Studies in Finland

Suomen Meriklusteri 2000

The Finnish Navigation Fund decided in its meeting on the 12thof June, 2000 to carry out a study of the Finnish maritime cluster. Master of Science in Engineering Timo Korhonen was given the task of conducting the study. The finished study, Suomen Meriklusteri 2000, was published on the 15th of September. It summed up studies conducted in different countries and also contained an interview-based study that, based on opinions obtained from different sources, re-vealed the need for a Finnish maritime cluster study.

Preliminary Research on Maritime Clusters in Finland

In its meeting on the 12thof March, 2001, the cluster work-ing group heard the opinions of different experts on carry-ing out a maritime cluster study in Finland. At this in-stance, the Turku University Centre for Maritime Studies offered to conduct the preliminary study of the Finnish Maritime Cluster Study. The Centre for Maritime Studies has a long experience in conducting domestic and interna-tional research projects in the fields of shipping, transport and logistics. The meeting recommended that the Ministry of Transport and Communications and the Ministry of Trade and Industry finance the preliminary study, and the Ministries later made the decision to do so.

The Centre for Maritime Studies conducted the prelimi-nary study to serve as a basis for the Finnish Maritime Cluster Study. During the preliminary study, the cluster working group and the representatives of the Centre for Maritime Studies met on a few occasions. In these meet-ings, the different stages of the study were presented to the working group and the group members gave their opinions on what should be emphasised in the future.

As the work progressed it was noted that certain terms and the theoretical framework of the study had been interpreted in different ways, which had led the researchers to use dif-ferent research methods and to get difdif-ferent results. As a consequence, the researchers had to redefine the concept of the cluster and to try and find the best methods for conduct-ing the actual research.

The preliminary research described, in detail, studies con-ducted in Holland and in Germany. The aim was to gain an understanding of how a similar study should be carried out in practice in Finland. In addition, the preliminary research was conducted to show how the actual study could benefit the government and the companies of a country. The pre-liminary study was not published separately, but the infor-mation gathered for it has been used in drafting this mari-time cluster research report.

Finnish Cluster Studies

Etla and its subsidiary Etlatieto Oy began cluster studies in Finland in 1992.1The beginning of the 1990’s was a time of deep economic depression in Finland. Economic and po-litical leaders as well as researchers were concerned for the level of competitiveness and the regeneration ability of the whole national economy. For example, the share of exports in the gross national product of Finland had decreased since the beginning of the 1980’s. Managers of the most important companies, the Permanent Under-Secretary of State of the Ministry of Trade and Industry and representa-tives from the Academy of Finland and different universi-ties participated in the steering group of the first cluster study. However, there were no representatives from the maritime cluster core companies in the group. The role of the steering group was important in the study, because the group was the first to know the results of the study before it was published. The group’s comments on the results had an impact on the final form of the publication.

1 As early as in 1987–1988, Professor Micael Porter invited Finland to join in an extensive international research project, in which the foundations for cluster studies were built on the basis of competitiveness studies conducted in 10 countries. The study also led to the publication of the Competitive Advantage of Nations in 1991. Porter’s offer was not accepted.

This research project and its 60 publications had a great im-pact on society.2

The project laid grounds for future indus-try and technology policies. In his doctoral thesis, “Klusteri tieteen ja politiikan välissä”, Jari Jääskeläinen documented the impact of this project on the society.3In the spring of 1993, the project researchers wrote Kansallinen

teollisuus-strategia, the national industrial strategy scheme together

with the leading officials of the Ministry of Trade and In-dustry. This strategy was accepted by the Finnish compa-nies, the central ministries and the VTT Technical Re-search Centre of Finland, Sitra (the Finnish National Fund for Research and Development), Tekes, the Academy of Finland and Finpro, the association that carries out the Finnish science and technology policy in practice. It was specifically the idea of the cluster and the implementation of cluster theories in planning different policies that was new in the strategy. There was also a marked shift away from the old industrial policy that supported and protected losers towards a policy that would create favourable oper-ating conditions for traditionally strong branches and new, growing branches of industry. The policy was to be carried out by training, research, product development, risk fi-nancing of technology and new businesses, and by devel-oping markets, removing obstacles preventing the develop-ment of trade and economic growth (integration policy) and presenting challenges (i.e. environmental regulations, energy policy) that promote competitiveness.4

In this project, the Finnish forest cluster was identified as a strong cluster. It includes, in addition to the competitive pa-per and cellulose industry, a globally active machine indus-try and a very well developed international service sector. The metal refinement and energy clusters were seen as me-dium strong clusters. Both have increased their market share in the world trade during the 1990’s. The export of energy technology nearly quadrupled in that time. Accord-ing to the cluster studies, the potential growth clusters in Finland were the transport cluster, the environment cluster, the welfare cluster and the telecommunications cluster, which was estimated to grow into another cornerstone of the Finnish economy beside the forest cluster. This indeed happened, and Finland has become very dependent on the telecommunications cluster, as recent developments in the economy have shown. In contrast, the welfare cluster was a disappointment to the researchers. The Finnish social and health services have not been able to renew themselves nor has the welfare cluster given rise to important companies

with the potential to expand to the international level. Fur-thermore, the welfare cluster has not developed successful international technology exports as other successful clus-ters have done. Finally, the environmental cluster was not seen as a separate unit but one divided among all the other clusters.

It was discovered that the transport cluster, earlier seen as a potential growth cluster, was very scattered. This is why small-scale, individual studies were conducted concerning the shipbuilding industry, passenger ship traffic and transit traffic to and from Russia. Of these industries, transit traf-fic seemed to have the best potential for growth. In addi-tion, it was noted that import and export transports were very important for several industries, especially the forest and metal refinement industries. A report that would have integrated these partial reports concerning the maritime cluster was never produced, as was the case for the reports concerning the other clusters. Because of this, the determi-nation of the maritime cluster’s true structure and the iden-tification of its strengths (products and companies) as well as a study its competitiveness (know-how, technology, mu-tual synergies) were never completed at this stage.

In addition to the clusters mentioned above, two clusters defined as latent were studied – the construction cluster and the food cluster. The construction cluster was in a deep cri-sis, as almost one half of the people working in construc-tion had been laid off during the depression. However, two strong fields were identified within the building cluster: building engineering product development and the build-ing material industry. The food cluster was studied because it was at the time adapting to totally new conditions. It’s main raw material supply area changed from Finland to Eu-rope and its 5 million strong consumer market changed into a 250 million strong consumer market when the border control of prices was removed.5

After this, new cluster studies have been carried out by Etla on the forest cluster, the telecommunications cluster, or in broader terms the ICT cluster, and the energy cluster. After the completion of studies funded by The Ministry of La-bour and the European Social Fund, a study of the key clus-ters supporting Finnish industries and employment was conducted.6The Finnish cluster know-how has also been exported to, for example, Ireland, Japan and Chile through consultation projects. Studies applying the cluster analysis

2 The partial reports have been listed in the final reports of the project Kansallinen kilpailukyky ja teollinen tulaveisuus, Etla B105, 1995 and Advantage Finland, The Future of Finnish Industries, Etla B115, 1996.

3 Jari Jääskeläinen Klusteri tieteen ja politiikan välissä – Teollisuuspolitiikasta yhteiskuntapolitiikkaan, doctoral thesis, University of Jyväskylä, Etla A 33, 2001.

4 Kansallinen teollisuusstrategia, Ministry of Trade and Finance 1/1993 and National Indutrial Strategy for Finland Ministry of Trade and Finance 3/1993

5 Later, “The chemical cluster – home from abroad” was published at the initiative of the Kemian keskusliitto. It is included in the publication Advantage Finland, Etla B115, 1996 and the The Finnish Hotel and Restaurant Council commissioned the study Laman varjosta uudelle vuosituhannelle.

6 Suomen energiaklusterin kilpailuetu, Etla B154, 1999. Metsäklusteri Suomen kansantaloudessa, Etla B161, 2000. Finnish ICT cluster in the digital economy, Etla B176, 2001. Suomen avainklusterit ja niiden tulevaisuus, ESR publications 88/01.

have been conducted on the Baltic Sea countries, and the latest series of cluster studies were conducted on North-West Russia.7

One of the central roles of Etla is to work within the inter-face between the industries and the government (including international organisations and inter-governmental organi-sations ) in order to produce information that will help in developing the competitiveness of companies. Etla also helps in processing this information into concrete strate-gies and measures. Different ministries and institutions providing financing, such as Tekes, Finpro and Teollisuus-sijoitus, have been consulted on the basis of the cluster studies. Etla also took part in the development and refine-ment of the cluster study in the OECD and the EU8.

2.2 The Maritime Cluster

in Statistics

The maritime cluster is made up of companies from several different sectors. This is why presenting statistics on this cluster is a challenging task. On the other hand, Finland produces a wide array of statistics. Yearly, and in some cases monthly, statistics of diverse fields are available. Be-cause the compilation of statistics has a long tradition in Finland, information covering long periods of time is avail-able. In the following, the most important phenomena and the statistics that portray them are discussed.

The Maritime Cluster in the Accounts of the National Economy

The accounts of the national economy depict the supply and demand of the nation. Supply is made up of the produc-tion and the exports of different industries. Demand, on the other hand, is made up of private and public consumption, investments and imports. The strength of the national ac-counts lie in the fact that they are extensive and also consis-tent in the sense that in supply and demand have to be in balance. Different statistics are used in drafting the ac-counts of the national economy, but for some parts we have had to rely on estimates.

The maritime cluster is made up of different industries. The most important variables of the national accounts when looking at the different industries of a country are the gross value of production and value added. The gross value of production of an industry is about the same as the total turnover of that industry. The value added is the difference between the value of sales and purchases of the industry.

The value added of all the industries can be combined to produce the gross value of all the industries of the country, or the gross national product. Other variables in the na-tional accounts are the number of people employed, the number of working hours, and the amounts of investments, imports and exports.

Because the maritime cluster is divided into different fields, it cannot be identified as such in the national ac-counts, even if information concerning each maritime in-dustry was available separately. In the 2001 statistics, the value added of the manufacturing of vehicles was EUR 1,041 million, of which the share of the value added of shipbuilding was EUR 438 million. The value added of wa-ter traffic, which includes sea and inland wawa-terway traffic, was EUR 765 million. In shipbuilding, the networking of production has led to a situation where simply calculating the value added of the industry is an inadequate way of measuring the value added of the whole production pro-cess. The value added of the whole production process is included in the value of gross production, which was EUR 2,069 million. This figure does not, however, tell us much about the industries in which the input sold was produced or the amounts of labour required in the subcontractor chains of different fields.

In order to clarify these facts, input-output tables are needed. These tables show, for example, in which indus-tries the productive inputs used by other indusindus-tries are pro-duced. Using this information, the input coefficients can be calculated, with the help of which the labour input of pro-duction and the amount of working hours and man-years be estimated. The input-output tables have been criticised for the fact that they do not take into account business between different industries in adequate detail. In addition, it is thought that too much of the basic information included in the tables is based on estimates and guesses. However, in practice, the input-output tables are the only calculation tool with which the multiplicative effects of the production and the employment of different industries on the national economy can be calculated.

Business Activity and Production Statistics of Different Industries

The company register of Statistics Finland, among other sources, offers statistics concerning the business activities of companies. It provides specific, detailed information on the number of offices, the turnover, the staff numbers and the wage expenses of companies in different fields. How-ever, the statistics only cover the companies liable to pay trade tax. The activities of the government are left outside

7 The North-West Russian cluster studies have been published as Emerging Clusters of Northern Dimension, Etla B197, From Russian Forests to World Markets, Etla B196, Energy3

– Raw Material, Production and Technology, Etla B197, The Melting Iron Curtain, Etla B198 and Busy Line, Hectic Programming, Etla B199. All published in 2003.

8 See for example Rouvinen, Ylä-Anttila, ”Finnish Cluster Studies and New Industrial Policy Making” in Boosting Innovation – The Cluster Approach, OECD 1999.

these statistics. For example, many ports do not operate as companies, and this is why their data cannot be found in the company register. In addition, the register does not contain information on, for example, the number of personnel working in education or research institutions or other gov-ernment units that serve the maritime cluster.

Statistics Finland provides very detailed statistic called The

Statistics on the Structure of Industry and Construction. This

offers easy access to information on the numbers of com-pany offices, the personnel and main personnel groups, working hours, wages, social security costs, numbers of entrepreneurs, the gross value of production and the value added and investments and imports in Finland. In addition, the inputs used in production have been detailed in the sta-tistics. Information is available on, for example, the cost of materials and supplies, repair services, maintenance and installation work, subcontracting, IT, design, program-ming and research services. The Statistics on the Structure of Industry and Construction gives a broad view of such ac-tivities as shipbuilding, ship-repairing, the manufacturing and repairing leisure boats and hydraulic engineering.

The Statistics on the Structure of Industry and Construction also contains information on the value and number of goods produced. For example, in 2001, 464 ship diesel en-gines were manufactured in Finland. Their market value was EUR 419 million. A total of 310 forklift trucks and portal cranes were manufactured and their total market value was EUR 167 million. The sales revenue from three cruisers that were sold was EUR 1,271 million and the sales revenue from two ferries sold was EUR 208 million. Drilling rigs and production rigs were manufactured for the value of EUR 255 million.

The Foreign Trade statistics compiled by Customs contains information concerning the export activities of the ship-building industry, the marine industries and the manufac-turers of port and terminal technology. Detailed informa-tion on the amount and value of exports of different coun-tries can be obtained from these statistics. Of course, infor-mation concerning competing imports can also be obtained from the same source. The foreign trade statistics contains over 6,000 entries. If the exact value of the maritime cluster exports were to be established, those goods that are consid-ered part of the maritime cluster production would have to be picked out from these statistics. With this information, the values of imports and exports could be followed sys-tematically. This kind of follow-up is already being done, for example, concerning the exports of energy technology and the goods exports of the building industry. At the same time, with the help of the OECD and EU statistics, the share of Finnish exports in the maritime clusters imports to different countries could be calculated.

Information concerning the economy of Finnish ports is presented in the statistical publication Suomen

satama-liiton tilastot produced by the Finnish Port Association.

This statistic gives information on traffic volumes includ-ing transit traffic and container traffic, and the income, ex-penditure, investments and fixed assets of ports. The infor-mation is also presented in the form of a profit and loss ac-count. In addition, this publication gives information on the staff numbers and capacities of ports. One half of the Finn-ish ports are members of the FinnFinn-ish Port Association, but over 90% of the Finnish maritime traffic passes through the member ports. The Finnish Maritime Association also pub-lishes the statistics Tavara- ja matkustajaliikenne aluksilla

Suomen Satamissa, which contains detailed information on

goods and passenger traffic in Finnish ports.

No statistics are systematically compiled in Finland on ste-vedoring companies, forwarding companies or other com-panies operating in ports. It should be noted that the value of network the network of port companies is much more significant than the value generated by the authorities oper-ating the ports, who only are in charge of the port infra-structure and services related to it.

Compiling water traffic statistics is also problematic. No combination statistics that would show the income, expen-diture and staff numbers of shipping companies (including ships operated and time chartered by the companies) are available. However, the FMA does compile the statistics

The Finnish Merchant Fleet. This statistics offers

informa-tion on the Finnish merchant fleet according to ship type, and it also offers information on the amounts of seafarers categorised by type of profession and man-years. It also of-fers reference data concerning the world merchant fleet by country and ship type. According to this statistics, the ca-pacity of the Finnish merchant fleet was greatest in 1981, being 2,478,938 tonnes. In 2001, the gross tonnage was 1,675,964 tonnes. The work input of the seafarers was 9,535 man-years in 2001.

The FMA also publishes statistics on the income from the foreign maritime traffic in Finland, which covers Finnish ships and ships time chartered from abroad including ships owned by Finnish shipping companies, whose financial transactions are handled in Finland. In 2001, the income from the foreign maritime traffic was EUR 1,534 million, of which EUR 1,276 million were earned by Finnish ships and EUR 268 million by ships time chartered from abroad. The traffic of these ships was very much tied to Finland: of the income, EUR 1,264 million was derived from voyages between Finland and other countries and EUR 280 million from traffic between foreign countries.

The traffic expenses of Finnish ships and ships time char-tered from abroad paid abroad were a total of EUR 451 mil-lion in 2001. Of traffic expenses paid abroad by Finnish ships, 60% were passenger ship expenses. The largest ex-pense items were exex-penses related to restaurants and shops (44%), port expenses (25%) and fuel expenses (18%). The largest expense item in traffic expenses paid abroad by

ships time chartered from abroad was time charter pay-ments (83% of all expenses).

What is needed is corresponding information on the inter-national business operations of shipping companies, the ships they have registered abroad and the foreign ships that they operate. Statistics on the labour costs of maritime per-sonnel in different countries would also be valuable infor-mation.

Transport Information

The most important information concerning the Finnish fairways, ports, the merchant navy, maritime companies and personnel and the goods and passenger traffic is com-piled in the Liikennetilastollinen vuosikirja, the statistical yearbook of traffic. This publication also contains informa-tion on the income from water transport handled by the mu-nicipalities and the government and the expenses of water transport. In addition, the statistic offers information on the energy use of water transport and water traffic accidents, and gives a general picture of the carrying capacity, pro-duction, and employment rate of water transport and other forms of transport. This year book is published by Statistics Finland. The FMA is responsible for the section on water transport.

The goods transport statistics offer information concerning the import and export of goods. This information is grouped according to weight by country and by category of goods. Separate information is given for the import and ex-port of cars, container transex-port and transit traffic. The Cus-toms statistics also contain information on imports and ex-ports by different modes of transport. In 2001, the share of maritime transport of all import transportations was 68.2% and of export transports 91.4%. The share of exports is greater because Finland exports large quantities of raw ma-terials for the needs of the industry and energy production from Russia by land. Measured by the value of the goods transported, maritime transports made up 72.5% of the value of import and 70.3% of the value of export trans-ports. The difference in their shares calculated according to weight and value can at least partly be explained by the fact that ships are used to transport goods of low value while goods of high value are transported by air.

Transit traffic through Finland is mostly made up of Rus-sian import and export transports that travel through Fin-land without being cleared through customs as imports to Finland or exports from Finland. Customs has recently be-gun to collect information on the values and contents of these transit transports. In 2002, the value of transit trans-ports was EUR 12 milliard. This value is four times the value of Finnish exports to Russia. Radios, televisions and computers made up over one quarter of the value of trans-ports (EUR 3.5 million). The value of extrans-ports of other ma-chines, equipment and transport devices was almost EUR 2 milliard and the value of chemical industry exports was

slightly over EUR 0.5 million. According to transit statis-tics compiled by Statisstatis-tics Finland, most of the transit transportations through Finland arrive at and leave from ports.

Foreign Trade and Tourism Statistics

Information on the development of foreign trade and tour-ism and the factors explaining this development are impor-tant for maritime transport and traffic. Trade between the Baltic Sea countries has grown extremely fast. The growth of trade flows can, for example, be predicted by using the

gravitation and catching up models. The gravitation model

is based on the knowledge of normal trade levels between the countries in relation to their gross national product per inhabitant, their population and the distance between the countries. In the Soviet times, the trade levels were clearly below the so-called normal level. The gross national prod-uct of countries on the eastern side of the Baltic Sea that now have the liberty to be part of the market economy will grow at a speed that is double to that of the countries on the East side of the Baltic Sea. It is possible to estimate the growth of trade in these countries, as it gradually reaches normal level. After this, the growth prediction can be con-verted into physical transports.

The Finnish Maritime Administration compiles passenger traffic statistics. The port and country of departure and ar-rival and the home country of the passengers are recorded. Information on the home country of the passengers is not published, despite the shipping companies’ enquires. Sta-tistics Finland also gathers information on tourism and publishes the statistics Suomen matkailu (tourism in Fin-land). The information for this statistic publication is col-lected monthly using a random sample of 2,200 people. In 2001, Finns made a total of 2.6 million trips that involved a stay of at least one night abroad. Of the 936,000 short trips taken abroad, (a stay of 1–3 nights) 505,000 were made to Estonia, 163,000 to Sweden and 126,000 to Russia. Of the 1,716,000 long trips abroad (4 nights stay or more), 140,000 were made to Estonia, 129,000 to Sweden and 60,000 to Norway.

Development Needs in the Compilation of Statistics

A fair amount of statistical data exists concerning the mari-time cluster. Good statistics also are available on the Finn-ish merchant fleet, ports and fairways. Particularly good statistics are compiled on the amounts of goods transported (by weight) and of the passenger numbers in passenger traffic.

There are no statistics concerning subcontractor and con-tractor networks, shipping company activities outside Fin-land or companies operating in ports (excluding the ports themselves). In addition, there are no statistics concerning companies that deliver technology for ports and terminals.

Neither are there statistics concerning the numbers of peo-ple working and the amounts of resources used in public offices, in education or research institutions or different as-sociations.

One of the reasons for this situation is the scattered nature of the associations. Small units do not have enough staff to help the authorities with the compilation and editing of sta-tistics. If only the maritime cluster were adequately de-fined, basic information gathered from companies could be modified in co-operation with the officials into very pre-cise maritime cluster statistics.

Experts would be particularly needed to convert the infor-mation into a form that is suitable for the public and to make it available for everyone for example by posting it on the Internet. In addition, there is an obviously lack of Eng-lish language statistics. For instance, when the European maritime cluster study was being conducted, the research-ers had to rely solely on material published in the

Naviga-tor magazine. This information, though solid, was too

lim-ited.

The construction cluster associations resolved the problem of their associations being scattered by regrouping all of them under one umbrella organisation, the Confederation of Finnish Construction Industries RT. The new organisa-tion can effectively gather and publish statistics in graphic form and on the Internet. The Confederation of Finnish Construction Industries RT co-operates with Statistics Fin-land and with the construction technology unit of VTT Technical Research Centre of Finland in producing and de-veloping statistics. RT has also been able to invest in the common technological development of the field supported by Tekes.

2.3 Maritime Cluster Research

Abroad

In this Chapter, maritime cluster studies carried out abroad are presented and their advantages and disadvantages are discussed. In addition, the situation in the Finnish maritime cluster is compared to the situations of the maritime clus-ters in other countries. Studies conducted elsewhere have been used as background to this study.

2.3.1 The Swedish Maritime Cluster Study

The Swedish Maritime Cluster Study has been viewed in light of the following reports that formed the basis for the proposal Den svenska sjöfartspolitiken (the Swedish mari-time policy): Svensk sjöfartsnäring och konkurrenskraften,Kommuner med störst relativ koncentration inom sjöfart-näringen, Svenska rederiers ekonomiska situation, Export av sågade trävaror, Kompetens i sjöfartsnäring, Den svenska

handelsflottan, Sjöfartsmarknaderna, Sjöfartspolitiken i EU, Jämförelse av arbetskraftskostnader i olika fartygsre-gister, Sjöfartens roll i den svenska ekonomin, and “TAP-avtalen”.

The eleven studies mentioned above have been presented on their own and as a whole from the viewpoint of the clus-ter analysis.

Background

Shipping companies (‘rederier’ in Swedish) were selected as the basis for the Swedish maritime cluster study. In the final report, companies that interact closely with the ship-ping companies, thus forming the maritime cluster with them, were described. The definition of the core of the cluster and its network was probably the most important step in cluster analysis. However, the partial reports or the final report do not clarify on a deeper level why any of the supposed interest groups is dependent on shipping compa-nies specifically in Sweden.

When comparing the Swedish and the Finnish approaches, we have to focus our attention on the social approach model used by the Swedes. This model greatly differs from the way the Finns see the cluster. Finnish researchers emphasise, according to Porter’s ideas, that the govern-ment has an impact on the clusters but does not play the main role in the industry or the development of its competi-tiveness. It is the companies that compete on the market, not the nations or the national economies. The role of the government is to create the most favourable operating con-ditions possible for private companies.

The cluster is useful in a situation where the government can not or will not subsidise companies, for example dur-ing times of economic depression. The cluster can help to solve problems, for instance, competition-related that can-not be directly solved by granting subsidies.

Production Factors

The Swedish studies and their summary can also be exam-ined in light of Porter’s diamond model. In this study, the production factors were considered first. It explains the factors of production (i.e. labour, capital) in detail. It is proven in the studies that educational institutes and compa-nies are in close contact with one another. An example of this is the fact that shipbuilding know-how was lost when the Swedish shipbuilding industry disappeared. The ship-building know-how would have been of great importance for the shipping industry in Sweden. The disappearance of technological knowledge that supported the shipping in-dustry in particular, and the subsequent weakening of the shipping industry, were noted in the study.

In the reports focusing on labour, the conclusions are rather one-sided; they almost solely focus on the high price and

the strictly regulated quality of the work. The expensive-ness of the labour input is determined by comparing the wages of employees of the Swedish merchant fleet to those of employees of merchant fleets in other countries. The studies do not clarify why labour is more expensive in Sweden.

Demand

Another cornerstone of the Porter diamond analysis is the demand situation. The Swedish reports show in detail how the demand of different groups of products has influenced the demand for transports by different types of vessels. The Swedish reports discuss in detail the influence of different economic situations on transport demand in the Baltic Sea area and internationally. The derivative nature of the trans-ports or the need for transtrans-ports are not brought up, but the demand for transports is explained by different phenomena such as globalisation. It should also be important to estab-lish how interaction and the benefits it generates have come into being.

If the purpose of the Swedish study concerning demand was to describe the demand in general and not go to the level of individual companies, it can be regarded as quite extensive.

Associated and Supporting fields

The most important task of the maritime cluster is to estab-lish a co-operative network of companies. With the help of this network, innovation and development can be pro-moted in the companies. This is a way to ensure the com-petitiveness of the shipping companies in the country and also to discover the strengths and possibilities of an indi-vidual shipping company. These factors were not really dealt with in the Swedish study, even though they may be seen as a key to solving problems related to international competitiveness in any field of industry using the cluster approach.

Competition

The last part of the diamond cluster in the Swedish studies is the competitive field and competitive strategy. Competi-tion is described in the studies but not analysed further. The descriptions are given to establish how the companies have arrived at the current situation. The reports reveal that the only strategy of the shipping companies has been to adapt to the current situation. No suggestions are given on how the implementation of new technology or long term devel-opment efforts could help to create new markets.

In the section dealing with the timber market, the imple-mentation of container transports between Sweden and Ja-pan is described in detail. This solution is described in a very technical manner. However, it would have been just as essential to establish the Asian way of doing business, but

this matter is only discussed shortly. Knowledge of the Asian business practices could provide the shipping com-panies with new opportunities, but the building of trade re-lations requires, above all, long term confidential inter-communication, which the study refers to in passing.

From the Micro Level to the Macro Level

The problem of the Swedish study seems to have been the summarising of information, which is only partly success-ful. The detailed study results presented in the individual reports have not made their way to the summary report and thus they have also been left out of the document Svenska

sjöfartspolitiken. In addition, the summary seems to

in-clude facts that are not a part of any of the studies and on the other hand, the summary is missing some fundamental observations that have to do with cluster analysis.

As the summary proceeds with the conclusions, the ship-ping companies are forgotten and the report starts discuss-ing the whole maritime cluster. The report moves from mi-cro to mami-cro economics, and solutions to problems on the micro level are forgotten. In the end, a model for a solution is proposed. This model is, however, precisely the model that cluster analysis was originally created as an alternative for.

Summary

The findings of the Swedish cluster study can be summa-rised as follows:

1. As a result of insufficient command of the theory and cluster concepts, only part of the conclusions of the study are correct.

2. The study describes the overall situation very well, but the significance of the individual studies for the cluster remains unclear.

3. There is a conflict between the cluster theory presented and the solutions proposed. (According to the cluster theory, government subsidies endanger healthy petition and companies can only develop through com-petition, whereas according to the Swedish maritime cluster study direct subsidising is proposed as a way to develop the shipping industry.)

4. The cluster-based examination is a good starting point for the examination of structural competitive advan-tages, and it helps in recognising concealed (structural) threats. However, the cluster offers few tools for the building of the future.

2.3.2 The Dutch Maritime Cluster Study

Aim and Structure of the StudyIn the Dutch maritime cluster study, the importance and the structure of the cluster are analysed. The aims of this study are, firstly, to describe the economic importance of the Dutch maritime cluster and to examine the level of

net-working of the maritime sector. The second aim is to estab-lish methods that could be used to encourage the Dutch maritime companies to be more enterprising and to contin-uously create more added value.

The Dutch maritime cluster study included 11 sectors and 11,850 companies. It is probably one of the most complete maritime clusters in the world. The following sectors were taken into account in the study:

1. Shipping 2. Shipbuilding 3. Marine equipment 4. Offshore 5. Inland navigation 6. Dredging 7. Ports 8. Maritime services 9. Fishing 10. Yachting 11. Royal Navy

The Dutch maritime cluster is not only exemplary because of its structure but also because it is very extensive. When the cluster was outlined, it became very important for the Dutch economy.

The Economic Research Results of the Dutch Model

The value of the direct production of the Dutch maritime cluster is about EUR 14.9 milliard. The value added is about EUR 7.8 milliard, which is about 2.5% of the total value added produced in Holland. There are about 137,000 employees in the Dutch maritime cluster.

The largest maritime sectors in terms of production are the port sector (20%), the shipping sector (15%) and the off-shore sector (14%). Together they account for about half of the total output of the maritime cluster. Judging by the value added, the port sector overtakes all other sectors with a result that is 30% of the value added generated by all the sectors included in the maritime cluster. The largest em-ployers are the port sector (19%), the marine industry sec-tor (14%), the offshore secsec-tor (13%) and the inland naviga-tion sector (10%).

However, the impact of the maritime sector extends further than the production, value added and employment within the cluster itself. Complex relationships of the maritime cluster with other clusters make it very important for the Dutch economy. The indirect impacts of the cluster extend to other areas of society as well.

The Dutch study uses input-output analysis to obtain esti-mates of the indirect impacts of the maritime cluster. Data for the study on the cluster’s impact on the whole of the economy was not readily available, so hundreds of

com-pany inquiries were carried out by the Dutch researchers. The input-output tables were created on the basis of these inquiries.

The importance of the Dutch maritime cluster to the whole of the economy is 35% greater than the direct importance measured in terms of production and value added, and al-most 40% greater than the direct importance measured in terms of employment. The total output was an estimated EUR 20 milliard and the value added slightly over EUR 10 milliard. The Dutch maritime cluster employs about 193,000 people.

Especially the shipbuilding, dredging, port and offshore sectors have a notable indirect impact on the economy. For example, the value added indirectly created by the ship-building sector is about 1.3 times greater than the value added directly created by the sector. In addition, the indi-rect impact on employment is clearly more significant than the direct one. The dredging sector also has a very signifi-cant indirect impact on the Dutch economy through em-ployment. However, the port sector is still the most impor-tant one for the economy of the maritime cluster. The sec-tor produces 27% of the total value added of the whole maritime sector. The offshore sector remains the second most important sector with a 14% share of the value added.

Part of the total value added flows back to the government as taxes and social security payments. The backflow is worth about EUR 3.9 milliard. The value added generated by a cluster or a sector is a very interesting measure of its impacts on the national economy. The value added of all the sectors is equal to the gross national product. From the political standpoint, employment and backflow are essen-tial indicators of the state of the national economy. How-ever, for the government it is most important to know what the impact of the income earned in the national economy is.

The cluster analysis carried out in the study shows for ex-ample that the maritime cluster makes investment worth EUR 2.1 milliard each year. Of these investments, 75% are made within the cluster and the rest in other sectors of the Dutch economy. Ships were the largest cost item, worth EUR 0.7 milliard, of the total maritime capital costs. The Dutch maritime cluster added a sum of EUR 2.9 milliard to the total consumption of Holland.

The conclusion of the study is that the maritime cluster is very important for the Dutch economy. In addition to the considerable direct impacts, the indirect impacts that reach far into the Dutch economy have to be considered. The maritime cluster also interacts closely with other sectors. This becomes evident when examining the well-executed basic cluster analysis presented in the study.

In the Dutch study, the economic relations between differ-ent sectors have been explained by terms of mutual

ex-change of goods and services. The overall turnout between different maritime cluster sectors was over EUR 3.3 mil-liard. The most important sectors offering products were the shipbuilding industry subcontractor sector and ship-ping subcontractor sector. Both of these subcontractor sec-tors deliver EUR 0.9 milliard worth of goods, services and capital equipment to other maritime sectors. The most im-portant sectors purchasing goods and services from ship-building and shipping subcontractors were the shipping, inland navigation, dredging, and offshore sectors and the ports. These sectors bought goods and services from the maritime cluster sectors with a total of EUR 2.3 milliard, of which 35% were purchases made by the shipping industry.

The shipping sector, pilotage, the offshore sector, the Navy and the fishing sector had great impact in creating demand in the maritime cluster. This has an important indirect im-pact on the economy of the maritime cluster as well as to the whole economy of Holland. The six sectors mentioned above had an impact of EUR 2.5 milliard on the maritime cluster. Of this EUR 2.5 milliard, 70% stayed in the cluster.

Other Results of the Dutch Maritime Cluster Study

In addition to important economic relationships, other rela-tionships also exist between maritime cluster sectors. These are an object of political interest. Examples of such relationships are strong technological interdependencies, the movement of labour from one cluster sector to another and the physical flow of traffic between inland water routes and ports.

Information collected from companies concerning cost structure, estimates on the value of production, value added, and employment together with the results of the cost analysis make it possible to predict the impact of different policy choices on the maritime cluster. In the end of the study, there is a short overview of the different policy choices. According to the study, the advantage of the Dutch policy is that subsidies granted by the government cannot be easily misused. However, the current policy ignores much of the potential for sustainable growth that exists in the maritime cluster. For example, a more specific mari-time policy would help to make the sector more effective and productive.

The suggestions of the Dutch maritime cluster study are be-ing modified into a cluster based policy. The policy is in-tended to help the companies expand in a sustainable man-ner, which means creating value added, sustaining the cur-rent level of value added and sustaining or increasing the national employment rate. It is evident from the study that the cluster policy is more effective and productive than the current general policy of the government.

2.3.3 The German Maritime Cluster Study

Commissioned by the German Ministry of Transport, the Policy Research Corporation N.V. and the Institute for Shipping Economics and Logistics (ISL) conducted a re-search project on the impact of the maritime sector on the German national economy. They published the report “Economic Impact Study for the German Shipping Sec-tor”, which was part of the European Economic ImpactStudy for the European Shipping Sector. The study was

completed in 1997.

The impact of the German shipping industry on the Ger-man and European economies was established and differ-ent future maritime policy choices for Germany were pro-posed and evaluated in the study. In addition, the impacts of the policy choices on value added, employment and the amount of money flowing back to the public sector were established. Finally, the impact of shipping in Germany on public and private consumption was defined.

2.3.4 The Norwegian Maritime Cluster

Study

In Norway, various studies concerning the maritime cluster have been carried out in the previous years. These studies were conducted to establish the factors that promote the global success of the Norwegian maritime industries and the regional impacts of the maritime cluster. The studies proved the undeniable status of the maritime cluster as one of the central supports of the industry and commerce in the entire country. Unlike other countries, the economic im-portance of the maritime cluster has always been recog-nised in Norway, and the country has strived to take care of the competitiveness of the maritime sector.

Maritime cluster studies have been carried out in Norway on regional and national levels. The factors that are impor-tant for the industries and companies in the maritime sector in Norway in the long run were examined in the Marine

Samfunn study. In this study, the technological, societal,

social and economic factors were examined in addition to factors related to the growth and change of population, the need for labour as well as the availability and placing of la-bour.

According to this study, technological know-how will be strengthened in the future. Fewer people will be employed in the industry, but the employees will have a higher educa-tion level. The increase in product development, new prod-ucts and making use of the new parts of the maritime sector speed up the diversification of the sector. New hygiene and environmental regulations will require substantial invest-ments. In order to develop transports to the market, traffic nodes have to be improved. Because of these develop-ments, more and more companies in Norway will be

spe-cialising in a certain field and merging with other compa-nies. On the other hand, an increase in the differentiation of companies will make it possible for smaller, regionally ac-tive towns to develop.

In their study Kompetanse som internasjonalt

konkurrans-efortinn on the Norwegian maritime sector, professor

Torger Reve and researcher Jorgen Björndahlen have shown that the Norwegian maritime industries have a high status in international competition that is based on solid know-how in the domestic market and on the strength of the companies that actively seek profit. The analysis out-lines the breadth and wide scope of the maritime sector and illustrates the fact that the strong concentration of the Nor-wegian maritime sector is an advantage in international competition. The core of the Norwegian maritime cluster is still in the shipping industry. Co-operation between Nor-wegian shipping companies and the rest of the maritime sector is efficient. This co-operation helps to create innova-tions and commercial competitiveness. The global orienta-tion of the markets is also seen as a strength of the maritime sector.

In the Norwegian maritime cluster study, it was established how the different parts of the maritime sector support each other and how the common origins of the sectors help in promoting co-operation and creating new forms of co-op-eration. Co-operation promotes the competitiveness of companies. The Norwegian shipping companies mostly compete on the international market. It is important for them to be able to offer services to the shipping companies at a competitive price. This would not be possible without co-operation between shipyards and research institutes that have in turn developed and offered new solutions for the market. Technical know-how gives the Norwegian ship-ping companies the advantage of being able to use and de-velop the Norwegian vessel classification system. Co-op-eration helps in developing high level technical know-how, which benefits all the parties involved. Co-operation be-tween shipping companies and experts of marketing, fi-nance, insurance and law is another prerequisite to success.

2.3.5 The Italian Maritime Cluster Study

The Italian maritime cluster study, The Second MaritimeEconomy Report 2002 – The Economic and Employment Impact of the Italian Maritime Cluster covers shipping,

shipbuilding, port operations, fishing, leisure boating, the navy, the coast guard and the port authorities of Italy.

The study shows the important impact that the maritime cluster has on the Italian economy. The Italian maritime cluster is estimated to produce goods and services worth

EUR 26 milliard annually. The maritime cluster directly and indirectly employs 356,000 people. The importance of the maritime cluster is expected to grow in the future.

The Italian study is mostly based on general statistics from Italy. The backgrounds of the statistics and the information are not clarified in the study, and because of this the scope of the cluster presented in the study remains unclear.

2.3.6 The EU Study of the Economic

Impact of Marine Industries

in Europe

Commissioned by the European Commission, the Policy Research Corporation N.V., in co-operation with the Insti-tute for Shipping Economics and Logistics (ISL), con-ducted the Impact of Maritime Industries in Europe study. This study was completed in 2001.

Figures and estimates concerning the European maritime cluster are presented in the study. The cluster is made up of ten independent maritime sectors that are shipping, building, ports, marine equipment, offshore, inland ship-ping, Royal Navy, yachting, fishing, maritime support ser-vices and dredging.

The study comments on the fact that exact figures or stud-ies were not available for all the countrstud-ies. Because of this, the information obtained could not be completely com-bined in the European study. The study only gives superfi-cial basic knowledge of the economic effects. For example, there was no information on the port operators, repair docks or shipbuilding subcontractors in Finland. On the other hand, the information given covers many different fields in all the member countries and Norway. In addition, the researchers had produced estimates to obtain the broad-est possible view when no statistics were available. The re-searchers hoped that the study would stimulate deci-sion-makers to continue the examination of the European maritime cluster and to develop the material available for different sectors.

The conclusion of the study, based on the information gath-ered and the estimates, was that the turnover of the Euro-pean maritime cluster was about EUR 159 milliard in 1997, the value added about EUR 70 milliard and that the cluster employed about 1,545,000 people. The backflow to the public sector in the form of taxes and social security contri-butions was a total of EUR 23 milliard. It was estimated that only some 17% (EUR 12 milliard) of direct value added was spent on goods and services from outside the EU.